Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

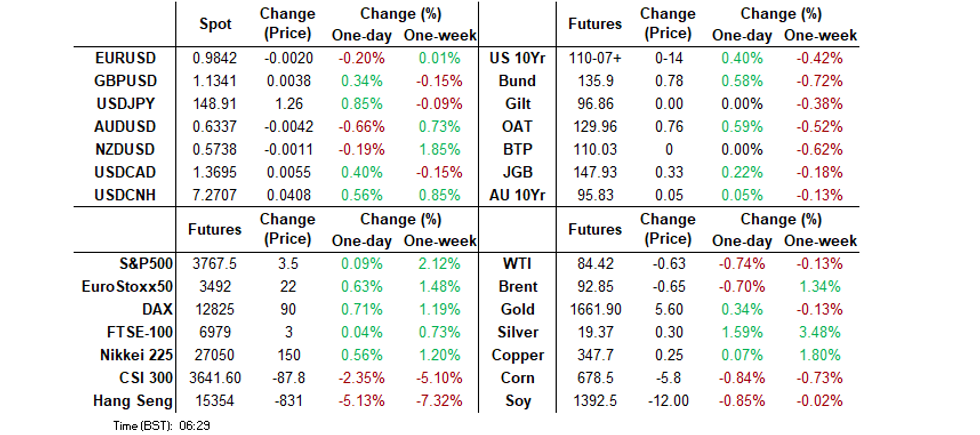

- It has been a volatile start to the week in FX markets, GBP surging on hopes of greater political stability, while early USD/JPY strength gave way to a sharp near 3% pull back on intervention fears. Outside of the pound, the USD has recouped some last week's losses, firmer by 0.3% so far.

- China related equities are down sharply, as the market assessed the revamped line-of of the party leadership and expectations of a continuation of current policy settings, such as dynamic Covid zero. This weakness took US equity futures off their respective highs, while US yields continued to trace, 2yr back to 4.425%, -5bps for the session. Commodities were quieter.

- China Q3 GDP beat estimates comfortably, but consumer spending/housing data still suggest underlying fragility to the economic recovery. Due later is PMI prints across the UK, EU area, along with US readings. Comments are due from BoE's Ramsden, who will testify to parliament for his reappointment.

US TSYS: Contagion From China Puts Bid Into U.S. Tsys

Core FI caught a fresh bid as Chinese equity benchmarks tumbled. Markets assessed the revamped line-up of Chinese Communist Party leadership, as well as delated data including Q3 GDP and September economic activity indicators. The data were a mixed bag, as China's economy expanded at a faster than expected clip and industrial output grew more than forecast, but retail sales underwhelmed, unemployment ticked higher and new home prices extended decline.

- T-Notes struggled to make much headway beyond last Friday's high before the spillover from Chinese markets spoiled the mood. TYZ2 advanced, printed a session peak at 110-06+ and stabilised. The contract last deals +0-10+ at 110-03+. Eurodollars run up to +8.0 ticks through the reds.

- The yield curve shifted lower in cash Tokyo trade. When this is being typed, U.S. Tsy yields sit 3.8-5.9bp lower, with belly outperforming.

- E-minis are close to erasing their initial gains, albeit all three still operate in the green.

- Flash readings of S&P Global PMIs & Chicago Fed Nat Activity Index headline the domestic data docket today.

JGBS: JGBs Advance Amid Yen Volatility, Risk Aversion; BoJ Policy Review Eyed

JGB futures started on a firmer footing, rising to 147.90 on the initial upswing, amid heightened JPY volatility. Another round of purchases emerged as broader risk sentiment soured on the back of weakness in Chinese equity space, with participants digesting the outcome of Chinese Communist Party's congress and a mixed bag provided by delayed Chinese activity data.

- JBZ2 last trades at 147.96, up 37 ticks from the prior settlement, printing new session highs. Cash JGB yields are mostly lower, save for 3s & 20s, with 7s leading gains. The yield on 10-Year JGBs tested the 0.25% cap imposed by the BoJ as part of its YCC framework.

