Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

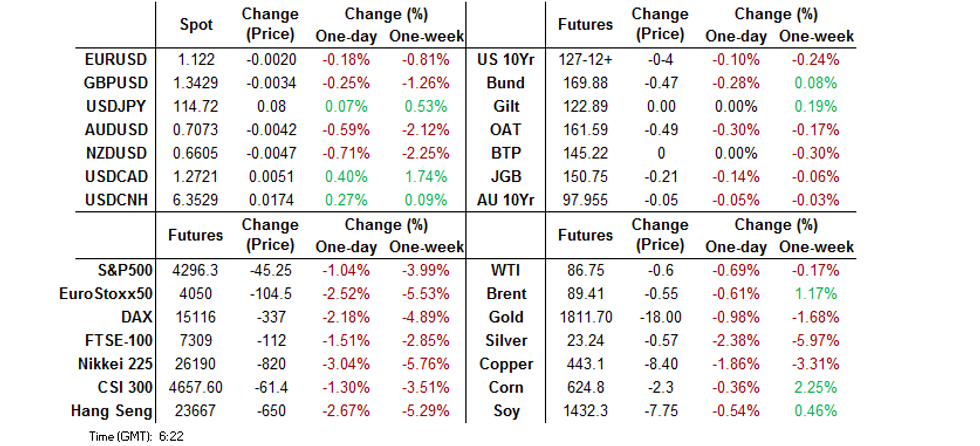

- The Fed's hawkish turn roils risk in Asia, sending regional equity indices lower, with the KOSPI & CSI 300 poised to enter bear market. Policymakers paved way for March rate lift-off & eyed faster tightening.

- Risk-off flows take hold across G10 FX space, with commodity-tied FX retreating along crude oil. Above-forecast CPI data fails to salvage NZD, which tests the $0.6600 figure against the greenback.

- JGBs & ACGBs falter under post-FOMC pressure, while Tsys stabilise after Wednesday's sell-off. Cash ACGB yields hit cycle highs as Sydney re-opens after a public holiday.

BOND SUMMARY: JGBs & ACGBs Under Post-FOMC Pressure, Tsys Stabilise

Asia-Pac core FI came under pressure from the post-FOMC impulse, while U.S. Tsys stabilised in the wake of a sharp sell-off. The Fed concluded their monetary policy meeting by paving way for a rate hike in March, while their rhetoric was testament to the potential for a steeper tightening path than had been previously anticipated.

- JGBs softened across the curve, as cash trading re-opened in Tokyo. Yields remain comfortably in positive territory, as Wednesday's FOMC meeting reinforced expectations of a growing policy divergence between the U.S. and Japan, with the BoJ committed to their current ultra-loose stance. JGB futures started the session on a softer footing and ground lower thereafter. JBH2 sits at 150.78, 18 ticks below last settlement, after hitting its worst levels in a week. The auction for 2-Year JGBs, which saw low bid match dealer expectations, provoked little to no market turbulence.

- ACGB yields shot higher as cash trading resumed after an Australian holiday, with Aussie bonds taking a hit from the FOMC's hawkish pivot. Yields last sit 6.2-8.7bp higher across the curve, after hitting fresh cycle highs in early Sydney trade. The main futures contracts tried to move away from worst levels, but YM eased off later in the session and last trades -8.0, with XM -6.0 (off lows) at typing. Bills trade 2-11 ticks lower through the reds.

- T-Notes blipped higher early on and stabilised thereafter. TYH2 last changes hands -0-03 at 127-13+. Eurodollar futures run 4.0-12.0 ticks lower through the reds. Tsy curve runs flatter in cash Tokyo trade, with yields last seen +3.0bp to -1.8bp. Advance GDP data, durable goods orders & weekly jobless claims headline the U.S. data docket today, with a 7-Year Tsy auction also due.

FOREX: Risk-Off Flows Sweep Across G10 FX Space After Fed's Hawkish Turn

The Fed's hawkish pivot turned the risk switch to off, driving defensive flows across the G10 FX space. Wednesday saw the FOMC set the scene for a March rate hike, while Fed Chair Powell signalled resolve in efforts to tackle elevated inflation, raising the prospect of a more aggressive tightening trajectory.

