Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- ACGBs are sharply cheaper (YM -9.0 & XM -4.0) after the RBA surprise the market again with a 25bp rate hike to 4.10%. The market had priced a 30% chance of a hike going into the meeting. There were few changes to the statement and the final guidance paragraph was the same as May’s. This indicates that the central bank has not finished and further moves in the months ahead are highly likely. AUD/USD surged to 0.6660/70, the top G10 FX performer.

- Elsewhere, Hong Kong and China stocks were in focus today. Hong Kong stocks have seen the greatest degree of volatility, starting weaker, before rebounding strongly on fresh stimulus hopes. There hasn't been great follow through, particularly for mainland stocks. Commodities like iron ore continue to push higher though. A meeting between US and China foreign ministry/state department officials also suggests some thawing in US-China tensions but there wasn't much market impact.

- In Europe today the data calendar is thin, German Factory Orders and Eurozone Retail Sales provide the highlights.

MARKETS

US TSYS: Marginally Cheaper In Asia

TYU3 deals at 113-26, -0-02+, a touch off the base of the 0-06 range on volume of ~52k.

- Cash tsys sit 1-3bps cheaper across the major benchmarks, the curve has bear flattened.

- Spillover pressure from ACGBs as the RBA lifted the cash rate 25bps to 4.15%, the market had been split between a hold at 3.85% or a 25bp hike, saw tsys marginally extend losses.

- Earlier in the session, tsys had ticked lower as better risk sentiment as Hong Kong equities advanced on speculation regarding fresh stimulus measures and the USD was marginally pressured.

- FOMC dated OIS price ~7bps hike into next week's meeting, the terminal rate is seen at ~5.3% in June. There are ~30bps of cuts priced for 2023.

- There is a thin data calendar in Europe today, further out Fedspeak from Cleveland Fed President Mester will cross.

GLOBAL DATA: PMIs Point To Pick Up In Growth, Trade Should Have Troughed

The global PMIs in May were steady and indicated that the global economy continues to grow. The composite PMI rose to 54.4 from 54.2, its highest since November 2021. It is well off the November 2022 low of 48. Growth is being driven by the services sector (May PMI 55.5), whereas manufacturing continues to see activity contract slightly. The manufacturing PMI was 49.6 for the third consecutive month. It is pointing to lacklustre global IP and merchandise trade over the months ahead but on the Brightside, the slowdown has probably reached a trough. April CPB global trade data is released on June 23.

Global composite PMI

Source: MNI - Market News/Bloomberg

Global growth

Source: MNI - Market News/Refinitiv/Bloomberg

JGBS: Futures At Session Highs, Smooth Absorption Of 30-Year Supply

JGB futures are sitting at session highs in afternoon Tokyo trade at 148.76, +18 versus settlement levels, after 30-year supply is smoothly absorbed but with less demand evident than in the May auction.

- JGB futures continue to operate close to recent lows, with 148.48 marking the near-term support. According to MNI's technicals team, the recent bounce off the lows helped stall a more protracted pullback, although the gap with key resistance at 149.17 remains.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined April labour cash earnings and household spending data, which surprised on the downside.

- Cash US tsys are trading above Asia-Pac cheaps but yields remain 1.2bp to 2.7bp higher.

- Cash JGBs are flat to slightly richer across the curve beyond the 1-year zone. The benchmark 10-year yield is 0.6bp lower at 0.428%.

- The 30-year zone is outperforming on the curve with its yield 1.8bp lower at 1.262% after today’s auction showed smooth digestion, albeit with slightly less demand exhibited than at the previous auction. While the low price met dealer expectations the cover ratio ticked down and the tail widened.

- Swap rates are 0.3-2.2bp lower across the curve with swap spreads tighter.

AUSSIE BONDS: Sharply Cheaper As The RBA Surprises With A 25bp Hike

ACGBs are sharply cheaper (YM -9.0 & XM -4.0) after the RBA surprise the market again with a 25bp rate hike to 4.10%. The market had priced a 30% chance of a hike going into the meeting.

