- China’s central bank announced a series of policy changes aimed at supporting the ailing economy and reaching the government’s 5% growth target. Chinese & Hong Kong equities have surged on the back of these measures with banking and property stocks the top performing.

- The RBA kept rates unchanged at 4.35% as was unanimously expected. The hawkish tone remained with the board ruling nothing in or out.

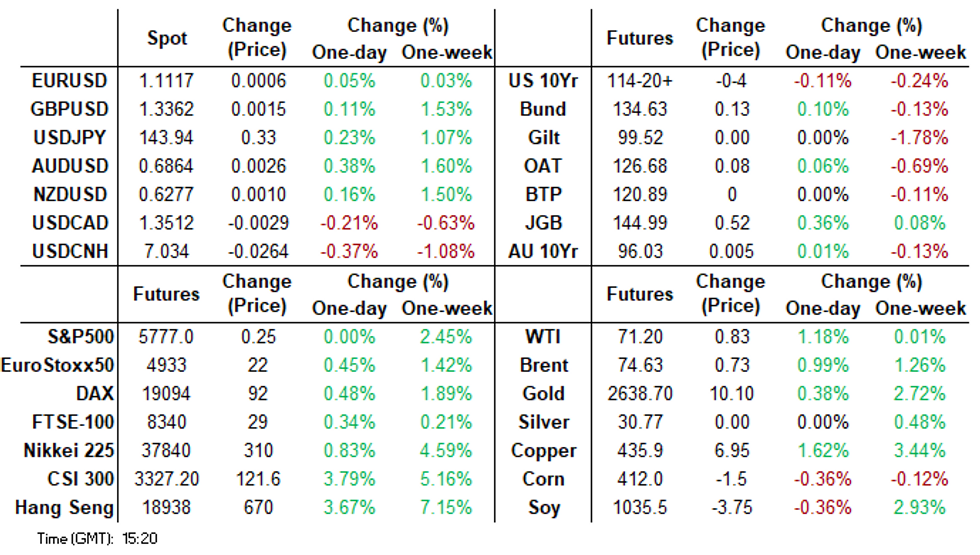

- The USD/JPY is been creeping higher after comments from Ueda repeats the tone from last week when he suggested rates were further away than market may have been expecting.

MARKETS / UP TODAY (TIMES GMT/LOCAL)

US TSYS: Tsys Futures Edges Lower, Curve Steepens, RBA Holds

- Tsys futures are slightly lower today, with the long-end underperforming. Focus in the region today has been on the PBoC market stabilization measures which saw China & Hong Kong Equities rally, while China bond yields continued to tighten with the 10yr hitting 2% for the first time on record, while the RBA as expected kept rates on hold.

- TU is trading -00⅞ at 104-10¼, while TY is -04 at 114-20+.

- JPM CEO Jamie Dimon stated in an interview with the Times of India that there is a possibility interest rates could remain elevated for a prolonged period. He sees less than a 70-80% chance of a soft economic landing, highlighting concerns about global geopolitical tensions and excessive fiscal spending.

- Cash tsys curves bear-steepened, yields are -0.5bps to +1.5bps. The 2yr closed -0.4bps at 3.582%, while the 10yr closed +0.8bps at 3.756%. The 2s10s is +0.989 at 16.989.

- Projected rate cuts into early 2025 rebound, latest vs. this Monday levels (*) as follows: Nov'24 cumulative -38.5bp (-36.5bp), Dec'24 -75.9bp (-72.8bp), Jan'25 -110.0bp (-107.0bp).

- Focus turns to House Price index data including Consumer Confidence and regional Fed mfg data. US Tsy to auction $69B 2Y notes as well as $60B 42D CMB bills.

JGBS: Solid Rally In Cash Bonds, PPI Services Data Tomorrow

JGB futures are sharply stronger but off session highs, +50 compared to the settlement levels, after trading resumed after yesterday’s holiday.

- Outside of the previously outlined Jibun Bank Flash PMIs, there hasn't been much by way of domestic drivers to flag.

- Today’s Enhanced Liquidity Auction covering 1-5-year OTR JGBs accepted JPY499.5bn of bonds, with an average accepted spread of -0.043 and a bid/cover ratio of 3.81x.

