Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- This week has started off in a similar fashion to how last week ended. The USD has continued to recover amid support from better US data outcomes and improvement in yield momentum against the G3. The BBDXY is back around 140.00, but remains below post payroll highs from early last week. Some nervousness ahead of tomorrow's US CPI print could also be a driver of sentiment. USD/JPY is the standout performer today, nearly 2% higher versus Friday's lows, last around 132.25/30. Tomorrow the focus will be on the new BoJ Governor, who will be presented to parliament.

- US-China tensions continue amid on-going balloon and other air related incidents. This has weighed on equity sentiment, although less so for China stock indices today. USD/CNH is at multi week highs, which coupled with yen weakness has weighed on Asia FX.

- RBA Governor Lowe will be under fresh scrutiny at this Wednesday's Senate hearing in Australia, amid local media reports of Australian fixed income reacting post a Lowe private briefing from late last week. The 3 yr AU bond touched a high of 3.55%, but we are now back to 3.47%.

- Looking ahead, there is a thin data calendar today. ECB speak from Lagarde and Panetta as well as Fedpseak from Gov Bowman provide the highlights of the day. Further out the focus is on Tuesday's US Jan CPI data.

MARKETS

US TSYS: Little Changed In Asia

TYH3 deals at 112-22+, +0-00+, in the middle of its 0-05+ range on volume of ~85k.

- Cash tsys sit flat to 1bp cheaper across the major benchmarks.

- TYH3 briefly looked through Friday's session lows in early trade however there was little follow through.

- ACGBs recovering from session lows provided support.

- There was little macro headline flow.

- There is a thin data calendar today. ECB speak from Lagarde and Panetta as well as Fedpseak from Gov Bowman provide the highlights of the day. Further out the focus is on Tuesday's US CPI data for Jan.

FOREX: JPY Pressured In Asia, Greenback Firmer

JPY has been pressured in today's Asia-Pac session, Yen is currently the weakest performer in G-10 space at the margins.

- USD/JPY prints at ¥132.10/20, ~0.6% firmer in today's trading. The pair looks to be playing catch up with the more supportive yield environment for the USD as US-JP 10 year swap spread has widened in recent dealing.

- AUD/USD prints at $0.6906, ~0.1% softer today. The pair has dealt in a narrow $0.6890/30 range for the majority of the session with support seen below $0.69. Pressure from lower Copper and Iron Ore has weighed on the Aussie.

- Kiwi is little changed from today's opening levels at $0.6300/05. NZD/USD has observed narrow ranges with dips below $0.63 supported and resistance seen above $0.6320.

- CAD and NOK are both ~0.3% softer; facing pressure from weaker Oil prices, WTI is down ~1%.

- EUR and GBP are both ~0.1% lower.

- Cross asset wise, e-minis are down ~0.4% and BBDXY is ~0.3% firmer. US Treasury Yields are little changed, although the front end 2yr yield is +1bps to 4.53%.

- There is a thin data calendar today. ECB speak from Lagarde and Panetta as well as Fedpseak from Gov Bowman provides the highlight of the day.

EQUITIES: Cautious Tone (ex China) Ahead Of Key Event Risks

Regional markets have been under pressure to start the week, although China markets have bucked the broader trend, tracking higher in the first part of trade. US futures are mostly lower, with eminis off -0.37%, Nasdaq futures -0.43% at this stage.

- Familiar themes are dominating sentiment, with fears over a stronger for longer US theme ahead of tomorrow's CPI print weighing. US-China relations are the other concern, as on-going balloon and other related air incidents risk raising tensions. Fresh US curbs on tech related exports to China is a potential action from the US side.

- The China Dragon Index fell sharply in Friday trade (-3.66%), while the HSI is off by around 0.4% so far today. The tech sub index was down over 2% in early trade, but has largely pared these losses.

- China mainland stocks are firmer though, +0.70% for the CSI 300 so far today. Tensions with the US haven't weighed materially, while property developer Vanke plans to raise 15bn yuan in a private placement, the biggest since regulators lifted restrictions on the sector last year.

- The Kospi and Taiex are both weaker, in line with tech weakness from Friday's session and further Nasdaq futures losses today. The Nikkei 225 is also off by 1% at this stage, even as JPY has been the weakest performer in the 10 space. The new BoJ Governor is expected to be presented to parliament tomorrow.

- Outside of Indonesian stocks, SEA bourses and Indian shares are tracking weaker so far today.

OIL: Profit Taking And Growth Fears Weigh On Crude Today

Oil prices have been trending down during the APAC session and are now trading close to their intraday lows. On Friday WTI rose 2.2% and Brent 2.4% after Russia announced it would cut output in response to sanctions but today global growth concerns have come to the surface again. Profit taking is adding to this move with WTI down 1% to around $78.95/bbl and Brent is down 0.9% to $85.60, close to intraday lows.

- WTI reached a high of $80 today followed by a low $78.86. Initial resistance is at $80.33 but $83.14 is key. Brent hit a high of $86.64 today followed by a low of $85.46. $86.90 is initial resistance and $89 is the bull trigger. Brent is just above the 100-day simple moving average, whereas WTI is just below.

