Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

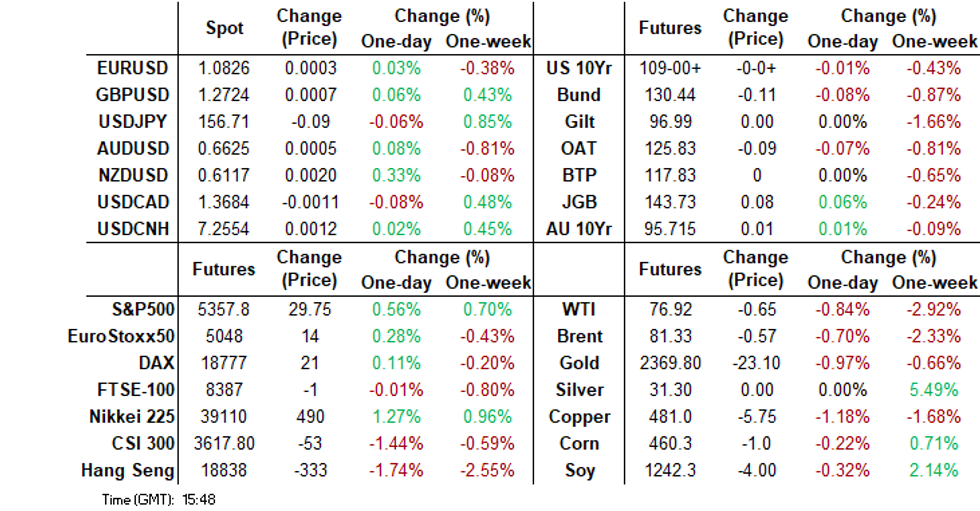

- The risk mood has been supported by a stronger US equity futures backdrop, which followed the better than expected Nvidia result from late Wednesday US time. This aided most regional equity markets, although HK/China markets lost ground.

- In the FX space, NZD was aided by broader equity gains and better data. It continues to outperform post yesterday's RBNZ.

- The BoJ left the bond buying amounts unchanged at today’s operations. This provided support for the market in the afternoon session.

- Looking ahead, the Fed’s Bostic and BoE’s Pill appear. US jobless claims, preliminary May PMIs and new home sales print. There’s also euro area May PMIs & consumer confidence, and Q1 negotiated wages. The G7 central bank governors and finance ministers meeting is taking place.

MARKETS

US TSYS: Treasury Futures Little Changed, Ranges Tight

- Treasury futures are little changed today, hold near overnight lows, the 10Y contract is unchanged at 109-01, while the 2Y contract is (- 00.125) at 101-19

- Volumes: TU 29k, FV 40k, TY 66k

- Tsys Flows: Block seller of 1.8k at 105-24.25

- Despite the latest pullback in Treasuries, the short-term trend condition remains bullish. Support now holds at 108-29 (20-day EMA), a break below here would see us look to test 108-15 (May 14 low), while to the upside initial resistance holds at 109-31+ (May 16 high/Bull trigger).

- The treasury curve bear-flattened on Wednesday, we have opened little changed with the 2Y yield +0.2bp at 4.871%, 10Y +0.2bp to 4.424%.

- Regionally: ACBG curve flatter, yields are +1.5bps to -4.1bps, NZGBs steeper, yields 4-8bps higher, while JGB curve steeper, yields are +2bps to -1bp.

- Rate cut projections are slightly lower vs. late Tuesday levels (*): June 2024 at -5% w/ cumulative rate cut 0bp at 5.323%, July'24 at -16.0% (-20%) w/ cumulative at -5.2 (-6.3bp) at 5.283%, Sep'24 cumulative -17.8bp (-19.9bp), Nov'24 cumulative -25.6bp (-27.6bp), Dec'24 -40bp (-43.7bp).

- Looking ahead: Chicago Fed Nat Activity Index, Jobless Claims & S&P Global US PMI

STIR: Varied Performances Across $-Bloc During May

STIR markets within the $-bloc have shown varied performances over the past three weeks. Australia and Canada have outperformed, softening by 11-12bps in year-end expectations, while the US remains unchanged.

