Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Brexit talks see final roll of the dice, headline flow mixed on fishing matters and familiar sources of discontent.

- Asia appears to be marginal buyer of U.S. Tsys on latest sell off (again).

- E-minis fade after the S&P 500 contract briefly showed above 3,700.

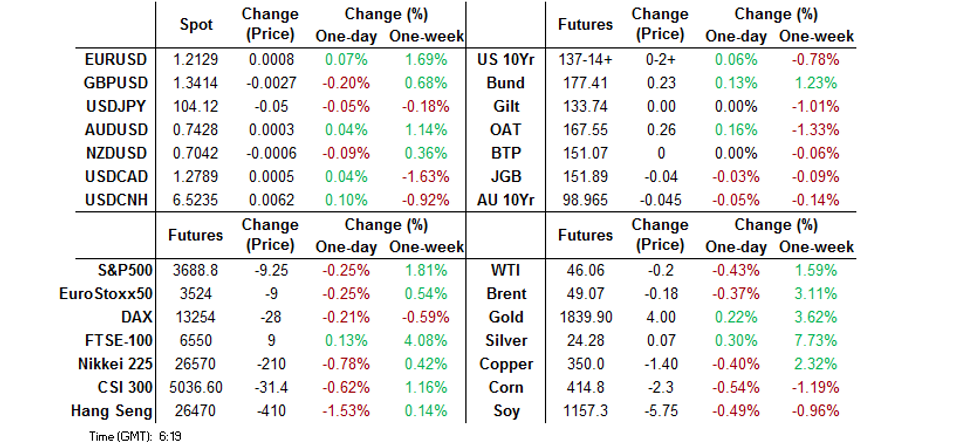

BOND SUMMARY: Tsys Edge Away From Friday's Lows

T-Notes have consolidated above unchanged levels after S&P 500 e-minis failed to hold onto early gains above 3,700. The contract last deals +0-02+ at 137-14+, a touch shy of best levels after the space looked through the latest round of Chinese trade data. Volume on the day is nearing ~115K as we move towards London hours. Cash Tsys run 0.2-1.9bp richer across the curve, with some light bull flattening at the fore. Some have pointed to the seemingly traditional Asia-Pac regional demand for cash Tsys as a source of the bid after Friday's sell off. Flow has dominated in what has been a quiet session for broader macro headlines, with what seemed to be profit taking of a 5.0K delta hedged USF1 172.00/170.00 put spread position via block sale. Elsewhere, there was 10.0K block sale of the TYF1 137.50/137.00 put spread on block, which was touted as further profit taking and was coupled with a 10.0K block trade in the TYG1 136.50/138.50 risk reversal (buying puts to sell the calls).

- JGB futures finished 3 ticks lower on the day. Cash trade seemingly lacked a cohesive sense of direction across the broader JGB curve, with yields sitting either side of unchanged at the bell. The latest round of BoJ Rinban operations saw the Bank leave the purchase sizes of the respective buckets unchanged, with the following cover ratios: 1-3 Year: 2.77x (prev. 2.55x), 25+ Year: 4.20x (prev. 7.46x). Elsewhere, Japanese PM Suga laid the way for comments re: fiscal matters in the coming days, as had been outlined by the local press in recent weeks, with the focus of any such measures seemingly set to fall on corporate liquidity provisions (which also provided no surprise). There was little else to digest domestically, outside of opinion polls pointing to support for PM Suga's government taking a further hit on the back of the COVID-19 dynamic.

- The move away from lows in U.S. Tsys allowed the Aussie bond space to recover from worst levels, with the RBA's A$1.0bn purchase of ACGB Apr '24 (to enforce its 3-Year yield target) providing a source of local incremental support. YM finished unchanged, with XM -4.5. The ACGB space shrugged off semi-government credit rating downgrades for both Victoria & NSW, courtesy of S&P and a less than inspiring cover ratio in the final round of conventional ACGB supply from the AOFM for calendar '20, although semi trade saw TCV and NSW underperform on the former.

