Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- China asset volatility has remained the focus point again today. Onshore & HK equities opened lower, before dip buyers emerged. The range of HK tech stocks is close to 10%. Offshore investors returns to onshore shares today, after yesterday's record outflow.

- The USD/CNY fix was set at the highest level since 2008 (7.1668), allowing onshore spot to break above 7.3000, CNH touched a fresh low near 7.3700. There was spill over to the rest of the region, but it was less evident compared to recent weeks. Oil nudged up but remains remain within recent ranges, while iron ore and copper fell despite firmer China equities. US yields tracked recent ranges, the 2yr holding close to 4.50%.

- Still to come is the Australian budget speech (7:30pm AEST), followed by tomorrow's Q3 CPI print. In the US tonight, local data highlights today include Conf. Board Consumer Confidence & Richmond Fed M'fing Index, while Fed's Waller will speak at a conference in Las Vegas.

US TSYS: Futures Halt Gains Amid Rebound In Chinese Equities

Initial topside impetus moderated as T-Notes topped out at 109-29+ and stabilised just shy of that level. E-mini futures oscillated between gains and losses amid heightened volatility in China's equity markets, staging an about-face after a spell of early-doors weakness. The ongoing debate on Fed terminal rate level may have factored into the price action, although swaps market pricing was little changed.

- There was little in the way of FI-specific headline flow in Asia-Pac hours, but regional players digested Monday's surge in gilts, stemming from the promise of stabilisation in UK political landscape.

- When this is being typed, T-Notes trade +0-04 at 109-27+, while Eurodollars trade -0.5 to +1.5 tick through the reds.

- Cash curve sits lower and runs flatter, with yields last seen 0.6-3.3bp as 10s outperform. The marginal tightening in 5-Year/30-Year Tsy yield spread brought it close to the breakeven level.

- Local data highlights today include Conf. Board Consumer Confidence & Richmond Fed M'fing Index, while Fed's Waller will speak at a conference in Las Vegas. Also coming up is an auction of 2-Year Tsys.

JGBS: Long-End Cash JGBs Regain Poise, 10-Year Yield Stays Near BoJ's 0.25% Cap

The outperformance of the super-long sector drove flattening in cash JGB yield curve, with 30s leading gains at typing. This represents a reversal of early price action, which saw the 20/30/40-Year sector lag shorter-dated bonds. Long-end purchases coincided with the publication of the results of a liquidity enhancement auction covering off-the-run JGBs with 15.5-39 years until maturity, which saw spreads widen, spread tail tighten a little and the cover ratio slip, relative to the previous auction. A spillover from other core FI markets may have facilitated the re-flattening of JGB curve.

- JGB futures had a strong start to the session, running to 148.05 in the initial upswing. The contract eased off into the Tokyo lunch break, which was out of sync with gains in T-Notes and Aussie bond futures, while coinciding with the latest round of comments from FinMin Suzuki. The contract found poise after lunch, albeit fell short of re-testing session highs, and last deals +15 ticks at 148.00.

- The latest speech from FinMin Suzuki reconstructed a familiar logic surrounding the division of labour between the MoF and BoJ, while reaffirming existing views on FX developments. The minister vowed to respect the central bank's independence as it's trying to achieve sustainable, wage-driven inflation. He noted that the MoF is in daily communication with the U.S. over market developments, despite earlier remarks from Tsy Sec Yellen, who said Japan did not notify the U.S. about any new FX interventions. Suzuki reiterated that officials are focusing on excessive volatility, while the exchange rate should be determined by the market, despite earlier conceding that the pass-through from currency depreciation to domestic price pressures is increasing.

- 10-Year JGBs operated in the vicinity of the 0.25% yield ceiling set by the BoJ as part of its Yield Curve Control programme. A scheduled round of 3-25+ Year Rinban operations tomorrow will be watched for any signs of escalation in YCC enforcement ahead of the BoJ's monetary policy meeting this Friday.

JGBS AUCTION: Japanese MOF sells Y498.8bn of 15.5-39 Year JGBs in a liquidity enhancement auction:

The Japanese Ministry of Finance (MOF) sells Y498.8bn of 15.5-39 Year JGBs in a liquidity enhancement auction:

- Average Spread: +0.060% (prev. +0.029%)

- High Spread: +0.067% (prev. +0.034%)

- % Allotted At High Spread: 19.8770% (prev. 46.2311%)

- Bid/Cover: 2.897x (prev. 2.403x)

AUSSIE BONDS: Bull Flattening Takes Hold Ahead Of Budget Speech

Bull flattening in ACGB yield curve was evident, with U.S. Tsy curve undergoing a similar (albeit less pronounced) transformation. At typing, ACGB yields sit 1.7-8.3bp lower, as we await tonight's budget speech. The gap between 3-Year/10-Year yields narrowed at the margin and last sits at 48.75bp.

- Futures contracts traded with a bullish bias, while flattening impetus took hold; YM last +1.0 & XM +5.5, stabilising near session highs after the initial rally. A rebound in Chinese/HK equities likely contributed to the moderation in demand for core FI assets.

