Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- In Australia, July CPI inflation rose 4.9% y/y down from 5.4%, which was lower than expected but still in the range of forecasts. With inflation declining more than expected and heading towards the RBA’s 4.1% Q4 2023 forecast, rates are likely to be on hold again at the September meeting. RBA-dated OIS pricing is 2-4bp softer for ’24 meetings. A 2% chance of a 25bp hike is priced for September. Still the AUD has pared losses, finding support at post data lows at 0.6450.

- Elsewhere, BoJ Board Member Naoki Tamura stated that the achievement of stable and sustainable 2% inflation is finally and clearly within sight. Cash JGBs are cheaper across the curve, with yields 0.1bp (1-year) to 0.7bp higher (3-year). US cash tsys sit ~1bp cheaper across the major benchmarks.

- Regional equities have mostly been positive, although China markets have struggled to maintain positive momentum. USD/CNH has moved back towards 7.3000. We have official PMI data for August on tap tomorrow.

- Looking ahead, early focus is on EU CPI's, later on US ADP employment for August, July trade balance and updated Q2 GDP are released.

MARKETS

US TSYS: Marginally Cheaper In Muted Asian Session

TYZ3 deals at 110-23, -0-03, a narrow 0-06+ range has been observed on volume of ~100k.

- Cash tsys sit ~1bp cheaper across the major benchmarks.

- Asia-Pac participants faded yesterday's richening in early trade perhaps using the opportunity to close long positions/enter fresh shorts.

- Losses were briefly pared after a bid in ACGB's, in lieu of weaker than forecast CPI ,spilled over.

- The move didn't follow through, tsys ticked lower dealing in a narrow range for the remainder of the session.

- In Europe today regional German CPI provides the highlight. Further out we have US GDP, wholesale inventories and pending home sales.

JGBS: Futures Weaker & At Session Lows, Heavy Local Calendar Tomorrow

JGB futures are weaker and at Tokyo session lows, -14 compared to settlement levels.

- With the data calendar empty so far today, the local market’s focus has been comments from BoJ Board Member Naoki Tamura. He stated that the achievement of stable and sustainable 2% inflation is finally and clearly within sight (See link ICYMI)

- US tsys in Asia-Pac trade also likely weighed on JGBs. Cash tsys sit ~1bp cheaper across the major benchmarks. Asia-Pac participants faded yesterday's richening perhaps using the opportunity to close long positions/enter fresh shorts.

- Cash JGBs are cheaper across the curve, with yields 0.1bp (1-year) to 0.7bp higher (3-year). The benchmark 10-year yield is 0.1bp higher at 0.654%, above BoJ's YCC old limit of 0.50% but below its new hard limit of 1.0%.

- As suggested previously, BoJ Rinban operations, which saw higher and flat to positive spreads and higher cover ratios for the 5-10-year and 25-year+ buckets did generate slight pressure, particularly for the 5-10 bucket and longer-dated JGBs, in the early rounds of the Tokyo afternoon session.

- The swaps curve has bear steepened, with rates 0.1-1.6bp higher. Swap spreads are wider beyond the 3-year.

- Tomorrow the local calendar is heavy, with Retail Sales (Jul), Industrial Production (Jul P), International Investment Flows (Aug 25) and Housing Starts (Jul). We also hear from BoJ Board Member Nakamura.

AUSSIE BONDS: Richer After CPI Monthly Undershoot, Q2 Capex Data Tomorrow

ACGBs (YM +4.0 & XM +2.5) sit richer after the CPI monthly data for July prints better than expected at 4.9% y/y versus 5.2% expected and 5.4% prior. The ABS also released the monthly goods/services and tradeable/non-tradeable components, which is likely useful for the RBA given its focus on services. Goods/tradeables are driving the moderation in headline CPI. However, services inflation eased to 5.6% y/y in July, after a sharp rise to 6.3% in June.

- Construction work done for Q2 and building approvals for July released today also surprised on the downside.

- Cash ACGBs are 3-4bp richer with the AU-US 10-year yield differential 1bp wider at -6bp.

- Swap rates are 2-4bp lower, with the curve steeper.

- The bills strip has bull flattened, with pricing flat to +6.

- (AFR) Inflation cools to 4.9pc, cementing interest rate pause. (See link)

- Qantas debacle helps explain why Future Fund is staying bearish. (See link)

- RBA-dated OIS pricing is 2-4bp softer for ’24 meetings. A 2% chance of a 25bp hike is priced for September.

