Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

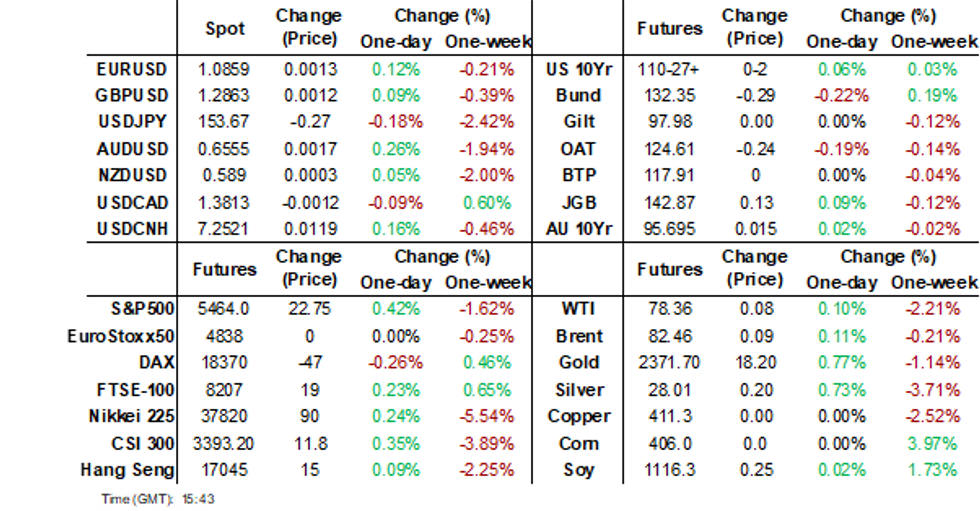

- Today saw some consolidation emerge after what has been a volatile week. The USD was slightly softer, with moves aided by higher US equity futures and some pick up in commodity prices.

- US Treasury futures are little changed today, with investors awaiting today's data, in particular core PCE. JGB futures are higher, after a solid 2yr auction, while Tokyo CPI was mixed ahead of next week's BoJ meeting.

- In Singapore, the MAS left policy settings on hold as widely expected.

- Outside of the PCE inflation print we also have the U. of Mich. Sentiment later.

MARKETS

US TSYS: Tsys Futures Steady Ahead Of PCE Later

- Treasury futures are little changed today, with investors awaiting today's data in particular core PCE, while personal income and spending, U. of Mich. Sentiment will also closely watched. TUU4 is unchanged at 102-16+, while TYU4 is + 01+ at 110-27.

- Volumes were on the low side today, there was a block buyer of 2,900 FV earlier.

- Cash treasury curve is little changed today, yields are about 0.5bps higher, with the 10Y at 4.243%

- The 2s10s reached it's least inverted level for the year overnight, although we now trade off those levels down 8bps at -19bps.

- (Bloomberg) PREVIEW: June PCE to Show Stretched Consumers, Soft Inflation - See link

- US futures are currently fully pricing in a cut in September, with cumulative 66bps of cuts in year-end.

JGBS: Futures Holding Higher, Solid 2yr Auction, BoJ Next Week

JGB futures are holding positive, but have been unable to breach the 143.00 handle. We were last 142.88 for JBU4, +.14 versus settlement levels.

- This leaves us towards the upper end of the trading range for the past few sessions.

- We had a solid 2yr auction result earlier. The bid to cover was 4.19, versus the prior 3.83, while the tail was 0.007 compared to 0.008 prior.

