Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

OVERNIGHT NEWS AND PRESS

* WHITE HOUSE UPS STIMULUS OFFER, PELOSI HOPEFUL ON DEAL THIS WEEK (BBG)

* MCCONNELL WARNS WHITE HOUSE AGAINST STIMULUS DEAL PRE-ELECTION (W POST)

* FED'S EVANS: NO URGENCY TO RAMP UP QE NOW (MNI)

* HUAWEI, CHINA FIRMS ARE SAID TO SEEK CURBS ON NVIDIA'S ARM DEAL (BBG)

* ASTRAZENECA U.S. VACCINE TRIAL EXP. TO RESUME AS EARLY AS THIS WEEK (RTRS SOURCES)

EXECUTIVE SUMMARY

Fig. 1: U.S. 30-Year Tsy Yield

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

CORONAVIRUS: Northern cities have been put on notice that more could follow Manchester into tough Covid restrictions by the weekend as Boris Johnson suggested that full-scale regional lockdowns may be close. (Telegraph)

CORONAVIRUS: North East leaders will tell the Government to "sod off" if they try to impose tier three restrictions, a council boss has said as more areas look set to move into the toughest measures. (Telegraph)

BREXIT: Deep in the European Commission's Brussels headquarters, officials are plotting how to make it look like Boris Johnson is a brilliant negotiator. With talks between the U.K. and European Union still deadlocked after the British prime minister nearly-but-didn't- quite stage a walkout Friday, that's the only way EU officials say they can secure the trade deal both sides say they want. Johnson, who had been unhappy about the pace of negotiations and at the EU's repeated demands for concessions, said on Friday he would only reopen discussions if the bloc showed "some fundamental change of approach." But EU officials, and senior diplomats from Europe's biggest capitals, say they are relaxed about the U.K.'s posturing, which they say they recognize is necessary for Johnson to be able to sell a compromise to euro-skeptics at home. One official described the current standoff as theatrics. Another called Friday's statement an expected and artificial provocation. (BBG)

BREXIT: U.K. business leaders were left disgruntled after a Downing Street briefing in which U.K. Cabinet Office Minister Michael Gove likened Brexit to moving house. Gove said leaving the EU will come with upfront costs but long-term benefits during a 20-minute conference call on Tuesday with senior figures from U.K. industry, according to three people present who asked not to be identified because they weren't authorized to speak publicly. (BBG)

BREXIT: Europe's car manufacturers have called on Brussels to take a less restrictive stance on future market access to the UK, warning that aspects of the bloc's current position are "not in the long-term interests of the EU automotive industry". The letter from the European Automobile Manufacturers' Association (ACEA) — a group that represents companies including BMW, Toyota and Fiat — urges Brussels to "reconsider its position" on rules for determining whether goods will qualify for tariff-free trade. (FT)

BREXIT: About half of U.K. firms are less prepared for Brexit compared to last year due to the impact of the coronavirus pandemic, a sign of Britain's vulnerability to disruption when it quits the European Union's single market and customs union at year-end. (BBG)

FISCAL:Boris Johnson's hopes of regaining the political initiative this autumn by setting out a three-year spending master plan for the rest of the parliament are set to be abandoned. Rishi Sunak, the chancellor, has told the prime minister that plans for a comprehensive review — setting out spending totals across Whitehall — should not go ahead amid the chaos of Covid-19. The issue has created tensions between the two neighbours in Downing Street and intensive negotiations have been going on over the past week, including on Tuesday night, on whether any compromise could be found. (FT)

FISCAL: Ministers have threatened to take direct control of Transport for London unless mayor Sadiq Khan accepts a package of measures including higher council tax, a much larger congestion charge zone and higher tube and bus fares in return for rescue funding. The mayor is seeking a £4.9bn settlement for the next 18 months to bail out TfL whose passenger numbers and revenues have shrunk since Covid-19 restrictions were introduced in March. The government gave an initial six-month package worth £1.6bn to the transport authority in May. (FT)