- Bills run unch. to +6 ticks through the reds.

- Treasurer Chalmers said that accelerating inflation was the "primary influence" on the spending plan, as he prepares to deliver his budget speech at 19:30 AEDT/09:30 BST (see our preview here).

AUSTRALIA: Budget Preview – Deficit To Halve But Deteriorating Outlook

The first budget for Australia’s new government is to be delivered tonight at 1930AEDT. Its focus is to establish Labor’s budgetary credentials while delivering on its election promises. Economic projections are to be downgraded while showing that Australia should avoid a recession. Treasurer Chalmers has been managing expectations and stating that the budget won’t add to inflation pressures.

- Treasury’s forecasts should show economic growth of 3.25% for 2022-23 (revised down 0.25pp) but 1.5% in 2023-24 due to higher inflation and rates, and slower global growth (compared with the RBA’s current 1.8% forecast). Wage growth is expected to remain below inflation, and the unemployment rate should rise to 4.5% in 2023-24. Inflation is forecast to end 2022 at 7.75% (consistent with the RBA). (The Australian)

- The budget is likely to show A$100bn revenue boost over the next four years, front loaded in the first 2 years, driven by commodities and tax revenue. Therefore, this year’s deficit is due to halve to $36.9bn (about 1.5% of GDP) but it deteriorates in the years following as structural spending rises. (The Australian)

- A$22bn of spending cuts are also likely to be announced, according to The Australian, and Finance Minister Gallagher said that there’ll be further cuts going forward.

- Additional budgetary pressures are expected from increased interest on the debt, although gross debt should trend down. An extra A$33bn is needed for the higher indexation of welfare payments, A$1.4bn for flood relief, A$900mn for the Pacific, and an additional A$10bn for aged-care and health.

- The Australian reports that the budget will forecast an almost 30% rise in power costs next year and that relief measures could be announced in the budget.

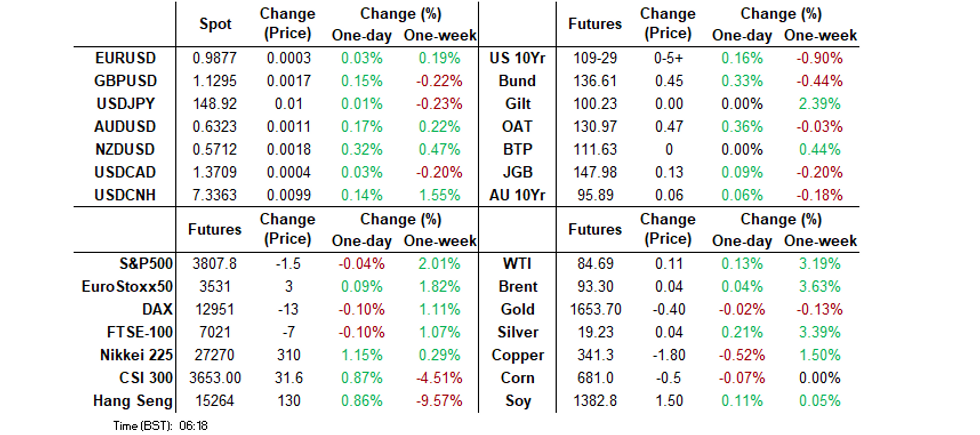

FOREX: USD Lower, Higher China Equities Help A$ & NZD Outperform

The USD is down slightly through today's session, the BBDXY off by -0.10% to 1339, but dips in the index were supported back to overnight lows. We have seen some commodity currency outperformance, although this is more reflective of more positive sentiment in HK/China equities rather than a rebound in commodity prices.

- AUD/USD dips towards 0.6310 have been supported, last around 0.6330, with highs above 0.6340 capping the pair. Iron ore futures in Singapore are sub $90/tonne, while copper is also down slightly. Oil has held up better. Dip buyers in HK/China equities have offset and helped the A$ push higher and remain above NY closing levels.

- NZD/USD has slightly outperformed, last around 0.5715, +0.35% for the session. Earlier RBNZ Chief Economist Conway stated the central is hopeful inflation has peaked, while Deputy Prime Minister Robertson stated no decision has been made on a minimum wage rise for 2023.

- USD/JPY has traded tight ranges, last just above 148.80. A host of official comments didn't appear to shed any fresh light on the intervention issue.

- EUR/USD is just above 0.9880, unable to break above 0.9900, while GBP/USD is trying to hold above 1.1300.

- Still to come is the Australian budget speech (7:30pm AEST), followed by tomorrow's Q3 CPI print. In the US tonight, local data highlights today include Conf. Board Consumer Confidence & Richmond Fed M'fing Index, while Fed's Waller will speak at a conference in Las Vegas.

ASIA FX: USD/CNY Holding Close To Upper Daily Trading Limit

USD/Asia trends have been more mixed today. The Chinese currency remains under pressure, while the won has outperformed, with mixed performances elsewhere. Tomorrow the data calendar is light in the region, with just South Korean business sentiment indicators out, we should also get Thailand trade figures over the next few days.