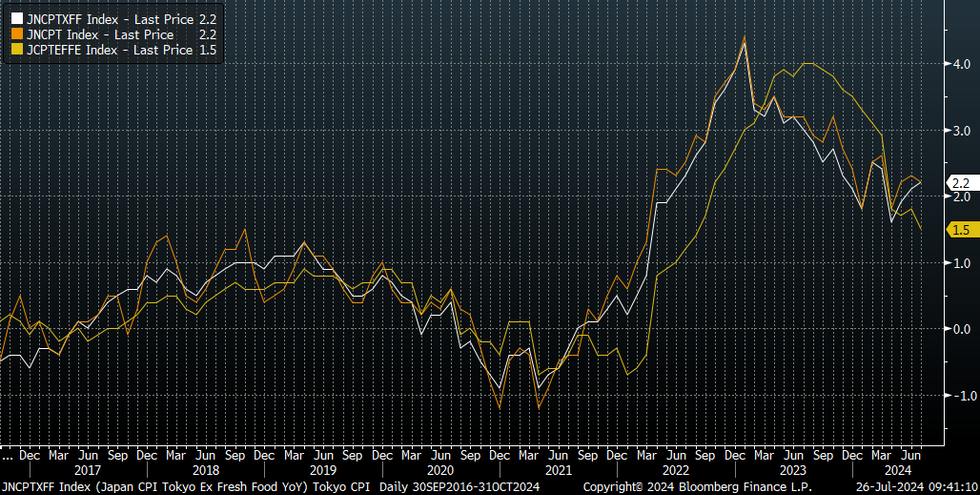

- Earlier the July Tokyo CPI update was mixed. Headline and the core ex fresh food trend remained above 2% y/y but core-core, which also excludes energy fell to 1.5%. Still, if history is a guide this core-core measure should follow the other headline metrics firmer in coming months.

- In the cash JGB space, we are mostly lower in yield terms, particularly towards the back end of the curve, off a little over 2bps for the 20-40yr tenors. The 10yr JGB yield remains under 1.06%. The 10yr swap rate is off 2bps to sub 0.98%.

- Looking ahead, next week's BoJ meeting outcome (on Wednesday) will be the key focus point. The broader consensus rests with no change at this stage, although reports this week (including from Reuters) have suggested the central bank is still considering a rate hike. The other focus point will be central bank's planned reduction in bond purchases.

JAPAN DATA: Tokyo CPI Slightly Below Expectation, Headline Above 2% Y/Y

Japan's July Tokyo CPI print was a little below forecasts. Headline 2.2% y/y (2.3% was forecast), ex fresh food as expected at 2.2%, while ex fresh food and energy was 1.5%y/y (1.6% forecast and 1.8% prior).

- The chart below plots the three metrics, with the core ex fresh food and energy in yellow. In recent years this metric has tended to lag the other two measures. Headline and core (ex fresh food) have had an average around 2% y/y since the start of this year.

- In m/m terms, headline was up 0.1% (versus 0.3% prior). the ex fresh food measure was 0.3% similar to the pace of the past two months. Good prices rose 0.3%, services were flat. In y/y terms services eased to 0.5% from 0.9% in June.

- By category, food and fresh food prices fell. Housing, utilities and household goods saw lower m/m outcomes compared to June. Clothing fell -1.0%m/m, while the strongest rise in m/m terms was entertainment at +1.3%, reversing the prior month's dip. Y/Y trends were mixed. Utilities up +12.6%y/y, but education a drag at -9.2%y/y.

- On balance, the data isn't likely to shift BoJ thinking greatly ahead of next week's meeting. CPI is close to the BoJ's target, but services price pressures are by no means painting a hawkish picture at this stage.

Fig 1: Tokyo CPI July Trends Mixed

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: ACGB Curve Flattens, OIS Slightly Firmer Into Year-End

ACGBs (YM +1 & XM +1.5) are richer today with what was a subdued trading session with little int he way of domestic drivers or data, as a results moves were largely tied to US tsys.

- The ACGB curve has bull-flattened today, yields are 1-4bps lower, with the 10Y back below 4.30% for the first time this week.

- The AU-US 10-year yield differential little changed today at+5bps.

- The swap curve has bull-flattened with yields +/- 2bps

- The bills strip has flattened, trading flat to +2.

- RBA-dated OIS pricing is a pricing 1-2bps firmer heading into year-end, with the first full cut not priced in until July 2025

- Cross assets: Equities were higher today, led by financials & miners with commodity prices higher, the AUD was the top performing G10 currency after falling over 2% this week as the yen carry trade was unwound.

- Looking ahead to next week, focus will be on Retail Sales & CPI on Wednesday.

