Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The RBNZ left rates at 5.5% at its October meeting which was widely expected. There was a tweak to the end of the statement saying that policy needs to remain restrictive for “a more sustained period of time” rather than “the foreseeable future”. This may be implying that rather than increase rates further, policy may stay tight longer than is currently expected.

- RBNZ dated OIS pricing is 4-8bps softer across meetings beyond October. In the FX space, NZD underperformed, but is up from session lows.

- Elsewhere, cash tsys are flat to 5bps cheaper across benchmarks, as the bear-steepening seen in yesterday's NY session extends into the Asia-Pac session. The BBDXY nearly got to 1280, but sits slightly lower now. Japan officials refused to confirm if they intervened in FX markets yesterday.

- Looking ahead, we have some ECB speak, headlined by Lagarde. Final September PMIs are due in the EU. Later the Fed’s Bowman and Goolsbee speak. There is also a swathe of US data including ADP September employment, September services PMI/ISM and final August durable goods orders.

MARKETS

US TSYS: Bear Steepening Extends Into Asia-Pac Dealings

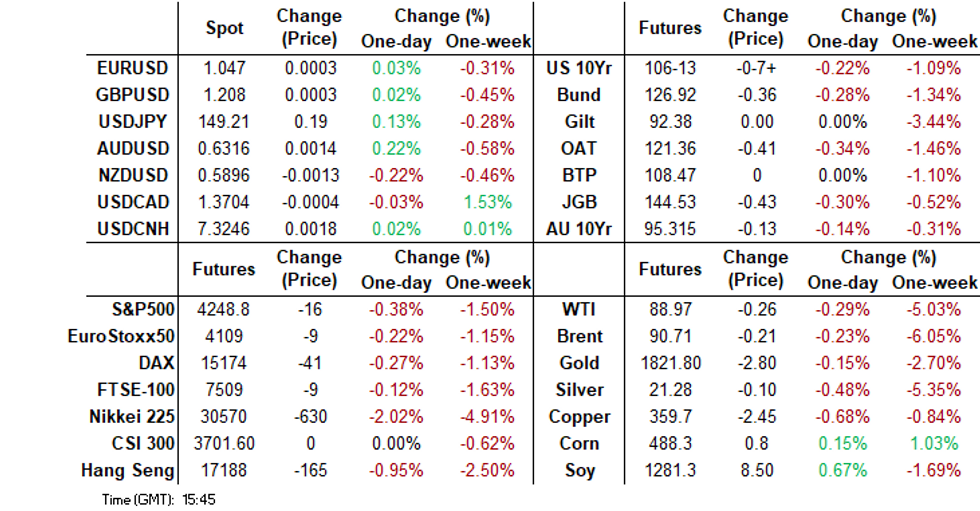

TYZ3 is currently trading at an Asia-Pac session low of 106-12+, -0-08 from NY closing levels.

- Cash tsys are flat to 5bps cheaper across benchmarks, as the bear-steepening seen in yesterday's NY session extends into the Asia-Pac session.

- There haven’t been any meaningful headlines so far in the Asia-Pac session, other than the US House of Reps voting to oust speaker McCarthy.

- Bloomberg reports that investors are positioning for the US tsy 10-year to exceed 5.0%. Most of the options action centred on November and December expiries, which have seen a jump in open interest across a number of put-option strikes equivalent to a 5% yield and higher. (See link)

- Later today sees a slew of US economic releases, including ADP Private Employment and ISM Services.

JGBS: Futures At Session Lows, JGB Curve Bear Steepens

In the Tokyo afternoon session, JGB futures are weaker and near session lows, -37 compared to settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Jibun Bank Services and Composite PMIs.

- Accordingly, JGBs have likely found direction from US tsys, which have extended overnight weakness. Cash tsys are flat to 5bps cheaper across benchmarks, as the NY session’s bear-steepening extends into the Asia-Pac session.

- The cash JGB curve has bear-steepened, with yields 0.7bp to 3.8bps (20-year) higher. The 30-40-year zone is 2.1-2.9bps cheaper. The benchmark 10-year yield is 2.2bps higher at 0.788%, above BOJ's YCC soft limit of 0.50% but below its hard limit of 1.0%. It is also slightly below the cycle high of 0.798% set earlier today.

