Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

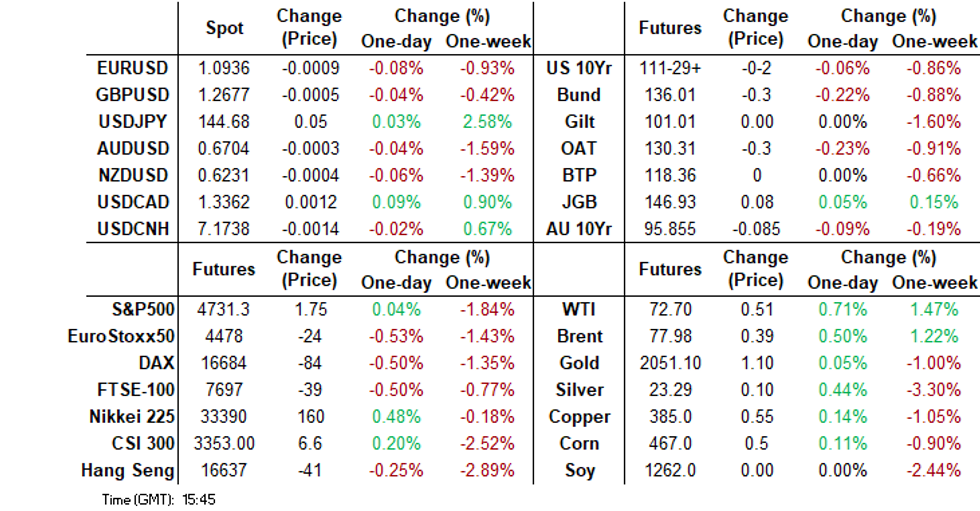

- Cash US tsys are dealing little changed in today's Asia-Pac session, ahead of the release of Non-Farm Payrolls data later today. Bloomberg consensus sees nonfarm payrolls growth of 171k in December after November’s 199k was boosted by 38k workers returning from strikes. See MNI's NFP Preview here.

- The USD has been supported on dips, but overall ranges have been muted. Regional equity sentiment has been mixed, while oil is tracking higher for the week, gold lower.

- Looking ahead, outside of the US NFP report, highlights will be Eurozone inflation figures. Additionally, German retail sales, UK construction PMI and Canada jobs data are all scheduled.

- Next week Tokyo CPI is out, along with Australian monthly CPI, as well as China inflation figures.

MARKETS

US TSYS: Cash Bonds Little Changed Ahead Of NFP Data

TYH4 is trading at 111-29+, -0-02 from NY closing levels.

- Cash US tsys are dealing little changed in today's Asia-Pac session, ahead of the release of Non-Farm Payrolls data later today.

- Bloomberg consensus sees nonfarm payrolls growth of 171k in December after November’s 199k was boosted by 38k workers returning from strikes. See MNI's NFP Preview here.

JGBS: Little Changed Ahead Of US Payrolls, Holiday On Monday, Tokyo CPI On Tuesday

JGB futures have pared overnight weakness back to an uptick of +4 compared to settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Monetary Base and Jibun Bank Services & Composite PMI data. Consumer confidence is due later but is unlikely to be a market mover.

- Accordingly, local participants appear to have been content to fade overnight US tsy-induced weakness through the local session ahead of tonight’s release of US Non-Farm Payrolls.

- Bloomberg consensus sees nonfarm payrolls growth of 171k in December after November’s 199k was boosted by 38k workers returning from strikes. See MNI's NFP Preview here.

- Bloomberg reported that more BoJ watchers joined those pushing back their predictions for the end of negative rates in the wake of the New Year’s Day earthquake and recent remarks by Governor Kazuo Ueda. (See link)

- Cash US tsys are dealing little changed in today’s Asia-Pac session.

- Cash JGBs are dealing slightly mixed across the curve. The benchmark 10-year yield is 0.5bp lower at 0.610% versus the Nov-Dec rally low of 0.555%.

- Swap rates are richer across maturities, with rates 1-2bps lower. Swap spreads are tighter out to the 30-year and wider beyond.

- Next week sees a public holiday on Monday followed by Tokyo CPI on Tuesday.

AUSSIE BONDS: Cheaper, Waiting For Payrolls, CPI Monthly Next Wednesday

ACGBs (YM -5.0 & XM -6.0) remain cheaper after dealing in relatively tight ranges in today’s Sydney session. With the local calendar empty, local participants have held the negative overnight lead in from US tsys ahead of Non-Farm Payrolls later today.

