Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

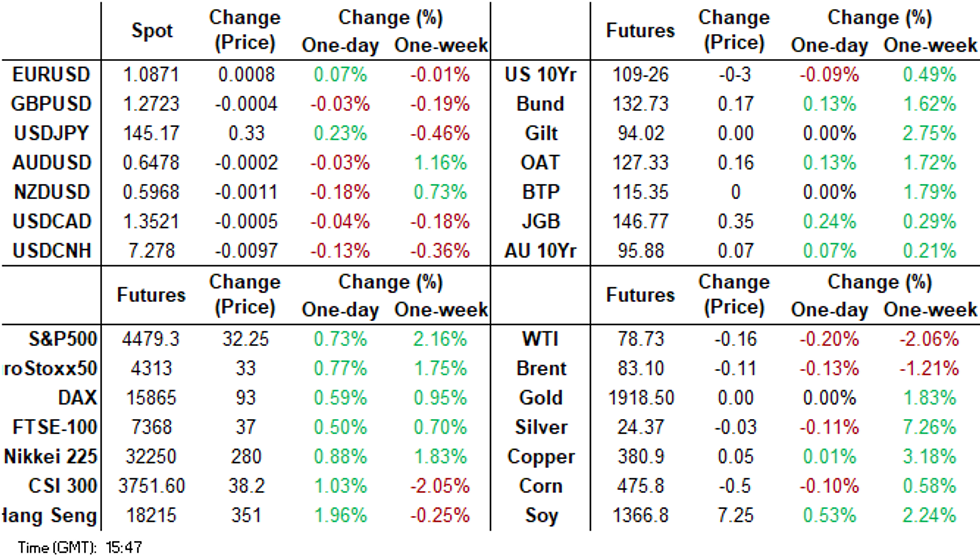

- Regional equities are firmer in Asia Pac trade on Thursday, as US futures have maintained a strong positive tone during the session. Shares in chip/AI bellwether Nvidia surged in extended trading as the company delivered stronger than expected sales for the 3rd straight quarter. This hasn't weighed on the USD much though, although yen has underperformed in the G10 space. USD/Asia pairs are lower, led by equity/tech sensitive plays.

- US Tsys trimmed some of yesterday's gains in early dealing, but had little follow through and tsys observed narrow ranges for the remainder of the session. JGB futures are stronger, +30 compared to settlement levels, having consolidated the overnight strengthening sparked by weaker-than-expected EU & US PMIs.

- The benchmark JGB 10-year yield is 1.4bp lower at 0.660% versus the post-BoJ YCC tweak high of 0.68% set yesterday. Tomorrow the local calendar sees Tokyo CPI for August and PPI for July.

- Looking ahead, there is a thin docket in Europe today, further out we have US initial jobless claims and durable goods. Kansas City Fed’s annual economic policy symposium in Jackson Hole begins. Fedspeak from Philadelphia Fed President Harker and Boston Fed President Collins will cross. The latest 30-Year TIPS Supply is also due.

MARKETS

US TSYS: Narrow Ranges In Asia

TYU3 deals at 109-25, -0-04, a 0-05+ range has been observed on volume of ~105k.

- Cash tsys sit 1bp cheaper to flat across the major benchmarks, light bear flattening is apparent.

- Tsys trimmed some of yesterday's gains in early dealing, there was no obvious headline driver for the move which came alongside the USD firming from session lows. Perhaps participants are looking ahead to Fed Chair Powell's speech on Friday, using yesterday's richening as an opportunity to enter fresh short positions.

- The early move lower didn't follow through and tsys observed narrow ranges for the remainder of the session. There was little meaningful macro news flow.

- There is a thin docket in Europe today, further out we have US initial jobless claims and durable goods. Kansas City Fed’s annual economic policy symposium in Jackson Hole begins. Fedspeak from Philadelphia Fed President Harker and Boston Fed President Collins will cross. The latest 30-Year TIPS Supply is also due.