- Bloomberg noted that Japan’s 10-year OIS has risen to 1% for the first time since January amid growing speculation the central bank will end its negative interest rate, which caused a spike in sovereign long-term yield. (See link)

- The swap curve has also bear-steepened, with rates 0.5bp to 4.0bps higher. Swap spreads are generally wider, apart from the 7-20-year bucket.

- Tomorrow the local calendar sees International Investment Flow data, along with 30-year supply.

AUSSIE BONDS: Bear Steepening As Longer-Dated US Tsy Yields Push Higher In Asia-Pac

ACGBs (YM -5.0 & XM -12.5) have experienced significant weakness, primarily driven by the long end, as the bearish steepening of the US tsy curve extended into the Asia-Pac session. US tsys are flat to 5bps higher across benchmarks, with a steepening of the yield curve.

- On the other hand, shorter-term ACGBs have displayed better performance, partly due to an RBNZ that appeared less hawkish than anticipated. As expected, the RBNZ maintained the OCR at 5.50% but hinted at the possibility of keeping policy tight for a longer duration rather than tightening it further.

- (AFR) A surge in long-term bond yields has driven the Australian dollar to an 11-month low and may force Reserve Bank of Australia governor Michele Bullock to deliver further cash rate rises, economists say. (See link)

- Cash ACGBs are 5-12bps cheaper, with the AU-US 10-year yield differential 2bps lower at -18bps.

- Swap rates are 7-14bps higher, with the 3s10s curve steeper and EFPs 1bp wider.

- The bills strip has bear-steepened, with pricing +1 to -10.

- RBA-dated OIS pricing is 1-6bps softer across meetings, with November leading.

- Tomorrow the local calendar sees Trade Balance data for August. Terminal rate expectations sit at 4.34% (+27bps).

AUSTRALIAN DATA: PMI Signalling Steady Growth

The Judo Bank composite PMI for September was revised up to 51.5, the highest since May, from the preliminary 50.2 and significantly higher than August’s 48. It implies that the economy grew in the final month of the quarter after contracting in July/August. This leaves the Q3 average at 49.2, in line with Q1 which still saw GDP growth of 0.4% q/q.

- If these levels are sustained, then the economy could be running at a steady rate and proving more resilient than expected.

- September services PMI was revised up to 51.8 from 50.5 and stronger than August’s 47.8. New business including from overseas grew at its fastest for 15 months in September, which resulted in increased employment. Judo Bank notes that respondents cited increased tourism and overseas students as boosting foreign new business. While input price inflation rose due to rising shipping, labour and fuel costs, this was passed on to customers at a slower pace due to less certainty re the future. This was reflected in business confidence falling again and it was already below the series average.

- See press release here.

Source: MNI - Market News/Refinitiv/Bloomberg

RBA: MNI RBA Review - October 2023: Pause, Forecasts Key To November Decision

- The RBA left rates unchanged at 4.1% for the fourth consecutive time. This was Michele Bullock’s first meeting as Governor and the little changed statement says something in itself - for now it is business as usual.

- Fuel prices were mentioned in the September minutes but this month they appeared in the statement too having “risen noticeably”. Another addition to the statement was the recognition that H1 growth had been stronger than projected but the RBA still expects it to be below trend.

- The Board retained its tightening bias and so has kept its options open for the November 7 decision given there will be updated forecasts and Q3 CPI due on October 25. Q2 2025 CPI is currently expected to be 3.1% but given that this is the boundary of the RBA’s “reasonable timeframe” an upward revision could be enough to drive another rate hike. So could a strong Q3 services CPI reading. A near-term upward revision to the CPI will be acceptable if 2025 is unchanged.

- Terminal rate expectations have only softened by 2bps to 4.34%. Accordingly, they remain approximately 20bps higher than early September and are at their highest level since late July.

- See full review here.

