Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The PBOC injects net CNY90bn via OMOs amid liquidity concerns related to the ongoing Evergrande saga, the upcoming Chinese long weekend as well as the week-long holiday coming up at the turn of the quarter.

- JPY on the back foot ahead of two local public holidays next week, NZD struggles after the release of BusinessNZ Manufacturing PMI. Major FX crosses hold tight ranges.

- Core FI tread water, with ACGB Apr '33 supply well absorbed.

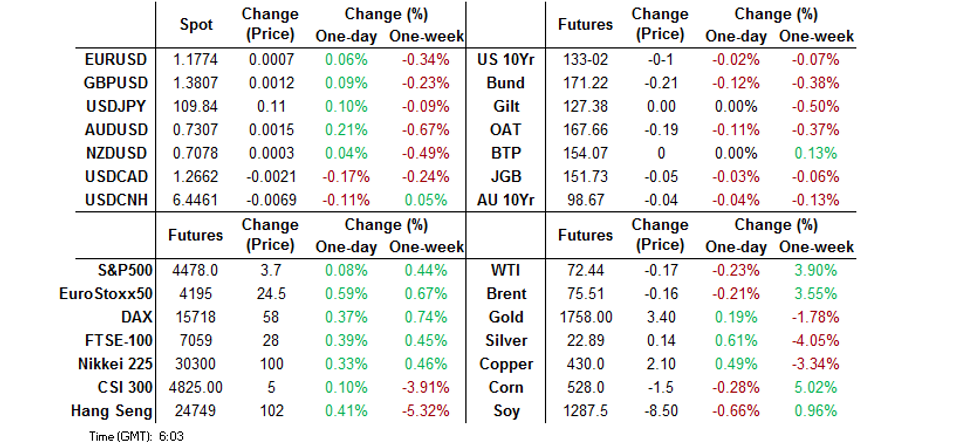

BOND SUMMARY: Core FI Happy To Hug Tight Ranges, ACGB Supply Well Received

T-Notes -0-01 at 133-02 at typing. The contract traded sideways, sticking to the confines of a 0-03 range. Cash Tsy curve runs flatter, with yields last seen flat to 0.9bp richer across the curve. Eurodollars sit +0.5 to -0.5 tick through the reds. Fiscal headwinds remain apparent, with Axios circulating a report pointing to a lack of breakthrough on that front, after talks between Pres Biden & key Democratic Senator Manchin yielded no progress. The preliminary reading of University of Mich. Sentiment takes focus from here.

- JGB futures ground higher initially, topped out at 151.75 and eased off into the Tokyo lunch break. The contract last sits at 151.71, 7 ticks shy of previous settlement. Cash JGB yields are marginally mixed. Official campaigning for LDP leadership election kicks off today, while Japan will observe a public holiday on Monday.

- Aussie bond futures held tight ranges, YM last trades -1.5, with YM -3.5. Cash ACGB yield curve has bear steepened, albeit yields have eased off initial highs. Bills run unch. to -2 ticks through the reds at typing. The supply of ACGB Apr '33 was well received by the market, as the dynamics surrounding relative appeal and expectations for the bond to outperform into XMH2 basket inclusion seemingly outweighed the headwinds touted ahead of the supply.

FOREX: NZD, JPY Underperform In Muted Trade

The Asia-Pacific docket lacked tier 1 risk events, while headline flow was relatively limited, keeping volatility in G10 FX space subdued. NZD edged lower after New Zealand's BusinessNZ Manufacturing PMI plunged deep into contraction following the implementation of Covid-19 restrictions in August. NZD/USD tested yesterday's low of $0.7060 but that level provided a formidable layer of support.

- New Zealand's Manufacturing PMI fell to 40.1 from 62.2, with accompanying commentary noting that "GDP and manufacturing output are expected to fall heavily in Q3," which is something of a reality check in the afterglow of yesterday's very strong Q2 GDP outcome".

- The yen went offered against most of its G10 peers, with Japan set to observe public holidays next Monday and Thursday.