- After Russia announced it would cut its output by 500kbd in March, OPEC+ suggested that it wouldn’t increase its production to make up the shortfall.

- Later the focus is likely to be on Fed Governor Bowman ahead of US CPI on Tuesday, as data is scarce. US January CPI data is expected to show a further moderation in inflation. Concerns that tightening has a lot further to go in the US continue to make markets nervous.

- Also both OPEC and the International Energy Agency will publish their monthly reports on Tuesday and Wednesday respectively.

GOLD: Bullion Down As Markets Wait For Tuesday’s US CPI Data

Gold prices have been moving sideways for most of February, as signs grow that Fed rates may peak higher than previously expected. They rose 0.2% on Friday and are now down 0.4% to $1858.80/oz, just above the 50-day simple moving average. During the APAC session they reached a high of $1864.05 followed by a low of $1858.19. The US dollar is up slightly.

- On Friday bullion broke through support of $1855.50 briefly. Trend conditions remain bearish and gold is in a corrective cycle for now.

- Later the focus is likely to be on Fed Governor Bowman ahead of US CPI on Tuesday, as data is scarce. The market is waiting for US January CPI data, which is expected to show a further moderation in inflation.

RBA: Model Indicates That Growth & Inflation Imply Hikes Needed Through 2023

We have updated our policy reaction function for the RBA with its latest forecasts provided on Friday. With the near-term upward revision to inflation and 2023 GDP expectations our equation now says that the economic fundamentals imply that rates should be 5bp higher by mid-year at around 4.18% and end-year around 5%.

- The equation has been extended to end 2023 and says that rates should continue to rise over H2 given the economic outlook. The model is forward looking as the inflation variable leads by two quarters. It estimates that the Q1 2023 cash rate should be 50bp higher than Q4, and Q2 and Q3 up another 50bp each meaning it is more hawkish than OIS market pricing, but its starting point is higher than the actual cash rate.

- When we take house prices into account, the rate path is lower with Q2 40bp below the model above and Q4 90bp. It is also below OIS market pricing in Q2 but in line for year end and closer than the equation without housing.

- It is worth noting that these are just estimates from a simple equation and like with all econometric analysis, estimates are not predictions.

Source: MNI - Market News/Refinitiv

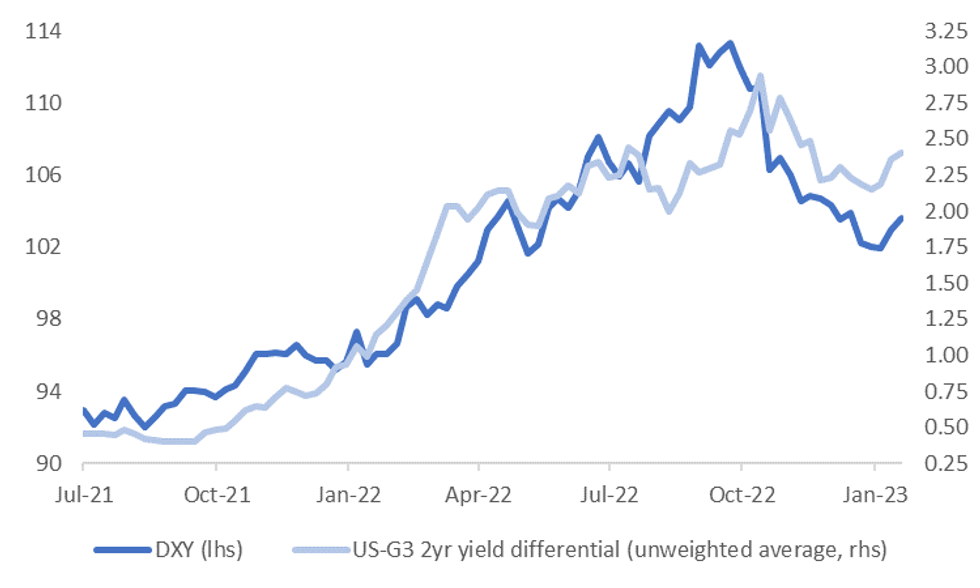

US Data Momentum Recovers Ground Against Other Major Economies

The USD has started the week positively. The BBDXY is up close to 0.20%, last around the 1239.50 level. Earlier highs were above 1240, while last week we ran out of steam around the 1243.50 region in the aftermath of the payrolls print.

- Focus rests with the CPI print tomorrow in the US, although the general trend in yield momentum still remains in favor of the USD. The first chart below plots the US-G3 2yr spread government bond yield spread (unweighted). The spread is back to around +240bps, we were close to +215bps in mid Jan.

