Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The BoJ remains the last dove standing, with no major changes announced at today's policy meeting. Inflation forecasts were revised higher, but next financial year are still expected to be sub 2%. In any case, the tone among major central banks is already turning more dovish, or at least opening the path to a reduced pace of tightening.

- China/HK equities resumed their downtrend today, amid fresh tech weakness, with earnings results disappointing, while the US administration is considering expanding curbs to tech exports to China. Most major equity indices were lower today in the region, but spillover to broader asset sentiment was limited.

- Still to come, economic and industrial confidence will print for the Euro area. In the US, the main focus will be on the PCE deflator, along with U. of Mich Consumer sentiment.

US TSYS: T-Notes Turn Heavy, Cash Curve Bear Flattens

T-Notes ground lower through the Asia-Pac session, even as a slew of weak earnings reports from U.S. tech giants this week generated weakness in NASDAQ 100 e-minis, which kept a lid on local equity-index futures. The move may have represented a correction of yesterday's dynamic advance, driven by a "dovish hike" from the ECB and underwhelming U.S. core PCE & durable goods data. A sudden, now mostly unwound post-BoJ drop in JGBs may have added pressure to core FI peers.

- T-Notes last trade -0-01 at 111-21, hovering just above 111-19 session low. Eurodollar futures run 1-8 ticks higher through the reds. Cash Tsy curve bear flattened, with yields last seen 0.9-3.1bp higher. The 5-Year/30-Year sector has moved closer to inversion territory, as the relevant spread sits at less than 1bp.

- With participants digesting the BoJ's monetary policy statement and outlook report, focus turns to the upcoming press conference with Gov Kuroda.

- U.S. data highlights today include employment cost index, personal income/spending, pending home sales & final Uni. of Mich. survey.

JGBS: Benchmark Futures Tumble Post-BoJ But Quick Rebound Ensues, Gov Kuroda's Presser Eyed

JGBs were volatile as the BoJ's monetary policy review took centre stage. Benchmark futures climbed to a session high of 148.95 in morning trade, but tumbled as trading restarted after the lunch break. During the pause in trading, the Policy Board announced the outcome of its unanimous vote to leave all key monetary policy parameters and dovish forward guidance unchanged, while tweaking the economic forecasts, sharply raising the inflation outlook and charting a flatter growth trajectory.

- Futures slumped to a session low of 148.41 in response to the BoJ's statement before a reassessment of the decision brought a rebound. The contract last deals at 148.66, unch. versus previous settlement.

- All eyes will are on Gov Kuroda's presser (15:30 JST/07:30 BST). His dovish briefing last month inspired aggressive yen sales, which led to Japan's first FX intervention to shore up its currency since 1998.

- Tokyo core CPI inflation, a bellwether of nationwide price dynamics, accelerated to the fastest pace since late 1980s, but the BoJ still sees the outcome as transitory, driven by temporary cost-push factors rather than the desired growth in wages.

- Ahead of the BoJ announcement, PM Kishida unveiled an Y29.1tn fiscal package designed to mitigate the impact of inflationary pressures.

- Cash JGB yields are lower across the curve, save for 5s, with curve flatter on the back of outperformance in the super-long end. 10s pulled back from the BoJ's 0.25% yield cap.

AUSSIE BONDS: Early Gains Pared, ACGB Nov-32 Sale Causes Little Reaction

ACGBs pulled back from highs, losing ground alongside U.S. Tsys as the session progressed. The sale of ACGB Nov-32 came and went, while the release of the AOFM's weekly issuance slate coincided with a brief bout of increased volatility.

- The auction of a Nov' 32 note drew a bid/cover ratio of 2.38x, down from 3.19x at the previous offering, while the tail widened. The yield on that tenor in secondary market sits at 1.42%, with little in the way of reaction to the auction today.

- The AOFM outlined its plans to hold just one bond auction next week, offering A$800mn of ACGB Nov-28 next Wednesday. It also outlined plans to issue a new May-34 Bond via syndication in the week beginning Nov 7.