- Yesterday, the FOMC Minutes for the May meeting delivered no major reaction from US STIR. “Participants noted disappointing readings on inflation over the first quarter and indicators pointing to strong economic momentum, and assessed that it would take longer than previously anticipated for them to gain greater confidence that inflation was moving sustainably toward 2%,” the minutes said. Some officials also appeared willing to contemplate interest rate increases if conditions appear to worsen.

- In contrast, New Zealand is approximately 20bps firmer, with most of the movement occurring after yesterday’s RBNZ policy decision. The central bank indicated that it expects to maintain tight monetary policy for an extended period due to domestic inflation pressures.

- December 2024 expectations and the cumulative easing across the $-bloc stand at: 4.95%, -39bps (FOMC); 4.36%, -64bps (BoC); 4.27%, -8bps from an expected terminal rate of 4.36% (RBA); and 5.27%, -23bps (RBNZ).

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

JGBS: Rinban Operations Support Market, National CPI Tomorrow

JGB futures are stronger, +6 compared to settlement levels, and near session bests.

- Outside of the previously outlined Weekly International Investment Flow and Jibun Bank PMIs, there hasn't been much in the way of domestic data drivers to flag. Machine Tool Orders data is due later.

- However, the market's focus today was on BoJ’s Rinban Operations covering 1-10-year JGBs after the 10-year yield reached a fresh cycle high above 1% yesterday.

- The BoJ left the bond buying amounts unchanged at today’s operations. Nevertheless, the operations went smoothly with negative spreads across the buckets and moderate to low offer cover ratios. This provided support for the market in the afternoon session.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s modest post-FOMC Minutes cheapening.

- The cash JGB curve has twist-steepened, pivoting at the 30s, with yields 1.2bp lower (7-year) to 1.5bp higher (40-year). The benchmark 10-year yield is 0.8bp lower at 1.001% after setting a fresh cycle high of 1.011% yesterday.

- Swap rates are 1bp lower to 1bp higher, with swap spreads mixed.

- Tomorrow, the local calendar will see National CPI and Department Sales data.

AUSSIE BONDS: Mixed, Relatively Narrow Ranges, Nov-28 Supply Tomorrow

ACGBs (YM -1.0 & XM +2.0) are slightly mixed after dealing in relatively narrow ranges in today’s Sydney session. There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Melbourne Institute Inflation Expectations and Judo Bank Preliminary PMIs.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s modest post-FOMC Minutes cheapening.

- Cash ACGBs are 1bp cheaper to 2bps richer, with the 3/10 curve flatter and the AU-US 10-year yield differential at -16bps.

- The swaps curve has bear-flattened, with rates flat to 2bps higher.

- The bills strip has slightly cheapened, with pricing flat to -1.

- RBA-dated OIS pricing is 1-4bps firmer for meetings beyond August. Only 7bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty apart from the AOFM’s planned sale of A$900mn of the 2.75% Nov-28 bond.

NZGBS: Post-RBNZ Sell-Off Continued

NZGBs closed 6-8bps cheaper, with the short-end underperforming. The stronger-than-expected Q1 Retail Sales excluding Inflation likely contributed but the primary driver was yesterday's announcement from the RBNZ that it expects to maintain tight monetary policy for longer due to domestic inflation pressures. (See MNI RBNZ Review here)

- Additionally, lacklustre demand at today's weekly supply, with cover ratios for the three lines at or below 2.00x, further impacted the market.

- Comments from Federal Reserve officials in the May FOMC minutes, indicating that US interest rates will need to stay higher for longer to combat persistent inflation, also weighed on NZGBs.

- 2-, 5- and 10-year yields are a cumulative 15bps, 11bps and 10bps higher respectively than pre-RBNZ levels.

- Swap rates closed 3-8bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS has continued to firm with pricing being 7-13bps firmer for meetings beyond October. Additionally, these meetings are now 18-23bps firmer than before the RBNZ Decision.

