Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

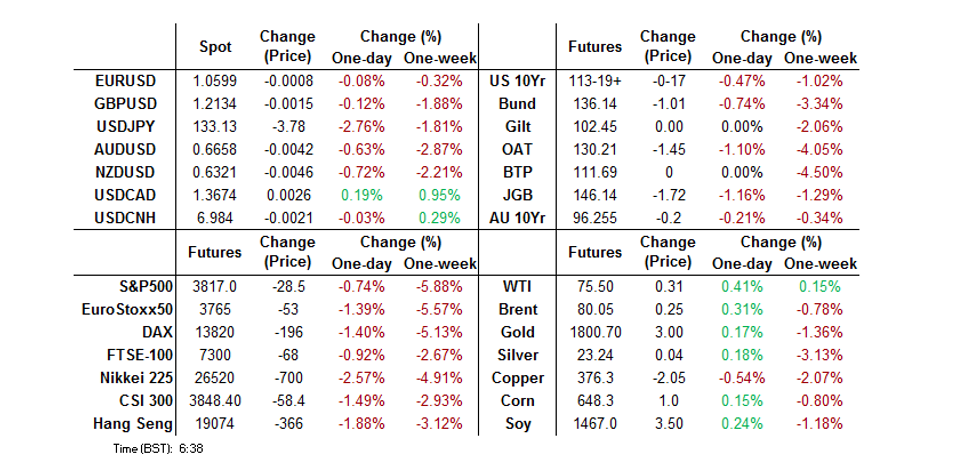

- JGBs experienced a state of freefall after the BoJ deployed a surprise widening of its permitted 10-Year trading band (to -/+0.50% vs. the previous -/+0.25%) at the end of its latest monetary policy decision. The BoJ obviously got to a point whereby enough was enough, noting that market volatility has heightened in recent months, with a modification in the YCC parameters apparently implemented to improve market functioning (the BoJ now holds over 50% of outstanding JGBs for the first time).

- JPY strength has dominated post the BoJ YCC shift.

- Outside of Kuroda's press conference, the upcoming focus will be on German PPI & ECB speak, while in the U.S., housing starts and building permits data are due.

US TSYS: BoJ Policy Tweaks Applies Notable Pressure, Triggers Huge Volume

The BoJ’s YCC tweak (outlined elsewhere) has loosened what is arguably the final remaining anchor for global duration, which pressured wider core global FI markets during the Asia-Pac session.

- That leaves the major cash Tsy benchmarks running 1.5-10.0bp cheaper into London hours, bear steepening. TYH3 is -0-18+ at 112-18, 0-06+ off the base of its 0-26 range, on outstanding volume of ~365K.

- Modest two-way gyrations had been observed pre-BoJ as Asia-Pac participants set up for the event and adjusted to Monday’s wider price action.

- A flurry of screen sales dominated post-meeting, with a block sale of TY futures also observed (-2,023).

- BoJ Governor Kuroda’s post-meeting press conference will dominate into London hours. ECB speak will then headline after the London handover, while building permits and housing starts data provides the most notable round of economic data during the NY session.

JGBS: BoJ Stirs Memories Of 1989

JGBs experienced a state of freefall after the BoJ deployed a surprise widening of its permitted 10-Year trading band (to -/+0.50% vs. the previous -/+0.25%) at the end of its latest monetary policy decision.

- The BoJ obviously got to a point whereby enough was enough, noting that market volatility has heightened in recent months, with a modification in the YCC parameters apparently implemented to improve market functioning (the BoJ now holds over 50% of outstanding JGBs for the first time).

- As a countermeasure to the potential for a fairly swift challenge of the BoJ’s new YCC settings it decided to deploy upsized JGB purchases in Jan-Mar ’23., as well as implementing a flurry of unscheduled Rinnban and fixed rate operations during the Tokyo session (with the fixed rate purchases also being deployed outside of the usual 5- to 10-Year zone, covering 1- to 5-Year paper). The deployment of scatter gun purchases during afternoon trade helped stem losses, with futures failing to challenge their cycle low (drawn off a continuation chart).

- JGB futures now sit ~160 ticks lower on the day nearly 80 ticks off worst levels. Cash JGBs run 2-17bp cheaper, with 10s coming under the most pressure, printing just off session cheaps at ~0.42%.

- Swaps spreads have widened across the entirety of the curve, excluding 10s, given the previous limitations placed on 10-Year JGB yields prior to today’s adjustment. There is still a ~35bp differential observable in 10-Year swap rates vs. JGB yields.