EUROPE

ECB: European Central Bank President Christine Lagarde said the unexpectedly early pickup in coronavirus infections is a "clear risk" to the economic outlook, in a sign that policy makers are gearing up for more monetary stimulus. "Most scientists in the euro zone were expecting the resurgence of the epidemic in November or December, with the cold," Lagarde said in a pre-recorded interview with France's LCI on Tuesday evening. "It's come earlier, and from that point of view that has surprised. It's not a good omen." (BBG)

ITALY: Italy's southern Campania region said on Tuesday it planned to introduce a nighttime curfew from the weekend, while other areas started drawing up their own restrictions to tackle a surge in COVID-19 cases. (RTRS)

U.S.

FED: MNI POLICY: Fed's Evans: No Urgency to Ramp Up QE Now

- Stepping up asset purchases will have a limited effect on already-low borrowing costs now, but the Fed could consider offering further accommodation later in the recovery, Federal Reserve Bank of Chicago President Charles Evans told reporters Tuesday - on MNI Policy Main Wire and email now - for more details please contact sales@marketnews.com.

FED: The Federal Reserve's actions to unfreeze credit markets had a significant effect on the corporate bond market, despite a small footprint, and the central bank would take a flexible approach to providing more support if needed, a senior New York Fed official said on Tuesday. (RTRS)

FED: Kent Hiteshew, one of the architects of the Federal Reserve's intervention into the municipal-bond market, said it's too soon to say whether an extension of the central bank's lending facility for state and local governments will be necessary. (BBG)

FED: The U.S. Treasury Department opposes extending the Federal Reserve's $500 billion municipal lending program beyond the end of 2020 or easing the costly terms that have left it virtually unused. (BBG)

FISCAL: The White House has boosted its fiscal-stimulus offer in negotiations with Democrats, and House Speaker Speaker Nancy Pelosi said she's hopeful for a deal this week. "Everybody is working real hard" to get an agreement by the weekend, White House Chief of Staff Mark Meadows said on CNBC, saying he had just spoken with Steven Mnuchin following the Treasury secretary's latest call with Pelosi. The administration's offer is now $1.88 trillion, he said. Pelosi, who has pushed for $2.2 trillion along with a number of requirements for how the money should be deployed, told reporters that she's still in hope of agreement this week. "That's the plan. That's what I would hope so, let me say that." (BBG)

FISCAL: White House chief of staff Mark Meadows outlined the state of talks following a 45-minute conversation between House Speaker Nancy Pelosi and Treasury Secretary Steven Mnuchin. He told CNBC the sides have made "good progress" but "still have a ways to go" to strike an agreement. Pelosi and Mnuchin plan to speak again Wednesday. "I would think that those discussions hopefully would make progress again tomorrow and perhaps the following day," Meadows said, adding that he hopes to see "some kind of agreement before the weekend." (CNBC)

FISCAL: Senate Majority Leader Mitch McConnell (R-Ky.) said on Tuesday that if the White House and House Speaker Nancy Pelosi (D-Calif.) reach a deal on coronavirus relief he would bring the agreement up for a vote on the Senate floor. McConnell had previously stopped short of explicitly saying an agreement would get a vote amid widespread opposition from Senate Republicans to a package with a large price tag. "If a presidentially supported bill clears the House at some point we'll bring it to the floor," McConnell told reporters during a weekly press conference. However, McConnell did not commit to a vote before the Nov. 3 election, which is roughly two weeks away. (The Hill)

FISCAL: Senate Majority Leader Mitch McConnell (R-Ky.) told Senate Republicans on Tuesday that he has warned the White House not to make a big stimulus deal before the election, according to two people familiar with his remarks. McConnell suggested that House Speaker Nancy Pelosi (D-Calif.) is not negotiating in good faith with Treasury Secretary Steven Mnuchin, and any deal they reach could disrupt the Senate's plans to confirm Amy Coney Barrett to the Supreme Court next week. (Washington Post)