- Tomorrow the local calendar sees Q2 Capex and the third estimate of 2023-24 Capex plans. Tax incentives, which expired on 30 June 2023, should boost Q2 capex.

AUSTRALIAN DATA: CPI Moving Towards RBA Forecast, Rates On Hold

July CPI inflation rose 4.9% y/y down from 5.4%, which was lower than expected but still in the range of forecasts. This is the lowest inflation rate since January 2022. Seasonally adjusted it increased 0.3% m/m after +0.5%. Trimmed mean remains higher but moderated to 5.6% y/y in July from 6%, the lowest in a year. With inflation declining more than expected and heading towards the RBA’s 4.1% Q4 2023 forecast, rates are likely to be on hold again at the September meeting.

- CPI ex volatile items & holidays eased to 5.8% y/y in July from 6.1%. It was up 0.5% on the month after 0.3% and 3-month momentum is around 4.5% where it has been since May. CPI ex volatile items is now down 1.4pp from its December 2022 peak whereas headline is down 3.6pp. While underlying inflation is looking stickier, it is still heading in the right direction (see chart).

- Auto fuel and fruit & veg put downward pressure on inflation falling 7.6% y/y and 5.4% respectively. Again the ABS pointed out that it is worth looking at CPI excluding the volatile items like food and fuel.

- Housing continued to be strong at 7.3% y/y with rents up 7.6% from 7.3% but new dwelling inflation at its lowest since October 2021 at 5.9% driven by building materials.

- Electricity prices rose 6% m/m in July to be 15.7% y/y higher and the ABS notes that without government rebates they would have risen 19.2% y/y.

Source: MNI - Market News/ABS

AUSTRALIA DATA: Monthly Data Show Sticky Domestically-Driven Inflation

The ABS has released the monthly goods/services and tradeables/non-tradeables components which given the RBA’s focus on services will be helpful. In the August RBA statement it said that “goods price inflation has eased, but the prices of many services are rising briskly”. Both services and non-tradeables inflation are off their peak but are not only still “too high” but are looking sticky. Goods/tradeables are driving the moderation in headline CPI.

- There was a sharp rise in June services inflation to 6.3% y/y and that eased to 5.6% in July but the series is volatile and has been zigzagging since the start of 2023. It continues to run ahead of goods prices which rose 4.4% y/y in July down from 4.7%. Wages are an important driver of services inflation.

Source: MNI - Market News/ABS

- The move down in the domestically-driven non-tradeables CPI was not as pronounced at 6.5% y/y from 6.6%. It has been running around this rate for the last three months and is looking reluctant to come down further. It is off its December peak of 7.7%. Tradeables moderated sharply to 1.7% from 3.2%.

Source: MNI - Market News/ABS

AUSTRALIAN DATA: Approvals Remain Depressed Despite Growing Population

Building approvals fell a sharper-than-expected 8.1% m/m in July after falling 7.9% in June. The weakness was due to the volatile multi-dwelling component which fell 15.8% m/m after -21.9% whereas private homes rose 0.1% after -1% to be down 16.9% y/y. The weakness in home building is a concern given working age population is growing at a series high and the impact it has on economic growth, which the RBA cited in its last meeting statement. Approvals in July were 21.2% below the February 2020 level.

Australia number of dwellings approved - private houses

Source: MNI - Market News/ABS

NZGBS: Closed At Session Bests, Business Confidence Tomorrow

NZGBs concluded the session near their best levels, with benchmark yields declining 5-6bp. While weaker dwelling approvals likely contributed to the bid, the more likely factor behind the through-session strengthening seems to be a partial unwind of weakness earlier in the week triggered by fiscal deterioration concerns.

- Despite some cheapening in US tsys in the Asia-Pac trading, the local market’s resilience allowed the NZ-US 10-year yield differential to close unchanged at +80bp. The NZGB 10-year outperformed its ACGB counterpart by 2bp on the day, despite favourable AU inflation data.

- Swap rates are 6-8bp lower, with implied swap spreads little changed.

- RBNZ dated OIS pricing is flat to 4bp softer across meetings. Terminal OCR expectations sit at 5.61%, the lower bound of its recent range.

- Dwelling approvals fell 5.2% m/m in July versus a revised +3.4% in June. House approvals fell 18.8% m/m in July versus +8.8% in June.

- The RBNZ sold close to NZ$4 billion ($2.4 billion) in July to build its reserves of foreign currencies. (See link)

- Tomorrow the local calendar sees ANZ Business Confidence.