- Reminder that Japan's central bank will hold a monetary policy meeting this Friday. The Policy Board has been adamant to stick with its super-dovish stance, even as the market keep putting it to a test. It is expected that the BoJ will keep the main parameters of its policy unchanged this week, remaining the last dovish holdout among major central banks.

- A round of flash Jibun Bank PMI readings caused little stir.

AUSSIE BONDS: Steepening Impetus Intensifies, Futures Turn Bid On Cautious Mood

Deteriorating risk environment lent support to Aussie bonds and their peers from core FI space. Nominations to the top decision-making bodies of the Chinese Communist Party were closely scrutinised, with local equity benchmarks retreating.

- Futures regained strength after paring initial gains. YM last +14.0 & XM +5.0, both are printing session highs. Bills trade 4-12 ticks higher through the reds.

- Initial steepening impetus evident in cash ACGB space deepened as the session progressed. Yields last sit -14.5bp to +4.2bp. 3-Year/10-Year ACGB yield spread widened to 52.5bp, the widest margin since mid-Jul.

- The AOFM sold A$300mn of ACGB Jun '51, drawing a bid/cover ratio of 1.54x (prev. 2.53x), with the price tail widening.

- The weekend saw one of the final rounds of comments from Treasurer Chalmers, who will deliver the budget tomorrow. The official said he has learned his lesson from the market reaction to the UK fiscal plan.

- Elsewhere, RBA Asst Gov Kent said this morning that the central bank is not currently worried by the risk of weak exchange rate amplifying imported inflation.

- Regional activity was limited by a market closure in New Zealand.

AUSTRALIA: Budget And CPI Focus Of The Week Ahead

This week the two major events in Australia will be the budget on Tuesday evening and CPI data for Q3 on Wednesday.

- The first budget for Australia’s new government is to be delivered on Tuesday at 1930AEDT. Its focus is likely to be establishing Labor’s budgetary credentials while delivering on its election promises. Economic projections are to be downgraded while showing that Australia should avoid a recession. Treasurer Chalmers has been managing expectations and stating that the budget needs to be responsible.

- On Wednesday, CPI data for Q3 and September are due to be published. While it is backward looking, it will be important for shaping RBA expectations. Economists expect the headline CPI to rise 1.6%q/q and 7%y/y (Q2 1.8%q/q and 6.1%y/y) and the trimmed mean by 1.5%q/q and 5.5%y/y (Q2 1.5%q/q and 4.9%y/y). The newly-established monthly series is expected to rise 7.1%y/y in September.

- On Thursday, export and import prices for Q3 are released with the former expected to fall 6.5%q/q on lower commodity prices and the latter to rise 0.8%q/q. This would result in deterioration in the terms of trade in Q3.

- Finally, on Friday the second-tier PPI for Q3 prints and should give an indication on pipeline inflation trends.

Source: MNI - Market News/NAB/Refinitiv

FOREX: USD Finds Supports As Equity Rebound Falters, GBP Outperforms

The USD has recouped some losses from late last week. The BBDXY is up around 0.30%, to 1340, albeit in a volatile start to the week. Ultimately flows have benefited the USD, as sharp falls were recorded across China related equities, taking the shine off early positive sentiment in Asia Pac markets.

- The early focus started GBP/USD, which surged 1% to +1.1400, as Boris John bowed out of the leadership race, spurring hopes of political stability. This leaves ex-Treasury, Rishi Sunak, as the likely next PM. The pound is back to 1.1335/40, but is still firmer for the session, the only major currency to do so against the USD.

- USD/JPY rose above 149.70, reportedly on buy orders that weren't filled through Friday's session, before slumping near 3% to sub 146.00. This likely reflected intervention flows, but nothing was confirmed by the authorities. We are now back just under 149.00.