- According to the statement, the decision was made to address high inflation, which, although it has peaked, remains at 7%, necessitating further measures to ensure its return to the target range. Recent data indicates increased upside risks to the inflation outlook, leading to the Board's response. Services price inflation remains high, while unit labour costs are rising, and productivity growth remains subdued.

- The Board stated that Australian economic growth has slowed, and while labour market conditions have eased slightly, they remain tight. The unemployment rate rose to 3.7% in April, and employment growth has moderated.

- The board added that further tightening of monetary policy may be necessary to achieve inflation target returns, contingent upon economic and inflation developments.

- Cash ACGBs are 6-9bp cheaper after the RBA decision to be 4-7bp cheaper on the day. The AU-US 10-year yield differential +7bp at +12bp.

- RBA-dated OIS pricing is 1214bp firmer for meetings beyond June with terminal rate expectations at 4.30%.

- Swap rates are 1-6bp higher on the day with EFPs 2bp lower and the curve 5bp flatter.

- The bills strip bear flattens with pricing -10 to -3.

RBA: 25bp Hike, Unchanged Guidance Points To More Tightening Ahead

The RBA surprised markets and most analysts again with a 25bp hike bringing rates to 4.1%, a cumulative 400bp of tightening this cycle. There were few changes to the statement and the final guidance paragraph was the same as May’s. This indicates that the central bank has not finished and further moves in the months ahead are highly likely. The details of Q1 GDP and no major change in the monthly data could mean another move on July 4. Sticky services prices may drive an extra hike at the August 1 meeting.

- RBA Governor Lowe speaks on Wednesday June 7 at 0920 AEST and Deputy Governor Bullock at 0950 AEST. This should provide more clarity around the decision.

- Increased upside inflation risks and growing concerns regarding meeting the inflation target by mid-2025 drove today’s tightening. The Board noted that “this further increase in interest rates is to provide greater confidence that inflation will return to target within a reasonable timeframe.” – implying that before the move they weren’t confident that this would happen. It probably also means that more is needed to make them “confident”.

- While wages growth is still consistent with the inflation target, higher public sector wage growth and the higher than last year’s award wage increase were noted. The risks from low productivity growth and strong unit labour costs were reiterated.

- The RBA no longer feels that inflation expectations are “well anchored”, as this was removed from the statement, and it will continue to monitor wage and price setting behaviour closely.

- The account provided more details as to why high inflation is so damaging and it seemed to speak to criticism regarding the impact on low-income households by saying that it “worsens income inequality”.

- Uncertainties around the consumer remain and most of the observations re this sector were unchanged. But instead of falling house prices weighing on consumption, the RBA observed that that they are rising again.

- See statement here.

AUSTRALIAN DATA: Q1 Net Exports Less Negative, Upside Risk To GDP

The current account surplus widened to $12.3bn in Q1 from the downwardly-revised $11.7bn in Q4 driven by a $2bn increase in the trade surplus to $41.05bn. Exports of goods & services rose 0.4% q/q while imports fell 0.9%. Net exports detracted 0.2pp from Q1 GDP (consensus -0.5pp), which was less than expected and thus there’s an upside risk to Wednesday’s GDP growth which consensus is currently forecasting to rise 0.3% q/q.

- The net primary income deficit widened $1.6bn to $28.5bn, the second highest on record.

- The ABS notes that the trade surplus was also the second highest, which was supported by a 2.8% q/q increase in the terms of trade as export prices (-1.3% q/q) fell less than import prices (-4% q/q – the largest decline since Q4 2010). The decline in imported inflation was driven by fuel & lubricants as global prices fell and helped by the stronger AUD.

- The rise in exports was driven by travel services, especially arrival of overseas students, and strong iron ore and lithium shipments. Overseas students are now at 94% of pre-pandemic levels, so most of the recovery has taken place. The tourism recovery also boosted exports.

- Chain volume exports rose 1.8% q/q in Q1 after 1.4% in Q4 while imports rose 3.2% q/q after falling 4%. This resulted in the real trade surplus narrowing $1.2bn after widening $6.2bn in Q4 and so a net export detraction of 0.2pp is estimated by the ABS.