FISCAL: Five Senate Democrats joined Republicans Tuesday in a vote on extending small-business Paycheck Protection Program loans without a broader COVID-19 stimulus deal. The defections bring Republicans in the Senate within striking distance of 60 votes needed to pass legislation, though House Speaker Nancy Pelosi (D-Calif.) insists on a larger package. In a "show" vote called by Senate Majority Leader Mitch McConnell, the five Democrats broke with party leaders giving a 57-40 division in favor of McConnell's preference for smaller bills. (New York Post)

CORONAVIRUS: The number of current coronavirus hospitalisations in the US topped 39,000 for the first time in two months on Tuesday, while infections rose by more than 60,000 for the first time in several days, reflecting the wider spread of the virus through the Midwest. (FT)

CORONAVIRUS: San Francisco plans to ease more of its coronavirus restrictions placed on businesses, including reopening non-essential office spaces and indoor rock-climbing centers, Mayor London Breed announced. (CNBC)

POLITICS: With two weeks until Election Day, more than 34 million Americans have already voted in the 2020 presidential election, according to U.S. Elections Project data Tuesday. Votes cast by mail and in person this election cycle have now reached 24.5% of the more than 136 million total ballots cast in the 2016 presidential election. By Oct. 23, 2016, only 5.9 million Americans had voted early. (CNBC)

POLITICS: A shift against President Trump among white college-educated voters in Georgia has imperiled Republicans up and down the ballot, according to a New York Times/Siena College poll released Tuesday, as Republicans find themselves deadlocked or trailing in Senate races where their party was once considered the favorite. In the presidential race, Joseph R. Biden Jr. and Mr. Trump were tied at 45 percent among likely voters, unchanged from a Times/Siena poll last month. (New York Times)

POLITICS: President Trump trails Democrat Joe Biden by five points in Pennsylvania, a state that was key to Trump's election in 2016. A new Rasmussen Reports telephone and online survey of Likely Voters in Pennsylvania finds Biden leading Trump 50% to 45%. Two percent (2%) prefer some other candidate, and three percent (3%) remain undecided. Factor in those who haven't made up their minds yet but are leaning toward one candidate or the other, and Biden leads 50% to 47%. (Rasmussen)

POLITICS: Republican Senator Thom Tillis of North Carolina pulled even with his Democratic challenger, and in Michigan, the Republican candidate for a U.S. Senate seat cut into the Democratic incumbent's lead, Reuters/Ipsos polls showed on Tuesday. (RTRS)

POLITICS: The Senate will vote to confirm Judge Amy Coney Barrett to the Supreme Court next Monday, Oct. 26, Majority Leader Mitch McConnell (R-Ky.) announced Tuesday. (Axios)

EQUITIES: More antitrust cases are likely to be filed against Alphabet Inc.'s Google soon by state attorneys general, even though partisan-tinged wrangling has clouded the path forward. At least two separate though overlapping groups of attorneys general are investigating the company concurrently. One effort, led by Texas Attorney General Ken Paxton, a Republican, focuses on online advertising and could lead to a lawsuit being filed within weeks, according to people familiar with the situation. (WSJ)

EQUITIES: Google and Alphabet CEO Sundar Pichai and the company's top lawyer, Kent Walker, urged employees to keep their heads down amid the Department of Justice's high-profile antitrust lawsuit, according to separate emails to employees Tuesday. (CNBC)

OTHER

GLOBAL TRADE: Chinese technology companies including Huawei Technologies Co. have expressed strong concerns to local regulators about Nvidia Corp.'s proposed acquisition of Arm Ltd., people familiar with the matter said, potentially jeopardizing the $40 billion semiconductor deal. Several of the country's most influential tech firms have been lobbying the State Administration for Market Regulation to either reject the transaction or impose conditions to ensure their access to Arm technology, the people said. Chief among their concerns is that Nvidia may force the British firm to cut off Chinese clients, they said, asking not to be identified discussing private deliberations. (BBG)