NZGBS: NZGB Curve Flattens Tracking US Tsys, NZ Consumer Confidence Jumps

The NZGB curve flattened today, with better buying through the 5-10yr part of the curve, the 10y yield dropped 5bps to 4.356%. There was little in the way of domestic drivers today, yields finished towards session's best, with equities finding some support.

- NZ consumer confidence increased in July, with the index rising to 87.9. This boost in confidence comes amid expectations of significant interest-rate cuts over the next year. Inflation expectations fell to 3.7%, the lowest since September 2020.

- The RBNZ is anticipated to start cutting rates soon due to falling inflation, rising unemployment, and a weak economy.

- RBNZ dated OIS pricing closed relatively stable out to year end today, but soften 2-7bps for 2025 meetings

- On a relative basis, the NZ-US and NZ-AU 10-year yield differentials continue to hover around their lowest levels since late 2022 at +11bps and +7bps respectively.

- The 2s10s swaps curve has bull-steepened, with rates 2 to 5bps lower.

- A 66% chance of a rate cut in August is currently priced in, with a cumulative 84.5% chance of a cut by October, before expectations jump sharply to three 25 bps cuts by year-end.

- Next week data is light on with just Building Permits & ANZ Business Confidence on Wednesday

ASIA PAC STOCKS: Asian Equities Find Support As Investors Weigh up Strong US GDP Data

Asian equities are mostly higher today, as investors weigh up strong US GDP data with firming chances of a US rate cut in September while awaiting US PCE and Personal Spending & Income due later today. South Korean equities are the top performers, led higher by major tech stocks, Japanese equities have seesawed ahead of the BoJs meeting next week and Taiwan returned after heavy Typhoons hit with the market playing catch up. Locally we have had Tokyo CPI which came in just below estimates.

- Japanese equities equities have fluctuated today although all major benchmarks now trade higher, the market is awaiting the BoJ meeting next week, while the USDJPY has held steady today trading in a tight range. bank stocks are the top performers today with the Topix Bank Index up 1%, while the border Topix is 0.20% higher while the Nikkei has erased earlier gains and now trade flat.

- China & Hong Kong equities were little changed today, Chinese small-cap were the top performers with the CSI 1000 & 2000 up about 1.50%, elsewhere major benchmarks are largely flat with the GSI 300 up 0.8% and the HSI up 0.10%. Headlines out of the region light on today.

- South Korean equities are higher today, although foreign investors have been net sellers of local stocks with rotation out of tech and into financials occurring. SK Hynix, up 1.50% has contributed most to the index gains. Kospi is 0.80% higher, while the Kosdaq is 0.10% higher.

- Taiwan equity markets have returned after strong Typhoons hit the island, with the Taiex falling about 4% on the open, we have since seen some recovery and now trade down 3.30%. Semiconductors have been hit hard over the past week or so with the Philadelphia SE Semiconductor Index down 8% over the past 5 sessions.

- Australian equities higher today, driven by a rebound in mining with Iron Ore 2.15% higher and firm financial stocks, the ASX200 is 0.75% higher. Next week focus will turn to Retail Sales and CPI on Wednesday. The NZX 50 has largely missed the weeks sell-off and trades up 0.70% for the week after large jump higher in three stocks, currently the index is unchanged for the day.

- In EM Asia markets are mixed with Malaysia's KLCI down 0.10%, Singapore's Strait Times is 1.15% lower, while Indonesia's JCI is 0.50% higher, Philippine's PSEi is 0.65% higher, India's Nifty 50 is 0.80% higher.

ASIA EQUITY FLOWS: Foreign Investors Continue Selling Local Tech Stocks

- South Korea: South Korean equities saw outflows of $592m yesterday, contributing to a net outflow of $1.056b over the past five trading days, the Kospi is down 2.58% over the same period with major Tech names such as Samsung (-4.74%) & SK Hynix (-9.31%) contributing the most to the sell off. The 5-day average outflow is $211m, compared to the 20-day average inflow of $55m and the 100-day average inflow of $100m. Year-to-date, South Korea has experienced substantial inflows totaling $18.157b.

