Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

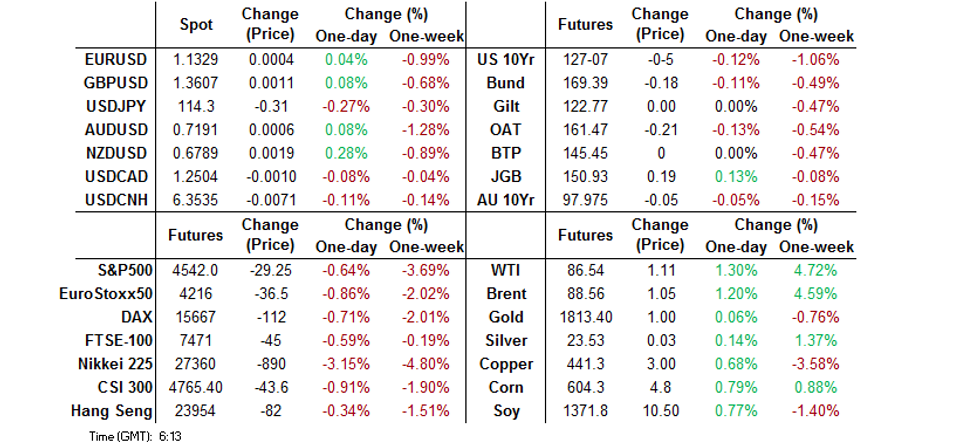

- The prospect of more aggressive monetary policy easing by the Fed keeps risk at bay. The yen catches bid on the back of risk aversion, with NZD showing resilience amid firm milk prices and hawkish RBNZ repricing.

- T-Notes and ACGBs extend recent losses but JGBs advance, after Tuesday's BoJ rhetoric underscored the growing policy divergence between the Fed and the BoJ.

- Crude oil futures extend gains to fresh cycle highs following the outage of a key Iraq-Turkey pipeline (it is set to resume operations shortly, per most recent updates).

BOND SUMMARY: JGBs Regain Poise After Confirmation Of BoJ/Fed Divergence, Tsys & ACGBs Extend Losses

Asia-Pac headline flow failed to add much to the familiar narrative, leaving familiar market dynamics in play, with focus on the policy outlooks of major central banks.

- Selling pressure hit T-Notes from the off, pushing the contract to fresh cycle lows. TYH2 edged away from worst levels (127-03+) in the Tokyo afternoon and last changes hands -0-06 at 127-06. Eurodollar futures operate 0.5-4.5bp lower through the reds. Cash Tsy curve continued to bear flatten in Asia, with the 20-Years outperforming ahead of today's auction of that tenor. The yield on 30-Year Tsys crossed above the 2.2% mark for the first time since June amid fresh cycle highs for yields across the curve. The U.S. data docket is limited to housing starts & building permits, with the main focus set to fall on aforementioned debt supply.

- Aussie bonds clung onto the tailcoats of faltering U.S. Tsys in cash Sydney trade, with yields last seen 3.2-5.5bp higher, albeit the ACGB curve has steepened a tad. The yield on 10-Year ACGBs showed above 2.0% for the first time since Oct. Main futures contracts wavered, with YM last -4.0 & XM -6.0. Bills trade 2-4 ticks lower through the reds. Westpac Consumer Confidence Index posted a somewhat surprisingly modest downtick but the ACGB space showed a limited reaction, with an auction for A$500mn of 2.75% 21 Jun '35 Bonds also largely shrugged off.

- JGB futures clawed back their initial losses and crept higher, extending gains after the Tokyo lunch break. JBH2 trades at 150.85 at typing, 11 ticks above last settlement and 2 ticks below session highs. Cash JGB curve steepened a tad, with yields easing across the curve, save for the super-long end. The BoJ yesterday gave a clear indication that they are keen to stick to their ultra-loose policy stance, which sets them apart from U.S. colleagues. Japan auctioned 1-Year Bills and conducted a liquidity enhancement auction for off-the-run JGBs with 1-5 years until maturity.

FOREX: Yen Benefits From Risk Aversion, Kiwi Firms On Hawkish RBNZ Bets

The yen swung from losses to gains as market sentiment turned sour, with Asia-Pac equity benchmarks retreating amid lingering angst surrounding the looming withdrawal of stimulus by the Fed. Spot USD/JPY lost altitude after charting a Doji candlestick on Tuesday.

- The NZD caught a bid as participants added hawkish RBNZ bets, with money markets now pricing ~31bp worth of tightening come the end of the Feb MPC meeting. ANZ revised their RBNZ call, noting that they expect the OCR to peak at 3% in Apr '23 rather than at 2% in 2H2022 as inflation pressures remain. Rising milk prices may have lent some additional support to the kiwi after a strong GDT auction held on Tuesday.

