Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

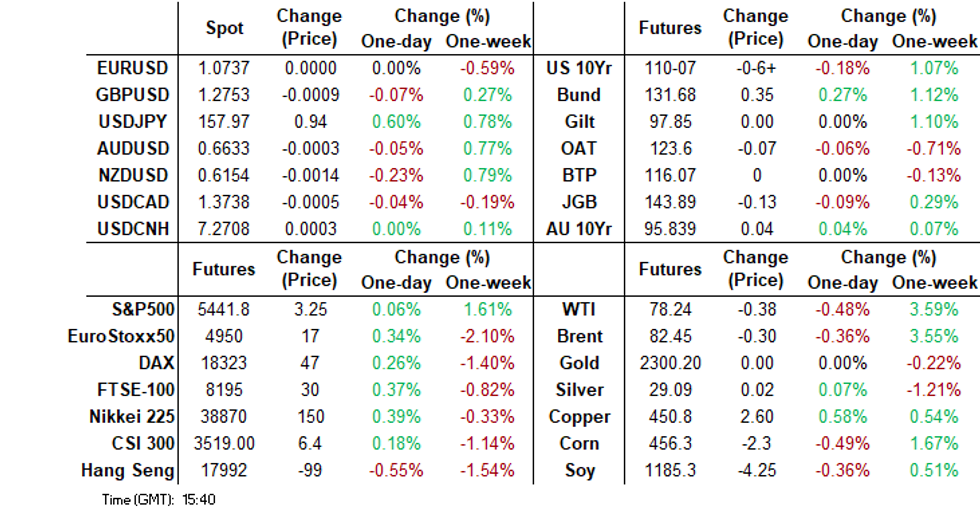

- The BoJ kept rates on hold as expected and announced plans to trim bond buying, but details won't be announced until the July policy meeting.

- Markets were left disappointed by the lack of detail. USD/JPY has rallied back close to 158.00, fresh highs since early May. In post-BoJ Decision dealings, JGB futures are higher at 143.95, +49 compared to the settlement levels, but well below the session high (JBU4 at 144.26) set early in the afternoon session following today’s BoJ Policy Decision.

- US Treasury futures have continued to grind lower all throughout the day and we now trade at session's worst levels. The USD is mostly higher. NZD/USD was weighed down by softer monthly inflation details. IDR fell back to fresh 202 lows on government debt plans.

- Looking ahead, the preliminary read of UMich sentiment and inflation expectations data are on tap. Fed speak also resumes.

MARKETS

US TSYS: Tsys Futures Edge Lower, Volumes Increase, Fed Blackout Ends

Treasury futures have continued to grind lower all throughout the day and we now trade at session's worst levels. TUU4 is -0-02⅝ at 102-06¾, while TYU4 is -0-07+ at 110-15+, later today we have Cleveland Fed President Loretta Mester and Chicago Fed President Austan Goolsbee speaking.

- Volumes are much higher than prior days: TU 125k, FV 208k, TY177k

- Tsys Flows: There were 2 large Block TU-FV-UXY fly, Seller belly, DV01 $1.27m, and Block likely Seller 1,500 FVU4 at 106-27 ¾.

- Cash treasury yields are 2-4bps higher, with the 2Y +2.7bp to 4.723%, 7Y +2.5bps at 4.260%, while the 10Y is +2.3bps at 4.267%.

- APAC rates: ACGB & NZGB yields are 4-5.5bps lower, focus in the region has been on the BoJ where they kept rate on hold, JGB yields are 1-5bps lower, curve bull-flattening.

- Barclays are shorting the 10-year US Treasury bond with an entry at 4.24%, anticipating a rebound in US economic activity and higher rates. They also shifted to a neutral stance after profiting from the yield difference between 5- and 30-year Treasury bonds, having seen significant steepening, per bbg.

- (MNI) June 2024 Fed Review Analyst Views: (See https://marketnews.com/june-2024-fed-review-analys...)

- Short end support sees rate cut projections near pre-FOMC levels (*): July'24 at -12% (-14%) w/ cumulative at -3bp (-3.8bp) at 5.298%, Sep'24 cumulative -20bp (-20.9bp), Nov'24 cumulative -29.3bp (-31.7bp), Dec'24 -50.4bp (-50.7bp).