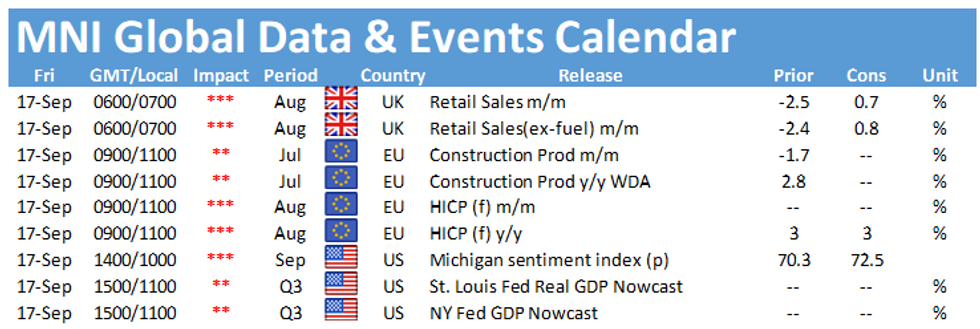

- Final EZ CPI and UK retail sales take focus in European hours, with flash U.S. University of Mich. Sentiment coming up later in the day. ECB's Makhlouf will speak at a workshop on inflation.

ASIA FX: Won Leads Losses Ahead Of Chuseok Holidays

Most USD/Asia crosses remained on the front foot due to the afterglow of strong U.S. retail sales data released yesterday, with market holidays in China and South Korea eyed next week.

- CNH: USD/CNH popped higher but gradually retraced that uptick, returning to neutral levels. The PBOC set their central USD/CNY mid-point at CNY6.4527, 7 pips above sell-side estimate, and injected net CNY90bn via OMOs, citing the need to keep liquidity stable ahead of the quarter-end. Note that China will observe a public holiday through Tuesday, with another week-long holiday coming up at the beginning of October, while the ongoing Evergrande saga continues to inspire concerns over repercussions for liquidity.

- KRW: South Korean markets are also set to shut in the early part of next week, owing to the upcoming Chuseok holiday. Local health officials fear a potential flare-up in Covid-19 cases, as the festive season is typically associated with higher travel activity. The won was the worst performer in the Asia EM basket, as cautious mood lingered. Spot USD/KRW printed its best levels since Aug 20, when it hit the latest cycle peak.

- IDR: The rupiah started on a softer footing but managed to recoup losses. USD/IDR tested its 200-DMA but failed to stage a convincing break above that moving average.

- MYR: The ringgit was among the weakest performers in the region, as the currency played catch up with market flows seen yesterday, when onshore markets were closed in observance of Malaysia's birthday.

- PHP: USD/PHP gave away its initial gains. The Dept of Health said that Metro Manila will remain under Alert Level 4 (under the new 5-level system) through the month-end, even as OCTA Research Group reported a dip in the virus reproduction rate in the capital region.

- THB: Spot USD/THB registered its strongest levels since Aug 24, holding gains after a firmer reopen. Daily Covid-19 cases rose for the third straight day, with participants assessing health risks related to the planned reopening of Bangkok and several other regions in October.

- SGD: USD/SGD crept higher, having a look above yesterday's high. Singapore's non-oil domestic exports data were mixed, as a miss in headline figure was coupled with a beat in electronic shipments.

GOLD: Finally Out Of The Narrow Range

A flat start to Asia-Pac trade for spot gold, last dealing little changed at $1,755/oz.

- A firmer USD and uptick in our weighted U.S. real yield monitor allowed gold to break out of its recent range on Thursday, with firmer U.S. retail sales data proving decisive on the day. Still, bears only managed to force a very shallow and minor breach below the 61.8% retracement of the Aug 9-Sep 3 rally, with Thursday's low ($1,745.3/oz) now providing the initial point of support. A move below there would allow bears to target the 76.4% retracement of the same Aug 9-Sep 3 rally ($1,724.5/oz). Initial resistance has moved to the Sep 14 low ($1,781.8/oz).

- Note that known ETF holdings of gold have operated in a sideways fashion in recent weeks, hovering just above the post-COVID lows witnessed in April, with that particular metric last sitting 10.4% off of the all-time highs seen in October '20.

- Participants await next week's FOMC decision, which will see focus fall on any commentary surrounding the tapering of the central bank's QE programme.

OIL: Little Movement Early In Asia

WTI and Brent crude futures sit a handful of cents lower on the day at typing, after finishing little changed on Thursday. The supply side headwinds that we flagged on Thursday (notably surrounding U.S. Gulf production coming back online, albeit slowly, and Libyan exports returning) provided some pressure for crude through early NY trade, with the usual round of profit-taking talk and uptick in the USD also weighing. Still, a recovery in U.S. equity indices as we moved through the day seemed to allow crude to end the session on a near enough neutral footing.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.