- Local data were shrugged off, with PPI inflation quickening to +6.4% Y/Y in Q3 from +5.6% prior. This comes after an expectation-busting CPI report published earlier this week.

- Benchmark futures contracts have virtually unwound early gains, with YM last +8.0 & XM +6.0 as YMXM sits +1.5. Bills run 3-10 ticks higher through the reds.

- ACGB curve still runs slightly steeper, with yields last 7.0-5.2bp lower. 3-Year/10-Year differential has tightened at the margin.

- Swaps still fully price a 25bp rate hike from the RBA at next week's Board meeting.

AUSSIE BONDS: ACGB Nov-32 Auction Results

The Australian Office of Financial Management (AOFM) sells A$800mn of the 1.75% 21 November 2032 Bond, issue #TB165:

- Average Yield: 3.7520% (prev. 4.0029%)

- High Yield: 3.7575% (prev. 4.0050%)

- Bid/Cover: 2.3813x (prev. 3.1938x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 5.3% (prev. 62.1%)

- Bidders 39 (prev. 42), successful 21 (prev. 11), allocated in full 16 (prev. 6)

AUSSIE BONDS: AOFM Weekly Issuance Slate

The AOFM has released its weekly issuance slate:

- On Wednesday 2 November it plans to sell A$800mn of the 2.75% 21 November 2028 Bond.

- On Thursday 3 November it plans to sell A$1.0bn of the 10 February 2023 Note, A$500mn of the 24 February 2023 Note & A$500mn of the 14 April 2023 Note.

- It also notes that subject to market conditions, a new May 2034 Treasury Bond is planned to be issued via syndication in the week beginning 7 November 2022. Further details of the issue will be announced next week.

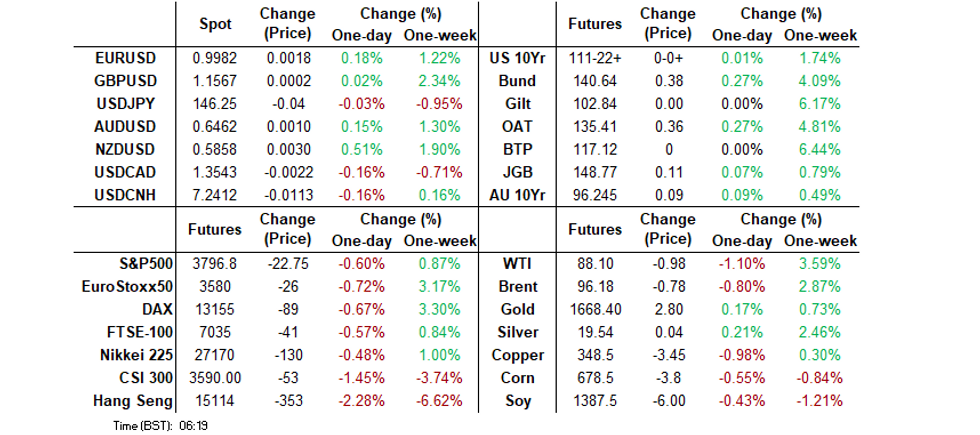

FOREX: JPY Underperforms Weaker USD Backdrop

The USD is lower, with the BBDXY back to 1321, moves up towards 1325 faded by the market. We haven't broken back strongly back below the simple 50-day MA though (1320.82). JPY has lagged the broader USD sell-off as the BOJ held steady.

- USD/JPY was volatile around the BoJ announcement, spiking towards 147.00, before slumping back to 146.00. As expected, no major changes to policy parameters were announced, while inflation forecasts were revised higher, but remain comfortably sub 2.0% for next financial year. The pair last sits around 146.25.

- EUR/USD has firmed back towards parity, last 0.9985. An initial catalyst was lower UST 2yr yields, which dipped below overnight lows, but EUR has held gains even as yields recovered (last 4.30%).