- "Bank of Japan watchers are keeping a close eye on the leadership election of the nation’s ruling Liberal Democratic Party for potential monetary policy implications, with attention focused on a strong advocate of maintaining an easing stance." (See BBG link)

- Cash US tsys are flat to 1bp cheaper in today’s Asia-Pac session. Today’s US calendar will see the House Price Index, Consumer Confidence and Regional Fed Mfg data.

- Cash JGBs are mostly richer across benchmarks beyond the 1-year (+2.3bps), with 2-year to 20-year yields 2-4bps lower.

- The swaps curve has twist-steepened, with yields 3bps lower to 5bps higher. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see PPI Services data alongside BoJ Rinban Operations covering 1- to 25-year JGBs and Inflation-Indexed Bonds.

ACGBS: Little Changed After RBA Leaves Cash Rate At 4.35%

ACGBs (YM +1.0 & XM flat) are slightly stronger but little changed after the RBA decided to keep the cash rate at 4.35%, as unanimously expected. The RBA Board noted:

- While inflation has fallen since its 2022 peak, it remains above the 2–3% target range and is not expected to return to target until 2026. However, longer-term CPI expectations remain consistent with the target.

- Wage pressures have eased, but labour productivity remains low.

- The Board's priority is to bring inflation back to target sustainably, remaining cautious about potential risks. Future decisions will be based on data and evolving economic conditions, both domestically and globally.

- Cash ACGBs are 1bp richer with the AU-US 10-year yield differential at +20bps.

- Swap rates are 1-2bps lower.

- The bills strip has twist-flattened, with pricing -1 to +2.

- RBA-dated OIS pricing is 1-2bps firmer after the decision. A cumulative 14bps of easing is priced by year-end.

- August CPI is released tomorrow with the headline forecast to moderate to 2.7% from 3.5% driven by federal government electricity subsidies. As a result, the trimmed mean will be the focus and was at 3.8% in July.

- Tomorrow, the AOFM plans to sell A$1.bn of the 3.75% 21 May 2034 bond.

NZGBS: Bull-Steepener, Light Local Calendar, Subdued Session

NZGB curve bull-steepened, with yields closing flat to 3bps lower. The market also closed at the session’s best levels. With the local market closed at the time of today’s RBA Policy Decision, any spillover will come early in tomorrow’s session.

- With the domestic calendar light today, the local market largely tracked developments in its $-bloc counterparts. The NZ-US and NZ-AU 10-year yield differentials finished ~1bp tighter.

- Cash US tsys are flat to 1bp cheaper in today’s Asia-Pac session. Today’s US calendar will see the House Price Index, Consumer Confidence and Regional Fed Mfg data.

- Swap rates closed flat to 2bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 1-2bps softer across meetings. A cumulative 85bps of easing is priced by year-end.

- Tomorrow, the local calendar is once again empty.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 3.00% Apr-29 bond, NZ$225mn of the 4.50% May-35 bond and NZ$25mn of the 2.75% Apr-37 bond.

OIL: Crude Jumps On Hopes China Stimulus Will Boost Demand

Oil prices have jumped after the PBoC announced numerous measures to stimulate China’s economy. WTI is up 1% to $71.08/bbl, close to the intraday high, after a low of $70.44 before the news. Brent rose 0.9% to $74.55/bbl after a low of $73.95. The market also remains nervous regarding an escalation the situation between Israel and Hezbollah, which is likely to be discussed by the UN today. The USD index is little changed.

- The PBoC announced a 20bp cut in the 7-day repo to 1.5% and 25bp for mortgage rates, as well as a 25bp reduction in the RRR with possibly another 25-50bp before year end depending on conditions. There are also measures to support China’s equity market and stabilise bonds. There has been concern it wouldn’t meet its 5% growth target, which had spooked crude.

- China will continue to be monitored closely, but now for signs that the monetary stimulus is having an effect on demand.

- Israel attacked Hezbollah targets in Lebanon on Monday, while Iran said that it is prepared to intervene to de-escalate the worsening situation as long as Israel does too.

- US industry-based inventory data is published today. There have been significant stock drawdowns recently but also signs that product demand is easing.