- The local calendar will see ANZ Consumer Confidence and Trade Balance data tomorrow.

- Later today, the US calendar will release the Chicago Fed Nat Activity Index, Jobless Claims and S&P Global US PMIs.

RBNZ: MNI RBNZ Review – May 2024: High For Even Longer

- The 0.2pp overshoot of the RBNZ’s Q1 CPI forecast seems to have driven a hawkish shift. Rates may now need to stay restrictive for “longer than anticipated” for the MPC to be confident that inflation will return sustainably to target. The RBNZ’s upward revision to its OCR path and the “real consideration” of another hike reflect this hawkish hold. It also said “rate cuts continue to be delayed”.

- The decision to leave rates at 5.5% was unanimous as the MPC decided that it could be patient as inflation is expected to return to the band by year end. It is likely to be on hold now for some time as it waits for further quarterly CPI releases.

- The end-2024 OCR and CPI forecasts were revised higher. Even though growth was revised down, lower assumed potential growth meant that the neutral interest rate and output gap were revised higher.

- The projected terminal OCR remains around 5.50%, but the cumulative easing expected by year-end has reduced to 23bps from 45bps before yesterday’s RBNZ decision.

- See full review here.

NZ STIR: RBNZ Dated OIS Has Shunted Firmer Since The RBNZ Decision

RBNZ dated OIS has continued to firm with pricing being 7-12bps firmer for meetings beyond October. This comes after the central bank said yesterday that it expected to keep monetary policy tight for longer due to domestic inflation pressures.

- Additionally, these meetings are now 18-23bps firmer compared to levels before the RBNZ Decision.

- The projected terminal OCR remains around 5.50%, but the cumulative easing expected by year-end has reduced to 23bps from 45bps before yesterday’s RBNZ Decision.

- For context, it's noteworthy that in late December, the market had anticipated over 100bps of easing by year-end, driven by expectations of a terminal OCR of 5.53%.

Figure 1: RBNZ Dated OIS Today Versus Pre-RBNZ Levels (%)

Source: MNI – Market News / Bloomberg

NEW ZEALAND DATA: Retail Spending Remains Weak

The rise in Q1 real retail sales is in contrast to recent weak activity indicators thus it may be pay back for Q4’s 1.8% q/q drop. This was the first quarterly increase since 2021. They rose 0.5% q/q with core sales up 0.4%. With consumer confidence declining sharply over 2024, household expenditure is likely to remain soft.

- The improvement was fairly broad based across regions and Stats NZ reported an increase in 9 of 15 retail sectors.

- The largest rises were recorded in food services +2.2% q/q, motor vehicles +1.1%, recreation goods +4.7% and accommodation +4.1%. Household durables remained weak.

- Retail sales volumes were still down 2.6% y/y while the population grew 2.5% y/y showing a significant drop in spending per person. Core sales fell 1.7% y/y.

Source: MNI - Market News/Refinitiv

FOREX: NZD Outperformance Continues On Data & Higher US Equity Futures

The BBDXY sits slightly lower for the first part of Thursday trade, the BBDXY index last under 1250. NZD has been the outperformer aided by better data and a firmer US equity futures backdrop.

- NZD/USD is back around 0.6120, up close to 0.40% for the session. This is still sub post RBNZ highs, but is maintaining the Kiwi outperformance theme.

- Retail sales for Q1 rose +0.5%, against a consensus expectation for a fall. The broader consumer spending backdrop remains soft though. RBNZ Governor Orr stated the central bank doesn’t want to risk a blowout in inflation expectations, although appeared to leave a high bar for a further hike.

- AUD/NZD is down 0.25% at 1.0830/35, close to the 200-day EMA support point. AUD/USD is higher, but trailing NZD, the pair last near 0.6630. Consumer inflation expectations eased to 4.1% in April from 4.6%.

- Risk sentiment has been aided by a positive US equity futures backdrop. Nasdaq futures are up nearly 1% (Eminis +0.60%), with Nvidia's strong earnings result from late Wednesday US time, a clear positive. This is helping to offset a more mixed regional equity tone, with China/HK markets tracking lower. US yields sit a touch higher.