- Participants sought shelter in safe havens. USD/JPY printed a one-week high in early trade before trimming gains as demand for the greenback re-emerged. The DXY touched its best levels since Dec 20.

- Commodity-tied currencies went offered alongside crude oil futures, with the Antipodeans leading losses. The kiwi dollar was the worst performer, despite another beat in New Zealand's inflation data. Consumer prices in New Zealand grew 5.9% Y/Y in Q4, topping the median estimate & Nov MPS projection of 5.7%, as headline inflation reached the fastest pace since 1990. Meanwhile, the RBNZ's preferred measure of underlying inflation accelerated to +3.2% Y/Y, moving further above the mid-point of the Reserve Bank's target range. NZD/USD ignored domestic data and tumbled to its worst levels since early Nov 2020.

- Offshore yuan sank as the Asia-Pacific digested hawkish FOMC rhetoric. A slightly weaker than expected yuan fixing may have amplified selling pressure which helped the redback move further away from a new cycle high printed pre-FOMC on Wednesday.

- Today's data docket is rather U.S.-centric and includes local GDP, durable goods orders & jobless claims. Comments are due from ECB's Scicluna.

FOREX OPTIONS: Expiries for Jan27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1100(E524mln), $1.1150(E687mln), $1.1200-05(E692mln), $1.1250(E552mln)

- USD/JPY: Y113.00($761mln), Y113.50-60($867mln), Y114.80-00($1.1bln)

- GBP/USD: $1.3285-03(Gbp576mln), $1.3548-70(Gbp795mln)

- EUR/JPY: Y127.00(E1.1bln)

- AUD/USD: $0.7220(A$640mln)

- USD/CAD: C$1.2560-65($927mln)

- USD/CNY: Cny6.3450($560mln), Cny6.3500($1.3bln)

ASIA FX: Asia EM FX On The Back Foot As Post-FOMC Flows Kick In

The Fed's monetary policy decision delivered in U.S. hours Wednesday provided the key driver for USD/Asia crosses. Prominent hawkish overtones in the Fed's rhetoric inspired a risk sell-off

- CNH: Spot USD/CNH advanced sharply, moving away from a new cycle low printed pre-FOMC on Wednesday. A weaker than expected PBOC fix may have rubbed salt into the yuan's wounds, even as the miss was not too impressive. Still, it contrasted with a streak of virtually in-line fixings delivered over the past few days.

- KRW: Spot USD/KRW found itself within touching distance from Jan 7 cycle high of KRW1,203.90, as the won absorbed the impact of the Fed's policy announcement. Geopolitical goings-on provided another source of concern, as North Korea test-fired two ballistic missiles in its sixth missile drill this month.

- IDR: The rupiah remained on the back foot, even as Bank Indonesia Gov Warjiyo signalled that the central bank is currently preparing policy normalisation with the government. The official reiterated that the key policy rate will remain low until there are signs that inflation is picking up.

- MYR: The ringgit plunged to levels last seen on Jan 7, with spot USD/MYR piercing its 50-DMA in the process. Health Min Khairy warned that a wave of infections with the Omicron variant is beginning in Malaysia and he expects daily cases to rise over the coming days.

- PHP: Spot USD/PHP threatened to attack key resistance from PHP51.500, as the post-FOMC impulse outweighed above-forecast Q4 GDP data released out of the Philippines. Econ Planning Sec Chua said that the economy is on track to return to pre-pandemic levels this year.

- THB: The baht went offered amid speculation that the BoT might struggle to keep up with Fed tightening, as the critical tourism sector will take some time to recover.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 27/01/2022 | 0700/0800 | * |  | DE | GFK Consumer Climate |

| 27/01/2022 | 1100/1100 | ** |  | UK | CBI Distributive Trades |

| 27/01/2022 | 1330/0830 | ** |  | US | Jobless Claims |

| 27/01/2022 | 1330/0830 | ** | | US | durable goods new orders |

| 27/01/2022 | 1330/0830 | *** | | US | GDP (adv) |

| 27/01/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 27/01/2022 | 1330/0830 | * |  | CA | Payroll employment |

| 27/01/2022 | 1500/1000 | ** | | US | NAR pending home sales |

| 27/01/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 27/01/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 27/01/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 27/01/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.