- Bloomberg consensus sees nonfarm payrolls growth of 171k in December after November’s 199k was boosted by 38k workers returning from strikes. See MNI's NFP Preview here.

- Cash US tsys are dealing little changed in today’s Asia-Pac session after yesterday’s 5-8bps cheapening.

- Cash ACGBs are 5-6bps cheaper, with the AU-US 10-year yield differential 1bp tighter at +11bps.

- Swap rates are 6bps higher, with the 3s10s curve unchanged.

- The bills strip is cheaper, with pricing -2 to -7.

- RBA-dated OIS pricing is 3-6bps firmer for meetings beyond May.

- Following the Australian Government’s release of the Mid-Year Economic and Fiscal Outlook (MYEFO) in December 2023, the AOFM announced today that Treasury Bond issuance for 2023-24 is planned to be around $50 billion (of which $23.6 billion has been completed).

- Next week the local calendar heats up with the release of Retail Sales and Building Approvals on Tuesday, and Job Vacancies and November’s CPI Monthly on Wednesday.

NZGBS: Bear-Steepening To End The Week, US Payrolls Watch

NZGBs have bear-steepened into the close, with yields flat to 6bps higher. All benchmarks closed mid-range, with trading ranges relatively narrow in a data-light session. Local participants appear to have been content to take their directional lead from US tsys ahead of the release of US Non-Farm Payrolls data later today.

- Bloomberg consensus sees nonfarm payrolls growth of 171k in December after November’s 199k was boosted by 38k workers returning from strikes. See MNI's NFP Preview here.

- Cash US tsys are dealing little changed in today’s Asia-Pac session after yesterday’s 5-8bps cheapening.

- Swap rates are 5-8bps higher, with implied swap spreads wider.

- RBNZ dated OIS pricing is 2-9bps firmer across meetings beyond February. The cumulative easing by November 2024 has been scaled back to below 100bps (96bps).

- Next week, the local calendar is relatively light again, with House Prices, Commodity Prices and Building Permits as the highlights.

FOREX: Dollar Index +1% For The Week, As NFP Comes Into View

Dips in the USD have generally been supported in the part of Friday trade. The BBDXY sits near session highs in recent dealings, last just above 1225.85.

- At this stage the USD index is over 1% higher for the week, its best gain since July. Of course, we still have the US NFP report to navigate later. Recent highs in the index have run out of steam above 1226.

- USD/JPY is leading the move higher, threatening to test above 145.00 (last 1244.90/95). US Tsy futures remain close to Thursday lows, but haven't broken to the downside yet. Data on Dec PMI revisions hasn't moved sentiment.

- AUD and NZD are down by less at this stage. AUD/USD is near 0.6700 in latest dealings, which is close to Thursday lows. NZD/USD is just under 0.6230, also close to Thursday lows.

- Looking ahead, highlights will be Eurozone inflation figures and the US employment report. Additionally, German retail sales, UK construction PMI and Canada jobs data are all scheduled.

EQUITIES: Japan Shares Outperform, Volatile Start For HK/China Shares

Regional equities are mixed as the US NFP comes into view. Japan markets are among the best performers, while Hong Kong and China markets have been volatile through the first part of trade. US equity futures tried to go higher in the first part of trade, but there was no follow through. Eminis last tracked at 4734, +0.10%, while Nasdaq futures are around 0.06% higher.

- Japan indices are seeing broad based gains, the Topix +0.80% and the Nikkei 225 up by nearly the same. The yen trend remains weaker, while BBG noted sell-side analysts are reducing the likelihood of an end to negative rates.

- Hong Kong and China bourses opened lower before recovering sharply. At the break, the HSI is off -0.14% (we were down by 1% at the lows), while the CSI 300 is marginally firmer (+0.17%).

- BBG noted this morning the attractive valuation of local equities relative to local bond yields, so this may have helped at the margin. Data related stocks have risen in China after the government encouraged investment and IPOs in the sector (BBG).

- South Korea's Kospi is weaker but up from session lows, the index last -0.30%. Headlines crossed earlier that the South Korean military ordered the evacuation of the island of Yeonpyeong, which is near the broader with North Korea (RTRS).

- In SEA, outside of weaker Thailand stocks (-0.35%), markets are firmer.