- NZD/USD has outperformed, up 0.60%, although has seen selling resistance above 0.5870. NZD/USD has lagged, up +0.30% to 0.6470. Fresh declines in iron ore (sub $80/tonne) not weighing materially. Both currencies though have outperformed the weaker tone from US/Regional equities.

- Coming up, German NRW CPI is still yet to print, while economic and industrial confidence will print for the Euro area. In the US, the main focus will be on the PCE deflator, along with U. of Mich Consumer sentiment.

ASIA FX: USD/Asia Pairs Lower, China PMIs Print Monday

USD/Asia pairs are mostly lower, in line with USD softness against the majors. This comes despite negative cross asset leads, with major regional equity indices lower, while UST yields recovered from earlier lows. Next Monday official China PMI prints for October are due. The focus is likely to be on whether the services sector can remain in expansion territory (consensus is 50.1 versus 50.6 last month). The manufacturing PMI is expected to slip to 49.9 from 50.1 prior.

- USD/CNH couldn't get above 7.2700, despite a fresh cyclical higher in the fix (near 7.1700). We last sat back under 7.2400, shrugging off weaker equity market sentiment. The market is likely to watch for potential shadow intervention again ahead of the 4:30pm onshore spot closing level.

- 1 month USD/KRW is sub 1420, although dips towards 1415 were supported, keeping us within recent ranges. The Kospi is lower (-0.55%) amid tech headwinds from the US, while offshore investors have sold local shares today (-$142.1mn so far). The authorities expect some relief for next week's CPI print (5% handle expected for the second consecutive month).

- Spot USD/IDR has shed 40 figs so far as the greenback underperforms. We were last at 15528, with bears looking for a move towards Oct 5 low of IDR15,162, while bullish focus falls on Oct 21 cycle high of IDR15,634. The next local data release of note is October CPI report, due November 1.

- PHP has continued to firm. USD/PHP is back to 57.86, -0.37 figs for the session. The 50-day MA sits at 57.787. We continue to move away the 59.00 figure level. Fitch affirmed the Philippines at "BBB" with a negative outlook, noting that this reflects the nation's medium-term growth prospects, fiscal adjustment path and external buffers.

- USD/THB is also trending lower, last at 37.685, -0.13 figs. Foreign investors were net buyers of $65.11mn in Thai stocks Thursday, representing a fifth consecutive day of inflows amid renewed offshore demand. The BoT will publish the weekly update on foreign reserves today. The stack of foreign reserves shrank in the week through Oct 14 to the lowest level since early Sep 2017.

EQUITIES: HK/China Downtrend Resumes

Major Asia Pac equity indices are lower, following negative overnight leads from US markets and weaker futures since the open. Amazon's profit result disappointed, while Apple presented mixed results (iPhone sales weaker than expected). Futures are away from worst levels though, with Eminis holding above 3800.

- The tech backdrop weighed on the HSI, which is down 2.3% currently, with the tech sub index down 4.2%. Both these indices are on track for weekly losses. The US Administration is reportedly considering expanding its curbs on technology related exports to China.

- In China, the CSI is off 1%, with a continued rise in local covid case numbers weighing, and on-going lockdowns in parts of the country. Building stocks were lower, even as the PBoC called on support for bond sales of local property developers.

- South Korea (-0.50%) and Taiwan (-0.90%) are down, weighed by tech headwinds. Sk Hynix amongst the worst performers for the Kospi. Offshore investors have also sold $127.5mn of local stocks so far today.

- The ASX 200 is down around 1%, weighed by miners amid the continued fall in iron ore prices (last just under $80/tonne). Japan stocks were mixed, as the BoJ left policy parameters unchanged, while fiscal stimulus efforts step up.

- Singapore shares are up 1.85%, a one bright spot for the region, as local bank UOB posted solid Q3 earnings.