- BoJ Governor Kuroda’s post-meeting press conference provides the immediate domestic focal point.

AUSSIE BONDS: Early Weakness Extends On BoJ Policy Move

Aussie bonds were under pressure for the majority of the Sydney session, initially extending weakness on cross-market type flows vs. NZ & U.S. equivalents, before the surprise BoJ policy tweak that we have outlined elsewhere applied pressure to the wider core global FI sphere, allowing the early cheapening & steepening to extend.

- That left YM -11.0 & XM -20.0 at the bell, with a fairly parallel shift observed in the 10+-Year of the cash curve.

- Weakness in bonds drove the move as EFPs narrowed post-BoJ.

- Bills finished flat to 10bp cheaper through the reds, bear steepening. Meanwhile, RBA dated OIS pricing was incrementally higher, albeit ultimately little changed, showing 19bp of tightening for the Feb ’23 decision, alongside a terminal cash rate of ~3.78%.

- The minutes from the latest RBA decision showed that everything from no change to a 50bp hike in the cash rate was discussed earlier this month (ultimately a third consecutive 25bp hike was enacted). The fact that the Bank openly discussed a pause in tightening for the first time this cycle gave some watchers more conviction in their call that we are nearing the end of the current tightening cycle. Still, this had little in the way of meaningful impact on price action, with the cheapening factors dominating.

- Looking ahead, Wednesday’s local docket is headlined by the monthly Westpac leading index print.

NZGBS: Twist Steepening Seen, Shielded From BoJ, Swap Rates Not So Privileged, Shunt Higher

NZGBS were insulated from the fallout from the latest BoJ decision, owing to the closing time of the market. This came after an all-time low headline ANZ business confidence reading, in lieu of the whirlwind round of tightening from the RBNZ, allowed the space to recover from the early session cheaps, which came as local participants reacted to Monday’s wider cheapening in core global FI markets.

- Swap rates weren’t sheltered from the initial post-BoJ impulse, as they pulled away from their session base, finishing 3-11bp higher, with some notable steepening evident, facilitating a further pull away from the post GFC lows in the 2-/10-Year swap spread.

- RBNZ dated OIS pricing was little changed on the day, with ~72bp of tightening priced for the Feb ’23 meeting alongside a terminal OCR of ~5.55%.

- Looking ahead, Wednesday’s local docket will be headlined by monthly trade balance data, the latest consumer confidence print from ANZ and credit card spending readings, although the delayed reaction to the BoJ move will likely dominate local matters.

FOREX: Yen Cross Liquidation Post BoJ

JPY strength has dominated post the BoJ YCC shift. USD/JPY eventually got down to a the 133.00 level, a near 3% gain in yen terms. This is fresh lows for the pair back to mid-August. We have stabilized somewhat, last around the 133.15 level, with Kuroda's press conference the focus early in London.

- The initial impetus was for the rest of G10 to rally post the BoJ, but this quickly reversed as cross asset headwinds materialized. Equities were weaker across the board (US/EU futures down over 1%), while core yields rose. US 10yr are around 10bps higher, last tracking at 3.68%.

- AUD/USD rose above 0.6740 post the BOJ, but is now back at 0.6630/35, 1% down for the session. This leaves AUD/JPY off by 3.66% and back to the 88.35/40 region.

- NZD/USD was initially an underperformer relative to the A$, following poor survey data, but losses have been on par this afternoon. NZD/USD is threatening uptrend channel support, last close to 0.6300.

- EUR/JPY is back sub 141.00, note the simple 200-day MA comes in close to 140.12.

- Outside of Kuroda's press conference, the upcoming focus will be on German PPI, while in the US housing starts are due.

FX OPTIONS: Expiries for Dec20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0350-55(E725mln), $1.0549-50(E518mln), $1.0700-05(E557mln)

- USD/JPY: Y136.32($573mln)

- AUD/USD: $0.6640-60(A$1.4bln), $0.6725(A$649mln), $0.6900(A$679mln)

- NZD/USD: $0.6179-95(N$725mln)

- USD/CNY: Cny7.0000($580mln), Cny7.2000($991mln)

ASIA FX: Only USD/KRW Follows USD/JPY Lower

The initial reaction in USD/Asia pairs was to move lower in sympathy with USD/JPY post the BoJ policy announcement. However, this proved to be short lived, as cross asset headwinds from weaker equities and firmer yields weighed. Only the won is showing a meaningful gain against the USD so far today. Taiwan export order data prints a little later, while tomorrow South Korean first 20-day trade data for December is out.