NZGBS: Twist-Steepens, Weighs A Less Hawkish RBNZ Vs. Higher Longer-Dated Global Yields

NZGBs closed with a twist-steepening of the curve, as the market weighed a slightly less hawkish RBNZ against higher longer-dated US tsy yields. Benchmark yields are 2bps lower to 11bps higher.

- The RBNZ left rates at 5.5%, which was widely expected, and it reiterated its higher-for-longer stance. The outlook “remained similar” to the last meeting implying that as of this month, the RBNZ’s forecasts are unchanged. There was a tweak to the end of the statement saying that policy needs to remain restrictive for “a more sustained period of time” rather than “the foreseeable future”. This may imply that rather than increase rates further, policy may stay tight longer than is currently expected.

- Meanwhile, US tsys have extended overnight weakness in the Asia-Pac session, with yields flat to 5bps higher across benchmarks, a steepening of the curve is evident.

- Swap rates are +/-3bps after the RBNZ decision to be flat to 10bps higher on the day. The 2s10s curve has bear-steepened.

- RBNZ dated OIS pricing is 4-8bps softer across meetings beyond October.

- Tomorrow the local calendar sees ANZ Commodity Prices and Government’s 12-month Financial Statements.

- Tomorrow the NZ Treasury plans to sell NZ$225mn of the 0.25% May-28 bond, NZ$225mn of the 3.50% Apr-33 bond and NZ$50mn of the 1.75% May-41 bond.

RBNZ: RBNZ On Hold, Rates May Be Higher Longer Than Thought

The RBNZ left rates at 5.5% at its October meeting which was widely expected and it reiterated its higher for longer stance. The outlook “remained similar” to the last meeting implying that as of this month the RBNZ’s forecasts are unchanged. There was a tweak to the end of the statement saying that policy needs to remain restrictive for “a more sustained period of time” rather than “the foreseeable future”. This may be implying that rather than increase rates further, policy may stay tight longer than is currently expected.

- While the risks to the RBNZ’s outlook are “similar” to August, there was mention of some upside risks to inflation. The stronger Q2 GDP outcome was acknowledged and the upside risk to demand from strong population growth noted. This “could slow the pace of expected disinflation”. Like with the RBA, the RBNZ also commented on higher oil prices and its risk to higher headline inflation. The November 29 meeting will include revised forecasts.

- The statement for August that the MPC is “confident” that current rates will return inflation to target was altered to rates need to “stay at a restrictive level”, thus making the central bank sound a little less sure of its policy stance.

- The few changes to the press release add a sense of less confidence in the on hold stance and add to the higher for longer view. But on the other hand the Committee observed that financial conditions tightened further as average mortgage rates and wholesale rates rose again despite an unchanged OCR. The lags involved in monetary policy were reiterated and “weak demand for credit” observed.

- The global economy, particularly China, remains a source of downside risks to NZ growth.

- See press release here.

FOREX: USD Uptrend Continues, NZD Underperforms Post RBNZ

USD indices have continued to track higher. The BBDXY getting close to 1280, fresh highs back to late November last year. Dollar sentiment has been aided by the continued rise in US yields, with the 10yr making fresh cyclical highs of 4.85%.

- NZD/USD has underperformed post the slightly less hawkish RBNZ (which left rates on hold as expected). The RBNZ language hinted potentially less need to tighten in November. The kiwi fell to 0.5871 but has since stabilized somewhat, last 0.5885/90, still 0.35% weaker for the session.

- AUD/USD was dragged lower by NZD but found support under 0.6290 (similar to lows from Tuesday). We now sit back near 0.6300, slightly outperforming broader USD trends. AUD/NZD has pushed back above 1.0700.

- USD/JPY has drifted a little higher. The pair was last near 149.25, after opening closer to 149.00. Highs for the session sit at 149.32. A raft of Japanese officials have refused to confirm if the authorities intervened in FX markets yesterday, while maintaining recent rhetoric around FX. Yen is outperforming the rise in US yields, but markets remain wary of intervention risks.

- Looking ahead, we have some ECB speak, headlined by Lagarde. Final September PMIs are due in the EU. Later the Fed’s Bowman and Goolsbee speak. There is also a swathe of US data including ADP September employment, September services PMI/ISM and final August durable goods orders.