Source: MNI - Market News/ABS

Australia terms of trade

Source: MNI - Market News/ABS

NZGBS: Yields Higher, Played Catch-Up To Global Bond Cheapening

NZGBs closed 6-11bp cheaper with the 2/10 curve 5bp steeper after it resumed trading after a long weekend.

- Swap rates are 4-6bp higher with implied swap spreads significantly tighter.

- RBNZ dated OIS opened 1-3bp firmer across meetings with May’24 leading.

- On the data front, NZ's commodity export prices rose 0.3% m/m in May versus -1.7% in April, according to ANZ Bank. The index falls 13.3% y/y and 9.9% y/y in NZD terms.

- Bloomberg reports that ASB Bank now expects the NZ economy will avoid a recession this year amid a surge in immigration. ASB expects Q1 economic growth to be flat subject to final partial indicators this week, whereas it previously projected a 0.6% contraction. (link)

- The local calendar tomorrow delivers Mfg Activity (Q1) along with the NZ Government’s 10-month Financial Statement.

- The global calendar is light today with Euro Area Retail Sales (Apr) as the highlight.

- Given that the local market has closed ahead of the RBA policy decision, tomorrow's opening is expected to reflect not only the Australian market's response to the announcement but also any fluctuations in the US tsys overnight.

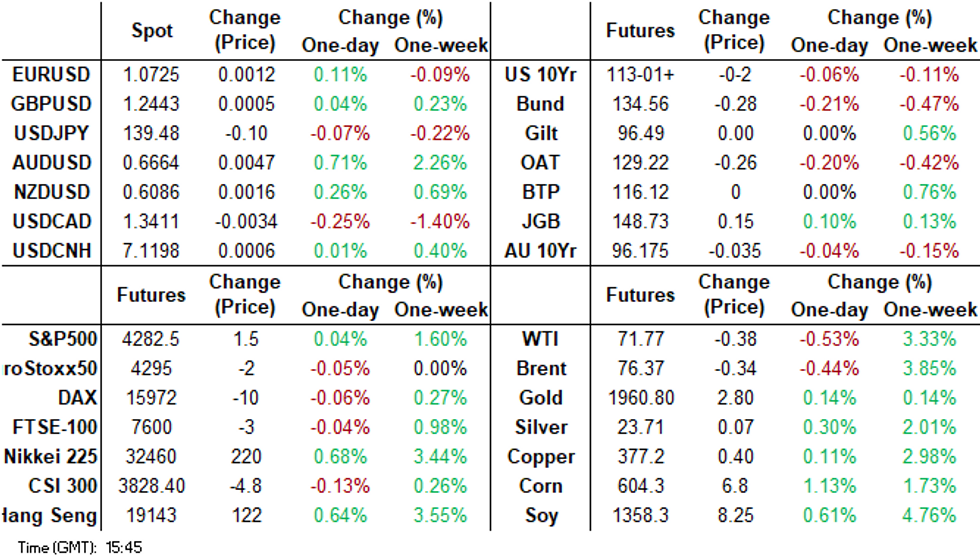

FOREX: AUD Firms After RBA Raises Cash Rate 25bps

The AUD is ~0.7% firmer in Asia today after the RBA raised the cash rate 25bps to 4.1%. Some forecasters had expected a hike however the majority rested with no change.

- AUD/USD prints at $0.6660/65, the pair is ~0.7% firmer. The pair sits above the 50-Day EMA ($0.6654) and the next upside target for bulls is $0.6710 the high from May 16.

- AUD/NZD is ~0.5% firmer, the pair printed its highest level since late February at $1.0959 before marginally paring gains. Bulls target the high from 20 Feb at $1.1088.

- Kiwi is moderately firmer as the bid in AUD spills over, NZD/USD prints at $0.6085/90 up ~0.3% from yesterday's closing levels.

- Yen is a touch firmer, USD/JPY is down ~0.1% however ranges have been narrow with little follow through for the most part.

- Elsewhere in G-10 BBDXY is down ~0.1%. NOK and SEK are ~0.4% higher however liquidity is generally poor for the currencies in the Asian session.