- USD/JPY got to fresh highs of 156.90, but now sits back in the 156.70/75, little changed for the session. BoJ bond buying ops were unchanged, while the preliminary manufacturing PMI for May moved back into expansion territory.

- Looking ahead, preliminary PMIs in the UK and EU are out, as well as the US. The Fed's Bostic also speaks.

ASIA EQUITY FLOWS: Asian Equity Flows Positive, As Investors Buy Tech Names

- South Korean equity markets were little changed on Wednesday after initially opening lower and testing the 20-day EMA. We ended a three day steak of foreign investors selling local stock, with the majority of flows heading into transport equipment names, the past 5 sessions have seen a total inflow of $145m. Nvidia's positive earnings should help with flows today, although we also have BOK rate decision later today. The 5-day average is now just $29m, below the 20-day average of $77m, and well down on the longer term 100-day average at $170m.

- Taiwan equities surged higher on Wednesday, as investors bought up Nvidia related stocks in particular supplier TSMC. Foreign investors bought $1.10b of equities, with the past 5 session seeing a total inflow of $2.58b. This week the focus will be on the unemployment rate and Industrial Production. The 5-day average now sits at $516m, well above the 20-day average at $364m and the 100-day average at $87m.

- Indian equities were higher again on Wednesday, although foreign investors continue selling stocks, we have had just one of the past 13 session of inflows. This week, we have HSBC India PMI data due out. The 5-day average is now -$123m, below both the 20-day average at -$192m and the 100-day average at $21.02m.

- Indonesian equities were higher on Wednesday, and bounced right off the 20 & 100-day EMA's, the selling from foreign investors is back with another $34m outflow, taking the past 5 session to just $0.5m, Indonesia is out for the remainder of the week. The 5-day average now $5m and now above the 20-day average at -$42m while the 100-day average is still positive at $5.35m.

- Philippines equities were lower on Tuesday, equity flow momentum has been mixed recently we have seen a net outflow of $9.85m over the past 5-days. This week the calendar is light with just the Budget Balance on Thursday. The 5-day average is $0.1m, above the 20-day average at -$42m, while slightly below the 100-day average of $5m

- Malaysian equities were lower on Wednesday, although just off all-time-highs. Flows over the past week have been positive, although there was a small outflows on Tuesday for a total inflow of $176m. This week we have Foreign Reserves and CPI. The 5-day average now $35m, now above the 20-day average at $33m and well above the longer term 100-day average at $0.65m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | 206 | 146 | 15301 |

| Taiwan (USDmn) | 1102 | 2585 | 5222 |

| India (USDmn)* | -225 | -619 | -3307 |

| Indonesia (USDmn) | -35 | 1 | -37 |

| Thailand (USDmn)** | 0 | 38 | -1910 |

| Malaysia (USDmn) * | -6 | 177 | 19 |

| Philippines (USDmn) | -11 | -19.5 | -293 |

| Total | 1031 | 2307 | 14995 |

| * Data Up To Apr 20th | |||

| ** Public Holiday |

JAPAN DATA: Japan Investors Step Up Offshore Bond Purchases

Offshore investors maintained net purchases of local stocks and bonds last week. However, the pace of inflows slowed. We had ¥248.1bn coming into local stocks, the fourth straight week of inflows, while purchases of local bonds was ¥427.4bn. This was the first back to back inflows into local bonds since the mid March period.

- In terms of outbound flows from local investors, we had a surge in purchases of offshore bonds (¥2192.2bn). This was the largest weekly purchase since late Dec last year. A softer core yield backdrop through the middle part of last week may have contributed to these domestic outflows.

- Offshore purchases of foreign stocks rebounded, but the trend has been indifferent in recent weeks for this segment.