- Tomorrow the NZ Treasury plans to sell NZ$225mn of the 0.25% May-28 bond, NZ$175mn of the 1.50% May-31 bond and NZ$100mn of the 1.75% May-41 bond.

FOREX: USD Trims Tuesday's Losses In Asia

The greenback has trimmed some of yesterday's losses in Asia today, the Antipodeans are the weakest performers in the G-10 space at the margins.

- AUD/USD is down ~0.2%, the pair last prints at $0.6470/75. CPI rose 4.9% Y/Y in July, below the estimate of 5.2%. July building approvals fell 8.1% m/m versus an estimated 0.5% contraction. The pair found support at $0.6450 and marginally pared losses through the session.

- Kiwi is the weakest performer in the G-10 space, NZD/USD is down ~0.2%. The RBNZ sold a net of $4bn NZD to build its reserves of foreign currencies. The Reserve Bank sold a net NZ$3.96 billion, according to data posted on its website, the largest sale in records dating to 2004. Early in the session July Building Permits fell 5.2% M/M, the prior read was revised lower to 3.4%.

- The Yen is also marginally pressured, USD/JPY has firmed above the ¥146 handle as US Tsy Yields tick higher. The uptrend remains intact, resistance comes in at ¥147.37 (yesterday's high) whilst support is at ¥144.77 (20-Day EMA).

- Elsewhere in G-10 EUR and GBP are both following broader USD flows and are down ~0.1%.

- Cross asset wise; BBDXY is up ~0.1% and US Tsy Yields are ~1bp higher across the curve. US Equity futures are firmer; e-minis are up ~0.2% and NASDAQ futures are up ~0.3%.

- In Europe today regional German CPI provides the highlight

EQUITIES: Lower Inflation Aids Australian Stock Outperformance

Regional equities are tracking higher in Asia Pac trade for Wednesday. Gains are quite uniform across the major indices, albeit with varying betas with respect to US gains from Tuesday's session. Australian stocks are the standout, while most other indices are less than 1% firmer at this stage. US equity futures are maintaining a positive trend, with Eminis last near 4514, which is levels last seen back in mid August. Nasdaq futures are slightly outperforming, last +0.24% to 15453.

- The ASX 200 is tracking +1.4% firmer in Australia, comfortably the best performer in the region. Financial stocks have led the way, post the July CPI miss, which may see the RBA pause further. Gains were also evident elsewhere, with 10 out of 11 sectors rising.

- China stocks were firmer earlier but couldn't sustain gains. The CSI 300 is +0.06% at the break after being as high as +0.60% earlier. The index sits below the 3800 level. Prospects for further bank interest rate cuts on mortgages and deposits has weighed on the banking sector. Still, Bloomberg notes China's largest ETF is on track for record inflows in August (see this link for more details).

- The HSI is +0.59% at the break, but also sub earlier highs. Tomorrow, we get official China PMI prints for August, which are expected to show a further loss of growth momentum.

- The Kospi and Taiex are tracking higher (around +0.60%), in line with better tech tones from Tuesday's US session.

- In SEA, Philippine stocks are up 0.90%, reversing some of the recent underperformance.

OIL: Crude Higher Again As Stocks Decline & Market More Optimistic On Demand

Oil prices are up another 0.4% after rising around 1.5% on Tuesday after API data showed a large US stock drawdown. Better risk sentiment is also supporting crude. WTI is up 0.4% to $81.50/bbl, close to the intraday high of $81.61. It is approaching resistance at $81.75. Brent is 0.3% higher at $85.75, which has opened up the bull trigger at $88.10. Oil has rallied despite the stronger dollar (USD index +0.2%).

- Bloomberg reported that API data showed a massive 11.5mn barrel US inventory drawdown in the latest week after -2.4mn, according to people familiar with the numbers. Distillate rose 2.5mn and gasoline +1.4mn. The official EIA data is out later today.

- Markets are generally more optimistic as they speculate that there will be more economic stimulus in China and that the Fed has done tightening. Key US payrolls are out Friday and China PMIs on Thursday.

- While markets are more positive this week on the demand outlook, Bloomberg is reporting that Russian seaborne crude shipments may have reached their highest in 8 weeks. Also talks continue to ease sanctions on Iran and Venezuela’s oil.

- US ADP employment for August, July trade balance and updated Q2 GDP are released today as well as the European Commission August survey and preliminary August German and Spanish CPIs.

GOLD: Strong Gain After Weak US Data

Gold is little changed in the Asia-Pac session, following a notable +0.9% increase on Tuesday that propelled it to its highest point in three weeks.