- AUD/USD has also performed poorly. We are up slightly from earlier lows, last around 0.6335/40, still -0.60% for the session. Outside of equity headwinds, the preliminary PMI for the services sector slipped into contractionary territory. RBA's Kent also downplayed concerns of a weaker AUD boosting imported inflation.

- Due later is PMI prints across the UK, EU area, along with US readings. Comments are due from BoE's Ramsden, who will testify to parliament for his reappointment.

ASIA FX: USD/CNY To Fresh Cyclical Highs

Most USD/Asia pairs are higher, with continued focus on USD/CNH. Only IDR has managed spot gains against the USD today. Several regional markets have been closed for holidays though - Singapore, Malaysia, Thailand & India. The main data focus tomorrow will be the September Singapore CPI print.

- The CNY fixing outcome, which today printed at 7.1230, is opening the door for slightly larger yuan depreciation pressures. Onshore spot is above 7.2500, fresh cyclical highs, but hasn't seen great follow through momentum. USD/CNH is back under 7.2700. China Q3 GDP beat estimates, but data for retail spending and the property sector still disappointed, relative to expectations.

- USD/KRW 1 month is higher, +0.50% on closing levels from the end of last week. We did find selling interest above 1140 though (last at 1436). The Kospi is off its highs, but +1% on closing levels form last week. Fresh support to credit markets has likely aided sentiment today. The authorities have pledged up to $35bn in funding support, following a recent missed payment in the space and signs of market stress.

- Spot USD/IDR deals at IDR15,578, down -55 figs on the day, with bears looking for a deeper retreat towards Oct 5/Sep 30 lows of 15,162/15,150. Bulls target the 16,000 figure. Foreign investors were net buyers of $75.41mn last Friday, with the Jakarta Comp testing its 100-DMA to the upside. The local data docket is virtually empty during the remainder of the week.

- BSP Gov Diokno drew a line in the sand at 60, vowing aggressive action to defend that level via a combination of interest-rate hikes and interventions in the currency markets. The impact on the PHP has been limited, with comments on the effective cap on peso weakness being mere reiteration of remarks from last Friday. USD/PHP remains slightly below recent highs, last at 58.77.

CHINA DATA: Q3 GDP Beat Masks Underlying Fragility

China's Q3 GDP beat, +3.9% q/q versus +2.8% q/q expected, doesn't suggest the economy is on a solid footing yet. The NBS stated just as much post the release. IP in September was much firmer than expected, +6.3% y/y, against +4.8% y/y forecast. This sector continues to recover, although retail sales fell back, +2.5% y/y, versus +5.4% y/y last month and +3.0% expected.

- This is still likely to leave the bias towards easier policy settings to support the property/consumer segments of the economy.

- Softer retail spending reflected lower spending in discretionary (outdoor dining) and the property related categories.

- Property investment remained weaker, down -8.0% YTD y/y, against -7.5% expected. This dragged the overall fixed asset investment result to 5.9% YTD y/y, slightly below the 6.0% forecast.

- Unemployment was higher than forecast 5.5%, versus 5.2% forecast. Youth unemployment will remain an area of concern (17.9% for 16-24 yr olds).

- The trade side remained resilient, exports +5.7% (4.0% forecast), imports 0.3% (against 0.0% forecast). The trade surplus remained healthy at $84.74bn as well, also above forecasts.

- Commodity imports were up in volumes terms for coal (12.19%) and iron ore (+3.6%), but still lower in y/y terms. Oil import volumes were down a touch.

EQUITIES: HK/China Equity Falls Take Shine Off Rebound

Losses across Hong Kong & China shares have taken the gloss of what looked like a promising start to the week for regional equity markets. US futures opened up strongly, with Eminis above 3800 at one stage but we are now back close too flat (3765/70). This curtailed gains for the major Asia Pac indices. Note several markets have been closed today due to holidays - Singapore, Malaysia, Thailand, India and NZ.

- China related markets were down sharply in early trading. The HSI China enterprise index off more than 5.5, the CSI 300 around 1.75%.