GOLD: Trying To Post Another Weekly Gain

Gold is little changed from levels that prevailed this time yesterday. The precious metal is around $1664 currently, near the middle of the $1655/$1675 range for the past few sessions.

- We are trying to post another weekly gain (currently +0.40%, last week was +0.80%).

- Dips overnight to $1655 were supported, despite the rebound in broad USD performance. Still, gold lags the correction in the USD seen since the middle of the month, so may be less sensitive to such shifts in the near term.

- The other overnight support came from lower US real yields, with the 10yr slipping back to 1.51%, from 1.60%. This is lows back near the start of the month.

- We saw fresh downside momentum in nominal UST yields today, but sentiment has now stabilized. The 2yr back to 4.29%, +2bps for the session.

OIL: Off Highs, But Still On Track For Solid Weekly Gains

Brent crude is down -0.80% from NY closing levels, last in the low $96/bbl region. This follows two sessions of strong gains, and we are still +2.87% on closing levels from the end of last week. Overnight highs around $97.30 were fresh highs going back to October 10. WTI is following a similar trajectory, last just above $88/bbl, but still +3.5% higher for the week. On-going tight supplies, coupled with a USD pull back, have aided crude sentiment.

- In terms of headline flow, US President stepped up his criticism of energy companies (after Shell's bumper profit result). This comes as domestic gasoline prices are trending higher, amid low inventories. The energy price issue is seen as important one for the Democrats ahead of the upcoming mid-term elections.

- Energy Ministers from Saudi Arabia and France stated the need to increase oil market stability, per Bloomberg reports. Both sides agreed to strengthen relations to secure supplies for global markets.

- Next week we get an update on China domestic demand conditions with official PMI prints on Monday. Bloomberg will publish a survey of OPEC crude production for October on Tuesday, we will also get the API report. Then on Wednesday is the EIA weekly report, along with the main macro event risk for the week, the Fed decision.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/10/2022 | 0430/0630 | *** |  | DE | North Rhine Westphalia CPI |

| 28/10/2022 | 0530/0730 | ** |  | FR | Consumer Spending |

| 28/10/2022 | 0530/0730 | *** | | FR | GDP (p) |

| 28/10/2022 | 0600/0800 | *** |  | SE | GDP |

| 28/10/2022 | 0600/0800 | ** | | SE | Retail Sales |

| 28/10/2022 | 0645/0845 | *** | | FR | HICP (p) |

| 28/10/2022 | 0645/0845 | ** | | FR | PPI |

| 28/10/2022 | 0700/0900 | *** |  | ES | GDP (p) |

| 28/10/2022 | 0700/0900 | *** | | ES | HICP (p) |

| 28/10/2022 | 0700/0900 | * |  | CH | KOF Economic Barometer |

| 28/10/2022 | 0800/1000 | *** | | DE | GDP (p) |

| 28/10/2022 | 0800/1000 | *** | | DE | Bavaria CPI |

| 28/10/2022 | 0800/1000 | ** |  | IT | PPI |

| 28/10/2022 | 0900/1100 | *** | | IT | HICP (p) |

| 28/10/2022 | 0900/1100 | ** |  | EU | Economic Sentiment Indicator |

| 28/10/2022 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 28/10/2022 | 0900/1100 | * | | EU | Business Climate Indicator |

| 28/10/2022 | 0900/1100 | *** | | DE | Saxony CPI |

| 28/10/2022 | 1030/1330 |  | RU | Russia Central Bank Key Rate Decision | |

| 28/10/2022 | 1200/1400 | *** | | DE | HICP (p) |

| 28/10/2022 | - | *** |  | JP | BOJ policy announcement |

| 28/10/2022 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 28/10/2022 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 28/10/2022 | 1230/0830 | ** | | US | Employment Cost Index |

| 28/10/2022 | 1400/1000 | ** | | US | NAR pending home sales |

| 28/10/2022 | 1400/1000 | *** | | US | Final Michigan Sentiment Index |

| 28/10/2022 | 1500/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.