- Taiwan: The local market was closed Wednesday &Thursday due to a Typhoon, expect heavy selling to resume once the market reopens after the Philadelphia SE Semiconductor Index has fallen 7.34% during the Typhoon outage and now off 15.59% from all time highs made on July 7th. The 5-day average outflow is $901m, higher than the 20-day average outflow of $380m and the 100-day average outflow of $77m. Year-to-date, Taiwan has experienced outflows totaling $2.855b.

- India: Indian equities saw outflows of $419m yesterday, flows have almost entirely been positive since the Indian Elections the past 5-days have seen an inflow of $1.216b. The 5-day average inflow is $243m, slightly below the 20-day average inflow of $270m and significantly higher than the 100-day average outflow of $48m. Year-to-date, India has experienced inflows totaling $4.458b.

- Indonesia: Indonesian equities recorded inflows of $24m yesterday, leading to a net inflow of $2m over the past five trading days, flows have been mixed recently with no trend emerging. The 5-day average is $0m, below the 20-day average inflow of $10m and close to the 100-day average outflow of $11m. Year-to-date, Indonesia has experienced outflows totaling $125m.

- Thailand: Thailand saw an outflow of $6m yesterday, resulting in a net inflow of $50m over the past five trading days with the SET down 2.50% over the same period. The 5-day average inflow is $10m, better than the 20-day average outflow of $10m and the 100-day average outflow of $27m. Year-to-date, Thailand has seen significant outflows amounting to $3.285b.

- Malaysia: Malaysian equities experienced outflows of $80m yesterday the largest outflow since May 31st, contributing to a 5-day net outflow of $67m. The 5-day average outflow is $13m, lower than the 20-day average inflow of $11m and the 100-day average outflow of $4m. Year-to-date, Malaysia has experienced inflows totaling $85m.

- Philippines: The Philippines saw outflows of $4m yesterday, resulting in a net inflow of $53m over the past five trading days. The 5-day average inflow is $11m, better than the 20-day average inflow of $4m and the 100-day average outflow of $6m. Year-to-date, the Philippines has seen outflows totaling $449m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -592 | -1056 | 18157 |

| Taiwan (USDmn)** | 290 | -4506 | -2855 |

| India (USDmn)* | -419 | 1216 | 4458 |

| Indonesia (USDmn) | 24 | 2 | -125 |

| Thailand (USDmn) | -6 | 50 | -3285 |

| Malaysia (USDmn) | -80 | -67 | 85 |

| Philippines (USDmn) | -4 | 53 | -449 |

| Total | -786 | -4308 | 15986 |

| * Up to 24th July | |||

| ** Closed due to Typhoon |

FOREX: AUD & JPY Marginally Higher, Amid Tight Ranges, US PCE Coming Up

The BBDXY USD index is marginally down for the first part of Friday trade, last 1256.5. All of the majors are up against the dollar, with JPY and AUD outperforming at the margins.

- USD/JPY hasn't spent too much time out of the 153.50-154.00 range, with an option expiry at 154.00 strike (for NY cut later) potentially influence spot. Yen remains comfortably the best performer in the G10 space in the past week.

- Risk off in the equity space, slumping metal prices (which has contributed to AUD/JPY losses) along with Fed expectations have all aided the yen.

- Post Thursday's Q2 GDP beat we did see front end Tsy yields stabilize somewhat. This comes ahead of this evening's US PCE inflation print.

- This may be leaving market participants somewhat on the sidelines, particularly after the volatility this week.

- The Tokyo July CPI print was mixed, although is unlikely to shift BoJ thinking greatly.

- AUD/USD has firmed back to 0.6550, aided at the margin by a better tone to copper and iron ore prices, although we sit away from best levels. China equity sentiment has mostly seen upticks sold as well.

- NZD/USD has lagged the A$, the pair last near 0.5890. The ANZ consumer sentiment measure rebounded but this reflected easing rate expectations.

