Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

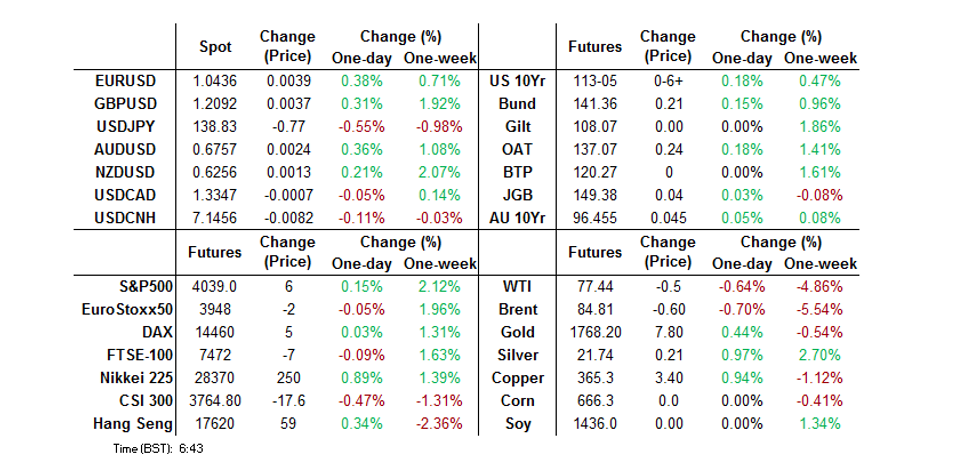

- Thanksgiving holiday-thinned Asia-Pac trade was dominated by regional reaction to Wednesday’s soft U.S. economic data (PMIs and jobless claims) and the FOMC meeting minutes, which pressured the USD.

- In terms of meaningful macro news flow, Asia-Pac hours saw another uptick in Chinese COVID cases, with the daily new case count exceeding the previous peak lodged earlier this year. More localised lockdowns were declared in the country.

- German IFO data, the accounts covering the latest ECB meeting and a range of ECB speakers headline on Thursday. We will also hear from several BoE speakers and receive the latest monetary policy decision from the Riksbank. A reminder that the U.S. observes a public holiday today.

US TSYS: Futures Twist Steepen A Touch In Holiday-Thinned Trade

The Tsy futures curve twist steepened a touch overnight, with the Asia-Pac reaction to the slightly dovish feel to the minutes covering the latest FOMC decision, and to a lesser degree soft U.S. PMI & jobless claims data, allowing that dynamic to unfold.

- Contracts out to UXY remain underpinned, while WN & US futures are softer on the day. TYZ2 deals +0-04+ at 113-03, operating in a narrow 0-05+ range on sub-standard volume of ~45K

- A reminder that futures will be subjected to curtailed trading hours and thinner liquidity on Thursday owing to the observance of the Thanksgiving holiday, while cash Tsys are closed until Friday’s Asia-Pac session.

- In terms of meaningful macro news flow, Asia-Pac hours saw another uptick in Chinese COVID cases, with the daily new case count exceeding the previous peak lodged earlier this year. More localised lockdowns were declared in the country.

- ECB speak headlines Thursday’s global docket.

JGBS: A Touch Firmer After Holiday

A modest bid crept into the JGB space as Tokyo participants played catch up after their mid-week holiday, leaving the major benchmarks 0.5-1.5bp richer across the curve, while JGB futures nudged higher, operating in a contained range to finish +5. The supportive global factors that we have outlined elsewhere aided the early bid.

- Local headline flow saw PM Kishida push back against the recent speculation surrounding the potential for a fairly imminent cabinet reshuffle.

- A softer round of PMI surveys was also observed, with the survey collators writing “activity at Japanese private sector firms declined for the first time in three months, according to November flash PMI data. Central to the latest downturn was a poor performance at Japanese manufacturing firms.”

- Looking ahead, Friday’s local docket is headlined by Tokyo CPI and services PPI data

AUSSIE BONDS: Firmer & Flatter On Global Inputs

The impulse from a firmer core global FI complex, linked to soft U.S. data, a dovish feel to the minutes covering the latest FOMC decision, the prospect of further monetary easing in China and firm demand at the latest round of longer dated NZGB auctions fed into demand for ACGBs, allowing the space to firm on Thursday.

- That left YM +3.0 & XM +4.5 at the bell, with wider cash ACGB trade seeing 2-6bp of richening as the curve bull flattened.

- Bills were flat to 3bp richer through the reds come the close, erasing early losses to bull flatten at the margin.

- We didn’t get much in the way of headline flow to facilitate idiosyncratic moves, with the local data docket and speaker schedule somewhat empty.