- Cross asset wise; e-minis are a touch firmer and 2 Year Us Treasury Yields are ~3bps higher.

- In Europe today the data calendar is thin, German Factory Orders and Eurozone Retail Sales provide the highlights.

EQUITIES: HK/China Shares Higher Again On Stimulus Hopes But Not Much Follow Through

Hong Kong and China stocks are in focus today. Hong Kong stocks have seen the greatest degree of volatility, starting weaker, before rebounding strongly on fresh stimulus hopes. Regional equity trends have been mixed elsewhere. US futures are close to flat, following Monday losses. We did see a small blip higher as HK shares rose, but there wasn't much follow through. Eminis were last around 4281/82.

- The HSI got close to 19400, but we now sit back near 19200 at the break, around 0.50% higher for the session. The HS Property sub-index is +1.59%, we were closer to +3% in earlier trade.

- Onshore China media ran reports, which stated new loans should rebound in May, whilst also stating RRR and interest rate cuts were possible for H2, quoting policy experts. This follows reports from last Friday of potential property market stimulus, per Bloomberg.

- The HK equity moves dragged mainland China stocks higher after a weaker start, but at the break, the CSI 300 is only 0.09% higher at this stage. The property sub index is +1.50% higher though.

- Elsewhere, trends are mixed. Japan stocks are modestly higher, +0.40% for the Nikkei 225, while the Taiex is +0.10% Onshore South Korean markets are closed today.

- The ASX 200 is down 0.50%, financials have been a weak point.

OIL: Crude Gives Up Monday’s Gains As Demand Outlook Drives Prices

Oil prices are down slightly today giving up most of the early gains post the Saudi announcement that it would cut its own production a further 1mbd from July, as the market became more cautious. The decision may put a floor under prices but while the demand outlook is uncertain, is unlikely to drive any sustained increase in prices. The USD is down slightly.

- Brent is 0.3% lower to $76.45 after reaching an intraday low of $76.14 before the high of $76.64. It is now up only 0.4% since Friday’s close. WTI is down 0.5% today to $71.82 with a high of $72.03 and a low of $71.54. It is now only 0.1% above Friday’s close.

- Later there is US June IBD/TIPP economic optimism, euro area April retail sales and consumer expectations. The API US inventory data is also due.

GOLD: Stronger But Remains In A Bear Cycle

Gold has experienced a slight weakening (-0.1%) during the Asia-Pacific session, following a 0.7% advance on Monday. The previous increase in gold prices occurred as tsy yields and the value of the dollar declined in response to disappointing US service-sector data. This data prompted traders to reassess their expectations regarding the Federal Reserve's path for interest rate hikes

- The May ISM Services report revealed the lowest level since December 2022, and the Prices Paid index dropped to its lowest point since May 2020. Additionally, the Employment component fell below 50 (49.2), marking the first time since December.

- FOMC dated OIS price ~6bp hike into next week's meeting with a terminal rate of ~5.25% in July. There are ~25bps of cuts priced for 2023.

- According to MNI’s technical team, the bear cycle in gold remains intact and recent short-term gains appear to have been corrective. A break of trendline support, drawn from November 3, at 1946.90 would reinforce bearish conditions and open $1903.50, a Fibonacci retracement.

CHINA DATA: China May Trade Out Tomorrow, Export Growth Expected To Slow

A reminder we have China May trade figures out tomorrow. The market looks for a noticeable slowing in export growth. The consensus looks for a -1.8% y/y outcome, versus 8.5% prior, (note the range on forecasts -11.1% to 7.0% y/y so quite wide). Base effects from last year are clearly playing a role (export growth rebounded to 16.4% in May last year from 3.5% in Apr).

- Some slowing would also be consistent with the softer backdrop presented by export orders from the official manufacturing PMI print.

- The chart below overlays the y/y change in this sub index against y/y export growth. China export growth has outperformed since the start of the year relative to other export orientated economies in NEA.