Table 1: Japan Weekly Foreign Investment Flows

| Billion Yen | Week ending May 17 | Prior Week |

| Foreign Buying Japan Stocks | 248.1 | 664.8 |

| Foreign Buying Japan Bonds | 427.4 | 1698.4 |

| Japan Buying Foreign Bonds | 2192.2 | -390.6 |

| Japan Buying Foreign Stocks | 528.6 | -390.9 |

Source: MNI - Market News/Bloomberg

ASIA STOCKS: HK & China Equities Lower, HSI Breaks Below 19,000

Hong Kong & Chinese equities have lower today after FOMC minutes suggested they would keep interest rates elevated for some time due to sticky inflation, while corporate earnings in the region have also weighed on sentiment, the HSI also breached the 19,000 and now trades at the lowest level in two weeks. China set its daily reference rate for the yuan at its weakest level since January, allowing for more currency depreciation alongside regional peers due to the dollar's rebound. Today, we have CPI composite with consensus at 2%, in line with May.

- Hong Kong equities are lower today, with property the worst performing sector. The Mainland Property Index is down 1.27%, while the HS Property Index is down 1.86%, HStech Index is down 1.68% while the wider HSI is down 1.38%. In China, the CSI300 is down 0.90% performing better than the small-cap CSI1000 and CSI2000 Indices which are trading down 1.70%, while the growth focus ChiNext Index is down about 1%.

- In the property space today, China Vanke has pledged about 27b yuan worth of shares in the Vanke logistics Development unit, to China Merchants Bank, which is typically used to obtain a loan.

- MNI China Press Digest May 23: Exports, Sino-EU, Electricity - (See link)

- Chinese automaker BYD plans to launch its low-cost Seagull hatchback in Europe next year, increasing competitive pressure on local carmakers like Stellantis and Renault. With premium features and a price under €20,000, the Seagull's arrival is part of a broader push by Chinese EV manufacturers into the European market, challenging incumbents and prompting discussions on tariffs and new industry alliances, as per BBG.

- Hong Kong’s retail investors are increasingly betting on a decline in local equities, pouring around $400 million into inverse exchange-traded funds (ETFs) this quarter, the highest since late 2022. These investments, largely driven by retail traders, suggest expectations of a market reversal following a 30% rebound in key equity gauges since January. Despite institutional interest, the trend is typical of retail behavior during market upswings. Concurrently, ETFs tracking Hong Kong stocks have seen significant outflows of $1.2 billion this quarter, primarily from those linked to the Hang Seng Tech Index.

- Today, we have HK CPI Composite at 1830 AEST/ 1630HKT

ASIA PAC STOCKS: Equities Edge Higher As Chip & AI Names Rally On Nvidia's Update

Asia markets opened lower this morning, but have largely erased those loses. A hawkish fed minutes initially weighed on sentiment, however as the day progressed chip and AI-related stocks pushed higher. Miners are underperforming today, although well off earlier lows after copper and oil prices fell on Wednesday. There hasn't been too much in the way of market moving economic data releases with NZ Retail Sales best estimates, AU Judo Bank PMI and Consumer Inflation Expectations both fell in May, JP Jibun Bank May PMI was mixed. Looking ahead to tomorrow, NZ Trade Balance data and JP National CPI will be the focus.

- Japanese equities are higher today, after initially opening lower, hawkish fed minutes have weighed on market sentiment initially, while lower commodity prices have dragged mining names lower, as the day progressed Technology stocks pulled the market higher. Earlier, Jiban Bank PMI Mfg was 50.5 vs 49.6, Services were 53.6 vs 54.3 while the Composite came in at 52.4 vs 52.3 prior. The Topix is up 0.54%, the Topix Oil & coal index is down about 1.90% while the Nikkei 225 is up 1.15%.

- Taiwan equities are higher today, the BBG Asia-Pacific Semiconductor Index has been grinding higher all throughout the day and now trade up 1.72%. Later today, April Industrial Production data is expected to show an increase from 3.99% to 11.25%. The Taiex is currently up 0.32%.