EQUITIES: Broad Based Losses Amid Continued US Yield Surge

Regional Asia Pac equities are once again under pressure. Losses are evident across the board, as the relentless rise in US yields continues to unsettle broader risk appetite. Japan markets and returning South Korean markets are among the weakest performers.

- US equity futures have also exhibited further weaker (following losses in Tuesday cash trade). Eminis are off by 0.40%, last near 4248, and close to the simple 200-day MA (we are already sub the 200-day EMA). Nasdaq futures are down by a similar amount. Strong US yield gains have continued in Asia Pac in Wednesday trade to date The 10yr yield making a fresh high of 4.85% (+5bps for the session). The higher for longer theme continues to see US yields adjust.

- Japan yields have risen, the 10yr swap rate above 1.0%, although yen has lost a little ground. Japan benchmark indices are down close to 2% at this stage.

- South Korean markets have returned (shut since last Thursday) and played catch up to the downside. The Kospi is off over 2%, the Kosdaq -3.5%. Offshore investors have sold -$425.3mn of local stocks so far.

- Hong Kong stocks remain on the backfoot, the HSI down over 1%. The ASX 200 is down around 1%.

- In SEA, Indonesian and Singapore indices are the weakest, down over 1% at this stage.

OIL: Prices Steady, OPEC Meeting Later Unlikely To Change Stance

Oil prices are down slightly during the APAC session and are off the session’s highs. Tight supply fundamentals are holding crude up despite a stronger greenback, USD index +0.2%, and rising US yields. Brent fell from a high of $91.21/bbl earlier in the session to a low of $90.62 on dollar strength but has come back to around $90.84/bbl. WTI has traded below $90 finding a floor at $89 and is currently around $89.16.

- The WTI prompt spread is off its peak but still wider than the end of August and continues to signal market tightness, according to Bloomberg.

- Bloomberg reported that there was a 4.21mn barrels US crude stock drawdown in the latest week according to people familiar with the API data. Gasoline rose 3.9mn and distillate 0.3mn. Later the official EIA data are released and oil inventories are expected to be close to flat.

- Russia is considering a lift of its diesel export ban for producers with an announcement likely in the next few days. This would put downward pressure on prices.

- According to Bloomberg, OPEC will have an online meeting on Wednesday to discuss the current position of global markets. Output was constant in September and its current stance is unlikely to be altered.

- Later the Fed’s Bowman and Goolsbee speak. There is also a swathe of US data including ADP September employment, September services PMI/ISM and final August durable goods orders. Euro area services PMIs, August retail sales and PPI also print. The ECB’s Lagarde, de Guindos and Panetta appear.

GOLD: Slightly Weaker After Hitting Lowest Level In Seven Months

Gold is slightly weaker in the Asia-Pac session, after closing -0.3% at $1823.02 on Tuesday. Tuesday’s close was the lowest in almost seven months, as US tsy yields continued to push to multi-year highs.

- US tsys finished 5-14bps cheaper across major benchmarks, with a steepening of the curve. Higher-than-expected JOLTS data drove the move, with the 10-year yield reaching a fresh cycle high of 4.8081%.

- US job openings unexpectedly rose sharply by 690k in August to 9.6m, breaking a run of declines. However, the quits rate was unchanged at 2.3%, matching the lowest level since 2020, consistent with workers remaining less confident in their ability to find another job in the current market.

- Fed Mester did little to dissuade the tsy sell-off. In contrast, Fed Bostic struck a more cautionary view: “I am not in a hurry to raise, but I am not in a hurry to reduce either.”

- Focus now turns to the scheduled economic data later today, including ADP Private Employment and ISM Services. US Non-Farm Payrolls are due for release on Friday.

SOUTH KOREA DATA: IP Data Points To Further Recovery

South Korea industrial production surprised firmly on the upside in August, rising 5.5% m/m, versus 0.2% forecast and -2.0% expected. This saw the y/y print come in at -0.5%, also well above expectations of -5.8% (prior -8.1%). The average operating ratio rose to 73.4% from 70.0% in July.