- Looking ahead, Friday will bring the release of the weekly AOFM issuance slate and A$700mn of ACGB Apr-25 supply.

NZGBS: Auction Dynamics Promote Flattening

The broader bid in core global FI markets observed during Asia-Pac hours generally facilitated an extension of the early bid in NZGBs.

- This, coupled with a solid round of demand at the latest NZGB May-32 & Apr-37 auctions, as each line saw 1 successful bidder, who paid up for access to the lines (note the NZGB Apr-25 leg of the auctions was only covered 1.00x and saw an ~11bp wide spread of accepted yields, probably on the back of some RBNZ-related caution, which weighed on the shorter end of the curve), promoted curve flattening, with the major NZGB benchmarks finishing flat to 9bp richer.

- Swap spreads were tighter in the front end to little changed further out, with the 2-/10-Year swap differential pulling further into inverted territory.

- RBNZ dated OIS price just over 70bp of tightening for the RBNZ’s next meeting (which will be held in Feb ’23), with a terminal OCR of just over 5.45% eyed (compared to the 5.50% peak seen in the Bank’s latest OCR track projection).

- Post-meeting parliamentary testimony from RBNZ Governor Orr & chief economist Conway mimicked the post-meeting statement’s focus on inflation, with Orr highlighting that the OCR is now in contractionary territory.

- Looking ahead Q3 retail sales volume data and the monthly ANZ consumer confidence survey headline the domestic docket on Friday.

FOREX: Dollar Under Pressure In Wake Of FOMC Minutes & U.S. Data

Thanksgiving holiday-thinned Asia-Pac trade was dominated by regional reaction to Wednesday’s soft U.S. economic data (PMIs and jobless claims) and the FOMC meeting minutes, which pressured the USD.

- We saw another uptick in COVID cases in China, with new daily case numbers in the country now through their previous ’22 peak.

- The JPY leads the G10 FX pack, with Tokyo returning from a mid-week holiday.

- Elsewhere, RBNZ Governor Orr & chief economist Conway reiterated the Bank’s focus on getting inflation under control in an early parliamentary address.

- We also saw the BoK deliver the widely expected 25bp rate hike, although the Bank signalled the likelihood that the tightening cycle will draw to an end in the early part of ’23, while indicating the board’s range of preferences re: the terminal rate (from no more tightening to 50bp of additional hikes).

- USD/CNH operates within the confines of Wednesday’s range, with no bias observed in today’s USD/CNY mid-point fixing, as markets looked through the latest round of COVID lockdowns in China and leant on both realised and expected support for the Chinese economy, which supported the yuan at the margin.

- Asia FX played catch up to the USD weakness witnessed since yesterday’s local market closes, with the respective moves extending throughout the day.

- German IFO data, the accounts covering the latest ECB meeting and a range of ECB speakers headline on Thursday. We will also hear from several BoE speakers and receive the latest monetary policy decision from the Riksbank. A reminder that the U.S. observes a public holiday today.

FOREX OPTIONS: Expiries for Nov24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0035(E598mln), $1.0100-10(E1.3bln), $1.0345-50(E571mln), $1.0380-00(E1.1bln)

- USD/JPY: Y138.00($816mln), Y140.30($765mln), Y141.15($600mln), Y150.00($1.4bln)

- AUD/USD: $0.6585-00(A$798mln)

- USD/CNY: Cny7.1500($1.1bln)

MNI Riksbank Preview - November 2022: Upside risks to 75bp

EXECUTIVE SUMMARY

- The MNI Markets team expects that higher CPIF ex energy than the Riksbank expected and a larger ECB hike will push the Riksbank to hike 75bp this week (more than its forward guidance of 50bp would have suggested).

- The MNI Markets team thinks that although a 100bp hike cannot be ruled out (and the risks are more in favour of a 100bp hike than 50bp hike in our view) that concerns about the housing market and an impending recession will be enough to stop the Riksbank from delivering such a large rate hike again.

- For the full MNI Riksbank Preview including summaries of 10 sellside previews see:MNI Riksbank Preview - 2022-11.pdf

MNI CBRT Preview - November 2022: Another 150bp Cut in Sight

EXECUTIVE SMMARY

- The CBRT is largely expected to cut rates again by 150bp this month, leaving the one-week repo rate at 9.00%.

- This is in line with President Erdoğan’s calls for single-digit rates by year-end as the bank remains highly politically influenced and willing to look through inflation in excess of 85%.

- In October the CBRT delivered a larger-than-expected 150bp rate cut, the third consecutive cut in the cycle.