- The U.S. dollar lost shine and fared worse than most of its major peers, with the DXY slipping from a one week-high printed Tuesday. This helped spot USD/CNH edge lower, even as the PBOC pledged to use more monetary policy tools.

- German, UK & Canadian inflation data, U.S. housing starts & building permits as well as comments from ECB's Holzmann & BoE officials take focus from here.

FOREX OPTIONS: Expiries for Jan19 NY cut 1000ET (Source DTCC)

- USD/JPY: Y114.50-55($585mln), Y115.00($512mln)

- AUD/USD: $0.7245-50(A$535mln)

NEW ZEALAND: 10-Year NZGB Yield Prints Best Levels Since Nov As Hawkish RBNZ Bets Are Added

Participants have seemingly been adding some hawkish RBNZ bets today, with the implied change in the OCR come the end of February MPC meeting edging higher to just over 30bp. It is the first time this year that money markets are pricing that much tightening in February, with modest upticks observed also further out the curve.

- Bloomberg have telegraphed an analytical note from ANZ, who said they now expect the OCR to peak at 3% by April 2023. They previously projected the OCR rising to a peak of 2% in 2H2022, but "domestic inflation pressures, and in particular the ongoing tightness in labour supply" prompted them to tweak their call.

- NZIER's Quarterly Survey of Business Opinion released yesterday underscored continued "acute labour shortages," which fuel a "lift in wage growth, and this is contributing to higher costs for businesses." The survey pointed to "inflation pressures in the New Zealand economy remaining strong over the coming year."

- Note that New Zealand's Covid-19 Response Minister Hipkins today suggested that the government could again delay border reopening, as officials rush to administer booster jabs to the population before Omicron penetrates the community. Pressing pause on border reopening would exacerbate existing labour shortages through a continued halt on the supply of foreign workers.

- The yield on the 10-year NZGB climbed to its best levels since November and closed just shy off there at 2.595%. The kiwi dollar is among the best G10 performers, with NZD/USD last +17 pips at $0.6788.

ASIA FX: Hawkish Fed Musings Undermine Asia FX, Yuan Shows Resilience

Currencies from the Asia EM basket were broadly weaker, coming under pressure from rising U.S. Tsy yields as money markets are pricing sooner and bolder tightening steps from the Fed.

- CNH: Spot USD/CNH traded with a mild bearish bias, with the PBOC providing another in-line fixing of the yuan reference rate. Separately, PBOC Dep Gov Liu pledged a more pro-active stance and said that the People's Bank will use more monetary policy policy tools to support growth. He mentioned that the PBOC will not allow one-way moves in the yuan, although this comment did not appear in the official transcript from.

- KRW: Spot USD/KRW crept higher in the wake of the overnight surge in U.S. Tsy yields. South Korea's daily cases topped 5,000 for the first time in 20 days.

- IDR: Spot USD/IDR jumped to its highest point in almost two weeks, with Tuesday's upswing in U.S. Tsy yields in the driving seat. Participants eyed Bank Indonesia monetary policy decision, due tomorrow.

- MYR: Bank Negara Malaysia will also make a policy announcement on Thursday. Spot USD/MYR crept higher as onshore Malaysian markets re-opened after a holiday.

- PHP: Spot USD/PHP showed above the PHP51.50 mark for the first time since Mar 18, 2020. Covid-19 headlines continued to dominate domestic news flow.

- THB: The Thai baht retreated as the prospect of more aggressive Fed tightening jumped into the driving seat, stealing attention from Thailand's plan to reinstate the quarantine-free travel programme as soon as in Feb.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/01/2022 | 0001/0001 | * |  | UK | XpertHR pay deals for whole economy |

| 19/01/2022 | 0700/0800 | *** |  | DE | HICP (f) |

| 19/01/2022 | 0700/0700 | *** | | UK | Producer Prices |

| 19/01/2022 | 0700/0700 | *** | | UK | Consumer inflation report |

| 19/01/2022 | 0900/1000 | ** |  | EU | EZ Current Acc |

| 19/01/2022 | 0930/0930 | * | | UK | ONS House Price Index |

| 19/01/2022 | 1000/1100 | ** | | EU | construction production |

| 19/01/2022 | 1200/0700 | ** |  | US | MBA weekly applications index |

| 19/01/2022 | 1330/0830 | *** |  | CA | CPI |

| 19/01/2022 | 1330/0830 | ** | | CA | Wholesale Trade |

| 19/01/2022 | 1330/0830 | *** | | US | Housing Starts |

| 19/01/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 19/01/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.