Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

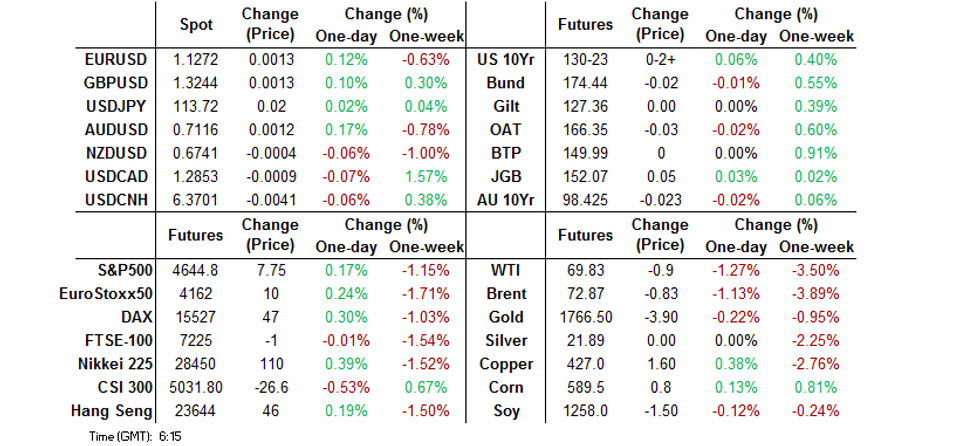

- T-Notes edge higher and the DXY wavers ahead of the announcement of monetary policy decision of U.S. FOMC.

- Asia-Pac equity indices are mixed, with Omicron risks and simmering Sino-U.S. tensions in the background.

- The PBOC roll over CNY500bn via MLF, only partially offsetting CNY950bn coming due, in line with expectations. The interest rate applied to the operations remains unchanged.

BOND SUMMARY: Tsys Post Marginal Gains Pre-FOMC, Flattening Hits Cash ACGB Curve

All eyes were on the impending announcement of the monetary policy decision from U.S. Fed, with continued assessment of Omicron risks and simmering Sino-U.S. tensions in the background.

- T-Notes ground higher, albeit very reluctantly. They last change hands +0-02 at 130-22+. Cash Tsy yields sit 0.2-0.9bp lower across the curve, with belly outperforming at the margin. Eurodollar futures last trade unch. to +1.0 tick through the reds. Note that U.S. retail sales & Empire M'fing Survey will hit the wires today, albeit they will be overshadowed by the latest showing from FOMC members.

- JGB futures went bid, topping out at 152.09 after the Tokyo lunch break. They last trade at 152.07, 5 ticks above previous settlement. Cash JGB yields sit slightly lower across the curve. The final reading of Japan's Oct industrial output was revised higher, while the BoJ conducted Rinban ops covering 1-10 & 25+ Year JGBs, but the JGB space was unfazed. BoJ Gov Kuroda told lawmakers that policymakers intend to continue persistently with its monetary stimulus.

- Overnight impetus weighed on cash ACGBs in early trade, with the short-end extending losses later on, which was paralleled by a recovery in the longer-end. This flattening dynamic leaves us with yields sitting 1.3-6.3bp higher across the curve. YM last trades -3.8 & XM -2.3, while bills run 2-6 ticks through the reds. Aussie bonds shrugged off a marginal deterioration in Westpac Consumer Confidence, as headline index remained in positive territory. Across the Tasman, NZGBs went bid after New Zealand slashed planned debt issuance over the next four years, but there was no real follow-through in ACGBs.

FOREX: Major FX Pairs Rangebound, All Eyes On Fed

Most G10 crosses were happy to hold narrow ranges ahead of today's monetary policy announcement from the Fed, who are expected to take a more hawkish stance, which should be reflected in a faster asset purchase taper, a more aggressive rate dot lot and tweaks to the language. The DXY wavered in close proximity to yesterday's high.

- The kiwi has underperformed at the margin as New Zealand's quarterly BoP current account deficit expanded more than forecast in the three months through the end of September. RBNZ Gov Orr did not offer any fresh insights in his latest address, noting that the OCR will likely move above its neutral level at some point. The Treasury's HYEFU showed improvement in debt outlook, with the Debt Management Office slashing their bond issuance plans for the next four years.

- The yuan showed little interest in China's economic activity data, which were (on balance) slightly weaker than expected. Industrial output rose marginally faster than expected but retail sales growth slowed more than forecast. Fixed assets and property investment missed expectations by a narrow margin, while the unemployment rate unexpectedly edged higher to 5.0% from 4.9%.

- Inflation reports from the UK, France, Italy and Canada as well as U.S. retail sales & Empire M'fing will take focus on the data front later in the day.

FOREX OPTIONS: Expiries for Dec15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200-15(E1.0bln), $1.1300(E670mln), $1.1350(E529mln), $1.1400(E2.2bln)

- USD/JPY: Y112.95-05($1.1bln), Y113.75-80($1.5bln), Y113.90-05($1.1bln), Y114.20($1.1bln)

- GBP/USD: $1.3235-50(Gbp705mln)

- EUR/GBP: Gbp0.8575-80(E811mln)

- AUD/USD: $0.7275(A$544mln)

ASIA FX: Calm Ahead Of Fed Decision, Chinese Data Fail To Move Needle

Most USD/Asia crosses were happy to hug tight ranges as participants awaited the upcoming monetary policy decision from the Fed, while Chinese activity data failed to move the markets.

- CNH: Spot USD/CNH stabilised in negative territory after meandering in early trade. The yuan shrugged off the latest batch of data out of China, which was fairly underwhelming. The slowdown in retail sales growth was more pronounced than expected and the unemployment rate edged higher, even as industrial output was marginally firmer than forecast. China's new home prices fell for the third straight month in November amid the ongoing crisis engulfing the local property market. Elsewhere, the PBOC rolled over CNY500bn of MLF loans, which generated a net drain of CNY450bn, holding the rate applied to the operations steady.

- KRW: Spot USD/KRW crept higher as PM Kim announced that the government considers tightening social distancing measures, to be unveiled on Friday. The authorities could limit restaurant and cafe operating hours and lower caps on private gatherings as critical Covid cases continue to surge, putting a severe strain on medical capacity. The won was the worst performer in the region.

- IDR: Spot USD/IDR pared its initial gains through the session. Indonesia's trade surplus shrank in November, as imports picked up more than expected.

- MYR: Spot USD/MYR reversed its initial gains. Domestic headline flow was fairly limited.

- PHP: The Philippine peso reopened on a firmer footing, after the government raised their 2021 GDP growth forecast and projected narrowing budget deficits going forward.

- THB: Spot USD/THB traded sideways. The World Bank said they expect Thai economic activity to return to pre-Covid levels by end-2022.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.