Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

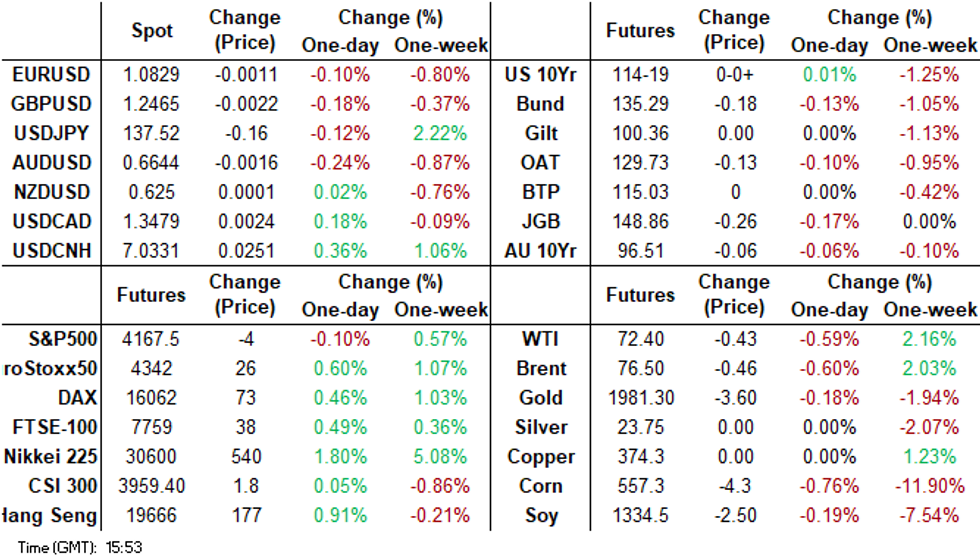

- NZGBs closed sharply cheaper with 2-year and 10-year benchmark yields respectively 17bp and 9bp higher after the NZ Treasury says the budget is stimulatory and so rates will stay “higher for longer”. ACGBs sit mid-range (YM -6.0 & XM -4.0) after the post-employment spike higher was all but reversed in after trade. The April Employment Report undershot expectations with a print of -4.3k m/m versus expectations of +25k and delivered an unexpected lift in the unemployment rate to 3.7% (3.5% est.) from 3.5%.

- In the equity space, regional stock markets are mostly higher, led again by Japan bourses. North East Asia markets have outperformed South East Asia, as tech sentiment continues to drive gains. Japan's Topix is up over 1%, with tech sentiment again positive. Micron will reportedly start making advanced chips in Japan with the aid of government subsidies. This is expected to boost local supplies, while Japan PM Kishida met the heads of other tech firms from South Korea and Taiwan, hence there is scope for further partnership/investments.

- This may have generated more of risk on tone but CNH has continued to depreciate. USD/CNH is now through 7.0300, as we continue to see fall out from the recent run of softer than expected data momentum and growth downgrades.

MARKETS

US TSYS: Marginally Richer In Asia

TYM3 deals at 114-21, +0-03, with a 0-05 range observed on volume of ~76k.

- Cash tsys sit ~1bp richer across the major benchmarks.

- Tsys firmed on spillover from ACGB's as Australia's unemployment rate ticked higher in April, however the move had little follow through and gains were pared.

- Narrow ranges persisted for the remainder of the session.

- A block buyer in TU (2.49k lots) added a layer of support.

- FOMC dated OIS price a terminal rate of ~5.1% in June, there are ~60bps of cuts priced for 2023.

- There is a thin docket in Europe today, further out we have Initial Jobless Claims and Philadelphia Fed Business Outlook. Fedspeak from Gov. Jefferson, VC Barr and Dallas Fed President Logan is on the wires. The latest 10 Year TIPS supply will cross.

JGBS: Futures Heavy, Lacklustre BoJ Rinban Operations

JGB futures push to session lows in the Tokyo afternoon session, -24 versus settlement levels, after the morning’s BoJ Rinban operations covering 1-10-year and 25-Year+ JGBs showed flat to positive spreads and slightly higher cover ratios.

- US tsys push away from session bests assisted the cheapening in JGBs in the afternoon session.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined weaker-than-expected trade data which only appeared to provide a brief pop higher in JGB futures at the start of the Tokyo session.