- Looking ahead, Fed Out of Blackout, Import/Exp Prices and UofM inflation expectations.

JGBS: Richer After The BoJ Policy Decision But Initial Gains Have Been Pared

In post-BoJ Decision dealings, JGB futures are higher at 143.95, +49 compared to the settlement levels, but well below the session high (JBU4 at 144.26) set early in the afternoon session following today’s BoJ Policy Decision.

- The BoJ kept its benchmark interest rate unchanged, maintaining it in a range between 0 to 0.1%, in a unanimous vote. The bank also announced plans to reduce the amount of its bond purchases and will specify the details at the next policy meeting. It will decide on JGB purchase amounts for the next 1-2 years

- (MNI) The BoJ board largely maintained its assessment of the overall economy and major economic components, including the assessment of inflation expectations. “Underlying CPI inflation is expected to increase gradually since it is projected that the output gap will improve and that medium- to long-term inflation expectations will rise with a virtuous cycle between wages and prices continuing to intensify." (See link)

- The cash JGB curve has extended its bull-flattening in post-decision dealings, with yields 1-6bps lower. The benchmark 10-year yield is 4.6bps lower at 0.929% versus the cycle high of 1.101%.

- Swaps are richer across maturities, with rates 2-5bps lower. Swap spreads are mostly wider.

- On Monday, the local calendar will see Core Machine Orders, ahead of BoJ Rinban Operations covering 1-25-year JGBs on Tuesday.

BOJ: Unchanged, Bond Buying Plan To Be Announced In July

The BoJ kept interest rates unchanged as widely expected, with the lower bound remaining at 0.0%, the upper bound at 0.10%. The central bank did announce it would trim JGB bond purchases, which was also what the consensus broadly expected.

- The central bank will specify reductions in its bond buying program at the July meeting though. It will outline its plans for the next 1-2 years at that meeting. In the interim bond buying will continue as per the guidelines from the March meeting.

- The central bank will also meet with various key stake holders in terms of the bond market plan, including banks and securities firms.

- Dovish board member Nakamura dissented the JGB decision, saying such a decision should have been made at the July policy meeting.

- On the rate decision, it was unanimous 9-0 outcome from the board members.

- Elsewhere the central bank noted that financial conditions have remained accommodative. It expects inflation to be around the 2% target in the latter half of the forecast period.

- Financial market developments need to be watched, particularly FX markets.

- The delay in the JGB tapering plan is the main takeaway from today's meeting, although BoJ watchers may have been looking for something more concrete to be announced today. USD/JPY has pushed higher, last near 157.85/90, while JGB futures have also gaped higher post the lunchtime break.

AUSSIE BONDS: Richer, Narrow Ranges, RBA On Hold Next Tuesday

In today's Sydney session, ACGBs (YMU4 +5.0 & XMU4 +3.9) hold richer after dealing in relatively narrow ranges. With the domestic calendar light, any extension of overnight gains has been held back by today’s 1-2bps cheapening in cash US tsys in today’s Asia-Pac session.

- Cash ACGBs are 4-5bps richer, with the AU-US 10-year yield differential at -11bps.

- Swap rates are 4-5bps lower.

- The bills strip has bull-flattened, with +2 to +7.

- On Monday, the local calendar will see ANZ-Indeed Job Advertisements, ahead of the RBA Policy Decision on Tuesday.

- (Dow Jones) “The Reserve Bank of Australia will take another cautious step into the unknown at its June policy meeting next week, deliberating on a mixed economic picture of growth barely registering a pulse against a backdrop of still-stubborn inflation risks.” (See link)

- According to all economists polled by Reuters, the RBA will hold its key policy rate for a fifth straight meeting on Tuesday due to" persistent price pressures". A majority, however, "expected the first cut to come in the last quarter of the year".

- RBA-dated OIS pricing is 3-6bps softer for 2025 meetings. A cumulative 12bps of easing is priced by year-end.

