Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The moves from U.S. policymakers re: stemming the fallout from the failure of SVB were front and centre. The introduction of a new Fed funding scheme for deposit taking institutions and the decision to make depositors at SVB (and another failed bank) whole provided the focal points.

- The USD faltered on this, with a subsequent pullback in swap rate pricing re: the Fed's terminal rate and deeper pricing of cuts by year-end adding further support to equities.

- There is a thin data calendar in Europe today, the session will be dominated by the evolving SVB situation and continued re-pricing of Fed rate expectations.

US TSYS: Curve Twist Steepens, Fed Rate Hike Expectations Pared

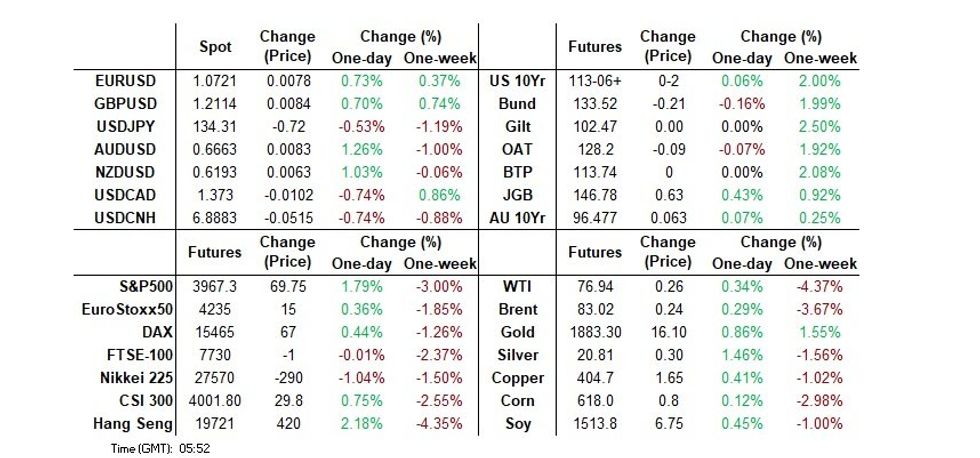

TYM3 deals at 113-07+, +0-03, with a 1-11 range observed on volume of ~412k. To recap early events in Asia, the Fed have created a new funding operation to stem the risk of a run on deposit taking institutions, while the Fed, US Treasury and FDIC noted in a joint statement that SVB depositors would be made whole.

- Cash tsys sit 14bps richer to 5bps cheaper across the major benchmarks, the curve has twist steepened pivoting on 20s.

- The rally in 2s adds to the largest 2 day gain lodged since the GFC.

- Tsys futures initially gapped higher at the re-open as Asia participants reacted to Friday's price action and the lack of immediate resolution re SVB.

- The initial move reversed on headlines that the Fed has announced a new emergency bank term funding scheme. Fed, US Treasury and FDIC noted in a joint statement that SVB depositors would be made whole, further adding further pressure.

- Tsys firmed off session lows as, on the sell side, Goldman Sachs updated their call for the March Fed meeting. They no longer look for a hike from the Fed later this month although they leave their 25bp hike calls for the May, June & July meetings pencilled in, albeit with considerable uncertainty cited.

- Fed-dated OIS has 23bps of tightening for next week’s meeting, after pricing ~43.5bp of tightening at one point last week. Pricing for the terminal rate is now at a touch below 5.1% now seen in June, trimming ~20bps today. There are ~43bps of cuts priced for H2 2023.

- There is a thin data calendar in Europe today, the session will be dominated by the evolving SVB situation. Tomorrow's February CPI, flagged by Fed Chair Powell as a key input into this month's FOMC decision, headlines the week's docket.

JGBS: Firmer & Flatter On Global Impulse

JGB futures were off best levels at the closing bell, although comfortably firmer, +57. Cash JGBs are flat to ~11bp richer, with the early flattening extending, aided by receiver side flows in swaps as swap spreads sit flat to tighter on the day. 10-Year JGB yields now sit at the lowest level observed since the BoJ’s surprise YCC tweak back in December (0.31%), nearly 20bp off the YCC cap.

- Global factors were at the fore today, with the moves from U.S. policymakers re: stemming the fallout from the failure of SVB front and centre. The introduction of a new Fed funding scheme for deposit taking institutions and the decision to make depositors at SVB (and another failed bank) whole provided the focal points.

- Locally, the junior ruling coalition partner, Komeito, indicated that it will be seeking several trillion JPY of stimulus spending, focused on supporting families with children and in a bid to reduce LNG prices.

- The latest quarterly BSI survey provided a deterioration in sentiment for large firms.

- Tomorrow’s domestic data slate is empty, although we will get the latest 5-Year JGB auction. That should leave the broader tone at the fore for most of Tuesday’s session.

AUSSIE BONDS: Focus On The SVB Situation Remains

ACGBs close firmer on the day (YM +12.4 & XM +6.3) but well off bests set before U.S. authorities made announcements about the Silicon Valley Bank (SVB) situation in early Asia-Pac trade. Cash ACGBs close 6-13bp lower with the 3/10 curve 6bp steeper.