- Cash JGBs are mixed with the 1-year and 7-year zones 1.4bp cheaper but little changed in between. The 10-40-year zones are flat to 0.9bp cheaper. The benchmark 10-year yield is 0.9bp higher at 0.379% with the 20-year yield flat at 0.976%, after yesterday's auction-induced decline of 3.7bp.

- The swap curve twist steepens with rates 0.1bp lower to 1.1bp higher. Swap spreads are wider except for the 1-year and 7-year zones.

- Tomorrow sees the release of the National CPI release for April along with the weekly auction of 3-month bills.

AUSSIE BONDS: Post-Jobs Data Spike Richer Is Unwound

ACGBs sit mid-range (YM -6.0 & XM -4.0) after the post-employment spike higher was all but reversed in after trade. The April Employment Report undershot expectations with a print of -4.3k m/m versus expectations of +25k and delivered an unexpected lift in the unemployment rate to 3.7% (3.5% est.) from 3.5%.

- A closer examination of the data, which revealed that the actual rise in the unemployment rate was only 1.2% before rounding and that March employment had been revised higher from 53k to 61.1k, saw the market quickly reverse course.

- A move away from the session best level for US tsys and sharply higher NZGB yields post-budget likely aided the ACGB reversal.

- Cash ACGBs are 1-2bp richer post-data but 4-6bp cheaper on the day with the AU-US 10-year yield differential +1bp at -9bp.

- Swap rates are sitting mid-range with 6-8bp higher and EFPs 1-2bp wider.

- The bills strip is steeper with pricing -1 to -13.

- RBA dated OIS are 4-10bp firmer on the day for meetings beyond September.

- The local calendar is light until Retail Sales on May 26.

- With the US calendar relatively light today, US tsys are likely to be on headline watch, particularly about debt ceiling negotiations.

AUSTRALIAN DATA: Inflation Expectations Rise In May But Q2 Average Lower Than Q1

Melbourne Institute consumer inflation expectations rose to 5.2% in May from 4.6% the previous month. It is concerning that moves below 5% are yet to be sustained. The Q2 average to date is still below Q1 at 4.9% compared with 5.2%, despite today’s shift up, and signalling that Q2 inflation should continue to moderate. Until recently the series has tended to exceed CPI inflation.

- There was good and bad news on inflation during May but it appears that consumers were more convinced by media commentary that the budget was inflationary than by Treasurer Chalmers reassurances that it would bring inflation down. There has also been a lot in the press about rising rents and house prices, plus people could also be reflecting how they feel every time they go supermarket shopping rather than when they get petrol.

Source: MNI - Market News/Refinitiv/ABS

AUSTRALIAN DATA: Employment Data Softer But One Month Doesn’t Make A Trend

April employment data came in weaker than expected with the number of jobs falling 4.3k, driven by full-time, and the unemployment rate rising to 3.7% with the participation rate down 0.1pp to 66.7%. But March was revised up to an even stronger 61.1k from 53k due to a 10k increase in full-time jobs. Hours worked are rising strongly indicating that labour shortages are still being filled by longer hours. After some concerning elements in the Q1 WPI data, the softer April labour market release potentially gives the RBA the reason it needs to wait and see at the June meeting, since one month doesn’t make a trend.

- The rise in the unemployment rate looks worse than it is. It was 3.54% in March (a high 3.5%) and 3.66% in April (a low 3.7%), thus April saw a 0.12pp rise, driven by a 4k drop in the number of jobs with an 18k increase in the number of unemployed.

- Job growth has averaged 28.1k/mth this year after the post-pandemic impacted 40.2k in 2022. Employment growth eased to 2.9% y/y (above 2019’s 2.3%) but it is showing rising 3-month momentum, especially in the full-time sector. FT fell 27.2k after an upwardly revised +82.5k in March, while part-time rose 22.9k after falling 21.4k.

- Hours worked rose 2.6% m/m to be up 7.4% y/y, driven by fewer people taking time off at Easter (55% compared to 60% in 2015), which the ABS says may be because their workplaces were short staffed given elevated vacancies.

- The underemployment rate fell 0.1pp to 6.1% and underutilisation rose 0.1pp to 9.8%. Both remain well below pre-pandemic levels.

- The population aged +15 years rose another 0.2% m/m to be up 2.4% y/y, to be the fastest annual growth rate since December 2008. The labour force continues to grow solidly at 2.7% y/y.