- Markets assessed the revamped line-of the party leadership, as well expectations of a continuation of recent policies, such as the dynamic covid zero policy.

- Higher covid case numbers in Guangzhou, which is a manufacturing hub, has prompted fresh restrictions for this district as well. Q3 GDP for China beat estimates, but retail spending, housing investment & prices disappointed for September.

- The HSI saw negative spill over as well, down 5% for the headline index, -7.7% for the tech sub-index.

- The Kospi (+0.75%) & Taiex (+0.45%) have fared better, following positive leads from US tech names late last week. South Korean markets were also supported by fresh measures to support local credit markets, following a recent payment miss, which unnerved confidence in the sector.

GOLD: Edging Lower On a Firmer USD

Gold is down slightly from closing levels at the end of last week, as the USD has recouped some losses from late last week. We were last around $1654, -0.20% for the session so far. We spiked above $1670 early in the session, as the yen rebound led a broad wave of USD selling, before correcting back lower.

- Still, the precious metal has held onto a good proportion of gains from late last week. The dip below $1620 level was supported on Friday evening, and we remained above recent cyclical lows from September 28th.

- The 0.80% gain for gold last week was a little at odds with higher US real yields (the 10yr finished the week down slightly at 1.68%, but this was still +10bps for the week), but it only partially reverses the -3% fall from the week prior.

- Us yield momentum will likely remain key to gold's fortunes over a multi-day horizon.

OIL: Demand Fears Again Have Upper Hand In Driving Prices

Supply issues had been driving a recent moderate rally in oil prices but today global demand concerns took over again, as negative sentiment surrounding China and Hong Kong drove markets generally. The release of Chinese data due last week also painted a mixed picture of the Chinese economy and its woes in the property sector remained a concern.

- WTI reached an intraday high of almost $86/bbl before global growth fears took over and is now trading around $84.60/bbl down 0.5%. Brent rose to $94.27 but is now trading just around $93 and is also down 0.5%. Near-term Brent contracts continue to be priced higher than ones further out, which is bullish but consistent with slower growth expectations for 2023.

- The tight supply environment and global demand worries should to continue to drive oil price developments for the foreseeable future. The market is likely to watch if the US takes further measures to increase supply and how compliant OPEC+ is with the production cuts due to take place next month.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/10/2022 | 0030/0930 | ** |  | JP | IHS Markit Flash Japan PMI |

| 24/10/2022 | 0715/0915 | ** |  | FR | IHS Markit Services PMI (p) |

| 24/10/2022 | 0715/0915 | ** | | FR | IHS Markit Manufacturing PMI (p) |

| 24/10/2022 | 0730/0930 | ** |  | DE | IHS Markit Services PMI (p) |

| 24/10/2022 | 0730/0930 | ** | | DE | IHS Markit Manufacturing PMI (p) |

| 24/10/2022 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (p) |

| 24/10/2022 | 0800/1000 | ** | | EU | IHS Markit Manufacturing PMI (p) |

| 24/10/2022 | 0800/1000 | ** | | EU | IHS Markit Composite PMI (p) |

| 24/10/2022 | 0830/0930 | *** |  | UK | IHS Markit Manufacturing PMI (flash) |

| 24/10/2022 | 0830/0930 | *** | | UK | IHS Markit Services PMI (flash) |

| 24/10/2022 | 0830/0930 | *** | | UK | IHS Markit Composite PMI (flash) |

| 24/10/2022 | 1300/1400 | | UK | Deadline for MPs to nominate next Cons leader | |

| 24/10/2022 | 1345/0945 | *** |  | US | IHS Markit Manufacturing Index (flash) |

| 24/10/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (flash) |

| 24/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 24/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 24/10/2022 | 1700/1800 | | UK | Result of 1st round of MP voting for next Cons leader | |

| 24/10/2022 | 2000/2100 | | UK | Result of 2nd round of MP voting for next Cons leader |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.