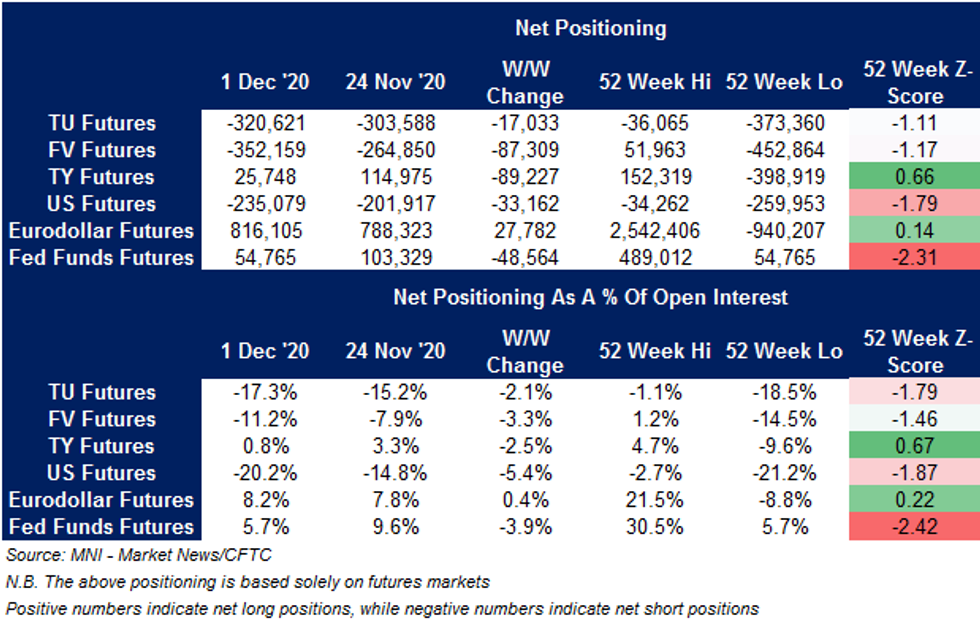

US TSYS: CFTC COT: TU, FV & US Net Shorts Build, TY Longs Trimmed

The latest CFTC COT report, covering the week through December 1, showed a widening of net short positions in the TU, FV and US futures contracts, while net length in the TY contract was cut, making for a cohesive picture in terms of the W/W moves for the major Tsy futures contracts.

- STIR net positioning changes were mixed.

FOREX: Sino-U.S. Tensions Weigh On Risk

Fresh signs of further Sino-U.S. frictions bolstered safe haven currencies, allowing JPY & CHF to top the G10 pile at the start to the week. RTRS reported that the Trump administration is planning to impose sanctions on at least a dozen of Chinese officials over the removal of Hong Kong opposition lawmakers. USD/JPY sank through the Y104.00 mark before establishing itself within a tight range around that figure.

- GBP went offered in early trade as duelling Brexit headlines from over the weekend stoked uncertainty. Several pieces suggested that the two sides made progress on fishing rights, but remain far apart on level playing field. Sterling trimmed losses as the Times reported that German Cll'r Merkel & French Pres Macron are willing to soften EU level playing field demands.

- MYR was the worst performer in Asia after Fitch downgraded Malaysia's sovereign credit rating to BBB+ from A- on Friday. TWD and KRW continue to hold around key levels in the absence of any catalysts.

- AUD was fairly quiet, AUD/USD moved in an approximately 15 pip range after coming off highs to end the US session on Friday. AUD shrugged off the news that S&P had lowered the rating of 2 Australian states, the move came as no surprise given the impact of the pandemic.

- The yuan initially continued to strengthen, before giving up the gains on the back of the US sanction headlines, but regained its poise after strong trade balance data. Exports soared above expectations, though imports were weaker than expected which could have negative implications for the domestic economy and capped gains.