- The 3s10s swaps curve bull steepens 5bp on the day with rates 2-8bp lower and EFPs 4-5bp wider.

- The bills strip richened 4-11bp on the day, led by late whites/early reds, but was well off session bests.

- RBA dated OIS pricing closed 7-12bp softer for meetings beyond April with pricing for the April meeting declining to a 27% chance of a 25bp hike.

- While light today, the local calendar delivers this week two releases explicitly cited by the RBA as important for April’s policy discussion, namely February NAB Business Survey tomorrow and the February Employment Report on Thursday. After two consecutive monthly declines the market is looking for a strong result (BBG consensus +50k) to defuse expectations of labour market stagnation.

- Until then, the market will likely continue to track the direction of U.S. Tsys as it wades through information regarding SVB and the U.S. authorities’ policy initiatives. The U.S. calendar also has the release of February CPI slated for Tuesday.

NZGBS: Tracking SVB Developments But Underperforming U.S. Tsys

In line with developments in global FI in Asia-Pac trade, NZGBs open stronger, reverse on policy announcements from U.S. authorities regarding Silicon Valley Bank (SVB) and then richen again to close 9-11bp stronger. The re-strengthening was linked to U.S. Tsy yields pushing below Friday session lows following news that Goldman Sachs no longer expected a hike from the Fed later this month.

- The 2/10 benchmark curve steepened by 2bp with the NZ/US 10-year differential +7bp.

- Swaps close 8-10bp richer, implying a wider 3-year swap spread.

- RBNZ dated OIS softened 7-19bp across meetings led by February-24. April meeting pricing softened to 36bp of tightening with terminal rate expectations falling below the RBNZ’s projected OCR peak of 5.50% to 5.44%.

- On the local data front, BusinessNZ PSI showed an upbeat 55.8 for February (54.5 in January) while February Food prices rose 1.5% M/M reflecting the impact of Cyclone Gabrielle.

- Tomorrow’s local calendar sees February REINZ house prices and Net Migration slated ahead of Q4 Current Account on Wednesday and Q4 GDP on Thursday.

- The market is however likely to remain almost entirely focused on developments in the SVB saga ahead of the release of US CPI for February on Tuesday.

FOREX: USD Pressured, Fed Rate Hike Expectations Pared

The greenback is pressured in Asia as expectations for Fed rate hikes are pared. OIS prices ~23bps of tightening for next week’s meeting, after pricing ~43.5bp of tightening at one point last week. To recap early events in Asia, the Fed have created a new funding operation to stem the risk of a run on deposit taking institutions, while the Fed, US Treasury and FDIC noted in a joint statement that SVB depositors would be made whole.

- AUD is the strongest performer in the G-10 space at the margins. AUD/USD prints at $0.6660/65 ~1.3% firmer today. The next upside target for bulls is $0.6695, the low from 1 March.

- Kiwi is also firmer, benefiting from the improved risk appetite. NZD/USD prints at $0.6195/0.6200, the pair is ~1.1% firmer. Westpac also revised their RBNZ call for the next meeting down to 25bps.

- USD/JPY prints at ¥134.10/20, dealing a touch below the 50-Day EMA at ¥134.23. The pair has been supported on breaks below ¥134.

- Elsewhere in the G-10 space broad based USD weakness is evident. BBDXY is down ~0.8%, having broken its 20-day EMA in early dealing.

- Cross asset wise, US Equity futures are firmer. S&P500 E-minis are up ~1.7%. The US Treasury Curve has steepened.

- There is a thin data calendar in Europe today, the session will be dominated by the evolving SVB situation and continued re-pricing of Fed rate expectations.

FX OPTIONS: Expiries for Mar13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500-10(E1.2bln), $1.0540-50(E1.0bln), $1.0600(E1.6bln), $1.0690-00(E2.1bln)

- USD/JPY: Y133.00($570mln), Y135.00($809mln), Y136.00($711mln), Y137.00($590mln)

- GBP/USD: $1.2075-00(Gbp577mln)

- USD/CNY: Cny6.8500($1.2bln)

ASIA FX: Broad Based Gains Amid US Yield Pull Back

USD/Asia pairs are lower across the board, albeit to varying degrees. The ADXY is back close to 101, +0.60% higher for the session, as broad USD sentiment has faltered amid the further pull back in US yields. The collapse of SVB has seen a sharp pull back in US tightening expectations, while the US authorities' steps (US Fed funding supporting, and ensuring SVB deposits are whole) has limited the fallout for regional equities. Still to come is Indian CPI for Feb, while tomorrow delivers South Korean trade prices and Indian wholesale prices. Philippines trade figures are also due.

- USD/CNH got to a low of 6.8645, but we now sit slightly higher at 6.8900. A modest recovery in US yields this afternoon has curbed USD losses, albeit only at the margin. New Premier Li Qiang stated it won't be easy to hit the 5% growth target, although onshore equities are firmer, near gains of 0.70%. The Premier also emphasized the importance of the private sector, while weekend news of Yi Gang being re-appointed as PBoC Governor was also a welcome surprise for markets looking for policy continuity.