NZGBS: Richer, Tracking US Tsys

NZGBs closed 5-6bps richer. Outside of the previously outlined NZ’s manufacturing PMI and Food Price data, there hasn't been much in the way of domestic drivers to flag.

- With the NZ-US and NZ-AU 10-year yield differentials little changed on the day, today’s movements appear driven by global bond developments rather than domestic factors.

- Indeed, the shift away from the session's best levels can be attributed to a 1-2bp cheapening of US tsys during today's Asia-Pac session.

- Swap rates are 6-8bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing is 5bps softer for 2025 meetings. A cumulative 31bps of easing is priced by year-end.

- Next Monday, the local calendar will see REINZ House Sales data and Performance Services Index.

- In Australia, the RBA Policy Decision is due on Tuesday. “Money markets are now comfortable with the idea that the RBA will delay cutting interest rates from the current 4.35% until well into 2025, with RBA Gov. Michele Bullock expected to confirm once again on Tuesday that the central bank's board took time to debate a further interest-rate increase.” (per DJ)

FOREX: Yen Weakens Through Late May Levels, BoJ Disappoints With Lack Of Detail On JGB Purchase Plans

The yen has weakened post the BoJ meeting outcome. The central bank stated it would curb its bond buying program but details wouldn't be announced until the July policy meeting. As expected, policy rates were left unchanged.

- USD/JPY rallied from under the 157.20 region to session highs of 157.98 post the BOJ outcome. We last track slightly lower, near 157.85, still 0.50% weaker in yen terms for the session.

- Disappointment around lack on details on the tapering of bond buys has fueled bearish yen sentiment.

- USD/JPY has breached late May highs and key resistance at the 157.71 level. Hence intervention risks may be more heightened if we see further gains in the pair over the next few sessions. A break above 158.00 opens up a retest of earlier highs above 160.00 from a technical standpoint.

- Elsewhere, the USD is mostly firmer, although is steady near 1.0740. NZD/USD has fallen back to 0.6150, with earlier data showing monthly inflation pressures had cooled. Westpac has revised down its Q2 inflation forecast as a result.

- AUD/USD is off slightly, last near 0.6630.

- The BBDXY is now up to 1265.4, slightly up for the session. US yields have regained some ground, up 1-2bps, led by the front end of the curve.

- Looking ahead, the preliminary read of UMich sentiment and inflation expectations data are on tap.

ASIA STOCKS: HK & China Equities Mostly Lower, Property Higher On Rate Cut Hopes

Hong Kong and China equities are mixed today as investors await key economic data due out on Monday for China. Property names rally on and erased most of the weeks losses on Rate Cut hopes. It has been a very quiet week for the region in terms of economic data and market moving headlines, major indices have sold off between 1-5% over the same period as investors concerns grow on the lack of market supporting policy updates.

- Hong Kong equities are mixed today, with the HSTech Index down 0.91%, real estate indices are trading better with the Mainland Property Index up 2.40%, while the HS Property Index is 0.83% higher, the wider HSI down 0.65%.

- China onshore equities are mostly lower today, small-cap indices are between 0.30-0.70% lower, while the CSI300 Real Estate Index is up 2.58%, the wider CSI 300 Index is down 0.40%.

- (MNI) MNI China Press Digest June 14: Sino-EU, Forex, Exports - (See link)

- Today, Hong Kong PPI & Industrial Production for 1Q is expected at 1830 AEST.

ASIA PAC STOCKS: Asian Equities Mixed As BoJ Holds Rates Steady, SK Short Selling Ban

Asian markets are mixed today, Japanese equities rose on a weaker yen after the Bank of Japan maintained its monetary policy, South Korean equities are higher after authorities decided to extend the ban on short selling. Overall, the MSCI Asia Index fell, with Alibaba and TSMC among the biggest drags, as traders assessed the potential for Federal Reserve rate cuts amid rising US jobless claims.

- Japanese stocks rose as a weaker yen supported exporters following the Bank of Japan's decision to delay reducing bond buying and maintain its benchmark interest rate. The Nikkei 225 is up 0.46%, while the Topix is 0.53%, banks stocks are the worst performing with the Topix Bank Index down 0.93%.