- Later the Fed’s Bowman speaks and US July housing data, September consumer confidence, Philly & Richmond Fed indices print. There’s also September German Ifo.

GOLD: Pushes Higher With Middle East Tensions & Fedspeak

Gold is 0.2% higher in today’s Asia-Pac session, after closing with a similar sized gain yesterday. Earlier in today’s session bullion reached another all-time high at $2,635.

- Fed speakers overnight indicated more cuts are in the future. However, comments suggested there is a high bar for an additional 50bps cut this year. Lower rates are typically positive for gold, which doesn’t pay interest.

- The yellow metal also likely received support from increased tensions in the Middle East.

- According to MNI’s technicals team, a bullish structure is still in place for gold. Focus is on $2,642.7 next, a Fibonacci projection.

- In contrast, silver fell by ~1.5%. The recent break of key short-term resistance at $30.192, the Aug 26 high, signals scope for an extension towards $31.754, the Jul 11 high. Key short-term support has been defined at $27.686, the Sep 6 low.

ASIA STOCKS: Asian Equities Mostly Higher, Supported By PBoC Stabilization

Asian markets are broadly positive as China’s recent stimulus measures aimed at boosting the economy lifted investor sentiment. Chinese property stocks surged after the government announced cuts to mortgage rates and down-payment requirements for second homes, although the market remain cautious on whether this will fully revive the housing market.

- The PBoC efforts to stimulate the economy, including allowing brokerages and funds access to central bank funding for stock purchases, further contributed to a 0.7% rise in the MSCI Asia Pacific Index. Additionally, China’s 10-year bond yield fell to a record low of 2%, signaling ongoing government support for both equity and bond markets.

- Hong Kong equities have surged with the HSI +3.73%, banks lead the way with the Mainland Banking Index +5.38% The HSTech Index is +4.80%, while Mainland Property Index is +4.80%. Chinese equities are also much higher with the CSI 300 +3.50%.

- Japanese equities opened higher, however has slowly given back some of the morning gains. The yen weakened to 143.86, providing further support to exporters, after BoJ Gov Ueda signaled that the central bank is not in a rush to raise interest rates following hikes earlier in the year, he is also scheduled to speak a bit later today. The Topix is 0.75% higher, while the Nikkei is 080% higher.

- Taiwan equities are little changed today, while South Korea's KOSPI is now trading 0.90% higher after spending most the day little changed. Foreign investors have continued selling local equities with majority of outflows coming from the tech space today.

- Australia stocks have seen little reaction to the RBA keeping rates on hold with the ASX200 trading 0.16% lower

ASIA STOCKS: Inflows Into Indonesia & Philippines Equities Continue

Indonesia has now seen 18 straight days of inflows, Philippines 16 days while India saw its largest inflow since Nov 2021 on Friday.

- South Korea: Saw outflows of $552m yesterday, with the past 5 sessions reaching -$1.68b, while YTD flows are +$11.34b. The 5-day average is -$336m, below both the 20-day average of -$329m and the 100-day average of -$23m.

- Taiwan: Saw inflows of $316m yesterday, with the past 5 sessions netting +$1.33b, while YTD flows are -$13.31b. The 5-day average is +$265m, above the 20-day average of -$276m but below the 100-day average of -$132m.

- India: Saw inflows of $1.82b Friday, with the past 5 sessions netting +$3.46b, while YTD flows are +$23.74b. The 5-day average is +$629m, above both the 20-day average of +$455m and the 100-day average of +$105m.

- Indonesia: Saw inflows of $81m yesterday, with the past 5 sessions netting +$390m, while YTD flows are +$3.76b. The 5-day average is +$78m, above both the 20-day average of +$145m and the 100-day average of +$30m.

- Thailand: Saw inflows of $13m yesterday, with the past 5 sessions totaling +$180m, while YTD flows are -$2.52b. The 5-day average is +$36m, below the 20-day average of +$48m but above the 100-day average of -$7m.

- Malaysia: Saw outflows of $28m yesterday, with the past 5 sessions netting +$36m, while YTD flows are +$966m. The 5-day average is +$7m, below both the 20-day average of +$31m and the 100-day average of +$16m.

- Philippines: Saw inflows of $32m yesterday, with the past 5 sessions totaling +$113m, while YTD flows are -$138m. The 5-day average is +$23m, above both the 20-day average of +$11m and the 100-day average of -$2m.