Source: MNI - Market News/ABS

Australia population growth y/y%

Source: MNI - Market News/ABS

NZGBS: Yields Sharply Higher, Stimulatory Budget, Increased Borrowings

NZGBs closed sharply cheaper with 2-year and 10-year benchmark yields respectively 17bp and 9bp higher after the NZ Treasury says the budget is stimulatory and so rates will stay “higher for longer”.

- An expansionary budget in an already capacity-constrained economy is likely to concern the RBNZ. RBNZ dated OIS closed 8-18bp firmer for meetings beyond May. 31bp of tightening is priced for next week’s meeting.

- The FY23 deficit is forecast to be considerably larger than predicted in December by $3.4bn or 0.9pp. FY24 deficit is to widen to $7.6bn or 1.8% of GDP. The return to surplus has been delayed a year to 2026 (0.1% of GDP) due to repair costs from recent extreme weather. The debt ratio should peak at 22% in FY24.

- The forecast 2023/24 NZ Government Bond programme has been increased to NZ$34 billion, NZ$4 billion higher than that published at the Half Year Economic and Fiscal Update 2022. The forecast NZGB programmes for 2024/25, 2025/26, and 2026/27 have all been increased, by NZ$2 billion, NZ$10 billion and NZ$4 billion respectively.

- Swap rates closed 10-17bp higher with the 2s10s curve 7bp flatter and implied swap spreads sharply narrower.

- The local calendar sees the release of April trade data tomorrow.

NZ Budget: Larger Deficit And Stronger Growth, RBNZ To Hike Further

The NZ government sees higher growth in FY24, which means it expects a recession to be avoided, but it is forecasting lower near term inflation. Due to the repair costs from recent weather events the budget deficit will be significantly wider in FY24 than projected in December, but in the following years it is due to narrow sharply and be in surplus in FY26, the opposite pattern to Australia. The Treasury has said that the budget is stimulatory and so rates will stay “higher for longer”. An expansionary budget in an already capacity constrained economy is likely to concern the RBNZ. A 25bp hike is expected on May 24.

- The FY23 deficit is forecast to be considerably larger than predicted in December by $3.4bn or 0.9pp. FY24 deficit is to widen to $7.6bn or 1.8% of GDP. The return to surplus has been delayed a year to 2026 (0.1% of GDP) due to repair costs from recent extreme weather. The debt ratio should peak at 22% in FY24.

- Treasury’s growth forecasts have been revised down to 3.2% in FY23 (previous 3.5%) but revised up to 1.0% from -0.3% for FY24 boosted by repair activity and the tourism recovery. Inflation should be lower in FY23 at 6.2% (6.4%) and FY24 3.3% (3.5%) despite this additional activity. The outer years have been revised up slightly.

- Finance Minister Robertson said that the recent current account deficit widening should reverse with it reaching 5.9% in FY24 after 7.8% in FY23 and 3.8% in FY27. This has been an area of concern for ratings agencies.

- With an election in October, unsurprisingly the budget contained some sweeteners for voters. Cost of living relief to include subsidies for early childhood education, prescriptions, free transport for children and lower household energy bills. There will be a $6bn National Resilience Fund with around $1bn available for immediate repairs in the next year and improving flood defences.

- See budget here.

FOREX: AUD Pressured, NZD Firmer In Asia

The antipodeans have dominated G-10 FX in Asia on Thursday, AUD was pressured after the latest Labour Market Report showed that the unemployment rate ticked higher in April. NZD firmed after the NZ Treasury noted they now expect the economy to avoid recession, with GDP growth of 3.2% in 2022/23. New Zealand also increased its bond issuance program by $20bn over 4 years.

- AUD/USD sits at $0.6645/50, the pair is down ~0.2%. In April the unemployment rate nudged higher to 3.7% from 3.5%. Support was seen below $0.6635 and losses were marginally pared.

- NZD/USD is ~0.2% firmer and deals a touch below the 200-Day EMA ($0.6263), a break through here opens the high from May 11 at $0.6385.

- Yen is marginally firmer, however ranges have been narrow with little follow through on moves. Wednesday's highs were tested in early dealing however they remain in tact for now.

- Elsewhere in G-10 moves have been limited, BBDXY is little changed from yesterday's closing levels.

- Cross asset flows are mixed; e-minis are a touch lower and Hang Seng is ~1.2% firmer. US Treasury Yields are ~1bp lower across the curve.

- There is a thin docket in Europe today, further out we have US Initial Jobless Claims and Existing Home Sales.