- On the import side, the market forecast is for little change in y/y momentum. The consensus sits at -8.0% y/y, versus -7.9% prior, (note the range of forecast estimates is -15.0% to -4%). The market will be watching commodity import trends closely, and broader growth momentum to gauge the domestic demand backdrop.

- The trade surplus is expected to remain healthy, projected at $95.45bn, versus $90.21bn in April.

Fig 1: China Export Growth & PMI Manufacturing Export Orders (Y/Y)

Source: MNI - Market News/Exports

ASIA FX: Mixed Trends Despite Further China Stimulus Talk

USD/Asia pairs have been mixed today. USD/CNH hasn't been able to build downside despite further talk of stimulus measures/rebound in May lending figures. SEA FX has seen some weakness, most notably THB and MYR as onshore markets have returned from holiday's yesterday. Tomorrow the focus will be on China May trade figures, while Taiwan trade figures are also out.

- USD/CNH has tried to go lower on a number of occasions today but hasn't seen much follow through. The pair was last at 7.1180/90, having seen a range of 7.1306 on the topside and 7.1063 on the downside. Property stimulus talk is again present, but this has done more for HK equities, rather than China equities, at least at an aggregate level. A meeting between US and China foreign ministry officials also suggests some thawing in tensions but there wasn't much market impact.

- USD/KRW 1 month has generally traded with a negative bias, although onshore markets have been closed today. The pair was last around the 1296/97 region. Better HK sentiment has aided the won, while the A$ post the RBA hike has also likely helped. Further prospects of China stimulus, per onshore media reports will also be a factor. The 1 month NDF is now sub its 100-day MA.

- USD/INR is dealing ~0.1% softer printing at 82.55/60 the pair has pared some of Monday’s losses as broader USD trends dominate. The pair remains in a technical up-trend, bulls look to target a break of the 83 handle. The RBI intervened in the FX market earlier in the year when we came close to the handle. Foreign Investors bought a net of $78.1mn of Indian equities on June 2, this was the 26th straight day of equity inflows. On the wires yesterday S&P Global Services PMI for May printed at 61.2 ticking lower from the prior read of 62.0 which was the cycle high of the index. Composite PMI held steady at 61.6.

- USD/MYR deals at 4.5950/80 the pair is ~0.4% higher today, onshore markets were closed yesterday for the observance of a national holiday. The ringgit has unwound some of Friday's gains as broader USD trends dominate flows. Palm Oil futures are pressured this morning, re-opening after being closed on Monday. The contract is down ~1.6% unwinding some of the gains seen late last week as we recovered off cycle lows. Malaysia PM and Finance Minister Ibrahim noted that the fiscal deficit must be reduced but not too drastically. Also saying that Malaysia's stance on raising interest rates is thorough and prudent.

- The SGD NEER (per Goldman Sachs estimates) is marginally firmer this morning, we remain well within recent ranges. We now sit ~0.8% below the upper end of the band. On the wires this morning the S&P Global Singapore May PMI ticked lower to 54.5 from 55.3. There was no estimate for the print and we remain comfortably within expansionary territory. USD/SGD prints at $1.3490/95, the pair fell below the $1.35 handle yesterday and has consolidated in a narrow range below it this morning. The pair sits between the 200-Day EMA ($1.3511) and the 20-Day EMA ($1.3459).

- Thailand markets have returned today, with USD/THB spiking back towards recent highs, the pair last in the 34.75/80 region. This is 0.6% weaker in baht terms versus closing levels from last Friday. This weakness is a little at odds with broader USD index trends in recent sessions. Recent highs come in close to 34.90, while the simple 200-day MA comes in at 35.20. On the downside the 50-day MA is back near 34.28. Headline CPI inflation for May came in well below forecasts at 0.5% y/y from 2.7% in April due to fuel and food prices and negative base effects. Inflation shot up in May 2022 to 7.1% y/y from 4.6%. Core CPI was more stable at 1.6% y/y down from 1.7%.