- The surge in the precious metal can be directly attributed to the decline of the USD and a substantial drop in US treasury yields. These shifts were instigated by underwhelming consumer confidence and JOLTS data, which further substantiated the notion that the Federal Reserve is drawing closer to concluding its phase of monetary tightening.

- The Conference Board's report on consumer confidence revealed figures lower than anticipated, encompassing key labour market indicators. Notably, the disparity between the indices for "plentiful" jobs and "hard-to-get" jobs dwindled to its lowest level since the early months of 2021.

- JOLTS data unveiled a more significant decrease in job openings than expected, reaching a point that hasn't been witnessed in over two years. Job openings have experienced declines in six out of the last seven months. Furthermore, the rate of employees voluntarily leaving their jobs reverted to levels observed before the pandemic took hold.

- This valuable metal has successfully surpassed the 50-day EMA ($1930.4), subsequently ushering in the possibility of reaching $1946.8 (the high point from August 4), as suggested by MNI's team of technical experts.

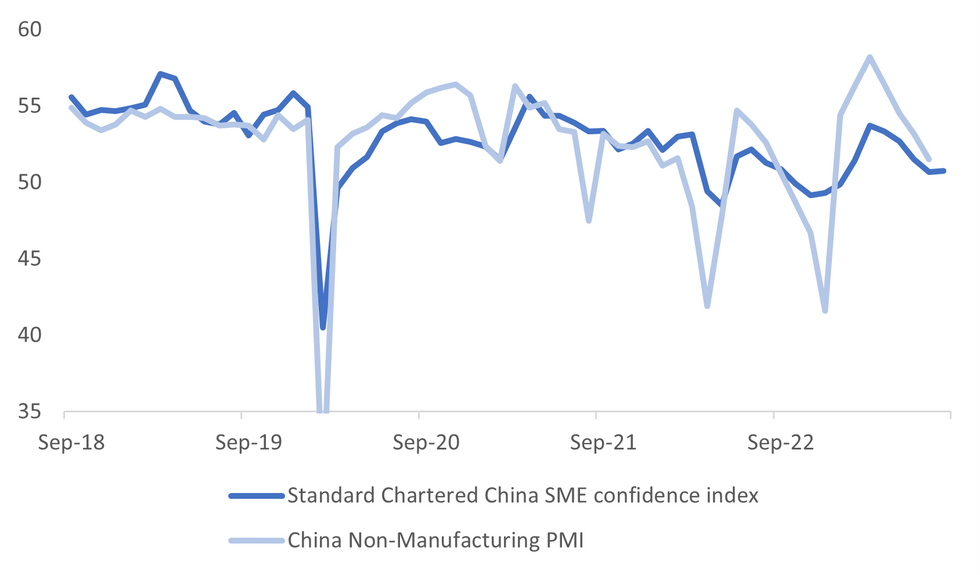

CHINA DATA: Official PMIs Expected To Weaken For August

A reminder that tomorrow sees official China PMIs print for August. The market expects both the manufacturing and services side to have lost momentum in the month. The market consensus for the manufacturing outcome is 49.2 (prior was 49.3, while the forecast range is 48.6 to 49.6). On the services side the forecast is 51.2 (prior was 51.5, forecast range is 50.5-52.0). The composite PMI printed at 51.1 in July, but there is no consensus estimate for this index.

- Headwinds persist in terms of property sector woes and restrained consumer spending, which is expected to weigh on services related activity in the month. This is also fits with the weaker equity tone over the past month, despite renewed policy efforts to support the economy.

- Note the Standard Chartered China SME index edged slightly higher in August to 50.8 from 50.7, see the chart below. The SC measure isn't suggesting a sharp turnaround though, which would also go against the headwinds outlined above.

Fig 1: Standard Chartered China SME Index Versus Services PMI

Source: Standard Chartered/MNI - Market News/Bloomberg

- On the manufacturing side, similar headwinds could be in play, albeit with government spending in the infrastructure area potentially providing some offset. External demand gauges will also be eyed, with export trends to China still fairly weak.

- The China Emerging Industry PMI has also printed for August, rising to 48.1 from 47.1 in July. Still the official manufacturing PMI rose in July, while the emerging industry PMI fell sharply, so the recent directional correlational is not that strong.

ASIA FX: USD/Asia Pairs Up From Lows, Busy Data Calendar Tomorrow

USD/Asia pairs have moved off earlier lows, with Asian FX losing momentum as the session progressed. USD/CNH pushed back above 7.3000, but remains below pre-US data levels from Tuesday's session. 1 month USD/KRW also couldn't break lower. USD gains are modest overall though. Tomorrow, we get China official PMI prints for August, which will be the main focus. South Korean IP also prints, along with Indian Q2 GDP and Thailand IP and Bop/trade data.