- The CBRT sees the accommodative financing conditions remaining of paramount importance as the economy loses further momentum. The October policy statement has laid the path for the final cut, disclosing that the CBRT “evaluated taking a similar step in the following meeting and ending the rate cut cycle”.

- Full piece here: MNICBRTPrevNov22.pdf

MNI SARB Preview - November 2022: Hike to Neutral Looks Likely

EXECUTIVE SUMMARY

- The South African Reserve Bank are likely to tighten policy further at this meeting, but the pace of this quarter’s increase remains up for question

- Markets are fully priced for a 50bps move this week and are approximately 50% priced for a 75bps step

- A sizeable minority voting for smaller hikes could indicate that the front-loading phase of the cycle has now ended

- Full preview including summary of sell-side views here: MNISARBPrevNov22.pdf

EQUITIES: Mostly Higher On FOMC Mins, Although Chinese Indices Give Back Early Gains

The slightly dovish feel to the minutes covering the latest FOMC meeting, coupled with a softer USD, as well as realised and swirling expectations for further Chinese policy support, allowed the majority of the major Asia-Pac equity indices to tick higher on Thursday.

- The Nikkei 225 outperformed its regional peers after the mid-week Japanese holiday, adding just over 1.00% as we head into the close, although a firmer JPY likely capped the strength in Japanese equities.

- The CSI 300 gave back its modest, early gains with a fresh round of localised COVID restrictions in China weighing. Still, the property sector outperformed on signs of the latest step up in policy support for the sector.

- E-minis nudged ~0.2% higher against this backdrop.

GOLD: Gold Prices Higher As USD Softens On December Fed Pivot

The gold price responded positively to the weaker USD in response to the signal from the FOMC minutes that there is likely to be a smaller rate hike in December. Bullion closed the NY session at just under $1750/oz but spot has moved 0.35% from there today to trade around $1755, as DXY as fallen another 0.35%.

- Gold has struggled this year as the Fed implemented aggressive monetary tightening. Signs that it may be slowing are good for bullion. But prices are still some way off the bull trigger of $1786.50, the November 15 high.

- The US is closed for Thanksgiving and so trading is likely to be light tonight. But there is the German IFO in Europe and the ECB meeting accounts plus a number of ECB speakers.

OIL: Prices Range Trading After Overnight Correction

Oil prices have been in a tight range today around the NY close of $77.94/bbl for WTI and $85.41 for Brent. Prices fell sharply overnight on continued Chinese demand concerns and discussions that the EU will implement a softer Russian oil price cap. WTI is now well below its 50-day MA.

- WTI has been trading between $77.30 and $78.00 today and Brent between $85 and $85.31.

- It looks like the EU will introduce an oil price cap on Russian shipments of $65-$70 rather than the originally proposed $40-$60. This would reduce the risks of severe retaliation from Russia. A higher cap is also likely to keep crude prices lower overall, given Russia’s influence it would allow more of its output onto the global market. Goldman Sachs doesn’t think that the cap at this level will be effective in hurting Russia and only the current oil embargo will impact its supply.

- The EIA reported a 3.69mn barrel drawdown in crude inventories in the US after -5.4mn last week. However, there was a much needed build in distillate and gasoline stocks of 1.72mn and 3.06mn respectively.

- The US is closed for Thanksgiving. But there is the German IFO in Europe and the ECB meeting accounts plus a number of ECB speakers.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/11/2022 | 0745/0845 | ** |  | FR | Manufacturing Sentiment |

| 24/11/2022 | 0830/0930 | ** |  | SE | Riksbank Interest Rate |

| 24/11/2022 | 0900/1000 | *** |  | DE | IFO Business Climate Index |

| 24/11/2022 | 0945/0945 |  | UK | BOE Ramsden Speech at BOE Watchers’ Conference | |

| 24/11/2022 | 1030/1030 | | UK | BOE Pill Panelist at BOE Watchers’ Conference | |

| 24/11/2022 | 1100/0600 | * |  | TR | Turkey Benchmark Rate |

| 24/11/2022 | 1115/1215 |  | EU | ECB de Guindos Speech at Analysis Forum in Milan | |

| 24/11/2022 | - |  | SK | South Korea BoK Rate Decision | |

| 24/11/2022 | - |  | ZA | SARB Rate Decision | |

| 24/11/2022 | 1300/1400 | | EU | ECB Schnabel Speech at BOE Watchers' Conference | |

| 24/11/2022 | 1330/0830 | * |  | CA | Payroll employment |

| 24/11/2022 | 1345/1345 | | UK | BOE Mann Panelist at BOE Watchers’ Conference | |

| 24/11/2022 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 25/11/2022 | 2330/0830 |  | JP | Tokyo Nov CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.