THAILAND DATA: Inflation Falls Sharply On Base Effects, Core Steadier

Headline CPI inflation for May came in well below forecasts at 0.5% y/y from 2.7% in April due to fuel and food prices and negative base effects. Inflation shot up in May 2022 to 7.1% y/y from 4.6%. Core CPI was more stable at 1.6% y/y down from 1.7%. This further easing of inflation pressures to an almost 2-year low, and the Commerce Ministry’s warning that June headline inflation could contract on fuel & power prices should mean that the Bank of Thailand is on hold in August after hiking rates to 2% in May. This could be the terminal rate if the tourism-related inflation risks don’t materialise.

Thailand CPI y/y%

Source: MNI - Market News/Refinitiv

SOUTH KOREA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of South Korean Newspapers and some other major news outlets from the past day or so.

ECONOMY: Korea's export dependency on China dips below 20% (link)

ECONOMY: Korea’s export destinations diversify as shipment to China remains sluggish (link)

ECONOMY: S. Korea’s manufacturing production capacity index hits record low in 38 months (link)

ECONOMY: Korea to up service exports to $250 bil. by 2030 (link)

HOUSING: New apartment prices in Korea soar on cement price hikes (link)

MARKETS: Foreign investor registration system abolished after 30 years (link)

TRADE: Imported car sales fall 9.2% in May on lack of supply volumes (link)

TRAVEL: Air passengers rise 24 percent in May amid return to pre-pandemic normalcy (link)

TRAVEL: Flights between Korea, Japan to increase to 1,000 a week (link)

US/S.KOREA: Yoon says alliance with US upgraded to 'nuclear-based alliance' (link)

POPULATION: Elderly Outnumber 20-Somethings in Korea's Workforce (link)

Indonesia: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of Indonesian Newspapers and some other major news outlets.

Economy: “Global economic growth to reach 2.8% in 2024: BI” – Antara News (see here)

- BI Governor Warjiyo said that global growth can reach 2.7% in 2023 and 2.8% in 2024 supported by developing countries and lower inflation. Growth in ASEAN is forecast to be 5.1% and 5.5%.

Economy: “Market expansion, CEPAs to boost manufacturing PMI: minister” – Antara News (see here)

- Minister sees the expansion of export markets and economic agreements to increase output and the PMI over 2023. He saw the decline in the May PMI as driven by soft foreign orders but he’s not “worried”.

Economy: “Govt, BI successfully controlling inflation together: Minister” – Antara News (see here)

Economy: “Economic recovery uniform across Indonesia: Minister Indrawati” – Antara News (see here)

Energy: “Global turmoil to make 2024 oil prices difficult to predict: minister” – Antara News (see here)

- The Finance Minister noted that oil prices are currently difficult to predict after Saudi Arabia cut output further. The ministry expects crude to be $80-$85/bbl in 2023 and $75-$85 in 2024. Indonesia is a net oil importer but is also an oil exporter, particularly within the region. Coal, one of the main exported commodities, is expected to decline to $200/mt in 2023 and then to $155 in 2024. She said these prices are important as they impact the budget significantly.

Trade: ASEAN works towards expanding RCEP trade deal membership” – Jakarta Globe (see here)

Geopolitics: “Ministers discuss improving Indonesia-China defence cooperation” – Antara News (see here)

Geopolitics: “Indonesia, Germany agree to improve defense collaboration” – Antara News (see here)

Geopolitics: “Indonesian-Australia cooperation important for peace: defence minister” – Antara News (see here)

Politics: “PAN signals support for Ganjar’s 2024 bid” – Jakarta Globe (see here)

Politics: “Golkar aims for 20 pct of house seats in 2024” – Jakarta Globe (see here)

Politics: “Mahfud turns down offer to become running mate for Anies” – Jakarta Globe (see here)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/06/2023 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 06/06/2023 | 0700/0900 | ** |  | ES | Industrial Production |

| 06/06/2023 | 0730/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 06/06/2023 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 06/06/2023 | 0900/1100 | ** | | EU | Retail Sales |

| 06/06/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 06/06/2023 | 1230/0830 | * |  | CA | Building Permits |

| 06/06/2023 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 06/06/2023 | 1400/1000 | * | | CA | Ivey PMI |

| 06/06/2023 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.