- South Korean equities are mixed today Kospi is 0.30% higher while the small cap index the Kosdaq is down 1%. Earlier, Import price index rose to 4.6 y/y from 2.9% with the Export price index also rising to 7.5% y/y from 6.2%. On Thursday, government officials announced that the short selling ban will remain until proper systems are ready, and that the tax incentive plan for the corporate "Value-Up" program will be prepared shortly. The broader market sentiment remained cautious due to potential impacts from international economic trends.

- Taiwan equities are higher today, led higher by tech names with the Philadelphia SE Semiconductor Index trading up another 1.48% overnight. Late on Thursday, the central bank kept interest rates on hold at 2%. The Taiex is currently trading 0.40% higher.

- Australian shares opened lower, following a weaker performance in global markets. The downturn was influenced by concerns over US economic data and its potential impact on local exporters and market dynamics. The ASX200 is 0.32% lower.

- Elsewhere, New Zealand equities are down 0.11%, earlier food prices fell 0.2% m/m from 0.6% in April and the lowest annual increase in almost six years. Singapore equities fell 0.28%, Malaysian equities are down 0.16%, Philippines equities are down 0.19%, Indonesian equities are lower on the back of President Elect announcing plans to increase the debt-to-gdp ratio to about 50% over the coming years.

Asian Equity Flows Turn Positive In the Short-Term

- South Korean equities were higher on Thursday (Kospi up 0.98%, Kosdaq up 0.08%), and both up 1% for the past 5 sessions. We saw a 1.25b inflow on Thursday the largest since March 21, with the past 5 session now netting a total inflow of $1.65b. The 5-day average is $331m, above both the 20 day average of $21mm and the longer-term 100-day average at $138m.

- Taiwan equities rose on Thursday, up 1.19% with a $1.2b inflow, and gaining 2.8% over the past five trading sessions. We had another strong inflow of $1.2b on Thursday, with the past 5 session's seeing a total inflow of $1.15b with the 5-day average now $231m, above both the 20-day average at $32m, while the 100-day average is just $32m.

- Thailand equities were slightly lower on Thursday, down 0.37% and off 1.84% for the past 5 sessions. Foreign investors continue to sell equities as we now have marked the 16 straight session of selling for a total outflow of $859m with $249m of that coming in the past 5 sessions. The 5-day average is now -$50m, below both the 20-day average at -$40m and the 100-day average at -$25m.

- Indonesian equities were lower on Thursday, down 0.27%, and off 2.88% for the past 5 sessions. We broke a run of 15 straight sessions of selling from foreign investors, with a large $182m inflows on Thursday which more than covered the prior 5 sessions of outflows. The 5-day average is now $9m, above both the 20-day average at -$17m and the 100-day average at -$4m.

- Indian equities were higher on Thursday, up 0.33%, and now 1.62% higher for the past 5 sessions. Foreign investors have been purchasing local stocks since the election results were counted with the past 5 sessions netting a inflow of $262m. The 5-day average is now $52m above both the 20-day average at -$51m, and the 100-day average at $11m

- Malaysian equities were slightly higher on Thursday, up 0.08% although 1.38% lower for the past 5 sessions. Foreign investors have been slightly better buyers recently, with the past 5 sessions seeing an inflow of $88m. the 5-day average is now $17m, above both the 20-day average at $7m and the 100-day average at -$1m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | 1256 | 1656 | 15590 |

| Taiwan (USDmn) | 1224 | 1157 | 3284 |

| India (USDmn)* | 81 | 262 | -3717 |

| Indonesia (USDmn) | 183 | 183 | -379 |

| Thailand (USDmn) | -55 | -250 | -2682 |

| Malaysia (USDmn) * | -18 | 88 | -33 |

| Philippines (USDmn) | -4 | -12.3 | -478 |

| Total | 2667 | 3085 | 11584 |

| * Data Up To Jun 11 |

OIL: Off Week to Date Highs As Risk Appetite Cools

The front month Brent contract sits off highs from this week. We were last just under $82.30. This is still comfortably firmer for the week (near +3.5%). WTI was last near $78.05, also up firmly for the week, but away from recent highs.