- Semiconductor production rose over 13%, while the electronics operating ratio rose to 97.2, from 88.7 in July. This is back close to levels from mid 2022.

- Combined with the weekend's better export data suggests external headwinds and chip demand may be on the improve.

- Other data showed the cyclical leading index at flat for August, versus 0.4 in July. Still to come is the September manufacturing PMI.

ASIA FX: Dollar Gains Continue For The Most Part

Most USD/Asia pairs maintained a firmer tone in Wednesday dealings. USD/CNH was steady with China markets still closed, while PHP continues to buck the broader USD trend. Likely intervention curbed USD gains elsewhere. Tomorrow, we have CPI prints in South Korea, the Philippines and Thailand as the focus points.

- USD/CNH has remained on the sidelines. The pair last near 7.3240, tracking tight ranges today and largely ignoring the firmer USD trend.

- South Korean markets have returned, with onshore equities slumping more than 2%, as catch up to recent global equity market weakness. Local data was better in terms of IP growth, but this didn't boost sentiment in the FX space. 1 month USD/KRW hasn't been able to break above 1360 though. The authorities stating they are prepared to act to curb excessive volatility in asset markets.

- Spot USD/TWD has continued to push higher, last near 32.43. The CBC (Taiwan central bank) told local lawmakers that there is no set level of defense for FX levels, but intervention smooths out volatility.

- USD/THB has hit fresh highs today, last at 37.20. We closed yesterday at 37.04, but the bias remains in the pair to test the upside. Broader USD trends remain firm, while local equities continue to track lower. The main macro focus today has been comments from BoT Governor Sethaput Suthiwartnarueput . On FX, the governor noted baht volatility has risen, but the central bank stands ready to curb excessive moves.

- USD/PHP tracks near 56.73 in recent dealings, down slightly (-0.12%), versus yesterday's closing levels. The pair has largely ignored the recent push higher in USD indices, although the move away in oil prices from recent highs has helped the terms of trade backdrop, albeit marginally. Tomorrow the focus rests on the September CPI print. The consensus looks for a 5.3% y/y outcome, the same as August. The m/m is expected at 0.4% (prior 1.1%). The BSP stated last week that its forecast range was 5.3-6.1% y/y for the September CPI.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/10/2023 | 0715/0915 | ** |  | ES | S&P Global Services PMI (f) |

| 04/10/2023 | 0745/0945 | ** |  | IT | S&P Global Services PMI (f) |

| 04/10/2023 | 0750/0950 | ** |  | FR | IHS Markit Services PMI (f) |

| 04/10/2023 | 0755/0955 | ** |  | DE | IHS Markit Services PMI (f) |

| 04/10/2023 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (f) |

| 04/10/2023 | 0815/1015 | | EU | ECB's Lagarde speaks at ECB MP Conference | |

| 04/10/2023 | 0830/0930 | ** |  | UK | S&P Global Services PMI (Final) |

| 04/10/2023 | 0900/1100 | ** | | EU | PPI |

| 04/10/2023 | 0900/1100 | ** | | EU | Retail Sales |

| 04/10/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 04/10/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 04/10/2023 | 1140/1340 | | EU | ECB's de Guindos speaks at Cyprus CB Conference | |

| 04/10/2023 | - | | UK | BoE's Bailey Interview in Prospect Magazine | |

| 04/10/2023 | 1215/0815 | *** | | US | ADP Employment Report |

| 04/10/2023 | 1345/0945 | *** | | US | IHS Markit Services Index (final) |

| 04/10/2023 | 1400/1000 | *** | | US | ISM Non-Manufacturing Index |

| 04/10/2023 | 1400/1000 | ** | | US | Factory New Orders |

| 04/10/2023 | 1400/1600 | | EU | ECB's Panetta speaks at ECB MP Conference | |

| 04/10/2023 | 1425/1025 | | US | Fed Governor Michelle Bowman | |

| 04/10/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 04/10/2023 | 1600/1800 | | EU | ECB's Lagarde speaks at Columbia University |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.