- US equity futures are tracking higher, lending some support to higher beta plays, although they aren't outperforming the JPY at this stage. US yields are close to flat.

- Outside of the US PCE print, the Friday calendar is light.

OIL: Brent Close To Flat For The Week, US GDP Beat Helps Rebound From Lows

Brent Crude prices continued to oscillate with the ongoing policy announcements from China.

- Recognizing that the announced stimulus measures reflect the ongoing challenges but are aimed at arresting them, saw Brent Crude pair back some of the intra week lows to finish flat on the week.

- Brent Crude was trading at $82.53 intraday in Asian time, trapped in a very tight trading range. This is unsurprising given the push pull in financial markets of China policy and the outlook from the FED.

- Brent Crude has held onto modest overall gains year to date though these are attributed more to OPEC output guidance, than the outlook for global growth. Last night’s surprise US GDP print likely contributed to the modest bounce back in price.

- During the week it was reported that projected overall oil-product consumption may fall in China in the second half of the year, reflective of the overall outlook

- for growth.

- WTI however had a somewhat softer week, falling to $78.43 during the morning

- following last week’s close of $80.13.

GOLD: Holding Lower For The Week, All Eyes On The Fed

Gold continued to trend lower this week, given the various stimulus measures announced out of China and last nights better than expected US GDP.

- Touching a low of $2,355.9 in Asian trading, prices appeared to stabilize at these levels as hopes of a near term rate cut from the FED appeared to dissipate. We were last near $2372.5.

- Despite the softer week, GOLD has enjoyed a strong year with prices up 13% year to date. The outlook for GOLD in the near term is hitched firmly to that of the FED.

- Market’s have priced in a September cut and earlier in the week a column from a Bloomberg columnist and former FED member Bill Dudley brought the FED’s

- upcoming meeting next week.

- The stronger than expected GDP has likely meant the next FED meeting may no longer be ‘live’, however tonight the Personal Consumption Expenditure’s index (a measure preferred by the FED as an underlying measure on inflation) now becomes a significant data release.

CHINA: China Stimulus To Push Move To Cleaner Technologies

CNY300bn of Stimulus to Revitalize Industrial Machinery and Incentivize Households to Invest in cleaner technology.

- Long dated Chinese government bonds will be issued to fund an initiative to replenish industrial and household equipment.

- With a focus on cleaner technologies this stimulus is seen as directly targeting China’s booming EV industry

- Subsidies for EV manufacturers will be complemented by local government incentives for households to trade in their vehicles for upgrades, and support demand for EV’s and EV manufacturers

- In an environment where the potential front runner for the White House sees EV’s as a ‘Green Scam’ and suggests that they will completely obliterate the US automotive industry, this program comes at an interesting juncture .

- To add to this, a 15% subsidy will be included for purchases of energy efficient household appliances.

CNH: Cross Asset Trends Still Point To USD/CNH Dips Being Supported

USD/CNH has been supported on dips in the first part of Friday trade, albeit with some degree of volatility. Earlier lows were at 7.2335, but we sit back at 7.2560 in latest dealings around session highs. The earlier dip came after a strong onshore spot open. USD/CNY spot got to 7.2293, but now sits higher at 7.2465/70, little changed for the session.

- Cross asset moves still point to yuan headwinds. Headlines have crossed of the 10yr CGB bond yield hitting a fresh record low (per BBG), now sub 2.20%.

- This is keeping US-CH yield differentials close to recent highs, despite Fed easing expectations. 2yr +292bps, the 10yr at +206bps.

- On the equity side, fresh rounds of stimulus aren't providing meaningful gains at this stage. The CSI 300 is close to multi month lows getting back to February. Additionally, the China to Global equity ratio has remained depressed, despite some sharp falls in global equities this past week.

- Tomorrow we get June industrial profits but greater focus will rest on Wednesday's July PMI outcomes. Market expectations for 2024 GDP growth are under 5% (albeit up from earlier 2024 lows). This week's flash PMI readings on the manufacturing side for other major economies have generally been softer.

- For USD/CNH, yen trends will obviously be important, with next week's BoJ meeting coming into focus.