- News flow has seen focus on slowing China refining demand (see this BBG link), in a further sign that China commodity demand is cooling after a number of decades of very strong growth. Elsewhere attacks on shipping by the Houthi rebels in Yemen appear to have picked up in recent days.

- More broadly risk sentiment has been slightly softer in the past 24 hours, with on-going political uncertainty in the EU a clear headwind for assets in that region, which has seen some spill over more broadly. Firmer USD levels will also be curbing oil gains to a degree.

- For WTI, key short-term resistance lies at $80.62, the May 29 high. On the downside, a resumption of weakness would open $71.33, the Feb 5 low.

GOLD: Lower Despite Lower US Treasury Yields

Gold is little changed in the Asia-Pac session, after closing 0.9% lower at $2304.21 on Thursday.

- Thursday’s decline came despite lower US Treasury yields. Lower rates are typically positive for gold, which doesn’t pay interest.

- US Treasuries recovered from their post-FOMC sell-off following yesterday's softer PPI and higher weekly claims. It rekindled 50bps in rate cut pricing by year-end.

- PPI final demand printed lower than expected at -0.2% vs. 0.1% m/m (2.2% y/y vs. 2.5% est), Ex Food and Energy m/m 0.0% vs. 0.3% est, (y/y 2.3% vs. 2.5%). Meanwhile, weekly jobless claims were higher than expected at 242k vs. 225k est, continuing claims 1.82m vs. 1.795m.

- According to MNI’s technicals team, the yellow metal traded below the 50-day EMA, at $2,313.6. The break confirmed a resumption of the reversal that started May 20 and opens $2,277.4, the May 3 low. Initial firm resistance to watch is $2387.8, the Jun 7 high.

INDONESIA: New Government Reportedly Plans To Raise Debt-To-GDP Ratio To 50%.

Bloomberg has reported that incoming Indonesian President Prabowo (who will come into office later this year) will steadily raise the country's debt to GDP ratio to 50%, from the current -39%. See this link for more details.

- The Newswire notes " He aims to raise the debt-to-gross domestic product ratio by 2 percentage points annually over the next five years, according to people familiar with the matter."

- It adds: "Prabowo is focused on how to fit his programs, especially the food and nutrition ones, into the 2025 budget in line with targets set by the current government while ensuring fiscal prudence, said Thomas Djiwandono, a member of the president-elect’s economic transition team."

- There has been speculation around increased government spending by the new administration, with focus likely to rest on how new funds would be spent. If it boosts Indonesia's long term growth outlook, there may be less fallout from the news from a market sentiment standpoint.

- Part of Prabowo's spending plan is aimed at providing free lunches for children, along with other welfare programs.

- Foreign ownership of Indonesia government bonds is lower in 2024 to date, but above 2022 lows in an outright IDR sense, see the chart below.

- INDON yields have moved 10-30bps tighter over the past month, with the belly of the curve seeing the most demand, while the ID-US 7yr spread difference has held steady over the same period.

Fig 1: Foreign Ownership Of Indonesia Government Bonds

Source: MNI - Market News/Bloomberg

INDONESIA: Local Debt Yields Higher On Prabowo Plans To Increase Debt-To-GDP

The INDON sov curve has moved tighter today, while USD to IDR debt spread has widened with local currency debt moving 5-12bps wider on headlines out earlier around President elect looking to increase the Debt-To-GDP ratio towards 50%.

- The INDON curve has seen better buying through the belly of the curve today, with the 3-7yr part of the curve about 4bps lower. The 2Y yield is -2bp at 5.25%, 5Y yield is -3.5bps at 4.965%, the 10Y yield is -3bp at 5.05%, while the 5-year CDS is 0.5bp higher at 72bps.

- Local debt yields have continued to sell off plans to increase debt over the coming years, currently the 5yr is trading 12bps higher at 7.04%

- The INDON to UST spread diff the 2Y is now 54.5bps (+4bp), 5yr is 70.5bps (+2bp), while the 10yr is 79bps (+4bp).

- In cross-asset moves: USD/IDR is up 0.50%, last near 16360 and now back of 2020 levels, the JCI is down -0.62%. US Tsys futures are a touch lower today, while yields are 1-3bps higher.