- The break higher in the USD/CNY fixing, to 7.1668, fresh highs back to 2008, drove another record high in USD/CNH to just under 7.3700. Onshore spot opened higher as well, but ran out of steam close to 7.3100, which is the upper daily trading limit. USD/CNH is also back to the 7.3350/00 region. The PBoC announced easing requirements for cross-border funding, aimed at supporting capital inflows.

- The won has bucked the weaker CNY/CNH trend. We spiked towards 1145 in early trade, but we have drifted lower since then, now back to 1433. Higher onshore equities have helped, but only at the margin. The Kospi last +0.20%.

- Singapore September inflation data came in as expected. Headline y/y to 7.5%, while core rose to 5.3%, also matching expectations. USD/SGD has been range bound today, last at 1.4220, with higher NEER levels still the likely preferred play.

- Spot USD/THB loses some altitude upon return from a long weekend in Thailand, with lower U.S. Tsy yields offering some support to the baht, on top of the overhang market impetus. The rate last sits -0.08 at 38.28. Thailand's Customs trade data are expected to hit the wires in the coming days.

- Spot USD/IDR has added 27.5 figs and changes hands at 15,615. A break above the Oct 21 high of 15,634 would bring Apr 16, 2020 high of 15,754 into view. Foreign players bought a net $89.45mn in local stocks Monday, while the Jakarta Comp climbed for the fourth consecutive day. The tightening in INDOGB 5-Year/10-Year spread has extended after last week's monetary policy decision from Bank Indonesia and last sits at 29.4bp, printing its worst levels since early 2019. Flattening impetus is likely amplified by Bank Indonesia's "Operation Twist."

EQUITIES: Dip Buyers Emerge For HK/China Equities, Offshore Flows Return

Hong Kong and China markets have remained in focus today. Both markets opened weaker, but are now back in positive territory, with large trading ranges for the session so far. Trading has been more muted elsewhere. US futures are range bound, ahead of important earning results later this week. Eminis just sitting in positive territory for the session, last around 3810.

- The range today on HSI has been over 3%. After opening lower (after yesterday's 6.36% fall) loss, dip buyers emerged, and we are now back to +0.5% the session. Ranges for the HSI tech sub index have been near 10%, with this index now around +2.7% for the session.

- Onshore equities are higher, albeit with reduced volatility. The CSI 300 last around +0.90% for the session, while the composite index is up 0.75%.

- There didn't appear to be fundamental catalyst for the turnaround in HK or China equity indices. Offshore investors have turned net buyers of China shares (+4.2bn yuan, after yesterday's record 17.9bn yuan outflow). Some technical support was also cited for the HSI, while the PBoC also announced measures which make it easier for domestic companies to raise funds offshore, although this looks to be more targeted at relieving yuan depreciation pressures.

- Elsewhere, the Topix is up 1.3%, amid broad based gains. The Kospi is edging higher, last +0.40%, but the Taiex is lagging -0.90%.

GOLD: Taking Cues From USD Sentiment

Gold has stuck to ranges from late NY trading during today’s Asia Pac session. We last sat around $1652, slightly up on NY closing levels (+0.15%). This is in line with modest pull back in broader USD sentiment today (BBDXY off -0.16%).

- The high from earlier in the session, near $1655, along with today's low $1647.30 remain within yesterday's ranges though.

- Gold appears comfortable to follow broader USD sentiment for now, lacking a fresh catalyst for a major shift in direction.

- Overnight US real yields edged down 3bps to 1.66%. Nominal yields fell, but more so outside of the US.

OIL: Late Recovery As USD Down And Hang Seng Rises

Oil prices traded lower during the day before they turned up again as the Hang Seng and Shanghai stock indices bounced and the USD moderated, making commodities cheaper for foreigners.

- The WTI is trading at $84.92 +0.4%, just below 20-day MA, and Brent is around $93.50 +0.3%. Oil prices seem range bound as concerns over supply issues counteract expectations of a slowdown in global demand.

- API weekly crude oil stocks in the US are published tonight for the week of October 21. The previous week saw a drawdown of 1.27mn barrels. A repeat of this would likely bring supply worries to the forefront driving prices higher again.

- There are signs that Europe’s sanctions on Russian oil are already having an impact before they’re implemented next month. Russian shipments by sea hit a 5-week low in the 7 days to October 21. (ANZ)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/10/2022 | 0600/0800 | ** |  | SE | PPI |

| 25/10/2022 | 0700/0900 | ** |  | ES | PPI |

| 25/10/2022 | 0800/1000 | *** |  | DE | IFO Business Climate Index |

| 25/10/2022 | 0855/0955 |  | UK | BOE Pill at ONS ‘Understanding the cost of living through statistics’ | |

| 25/10/2022 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 25/10/2022 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 25/10/2022 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 25/10/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 25/10/2022 | 1300/1500 | ** |  | BE | BNB Business Sentiment |

| 25/10/2022 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 25/10/2022 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 25/10/2022 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 25/10/2022 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

| 25/10/2022 | 1755/1355 | | US | Fed Governor Christopher Waller |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.