- South Korean equities are higher today, similar to other markets we opened lower but have been griding higher throughout the day. The BOK left rates unchanged at 3.5% as expected with a restrictive stance expected for a sufficient period of time. The large-cap Kospi is up 0.20%, while the small-cap Kosdaq is up 0.30%

- Australian equities are lower today are the FOMC minutes signaling they are in no rush to cuts rates, which pushed commodity prices lower, unlike other markets the ASX200 has a much smaller exposure to tech and chip names and has lagged the move higher by other regional markets. Judo Bank PMI composite fell in May to 52.6 from 53.0. The ASX200 is down 0.50%

- Elsewhere in SEA, New Zealand equities are up 0.50%, earlier retail sales ex inflation beat estimates coming in at 0.5% vs -0.3%, Singapore returned from a break on Wednesday with equities trading up about 0.26%, Malaysian equities continue to march higher as foreign investors continuing their buying streak, the KLCI is up 0.38%, the Philippines PSEi is up 0.33%, Indian equities are up 0.33%.

OIL: Crude Continues Falling On US Rate Fears

Oil prices continued falling during APAC trading on the back of hawkish FOMC minutes. If it continues, it will make four straight daily declines. WTI is down 0.7% to $77.04/bbl but off the intraday low of $76.83, to be down 3.2% this week. Brent is 0.6% lower at $81.45/bbl after a low of $81.21. Both have remained above initial support levels. The USD index is down 0.1%.

- EIA reported US crude inventories rose 1.83mn barrels last week but they were boosted by the largest adjustment factor since November. Gasoline demand rose 0.44mbd to 9.315mbd and inventories fell 945k barrels but the market looked through this positive information once it became concerned that Fed easing would be delayed further.

- While prices are lower this week, they are within recent ranges as the market waits for the June 1 OPEC meeting where it is widely expected to extend output cuts into H2. Russia has said it will present a plan to deal with its overproduction.

- The Fed’s Bostic and BoE’s Pill appear. US jobless claims, preliminary May PMIs and new home sales print. There’s also euro area May PMIs & consumer confidence, and Q1 negotiated wages. The G7 central bank governors and finance ministers meeting is taking place.

GOLD: Extends Post-Minutes Dump

Gold is 0.3% lower in the Asia-Pac session, after closing 1.7% lower at $2378.85 on Wednesday following the release of the FOMC Minutes for the May meeting. The yellow metal is now around $80 below the record high reached on Monday.

- Comments from Federal Reserve officials that US interest rates will need to stay higher for longer to combat stubborn inflation weighed on bullion.

- “Participants noted disappointing readings on inflation over the first quarter and indicators pointing to strong economic momentum, and assessed that it would take longer than previously anticipated for them to gain greater confidence that inflation was moving sustainably toward 2%,” the minutes said. Some officials also appeared willing to contemplate interest rate increases if conditions worsen.

- According to MNI’s technicals team, the medium-term outlook for gold remains bullish, with attention on 2452.5 next, a Fibonacci projection. On the downside, the 50-day EMA, at $2293.9, represents a key support.

BOK: To Remain Restrictive Until Confidence In Attaining Inflation Target Is Established

The BoK kept rates unchanged as widely expected, leaving the policy rate at 3.50%. The accompanying BoK statement lent slightly hawkishly, although it is likely within broad market expectations.

- Not surprisingly, 2024 growth forecasts were revised higher to 2.5% from 2.1% made in February. This followed the strong Q1 growth beat. Consumption growth is expected to pull back in Q2 before following a steady recovery path in H2. Exports are expected to remain a key driver of growth. 2025 growth was revised down to 2.1% from the 2.3% projection made in February.

- There were no changes to the headline inflation forecasts (at 2.6% this year, 2.1% next year), while core inflation for 2024 was also left unchanged at 2.2%.

- Upside risks to inflation prevail from the stronger growth backdrop but they are not expected to be strong given the modest consumption recovery. High uncertainty remains around the inflation outlook, with oil prices, FX trends, food price shifts and underlying growth all highlighted as risk factors.

- This backdrop leaves the central bank still lacking confidence that inflation will return to the 2% target level. In turn the central bank stated policy will be held restrictive for a sufficient period of time until such confidence is established.