- Indonesia's President-elect Prabowo Subianto plans to gradually increase the country's debt-to-GDP ratio by 2 percentage points annually, aiming for a 50% ratio by the end of his term to fund welfare programs and infrastructure, while maintaining investor confidence through fiscal prudence. This approach marks a shift from Indonesia's traditionally conservative fiscal policy, yet aims to keep debt levels below those of regional neighbors Malaysia, Thailand, and Singapore.

- Looking ahead: There is little on the local data calendar until Trade Balance data on Wednesday

ASIA FX: USD/Asia Pairs Higher, USD/IDR To Fresh Highs On Debt Plan Concerns

USD/Asia pairs are mostly higher, amid a broadly supportive USD backdrop, along with fresh yen losses in the aftermath of today's BoJ decision. IDR has fallen to fresh lows back to early 2020, after Bloomberg reported incoming President Prabowo is likely to raise the country's debt to GDP level to 50% (from the current ~39%). Regional equity markets are also mostly lower. Next Monday we have China's 1yr MLF rate (no change expected), along with May activity data prints. Later next week is the BI decision.

- USD/CNH has been supported on dips, but overall ranges have been tight. We were last near 7.2710, slightly off recent highs near 7.2750. The USD/CNY fix rose to fresh highs back to Jan 19. USD/CNY spot has gravitated close to its upper daily trading limit. Local equities are weaker continuing the recent run of softness.

- 1 month USD/KRW has mostly spent the session on the front foot, we were last near 1375.5, close to session highs, but still sub 1380. Spill over from yen weakness has likely been a headwind. Local equities are outperforming on the back of resilient global tech equity trends. The Kospi was last +0.30% higher, with the extension of the short selling ban also aiding the local equity backdrop.

- Similar factors have pushed USD/TWD higher as well. Spot was last near 32.40. Late yesterday the CBC kept rates on hold by raised the RRR in order to curb liquidity in terms of flows to the local property market.

- USD/IDR is seeing firm gains in the first part of Friday trade. Spot is up 0.65%, last near 16375, which is fresh highs in the pair back to early 2020 (during the risk off period around the onset of the Covid pandemic). Highs from that period were at 16625. On the downside the 20-day EMA is back near 16192. Through June dips in the pair have been supported sub 16200. Weaker sentiment has likely reflected market reaction to a Bloomberg story that incoming President Prabowo plans to raise the debt-to-GDP level to 50% (from the current ~39%). Fiscal slippage remains a market concern, with onshore bond yields, up 7-8bps for the 5 and 10yr tenors.

- Elsewhere, the USD is mostly firmer. USD/THB is up around 0.30%, last near 36.75/80. Part of this is reflective of dollar gains post yesterday's onshore close, but the weaker yen trend today will be an additional headwind.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/06/2024 | 0600/0800 | *** |  | SE | Inflation Report |

| 14/06/2024 | 0645/0845 | *** |  | FR | HICP (f) |

| 14/06/2024 | 0830/0930 | ** |  | UK | Bank of England/Ipsos Inflation Attitudes Survey |

| 14/06/2024 | 0900/1100 | * |  | EU | Trade Balance |

| 14/06/2024 | 0900/1100 | | EU | ECB's Lane participates at Dubrovnik Economic Conference | |

| 14/06/2024 | 0900/1100 | | EU | ECB's De Guindos at Carlos V European Prize Ceremony | |

| 14/06/2024 | 1230/0830 | ** |  | US | Import/Export Price Index |

| 14/06/2024 | 1230/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 14/06/2024 | 1230/0830 | ** | | CA | Wholesale Trade |

| 14/06/2024 | 1330/1530 | | EU | ECB's Schnabel in European Fiscal Board Meeting | |

| 14/06/2024 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 14/06/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 14/06/2024 | 1730/1930 | | EU | ECB's Lagarde Speech at Dubrovnik Economic Conference | |

| 14/06/2024 | 1800/1400 | | US | Chicago Fed's Austan Goolsbee | |

| 14/06/2024 | 2300/1900 | | US | Fed Governor Lisa Cook |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.