EQUITIES: North East Asia Stocks Outperform On Tech Optimism

Regional stock markets are mostly higher, led again by Japan bourses. North East Asia markets have mostly outperformed South East Asia, as tech sentiment continues to drive gains. US futures sit close to flat after a positive Wednesday session.

- Japan's Topix is up over 1%, with the index now tracking higher for 5 straight sessions. Tech sentiment has again been positive. Micron will reportedly start making advanced chips in Japan with the aid of government subsidies. This is expected to boost local supplies, while Japan PM Kishida met the heads of other tech firms from South Korea and Taiwan, hence there is scope for further partnership/investments. Sony is also tracking higher after it was reported the company is considering spinning off its financial unit.

- In Taiwan, the Taiex is up a further 1%, with the index back to June 2022 levels (above 16000). Again, semiconductors are leading the move higher. Positive spill over from Japan news is helping, along with optimism around the demand outlook. The Kospi is +0.65%, with offshore investors adding a further $167.7mn to local shares.

- The HSI is also higher +1.1%, with the underlying tech index +1.73%. This comes despite weaker Tencent trends, after a disappointing earnings update. Alibaba reports later today. Mainland China shares are higher, but up a more subdued +0.38% for the CSI 300 at this stage. SoE firms are doing better on the back of strong ETF demand.

- In SEA, Thai stocks are performing the strongest, up near 0.9%, although who the next PM will be remains uncertain at this stage.

OIL: Crude Holds Onto Most Of Wednesday’s Gains, But Still Jittery

Oil prices are down around 0.4% during the APAC session but have been trading in narrow ranges. They rose around 2.5% yesterday on increased confidence there would be a timely solution to the US debt-ceiling impasse. WTI is around $72.56/bbl up from the intraday low of $72.49, while Brent is $76.68 after a low of $76.57. The USD index is slightly higher.

- Demand concerns persist in the crude market driven by lacklustre data from China and continued US rate hikes. It continues to worry that there will be a recession in the US. While there have been some supply disruptions, overall it remains solid as Russia does not appear to have cut output despite its reassurances that it will to support prices.

- Later the Fed’s Jefferson gives a speech on the economic outlook and Barr and Logan are also speaking. On the data front, there is US April existing home sales, the leading index, jobless claims and the May Philadelphia Fed index. ECB President Lagarde is also due to speak.

GOLD: Hovering At Three Week Lows In Asia-Pac Trade

Gold is hovering close to its lowest level in nearly three weeks at 1982.15 in Asia-Pac trade. The positive sentiment surrounding the resolution of the US debt-ceiling issue increased risk appetite, diminishing gold's appeal as a safe-haven asset. President Joe Biden expressed confidence in reaching an agreement to avert a default, and House Speaker Kevin McCarthy remained hopeful about a deal.

- The price of bullion has declined by 1.7% in the previous two sessions.

- Additionally, the strengthening of the US dollar and rising US Treasury yields are further factors weighing on gold, which lacks interest-bearing properties.

- According to MNI’s technical team, gold trend conditions are bullish, however, the yellow metal remains in a bearish cycle and the recent move lower is corrective. Support to watch is 1976.8, the 50-ema and 1963.3, the April 19 low.

ASIA FX: USD/CNH Above 7.03, KRW and TWD Remain Resilient

USD/Asia pairs are mixed, with CNH continuing to weaker, while KRW and TWD remain resilient on the back of stronger local equities, as the tech led recovery continues. USD/PHP is back sub 56.00 ahead of the upcoming BSP decision (no change expected), while USD/INR is drifting higher, back towards 82.50. The data calendar is light tomorrow, with just Malaysian trade data on tap, along with Taiwan BoP figures.

- USD/CNH continues to trend higher, breaching the 7.0300 level this afternoon. We hit a high of 7.0333 before some selling interest emerged. This is +100pips above yesterday's high. The move has been aided by onshore spot USD/CNY gains, with this pair now above 7.01. Onshore equities are firmer but lagging other North East Asia markets.

- 1 month USD/KRW tried to go lower in earlier trade, amid better equity trends, but couldn't get sub the 1327/28 region. We are now back to 1332/33, as weaker CNH levels have weighed. The Kospi has seen better traction, up 0.75%, amid tech optimism, while offshore investors have added a further $185.4mn to local shares.