- USD/CNH has tracked higher in recent dealings, last near 7.3000, around 0.20% weaker since the open in CNH terms. Earlier lows were at 7.2816. This keeps us within recent ranges, but we have unwound some of the USD weakness seen post Tuesday data misses - highs for USD/CNH prior to these prints were just above 7.3100. CNH weakness has coincided with a loss in positive momentum for local equities, which are back to around flat after being as high as +0.60%for the CSI 300.

- 1 month USD/KRW couldn't test lower, despite a positive equity lead from Tuesday. The Kospi is +0.50% higher, but the 1 month is still support in the 1316/17 region. We last tracked near 1321, remaining well within recent ranges.

- USD/THB is above earlier lows just under 35.00, the pair last near 35.10. We remain comfortably within recent ranges, with baht bulls targeting a sustained break of the 20-day EMA, which comes in at 35.03, while on the topside, August highs sit back near 35.60. On the tourism front, new PM Srettha is reportedly looking at easing rules (such as cutting fees and extending stay limits) for travelers from China and India in order to boost the outlook ahead of the Q4 peak tourism season.

- USD/IDR gapped lower at the open, hitting 15217, but sits slightly higher now, last near 15235, still ~0.15% firmer in IDR terms versus yesterday's close. The 1 month NDF has seen modest upside today versus NY closing levels on Tuesday, last at 15241. IDR has benefited from the pull back in US real yields following US data misses, the 10yr back to +183bps, versus recent cyclical highs of +200bps. BI Governor Wariyo stated late yesterday that 68 exporters had placed export proceeds into special accounts onshore, up from 34 previously. The Governor stated this could bring in $8-9bn in extra FX reserves by December. The central bank sees USD/IDR averaging 14850 next year versus 15000 for 2023. Note the YTD 2023 average is 15080.

- The Rupee sits marginally below Tuesday's closing levels. USD/INR prints at 82.76/78, ranges in the pair remain narrow and moves have had little follow through in recent dealing. We sit above 20-Day EMA (82.6844) and well within the August range. India has cut cooking gas prices to soften the impact of rising inflation on household expenses as the nation heads into seasonal festivals and key elections. Q2 GDP is due tomorrow, an uptick to 7.8% Y/Y from 6.1% is expected. Also on the wires tomorrow is the July Fiscal Deficit and Eight Infrastructure Industries Index.

- The Ringgit is firmer in early dealing as onshore markets digest yesterday's weaker than forecast US data. USD/MYR prints at 4.6385/4.6430 ~0.1% lower in early dealing. The pair now sits ~0.6% below the August high as monthly gains continue to be trimmed.

- The SGD NEER (per Goldman Sachs estimates) is marginally softer in early dealing and has ticked away from its highest level since 18 Jul in recent dealing. The measure is ~0.4% below the top of the band. The SGD NEER (per Goldman Sachs estimates) is marginally softer in early dealing and has ticked away from its highest level since 18 Jul in recent dealing. The measure is ~0.4% below the top of the band. The pair has found support below the 20-Day EMA ($1.3511) and sits a touch above the measure in early dealing today.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/08/2023 | 0530/0730 | *** |  | DE | North Rhine Westphalia CPI |

| 30/08/2023 | 0600/1400 | ** |  | CN | MNI China Liquidity Survey |

| 30/08/2023 | 0700/0900 | *** |  | ES | HICP (p) |

| 30/08/2023 | 0700/0900 | ** |  | SE | Economic Tendency Indicator |

| 30/08/2023 | 0700/0900 | * |  | CH | KOF Economic Barometer |

| 30/08/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 30/08/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 30/08/2023 | 0800/1000 | *** | | DE | Bavaria CPI |

| 30/08/2023 | 0830/0930 | ** |  | UK | BOE M4 |

| 30/08/2023 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 30/08/2023 | 0900/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 30/08/2023 | 0900/1100 | *** | | DE | Saxony CPI |

| 30/08/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 30/08/2023 | 1200/1400 | *** | | DE | HICP (p) |

| 30/08/2023 | 1215/0815 | *** | | US | ADP Employment Report |

| 30/08/2023 | 1230/0830 | *** | | US | GDP |

| 30/08/2023 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 30/08/2023 | 1400/1000 | ** | | US | NAR Pending Home Sales |

| 30/08/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.