OIL: Holding +1% Higher For The Week

Brent crude has tracked tight ranges for the first part of Friday trade. We were near $77.85/bbl for the front month contract, slightly above Thursday closing levels. At this stage, we are tracking higher for the week, with a gain of just over 1%. The WTI front month benchmark is also higher for the week (+1.3%) and last tracking at $72.60/bbl.

- Pressure came on Thursday from large US product builds, while strong non-OPEC production is also evident. This is outweighing support from a larger than expected draw in US crude stocks and continued disruption in the MENA region.

- Oil prices are not reacting much to Red Sea escalations and geopolitical tensions because fundamentals are softer for crude right now according to Energy Aspects Director Amrita Sen.

- Brent crude remains broadly within recent ranges, with lows year to date coming around $75//bbl, but hasn't been able to break back above $80/bbl on the topside. Still a gain this week is impressive for the week given the strong USD rebound.

GOLD: Heading For A Weekly Drop Ahead Of US Payrolls Data

Gold is slightly higher in the Asia-Pac session, after closing 0.1% higher at $2043.65 on Thursday.

- Bullion is poised for its first weekly drop in a month on increasing signs the Federal Reserve will be slower to start easing policy than was anticipated at the end of last year.

- On Thursday, US Treasuries continued their recent cheapening trend, fueled by a rethink of aggressive rate hike bets, stronger data, profit-taking, and supply.

- Cash US Treasuries finished 5-8bps cheaper, with the curve steeper, following higher-than-expected ADP Employment Change data (164k vs 125k est) and lower-than-expected Initial Jobless Claims (202k vs. 216k est). The market now awaits Non-Farm Payrolls data later today.

- According to MNI’s technicals team, moving average studies are still in a bull-mode position despite the weakness seen this week. Key support lies at $1973.2, the Dec 13 low.

ASIA FX: Won Weighed By South Korea/North Korea Tensions

USD/Asia pairs have tracked higher for the most part in Friday trade to date. USD/CNH probed above 7.1800, fresh highs back to Dec 13 but it didn't follow through. The won has been weighed down by fresh tensions between South Korea and North Korea. Thailand and Philippines CPIs were weaker than expected. The Taiwan Dec inflation report is due later.

- USD/CNH got a high of 7.1803 as HK and China equities opened up weaker. Sentiment quickly turned around though and we are away from lows for both indices, although positive impetus hasn't been that strong. USD/CNH last tracked near 7.1770.

- 1 month USD/KRW got to fresh highs near 1315 on headlines of shelling from North Korean and South Korea evacuating an island near the boarder with North Korea. There are no reports of casulities though. We sit back slightly lower now, last near 1313. Onshore equities are down 0.55% for the Kospi at this stage.

- USD/THB has continued to track higher, not too far highs for the week near 34.60. CPI was weaker than expected in terms of the headline, which should leave pressure on the BoT to shifts its policy bias in 2024. The baht is the second worst performer (behind KRW), for this past week, losing nearly 1.15%.

- USD/SGD has drawn selling intertest on moves above 1.3300 so far this week, the pair last around 1.3305, little changed versus end Thursday levels in NY. The 20-day EMA which comes in at 1.3293 may be acting as somewhat of a resistance point. A clean break above 1.3300 could see 1.3385/90 targeted, which is where the 50-day EMA comes in. Recent lows rest under 1.3160. Retail sales were close to expectations for Nov.

- USD/PHP has tracked higher, last near 55.75/80, around 0.50% weaker in PHP terms for the session. This may reflect some catch up for earlier outperformance from PHP this week. Dec CPI data was slightly weaker than expected, but it's unlikely to shift the BSP bias in the near term.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/01/2024 | 0700/0800 | ** |  | DE | Retail Sales |

| 05/01/2024 | 0830/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 05/01/2024 | 0930/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 05/01/2024 | 1000/1100 | *** | | EU | HICP (p) |

| 05/01/2024 | 1000/1100 | ** | | EU | PPI |

| 05/01/2024 | 1000/1100 | *** |  | IT | HICP (p) |

| 05/01/2024 | 1330/0830 | *** |  | CA | Labour Force Survey |

| 05/01/2024 | 1330/0830 | *** |  | US | Employment Report |

| 05/01/2024 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 05/01/2024 | 1500/1000 | *** | | US | ISM Non-Manufacturing Index |

| 05/01/2024 | 1500/1000 | * | | CA | Ivey PMI |

| 05/01/2024 | 1500/1000 | ** | | US | Factory New Orders |

| 05/01/2024 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 05/01/2024 | 1830/1330 | | US | Richmond Fed's Tom Barkin |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.