Table 1: EM Asia Equity Flows

FOREX: Risk-Sensitive Currencies Outperform On China Stimulus News

Risk-sensitive currencies outperformed today driven by China’s announcement of numerous stimulus measures and support for the equity and bond markets, which also boosted share and commodity prices. The USD index is little changed.

- AUDUSD is up 0.3% to 0.6860 after a high of 0.6861 reached on the RBA decision. It fell to 0.6826 before the PBoC announcement but has traded above key resistance at 0.6824 through the session, which if sustained will confirm the resumption of the bull cycle.

- The RBA left rates at 4.35%, as expected, and remains “vigilant” to upside inflation risks. There was some volatility around the announcement with AUDUSD slightly higher.

- NOK and CAD are the other outperformers with USDNOK down 0.3% to 10.461 and USDCAD -0.2% to 1.3516.

- Kiwi has not performed as well with NZDUSD little changed at 0.6270 but AUDNZD is up 0.3% to 1.0939. The pair reached 1.0936 following the China news.

- USDJPY has range traded through the session and is currently up 0.2% to 143.81 after a high of 143.91 followed by falling to a low of 143.38 when PBoC stimulus was announced.

- The euro and pound are slightly stronger against the greenback at 1.1116 and 1.3356 respectively. The ECB’s Lagarde said that the inflation fight was not yet quite won.

- Later the Fed’s Bowman speaks and US July housing data, September consumer confidence, Philly & Richmond Fed indices print. There’s also September German Ifo.

RBA: RBA On Hold, Remains “Vigilant”, Nothing Ruled "In or Out"

The RBA kept rates unchanged at 4.35% as was unanimously expected. The hawkish hold tone was maintained with the key changes in the September statement only updates for the data released since the August meeting. Expect Governor Bullock to reiterate in the upcoming press conference at 1530 AEST not to expect easing in the “near term”.

- There was greater emphasis on the temporary nature of the current decline in headline inflation. The RBA noted that “underlying inflation is more indicative of inflation momentum”. Underlying inflation is not expected to “sustainably” return to target until 2026.

- Inflation “remains too high” and the Board will continue to be “vigilant to upside risks to inflation”, while “not ruling anything in or out”. As a result, rates will need to stay “sufficiently restrictive until the Board is confident that inflation is moving sustainably towards” target.

- The statement included more details on the labour market than usual. It said that it is tight and there are “some signs of gradual easing” but observed the stabilisation in hours worked, a record high participation rate and elevated vacancies.

- The board acknowledged the “weak” Q2 GDP/consumption outcome but said that spending by tourists and students was more resilient than residents who had cut back on discretionary spending due to previous declines in real disposable income and higher rates.

- Uncertainties around the outlook persist, especially from overseas, and risks in both directions around consumption were discussed.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 24/09/2024 | 0800/1000 | *** |  DE DE | IFO Business Climate Index |

| 24/09/2024 | 0900/1000 | * |  GB GB | Index Linked Gilt Outright Auction Result |

| 24/09/2024 | 1230/0830 | ** |  US US | Philadelphia Fed Nonmanufacturing Index |

| 24/09/2024 | 1255/0855 | ** | US | Redbook Retail Sales Index |

| 24/09/2024 | 1300/0900 | ** | US | S&P Case-Shiller Home Price Index |

| 24/09/2024 | 1300/0900 | ** | US | FHFA Home Price Index |

| 24/09/2024 | 1300/1500 | ** |  BE BE | BNB Business Sentiment |

| 24/09/2024 | 1400/1000 | *** | US | Conference Board Consumer Confidence |

| 24/09/2024 | 1400/1000 | ** | US | Richmond Fed Survey |

| 24/09/2024 | 1530/1130 | * | US | US Treasury Auction Result for Cash Management Bill |

| 24/09/2024 | 1700/1300 | * | US | US Treasury Auction Result for 2 Year Note |

| 24/09/2024 | 1710/1310 |  CA CA | BOC Governor Macklem fireside chat on "Growth During Uncertainty" | |

| 24/09/2024 | 2210/1810 | US | New York Fed's Roberto Perli |