- This should push back against any near term easing expectations. Coming up shortly we have BoK Governor Rhee's press conference.

ASIA FX: Tech Related FX Outperforms, SEA Currencies Mostly Weaker

USD/Asia pairs are mixed in the first part of Thursday. We have seen some modest KRW and TWD outperformance, aided by tech equity gains. SEA FX is weaker albeit away from session lows. USD/CNH has been relatively steady around 7.2550, even as the USD/CNY fixing printed fresh highs back to January. We still wait for Thailand April customs trade figures, while Taiwan IP prints later. Coming up tomorrow we have Malaysian CPI.

- The USD/CNY fixing rose close to 7.1100, fresh highs going back to January. Spot CNY and CNH markets have been well behaved though. USD/CNH hasn't drifted too far away from the 7.2550 level. Local equities and Hong Kong bourses continue to retreat from recent highs.

- 1 month USD/KRW sits away from session highs, the pair last near 1360, up around 0.35% in won terms versus end NY levels from Wednesday. Earlier we got to 1365.30. The Kospi has ticked up from earlier weakness to be marginally higher for the session. This is outperformer weaker trends seen in HK/China markets so far today. A chip support package announced by the government worth $19bn (per BBG) has likely aided the local equity recovery and seen some modest positive spillover to the won. The BoK outcome lent hawkishly but is unlikely to surprised the market. BoK Governor Rhee stated it was unclear when the central bank would start discussing rate cuts.

- 1 month USD/TWD is back to the 32.20 region, aided by broader tech gains, with US futures up strongly post the Nvidia result. We are still comfortably above recent lows sub 32.00.

- USD/THB has continued to recover in the first part of Thursday trade. We were last around 36.50, just off session highs, but still 0.50% weaker in baht terms. We are around +2% higher from lows earlier in the week, with baht gains, aided by a stronger than expected Q1 GDP print, proving to be fleeting. A stronger USD backdrop, particularly in terms of USD/JPY levels, won't be helping, likewise gold prices moving off recent highs. Headlines have also cross this afternoon that a Thailand court has accepted a petition from a group senators seeking to dismiss Premier Srettha for an ethics breach. This follows Srettha appointing a cabinet minister last month. The PM has 15 days to respond and can continue duties until the court makes a ruling (see this BBG link).

- USD/PHP is around 58.15/20, just off session highs, and 0.20% weaker for the session. This is fresh highs back to 2022. The pair continues to consolidate post the recent break above the 58.00 figure level. Comments from BSP Governor Remolona crossed the wires late yesterday. He stated the central bank intervened modestly on Tuesday in FX markets. This followed the break above 58.00 in the pair during that session. The Governor stated they are looking to curb speculative activity on such moves. Still, it was reiterated that the authorities are not intervening every day and when they do, it is only in modest amounts. Such commentary doesn't suggest any great alarm around current FX trends, nor a firm line in the sand around a particular level.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/05/2024 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 23/05/2024 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 23/05/2024 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 23/05/2024 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 23/05/2024 | 0800/1000 | ** |  | EU | S&P Global Services PMI (p) |

| 23/05/2024 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 23/05/2024 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 23/05/2024 | 0830/0930 | *** |  | UK | S&P Global Manufacturing PMI flash |

| 23/05/2024 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 23/05/2024 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 23/05/2024 | 1000/0600 | *** |  | TR | Turkey Benchmark Rate |

| 23/05/2024 | - | | EU | G7 Finance/CB Meet | |

| 23/05/2024 | 1230/0830 | *** |  | US | Jobless Claims |

| 23/05/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 23/05/2024 | 1345/0945 | *** | | US | S&P Global Manufacturing Index (Flash) |

| 23/05/2024 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 23/05/2024 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 23/05/2024 | 1400/1000 | *** | | US | New Home Sales |

| 23/05/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 23/05/2024 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 23/05/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 23/05/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 23/05/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 23/05/2024 | 1900/1500 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.