- Spot USD/TWD has backed away from recent highs, last around 30.76, around 0.20% firmer in TWD terms for the session so far, albeit away from highs. We are back below the simple 200-day MA, which comes in at 30.78, but this doesn't look to be a major inflection point at this stage. The 50 and 100-day MAs sit lower (30.61 and 30.52 respectively). Recent highs have been between 30.80/85. Better local equity trends are aiding the TWD, particularly relative to the softer China currency trend. The TWSE has broken above the 16000 level today, fresh highs back to June last year. There still remains a wedge between these strong levels and USD/TWD, although CNY weakness, coupled with a yield differential still in favor of the USD will be providing an offset.

- USD/INR is a touch firmer in early dealing, the pair prints at 82.43/44 as the rupee follows broader USD/Asia trends on Thursday. Yesterday the pair printed its highest level since early April, strong US data boosted the greenback and rising Oil prices weighed on the rupee. Equity inflows from Foreign Investors remain strong, there have been ~$2.66bn in flows in May thus far. The data calendar is empty for the remainder of the week.

- Elsewhere in SEA, USD/PHP is back below the 56.00 level, as the markets awaits the BSP decision. No change is expected. USD/THB tried to move lower in early trade, but found support, the pair last in the 34.25/30 region.

SOUTH KOREA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of South Korean Newspapers and some other major news outlets from the past day or so.

ECONOMY: Korea’s economic recovery to be slower than Japan on weak exports (link)

ECONOMY: Inflation driving up costs to eat out (link)

ECONOMY: Hyundai, Kia's Europe sales rise 1.1% in April (link)

INFLATION: Seoul considering 150 won hike of subway fare in second half (link)

TRADE: Korea's tourism industry deficit widens after pandemic ends (link)

POPULATION: Korea needs to increase immigrants fourfold to avoid demographic cliff (link)

TECH: Korea bets on potential of advanced display technologies (link)

TECH: Korea’s big 3 battery makers estimated year-end orderbook to reach $749 bn (link)

MARKETS: Earnings at some Korean listed companies expected to improve from Q2 (link)

GEOPOLITICS: Biden may hold trilateral summit with S. Korean, Japanese leaders if possible: Sullivan (link)

GEOPOLITICS: Yoon, Trudeau agree to deepen partnership in critical minerals, youth exchanges (link)

POLITICS: Yoon vows to confront challenges by upholding spirit of 1980 pro-democracy uprising (link)

Indonesia: Highlights From Local News Wires

Below is a collection of news wire reports from English versions of Indonesian Newspapers and some other major news outlets.

Economy: “Indonesia’s manufacturing exports will increase again: Ministry” – Antara News (see link)

- Industrial exports fell sharply in April 2023 due to seasonal patterns and lower commodity prices. The industry minister believes though that they will recover as PMI and confidence data point to growth.

Economy: “Use budget in creative, innovative ways: Finance Minister” – Antara News (see link)

Economy: “Indonesia, EU to conclude trade deal negotiations this year: official” – Jakarta Globe (see link)

Economy: “Domestic market security main priority: Trade Policy Agency” – Antara News (see link)

Demographics: “Indonesia’s population to hit 324 million in 2045: gov’t” – Jakarta Globe (see link)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/05/2023 | 0630/0830 |  | EU | ECB de Guindos Remarks at PwC Seminar | |

| 18/05/2023 | 0745/0845 |  | UK | BOE Pill Opens CCBS Macro-finance Workshop | |

| 18/05/2023 | 0915/1015 | | UK | BOE Bailey Broadbent, Ramsden give TSC evidence on QE, QT at Bank, Threadneedle St | |

| 18/05/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 18/05/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 18/05/2023 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 18/05/2023 | 1305/0905 | | US | Fed Governor Philip Jefferson | |

| 18/05/2023 | 1330/0930 | | US | Fed Vice for Supervision Michael Barr | |

| 18/05/2023 | 1400/1000 | *** | | US | NAR existing home sales |

| 18/05/2023 | 1400/1000 | | US | Dallas Fed's Lorie Logan | |

| 18/05/2023 | 1400/1000 |  | CA | BOC publishes Financial System Review | |

| 18/05/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 18/05/2023 | 1500/1100 | | CA | BOC Governor press conference to discuss Financial System Review | |

| 18/05/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 18/05/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 18/05/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 18/05/2023 | 1700/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 18/05/2023 | 1900/1500 | *** |  | MX | Mexico Interest Rate |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.