Fig 1: USD Index Following Yield Spread Momentum Higher

Source: MNI - Market News/Bloomberg

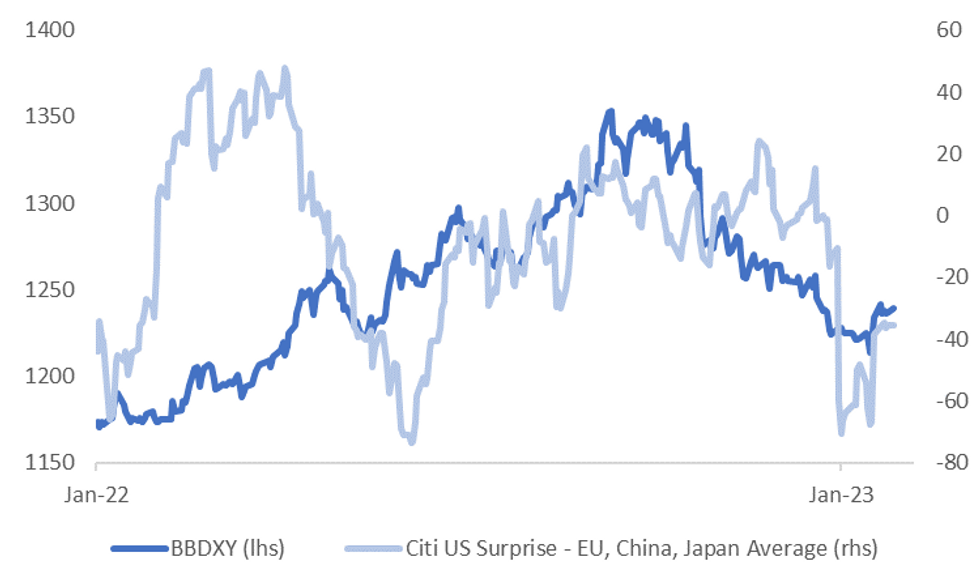

- The skew of data surprises, as measured by the Citi indices, has swung back in the USD's favor as well, see the second chart below. Earlier in the year we were around cyclical lows in terms of US data surprises relative to other major economies. We have since recovered some ground, although on average, the US data surprise index is still below that of other major economies/regions.

- Interestingly, the Citi US index is now back at 24, close to fresh highs going back to May of last year.

- We may need to see continued US data relative outperformance to see a further recovery in USD indices.

Fig 2: USD & Relative Data Surprises Against Other Major Economies/Regions

Source: Citi/MNI - Market News/Bloomberg

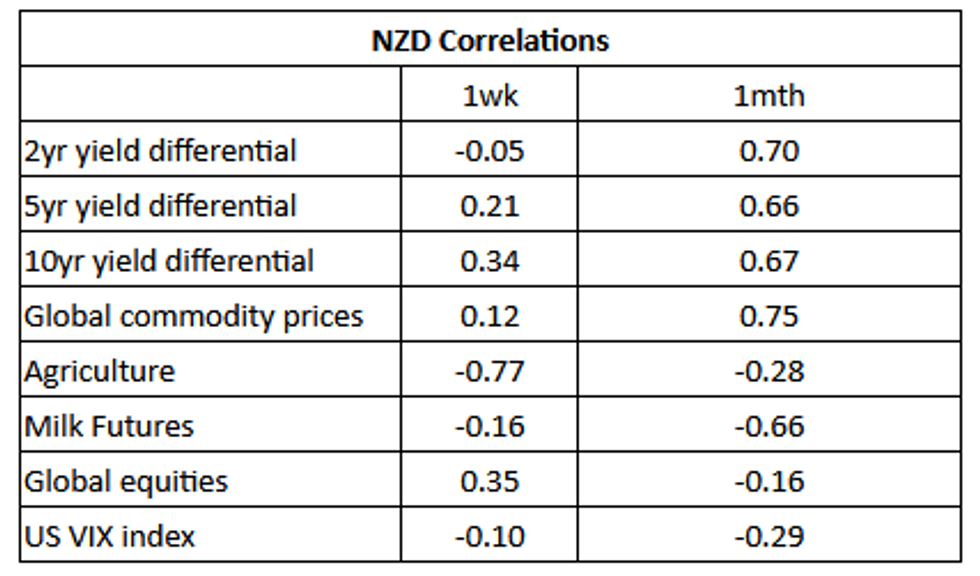

No Standout Macro Driver Last Week; Rate Differentials, Commodities Longer Term Drivers

NZD/USD consolidated last week, the pair finished last week ~0.4% softer from last Monday's opening levels, dealing in a narrow ~2% range over the week. The table below presents levels of correlations between NZD and key macro drivers (note the yield differential reflects swap rates).

- There was no dominant macro driver however 10 year yield differentials and Global equities both provided some direction.

- Kiwi looked through strength in Agriculture prices, which didn't appear to provide much support to the NZD.

- Over the longer time frame 2,5 and 10 year rate differentials and Global Commodity prices provide the main drivers of the NZD.

Source: Market News International (MNI)/Bloomberg

UP TODAY (TIMES GMT/LOCAL

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/02/2023 | 0730/0830 | *** |  | CH | CPI |

| 13/02/2023 | - |  | EU | ECB Lagarde & Panetta at Eurogroup Meeting | |

| 13/02/2023 | 1300/0800 |  | US | Fed Governor Michelle Bowman | |

| 13/02/2023 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 13/02/2023 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.