JGBS: Futures Holding Richer, Near Session Highs, Tokyo CPI Tomorrow

JGB futures are stronger, +30 compared to settlement levels, having consolidated the overnight strengthening sparked by weaker-than-expected EU & US PMIs.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined weekly investment flow data that showed offshore purchases of Japanese bonds surged last week, while local investors continued to sell offshore bonds.

- Accordingly, local participants have likely been on headlines and US tsys watch.

- US tsys sit 1bp cheaper to flat across the major benchmarks, light bear flattening is apparent. US tsys trimmed some of yesterday's gains in early dealing, but there was no obvious headline driver for the move which came alongside the USD firming from session lows. Perhaps participants are looking ahead to Fed Chair Powell's speech on Friday, using yesterday's richening as an opportunity to enter fresh short positions.

- The cash JGB curve has twist-flattened, with yields 0.1bp higher to 3.8bp lower (20-year). The benchmark 10-year yield is 1.4bp lower at 0.660% versus the post-BoJ YCC tweak high of 0.68% set yesterday.

- The swaps curve has bull flattened, with swap spreads broadly wider.

- Tomorrow the local calendar sees Tokyo CPI for August and PPI for July. Department Store Sales for July are also on tap.

AUSSIE BONDS: Richer But Have Pared Early Gains, Tracking US Tsys

ACGBs (YM +5.0 & XM +7.0) are stronger but have pared early gains sparked by weaker-than-expected EU & US PMIs. With the domestic data docket empty today, local participants have likely eyed headlines and US tsys.

- US tsys have been pressured in recent dealing, the move comes alongside a move off session lows in the USD. US tsys sit flat to 2bp cheaper across the major benchmarks, with the curve flatter.

- Cash ACGBs are 5-7bp richer with the AU-US 10-year yield differential +2bp at -8bp.

- Swap rates are 4-5bp lower, with the 3s10s curve flatter and EFPs wider.

- The bills strip has bull flattened, with pricing flat to +5.

- RBA-dated OIS pricing is 2-5bp softer for meetings beyond December, with May'24 leading.

- Tomorrow the local calendar is empty.

- July retail sales print on Monday, August 28. They fell 0.8% m/m in June to be up 2.3% y/y. Since that release, CBA has published its revamped household spending series. See MNI CBA Spending Insights Shows Continued Soft Consumption for more details. In July the HSI was flat on the month to be up 1.3% y/y. A flat reading for July retail sales would result in annual growth easing further to 1.6%.

NZGBS: Sharply Richer But Pared Gains Into The Close

NZGBs closed 7-10bp richer, but 3-4bp off session bests. The away from session bests coincided with a cheapening in US tsys in Asia-Pac trade.

- US tsys have been pressured in recent dealing, the move comes alongside a move off session lows in the USD. US tsys sit flat to 2bp cheaper across the major benchmarks, with the curve flatter.

- Today’s weekly supply also likely weighed, particularly at the short end. The NZGB auctions showed mixed results, with the cover ratio for the Apr-27 bond collapsing to 1.38x from 2.79x. Meanwhile, the cover ratios for the May-32 and May-51 bonds held around 3.00x. In post-auction trade, the lines were flat to 0.5bp cheaper, led by the Apr-27 bond.

- RBNZ publishes new residential mortgage lending data for July. Lending to all borrowers fell 12% m/m to NZ$5.0bn, the lowest for July since 2017. (See link)

- Swap rates are 4-9bp lower, with the 2s10s curve 4bp flatter and implied swap spreads wider.

- RBNZ dated OIS pricing is 3-6bp softer for meetings beyond October, with Jul’24 leading. Terminal OCR expectations soften 3bp to 5.64%.

- Tomorrow the local calendar is empty.

STIR: $-Bloc June’24 Easing Expectations Little Changed After Weak Global PMIs

Expectations regarding easing by June 2024 in the $-Bloc are little changed from earlier in the week, despite the latest round of US, European and Australian PMI data pointing to a greater-than-expected slowdown in economic activity.

Figure 1: $-Bloc STIR: Terminal Rate Expectations & June’24 Pricing

Source: MNI – Market News / Bloomberg

FOREX: Narrow Ranges In Asia

There have been narrow ranges across G-10 FX with little follow through on moves in Asia.