- USD/CNH dipped towards 6.9700 post BoJ but is now back near 6.9900, slightly higher for the session. China equities continue to weaken, the CSI 300 off nearly 2%. As expected, the LPRs were left unchanged, while the fixing bias shifted back to a firmer CNY trend.

- 1 month USD/KRW fell below 1290 after the BoJ before finding support. The pair climbed back to 1300 before renewed selling interest emerged. We last tracked close to 1293. Onshore equities are weaker, the Kospi down nearly 1%, while net equity outflows picked up.

- USD/TWD spot is down from earlier highs, last around 30.75. The trend in the pair still looks skewed to the upside. Onshore equities have fallen by 1.8% today, while the market expect export orders to show further weakness for the November print (-12.8% forecast against -6.3% prior).

- USD/MYR is slightly higher, last around 4.4335, +0.10% for the session. The simple 200-day MA is nearby at 4.4377. New PM Anwar will table the 2023 budget by early March next year. He also announced a fresh 2bn MYR in cash aid, while the retail prices of 11 food items will be capped between Dec 23-27.

- USD/INR is once again close to the top end of its recent range, last around 82.83. Intervention risks will be higher at these levels. USD/IDR is also firmer but is not as close to recent highs as USD/INR. The rupiah last changed hands at 15626, unable to hold sub 15600 from earlier in the session. The risk of higher core yields likely weighing.

EQUITIES: Weakness Follows BoJ YCC Shift, Shanghai Property Index Back Below 200-Day MA

Regional equity markets are down across the board, with sentiment weighed by the BoJ surprise YCC shift. US and EU futures are down near -1/-1.2% at this stage across the major bourses.

- The Nikkei 225 is off by over 2.6%. The market was tracking higher prior to the lunch break, but the BoJ's shift on YCC saw push sharply lower when trading resumed. The high to low move was around 3.4%. All eyes will rest on Kuroda's press conference later.

- The HSI is down nearly 2%, with weakness fairly broad based. At 3pm HK time we will have a press conference with a further easing in Covid restrictions to be announced.

- The property sub-indices remain under pressure, as developers continue to raise cash through share placements. Onshore, the Shanghai Property sub-index is down a further 2.43% and is back below its simple 200-day MA.

- The Kospi and Taeix are both lower, with offshore tech leads also weighing in this space.

- The Philippines index is the only regional bourse higher at this stage, +0.35%.

GOLD: Rangebound, As Higher Core Yields Help Offset Weaker USD Post BoJ

Gold spiked post the BoJ announcement but couldn't get much beyond the $1795 level. We last sit close to $1790, only up slightly for the session and lagging broader USD index moves (BBDXY -0.30%).

- In terms of near term levels, Monday session highs were close to $1799, while on the downside dips sub $1785 have been supported. Overall though we remain range bound.

- A firmer yen, to the extent that it spills over to broader USD weakness, should be positive gold. However, the evidence is mixed on this so far, with the USD mostly recovering (ex JPY) post the BoJ.

- The spill over of higher Japan yields to the rest of the world may also work against gold demand. We saw last week gold suffered amidst a more hawkish ECB outlook.

OIL: Early Gains Unwound As Cross Asset Headwinds Dominate

Brent crude has unwound early session gains, last tracking just below $80/bbl. We did get to $80.90/bbl in the first part of the session, but weaker risk appetite post the BOJ decision has weighed on sentiment. WTI has followed a similar path, last around $75.40. Both benchmarks rose by around ~1% for Monday's session.

- Stepping back, crude is still in the middle of recent ranges. For Brent we have been in a rough $75-$83/bbl range in recent weeks.

- On the supply front, TC Energy's restart plan for the Keystone is under review with the US authorities. Elsewhere, North Dakota has 300k barrels per day offline following a blizzard last week and will reportedly take a number of weeks to come back online.

- This evening we have the API weekly report on US oil inventories due.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/12/2022 | 0700/0800 | ** |  | DE | PPI |

| 20/12/2022 | 1000/1000 | ** |  | UK | Gilt Outright Auction Result |

| 20/12/2022 | 1000/1100 | ** |  | EU | EZ Current Account |

| 20/12/2022 | - | *** |  | JP | BOJ policy announcement |

| 20/12/2022 | 1330/0830 | ** |  | CA | Retail Trade |

| 20/12/2022 | 1330/0830 | *** |  | US | Housing Starts |

| 20/12/2022 | 1330/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 20/12/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 20/12/2022 | 1500/1600 | ** | | EU | Consumer Confidence Indicator (p) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.