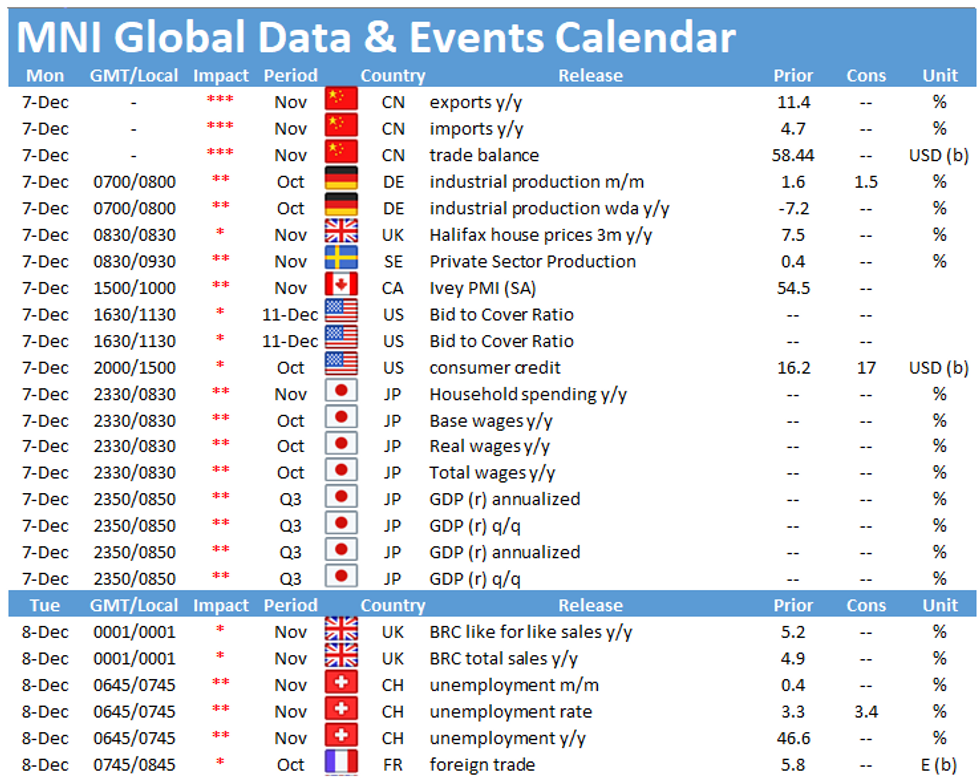

- There is little in the way of scheduled events today, with German industrial output & Riksbank Nov MonPol meeting minutes due. Brexit developments will remain under scrutiny, with EU Chief Negotiator Barnier expected to brief EU ambassadors on the state of negotiations before EU Commission Pres von der Leyen phones UK PM Johnson.

FOREX OPTIONS: Expiries for Dec7 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E655mln), $1.1840-50(E676mln), $1.2000(E583mln), $1.2045-55(E794mln), $1.2100-15(E621mln)

- USD/JPY: Y103.45-50($550mln), Y104.00-05($515mln),

Y104.25-30(E517mln), Y104.50($700mln), Y105.00($605mln) - EUR/GBP: Gbp0.8970-90(E527mln)

- AUD/USD: $0.7170-75(A$625mln), $0.7350(A$606mln)

- AUD/NZD: N$1.0487(A$680mln-AUD puts)

- USD/CAD: C$1.2800($410mln-USD puts), C$1.2900($670mln), C$1.3000($540mln-USD puts)

EQUITIES: Generally Lower To Start The Week

E-minis ran out of steam after an early show higher, as the S&P 500 futures contract failed to consolidate its brief showing above the 3,700 level (during which the contract lodged another fresh, all-time high).

- There is some expectation that lawmakers in DC will sign off on a stopgap funding package to prevent a government shutdown on Friday, with broader focus looking to ever-more positive rhetoric re: the prospects of a streamlined fiscal pact on the Hill.

- Further afield, vaccine deployment matters continue to attract attention, as do Sino-U.S. tensions, with reports pointing to DC readying itself to levy a fresh round of Hong Kong related sanctions on Chinese officials providing the latest potential point of stress.

- A wider than expected Chinese trade surplus was a by-product of better than expected exports and softer than expected imports, which didn't paint a particularly firm picture re: internal demand in China, meaning that the reading failed to provide any real support for local equities. Elsewhere, A-Shares may have been pressured after FTSE Russell noted that it will delete Hikvision equities, in addition to 7 other Chinese co.'s covered by U.S. restrictions surrounding military ties, from the relevant metrics.

- Nikkei 225 -0.8%, Hang Seng -1.3%, CSI 300 -0.6%, ASX 200 +0.6%.

- S&P 500 futures -11, DJIA futures -94, NASDAQ 100 futures -11.

GOLD: Still Not Through Resistance

Spot bullion last deals little changed around the $1,840/oz mark, with U.S. real yields sitting unchanged to a touch lower, while the USD, as measured by the broad DXY index, is little changed on the day. Bulls still haven't managed to force a break of former key support in the shape of the September 28 low, located at $1,848.8/oz.

- Elsewhere, known ETF holdings of gold continue to slide, but remain at elevated levels in historical terms.

OIL: Crude Edges Lower

WTI & Brent sit ~$0.15 below their respective settlement levels, with the downtick coming alongside some light pressure for e-minis during Asia-Pac hours. It should be noted that the modest downtick comes after 5 consecutive weekly gains for the major crude benchmarks.

- Weekend developments saw Saudi Aramco raise all pricing of crude exports to Asia for the month of January. Pricing was more mixed in other regions, although Aramco lowered all of its shipping differentials for the U.S.

- Elsewhere, Iranian state media noted that the country has instructed its oil ministry to prepare facilities for production & sale of crude at full capacity within a 3-month horizon, which will no doubt draw some focus from OPEC+.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.