- Kiwi is marginally pressured, NZD/USD trimmed some of yesterday's gains before unwinding a ~0.3% loss to sit ~0.1% lower last printing at $0.5970/75.

- AUD/USD is little changed, the pair briefly dealt above Wednesday's high however there was little follow through and gains were pared. Despite the recent rally the trend outlook is bearish, support comes in at $0.6365 (low from Aug 17) and resistance is at $0.6522 (20-Day EMA).

- Yen is marginally softer, however USD/JPY remains well within recent ranges. Support comes in at ¥144.17, the 20-Day EMA, and ¥143.00, low from Aug 9. Resistance is at ¥146.56 (Aug 17 high) and ¥146.93 (8 Nov 22 high).

- Elsewhere in G-10; SEK is pressured however liquidity is poor in Asia and GBP is ~0.1% firmer.

- Cross asset wise; US Equity futures are firmer after Nvidia's bullish revenue outlook spills over into a wider bid. E-minis are up ~0.7% and NASDAQ futures are up ~1.3%. BBDXY is down ~0.1% and US Tsy Yields are ~1bp firmer across the curve.

- There is a thin docket in Europe today, further out we have US Durable Goods and Initial Jobless Claims.

JAPAN DATA: Offshore Investors Switch From Local Stocks To Bonds

Weekly investment flows into Japan stocks and bonds were mixed last week. Offshore purchases of local bonds surged to ¥1131.5bn, the first weekly inflow since the start of July and the largest weekly inflow since early April. Net outflows from local stocks provided some offset, printing at -¥740.7bn. This was the largest weekly outflow since end March.

- In terms of Japan purchases abroad, we saw a modest pick up in flows to offshore equities, ¥185.6bn. This was the first outflow to foreign stocks since mid June. Local investors continued to sell offshore bonds though, -¥263.2bn.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending August 18 | Prior Week |

| Foreign Buying Japan Stocks | -740.7 | 226 |

| Foreign Buying Japan Bonds | 1131.5 | -871.1 |

| Japan Buying Foreign Bonds | -263.2 | -333.6 |

| Japan Buying Foreign Stocks | 185.6 | -54.2 |

Source: MNI - Market News/Bloomberg

EQUITIES: Surging US Tech Futures Aid Asia Pac Sentiment

Regional equities are firmer in Asia Pac trade on Thursday, which follows a positive lead from US/EU markets in Wednesday trade. US futures have also maintained a strong positive tone during the session, with the Nasdaq leading the charge, +1.24%, while Eminis are +0.68%, last near 4477 and the simple 50-day MA on the topside. Shares in chip/AI bellwether Nvidia surged in extended trading as the company delivered stronger than expected sales for the 3rd straight quarter.

- Hong Kong markets have been amongst the strongest performers, the HSI up 1.91% to the break. The tech sub index up over 3% at this stage, its 3rd straight session of gains.

- China stocks were slow to post gains in the first part of trading, but the CSI 300 is up nearly 1% to the break. The Shanghai Composite is near +0.50% firmer.

- Tech sensitive plays like the Kospi, have also rallied, the bourse up 1%, while the Taiex +0.80% at this stage. Offshore investors have added $246.1mn to local Korean shares.

- Japan stocks have lagged, the Topix up 0.25%, the Nikkei 225 +0.45%. The head of the Japan Exchange Group stated that the benefits of a weaker yen were diminishing for Japan stocks.

- In SEA, market gains have been more limited, with bourses rising less that 1% for the most part. The Philippines is the exception, up 1.2% at this stage. The JCI is lagging in Indonesia, close to flat.

OIL: Crude Off Lows But Possible Supply Increase Weighs On Prices

Oil is off its intraday low but still down during the APAC session. Prices fell almost 1.5% on Wednesday and are down another 0.3% today, as a possible easing of sanctions against Venezuelan oil would increase supply. The USD index is 0.1% lower.

- WTI is down 0.3% to $78.62/bbl but off the low of $78.27 earlier in the session. Brent is 0.3% lower at $82.99 but has struggled to hold breaks above $83 today. It is off the low of $82.64.