- 1 month USD/KRW sits slightly above session lows, last near 1299 (we got to 1297 earlier). Onshore equities have recovered from earlier losses, with the Kospi now +0.65%. The South Korean authorities stated they are ready to curb excessive market moves in the wake of the SVB collapse if needed.

- USD/SGD is softer today, as falling US Yields weigh on the greenback, last printing at $1.3440/50 down ~0.%. The pair tested its 20-day EMA ($1.3435) as bears look to continue today's move lower, but we last sit slightly higher. On Friday SGD NEER (per Goldman Sachs estimates) was marginally softer. We sit ~0.9% below the top end of the band.

- USD/INR prints at 81.90/00, ~0.2% softer today. The rupee is benefitting from the broad based USD weakness in Asia, however USD/INR is lagging compared to its peers (ADXY is up ~0.6%), perhaps a reflection of the INRs recent outperformance in March. Equity inflows continued last week with ~$564mn in local equities bought by global investors in the week to Thursday. On the wires today we have Feb CPI, the Bloomberg Median Estimate is at 6.4% which is above the upper inflation target of the RBI. A firm print may reduce odds of an RBI pause in the April policy meeting.

- USD/IDR is down 0.60% last near 15360/65. Pared Fed expectations should benefit the IDR, all else equal. Rupiah bulls will target a move towards the 20-day EMA, which is just below 15290. USD/THB has pulled back sharply, last near 34.60. We did get as low as 34.425 in the pair.

EQUITIES: HK/China Equities Outperform, Higher US Futures Limit Losses Elsewhere

HK and China related equities have outperformed so far today. The HSI is up over 2%, the China Enterprise Index near a 3% gain. Elsewhere the focus has been on the rebound in US futures, with eminis and Nasdaq futures up +1.6%, as the US authorities seek to limit the fallout from the SVB collapse, with a number of backstops now in place ahead of Monday's US open. This has helped regional markets pare losses or climb into positive territory for today's session.

- China and HK shares have likely benefited from the NPC announcement over the weekend that current PBoC Governor Yi Gang would continue to serve in the post. It had been widely expected that he would retire. The Commerce and Finance Ministry positions also maintained the status quo. This should give the market some comfort of policy continuity.

- Mainland shares have lagged HK moves, but are still up near 0.90% for the CSI 300.

- Elsewhere, the picture is more mixed. Japan's Nikkei 225 is down around 1.5% at this stage, although away from lows for the session. Banking and finance related names have been a saw of weakness. The Kospi (+0.45%) and Taiex (0.10%) have fared better.

- The ASX 200 is down 0.50%, while Singapore and Malaysian markets are off by 0.7% and 0.9% respectively.

GOLD: Benefiting From Continued USD Pullback, But Some Resistance Ahead of $1890.

Gold continues to recover, up a further 0.80% so far today. We have gotten close to $1890 on a couple of occasions but there appears to be some resistance ahead of this level. We last tracked at $1882. The $1890 region represents highs from early February for the precious metal, so may be acting as a near term resistance point.

- Gold is back above all key EMA levels. Beyond $1890 lies the $1900, which we haven't been above since early February.

- Gold's move higher today is in line with USD weakness, with the BBDXY off by around 0.80% at this stage. Reduced risk aversion, evidenced in the equity space, is not diminishing gold demand from a reduced safe haven demand standpoint, although this may have helped limit gains beyond the $1890 level.

- The bigger driver is the weaker USD trend and yield pull back.

OIL: Underperforming Other Risk Assets

Brent crude is marginally firmer, +0.20% for the Monday session so far. This is underperforming broader risk appetite trends, where the USD is off by ~0.80%, while US equity futures are close to session highs. For Brent, we haven't been able to make much headway above the $83/bbl level, which is where we currently track. For WTI, we are just shy of the $77/bbl level.

- Brent is sub all the key EMA levels, with the 20-day, around $83.65/bbl, not too far away on the topside.

- China comments from new Premier Li Qiang that hitting the 5% growth target won't be easy may have weighed on oil sentiment at the margins. Still, other comments were encouraging from the perspective of opening up the China economy and support of the private sector.

- The skew of market positioning still remains placed for higher oil prices. ICE Brent futures data remain heavily skewed towards longs, as of Tuesday last week.

- Looking ahead, on Tuesday we get the OPEC monthly oil report, along with US CPI. While on Wednesday the IEA monthly report is out, as well as China monthly activity figures.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/03/2023 | - |  | EU | ECB Panetta at Eurogroup Meeting | |

| 13/03/2023 | 1230/0830 | * |  | CA | Household debt-to-disposable income |

| 13/03/2023 | 1530/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 13/03/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 13/03/2023 | 1805/1805 |  | UK | BOE Dhingra Panellist at International Women’s Day event |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.