- Levels wise, Thursday intra-session lows were 7.2032, while current levels are close to the 100-day EMA. The 50-day is higher at 7.2724.

SINGAPORE: MAS On Hold As Expected, USD/SGD Little Changed

The MAS left its policy settings unchanged. The central bank maintained the current pace of SGD NEER appreciation, while the width and the level at which the band is centered were also left unchanged. This was as expected per the market consensus.

- The inflation outlook is likely to be key in terms of a potential MAS easing at some stage in the future.

- The central bank, in its accompanying statement noted: "MAS Core Inflation is expected to step down more discernibly in Q4 this year and into 2025. For 2024 as a whole, MAS Core Inflation is expected to average 2.5–3.5%."

- Headline CPI is now projected at an average of 2.5% for this year, down from the previous forecast 3.0%. This reflects lower than expected private transport costs.

- Inflation risks are balanced. Upside risks rest with any positive domestic demand surprises and geopolitical risks, while downside pressures may come from a weaker global backdrop if interest rates are held higher longer than anticipated.

- Importantly the MAS stated: "The prevailing rate of appreciation of the policy band will keep a restraining effect on imported inflation as well as domestic cost pressures, and ensure medium-term price stability."

- Any easing may not be forthcoming until further signs of core inflation moving towards or at 2%y/y.

- On the growth side, the MAS noted: ""Growth momentum in the Singapore economy should improve in the second half of 2024. GDP growth is likely to come in closer to its potential rate of 2–3% for the full year. "

- USD/SGD is little changed post the result, last near 1.3425/30, down slightly as broader USD sentiment has softened. the SGD NEER (per the Goldman Sachs estimate) is slightly higher at -0.38% from the top end of the policy band (we ended Thursday trade at -0.43%).

ASIA RATES: Front End Rates Mostly Skewed Lower This Week

INDIA

- In a week dominated by the new budget, it was easy to miss the analysis showing the benefit of India’s inclusion in the JPMorgan index recently

- Long dated demand from overseas investors (according to The Clearing Corporation of India showed that the maturity of over 20% of foreign investors holdings were in excess of 10 years, per BBG).

- The addition of India into the benchmark is timely given the recent budget committing to continued fiscal targets and voices within the Central Banks entertaining the idea of cuts.

- As with other Central Banks globally, the Indian Central Bank’s decision makers will be considering their next moves in the context of FED moves

- Bonds performed well across the curve today as yields finished lower on the week

2yr 6.762 (-4bp) 6.856% (-2bp) 6.943% (-1bp) 7.027% (-0.5bp)

INDONESIA

- In the absence of key data releases the Indonesian market took guidance from good demand for new issues and regional expectations for rate cuts.

- New issues drew up to 4 times demand for the new securities issued in 2029, 2034, 2043 and 2054 maturities

- Yields finished lower for the week across shorter dated maturities with intermediate to longer dated securities finishing flat to marginally higher due to issuance.

2yr 6.762% (-4bp) 5yr 6.856% (-2bp) 10yr 6.943% (-1bp) 30yr 7.027% (-0.5bp)

SOUTH KOREA

- The week was dominated by weaker than expected data pushing investors to position for rate cuts.

- This puts the BOK in an interesting position ahead any moves by the FED and property prices in Seoul rising more than expected.

- Bond yields followed regional trends with most maturities finishing the day lower with the exception of 3-5 year maturities, following KRW1.1tn of issuance.

2yr 3.107% (-1.5bp) 5yr 3.087% (+3bp) 10yr 3.119% (-1bp) 30yr 3.00% (-0.5bp)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/07/2024 | 0600/0800 | ** |  | SE | Unemployment |

| 26/07/2024 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 26/07/2024 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 26/07/2024 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 26/07/2024 | 0800/1000 | ** |  | EU | ECB Consumer Expectations Survey |

| 26/07/2024 | - | | EU | ECB's Cipollone at Rio de Janeiro G20 Fin min/central bank meeting | |

| 26/07/2024 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 26/07/2024 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 26/07/2024 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 26/07/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.