- The possible temporary lifting of sanctions against Venezuela comes at a time of soaring Iranian crude shipments, but also Saudi/Russia output cuts and low US stockpiles. The market also remains concerned re demand given the disappointing recovery in China and possibly further rate hikes in the US.

- Woodside employees vote today on the “in-principle” agreement between the company and unions. If supported, industrial action will be called off. The Chevron ballot deadline is today. European LNG prices fell on Wednesday on optimism that there would be a deal.

- Later the Fed’s Harker and Collins speak. On the data front there are US jobless claims, July durable goods orders and Chicago & Kansas City Fed Indices.

GOLD: Strong Rally On Back Of Declines In USD & Bond Yields

Gold is slightly stronger in the Asia-Pac session, after closing +1.0% at $1915.48 on Wednesday. Bullion benefited from the sharp reversal of recent USD strength and a large rally in US tsys.

- US tsys strengthened in the European session as European bonds reacted to weaker-than-expected Euro Area PMIs. US tsys then extended gains after flash US PMIs printed softer than forecast, with technical flows and position squaring adding a level of support through the session. US tsys finished 8-13bps richer across the major benchmarks.

- The pivotal economic event of this week centres on the speech by Fed Chair Powell at the Jackson Hole gathering on Friday. The prevailing concern is that Powell might undermine investors' optimistic expectations, specifically the notion that the Federal Reserve has concluded its interest rate hikes and is poised to initiate rate cuts in the early months of the upcoming year.

- According to MNI's technicals team, Wednesday’s high of $1920.40 cleared resistance at $1916.3 (20-day EMA) to open $1932.7 (50-day EMA).

SOUTH KOREA: BOK - Another Hawkish Hold

The BOK left rates on hold as widely expected at 3.50%. The statement strikes a hawkish tone though, with the central bank stating that rates will be restrictive for a considerable period, while making a judgement whether to raise the base rate further.

- In terms of forecasts, the BoK's GDP and inflation forecasts for 2023 were left unchanged, at 1.4% for growth and 3.5% for headline CPI. 2024 GDP growth expectations were nudged down to 2.2% from 2.3%, while headline CPI was left unchanged at 2.4%. The core inflation forecast for 2023 was nudged up to 3.4% from 3.3%.

- The central bank expects August inflation to print around 3% and remain above target for a considerable time. This leaves the board making a judgement regarding the need to raise rates further.

- Factors deciding this path include inflation, financial stability, economic downside risks, the impact of cumulative rate rises, monetary policy offshore and household debt growth.

- The growth recovery is expected to be moderate, with household spending improving modestly, while the drag from export growth should subside. Considerable uncertainty remains over the outlook though, with China and the timing of the tech cycle rebound highlighted.

- House prices and household borrowing were highlighted as watch points.

ASIA FX: Equity Gains Drive USD/Asia Pairs Lower, Tech Sensitive Plays Outperform

USD/Asia pairs are lower today, with equity sensitive plays outperforming, particularly in the tech space. This has been evident for both KRW and TWD. The regional equity tone has been strong, led by higher US tech futures post the Nvidia results. USD/CNH has been faded on upticks, the pair touching fresh lows for the week sub 7.2700. Still to come is the BI decision, with no change expected. Tomorrow, Malaysia CPI is out, along with Singapore IP and Thailand trade.

- USD/CNH has turned back lower. We hit fresh lows for the week at 7.2679, but sit back above 7.2700 in latest dealings. Earlier highs were near 7.2950. Onshore equities started slowly, but gains have improved as the session progressed. The CSI 300 now up over 1.3%, while the HSI has rallied more than 2%. For USD/CNH we aren't too far off the 20-day EMA, near 7.2600. The pair hasn't been sub this support level since late July in any meaningful way.

- Spot USD/KRW has sunk 1.4% today to be back near 1320. This is back to earlier August levels, with the won riding the better equity wave in the tech space. The Kospi is +1.20% firmer at this stage, with offshore investors adding nearly $300mn to local equities so far. A hawkish BoK hold earlier also likely helped at the margins. Spot is close to its 20-day EMA (~1319), but the 1 month NDF has already tested this support point.

- Spot USD/TWD has played some catch up to the downside, the pair slipping 0.50% to be back at 31.76. The 20-day EMA isn't far off at 31.74. The better tone to tech equities has aided local shares, the Taiex +1.2% at this stage.

- Spot USD/HKD broke above 7.8400 late yesterday and hit highs in NY trade near 7.8425. We sit slightly lower now, back near the 7.8395 level, having been range bound for much of today's session. US-HK yield differentials maintained an uptrend for Wednesday, with the US yield pullback less evident in the very short end. 3 month Hibor fell to 4.78% in yield terms on Wednesday, we were above 5% at the end of last week.

- USD/IDR is back near 15250, lows back to the first half of August. We aren't too far away from the simple 200-day MA which comes in at 15210, the 20-day EMA is slightly higher around ~15218. Spot IDR gains are close to 0.30% at this stage. The rupiah is benefiting from the broader improvement in risk appetite, which is being led by global equities at this stage. The focus ahead will be on the upcoming BI policy meeting later. No changes to rates are expected, with recent IDR weakness the central bank is unlikely to turn too dovish.

- The Ringgit has firmed in early dealing as participants digest yesterday's US PMI print which was softer than forecast. USD/MYR is down ~0.3% and sits a touch above the 4.64 handle. In Wednesday's dealing USD/MYR edged higher printing it's highest close since mid-July. July CPI crosses tomorrow, a downtick in inflation to 2.1% Y/Y from 2.4% is expected.

- The Rupee has opened dealing on the front foot as local participants digest yesterday's US PMI print which was softer than forecast. USD/INR prints at 82.45/46, the pair is ~0.3% lower today. Reserve Bank of India's Das said on Wednesday that core inflation was still elevated although he expects food prices to start cooling from September. A reminder that the docket is empty for the remainder of the week.

- The SGD NEER (per Goldman Sachs estimates) is marginally firmer in early dealing and sits a touch off its highest level since 3 Aug. The measure is ~0.5% below the top of the band. USD/SGD is softer in early dealing , the pair is ~0.1% lower this morning. Broader USD trends dominated flows yesterday, the pair fell ~0.5% after the softer than forecast US PMI print. Looking ahead on the wires tomorrow we have July Industrial Production. A fall of 3.4% Y/Y is expected.

INDONESIA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of Indonesian Newspapers and some other major news outlets.

Economy: “Bank Indonesia to hold rates steady as currency wobbles on Fed” – Bloomberg (see link, also see MNI Bank Indonesia Preview - August 2023: FX Stability Centre Stage)

Economy: “Indonesia’s economy to top 5 percent in 2023: central bank” – Jakarta Globe (see link)

Economy: “Civil servant salary increase will not cause inflation: ministry” – Antara News (see link)

- Civil servants will receive an 8% wage rise from the start of 2024 and pensions for retired civil servants will rise 12%. President Jokowi has said the pay increase has to be accompanied by increases in productivity.

Economy: “Indonesia’s digital economy has grown rapidly: finance ministry” – Antara News (see link)

Economy: “Indonesia needs US$200 bln for sustainable development: minister” – Antara News (see link)

Industry: “Govt aims to make Indonesia world’s largest EV battery producer” – Antara News (see link)

Trade: “China to import more Indonesian palm oil in 2024: Gapki” – Jakarta Globe (see link)

Trade: “RI eyes US$3.37 billion non-oil, gas export target with Australia” – Antara News (see link)

Trade: “Russia is crucial trade partner for ASEAN: Indonesian trade minister” – Antara News (see link)

Geopolitics: “Jokowi embarks on first African Tour” – Jakarta Globe (see link)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/08/2023 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 24/08/2023 | 1000/1100 | ** |  | UK | CBI Distributive Trades |

| 24/08/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 24/08/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 24/08/2023 | 1230/0830 | * |  | CA | Quarterly financial statistics for enterprises |

| 24/08/2023 | 1230/0830 | ** | | US | Durable Goods New Orders |

| 24/08/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 24/08/2023 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 24/08/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 24/08/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 24/08/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 30 Year Bond |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.