GLOBAL TRADE: Brussels should intervene and block the acquisition of Britain's tech jewel ARM by U.S. chip giant Nvidia, according to Peter Mandelson, a former EU trade commissioner and former U.K. business minister. Mandelson argued that Brexit should play no role in the EU's calculus and sent a letter to European Commission President Ursula von der Leyen in which he mapped out what he saw as the broader strategic importance of keeping ARM within a European commercial eco-system. (Politico)

GLOBAL TRADE: Valdis Dombrovskis rejected an offer made by U.S. Trade Representative Robert Lighthizer, who suggested the U.S. would scrap punitive tariffs if Airbus repaid aid to European governments, Sueddeutsche Zeitung writes, citing an interview with the EU's Economy Commissioner. (BBG)

GLOBAL TRADE: Britain and the United States are intensifying trade talks, trade minister Liz Truss said on Tuesday, announcing the start of a fifth round of negotiations focused on goods tariffs. (RTRS)

GLOBAL TRADE: The U.S. Department of Commerce will investigate aluminum foil imported from Armenia, Brazil, Oman, Russia and Turkey for potential dumping or unfair subsidies, it said in a statement on Tuesday. The department said it would take up the probe following a petition from an industry trade group as well as three of its member companies. (RTRS)

GEOPOLITICS: The French and Russian Presidents Emmanuel Macron and Vladimir Putin agreed to pursue efforts as part of the so-called Minsk group to enforce a ceasefire in the disputed territory of Nagorno-Karabakh, Macron's office says in a statement following a phone call between the two leaders. (BBG)

CORONAVIRUS: AstraZeneca's COVID-19 vaccine trial in the United States is expected to resume as early as this week after the U.S. Food and Drug Administration completed its review of a serious illness, four sources told Reuters. AstraZeneca's large, late-stage U.S. trial has been on hold since Sept. 6, after a participant in the company's UK trial fell ill with what was suspected to be a rare spinal inflammatory disorder called transverse myelitis. The sources, who were briefed on the matter but asked to remain anonymous, said they have been told the trial could resume later this week. It was unclear how the FDA would characterize the illness, they said. (RTRS)

CORONAVIRUS: In an Oct. 2 memo, Food and Drug Administration compliance officers wrote that findings from an inspection of Lilly's New Jersey facility in July and August "support a major failure of quality assurance." They noted that Lilly planned to make its antibody therapy at the plant and said the inspection group "feels it is still imperative that FDA take action." The assessment was based on a four-week site inspection that ended on Aug. 21, the details of which haven't previously been reported. (BBG)

HONG KONG: Hong Kong-based banks have been told to report any transactions that they believe may violate the national security law, in new advice from the financial regulator. (BBG)

BOJ: MNI POLICY: BOJ Sakurai: Prepare For Contingency; Act Swiftly

- The Bank of Japan should conduct additional easing policy swiftly and in an appropriate manner if needed, while maintaining cooperation with the government and major central banks, BOJ board member Makoto Sakurai said on Wednesday - on MNI Policy Main Wire and email now - for more details please contact sales@marketnews.com.

NEW ZEALAND/RATINGS: Labour's victory in New Zealand's election on 17 October will give the party unprecedented control over the government's policy direction, says Fitch Ratings. This reinforces our expectation that the administration in its second term will maintain a commitment to prudent fiscal management and rebuilding fiscal buffers over the longer term following the coronavirus shock. The long-term trajectory of public debt will be key to our assessment of New Zealand's sovereign rating. (Fitch)

TAIWAN: Taiwan plans to expand reserve force to about 268,000 soldiers from about 210,000 soldiers currently, Apple Daily reports, citing Defense Ministry's report to lawmakers. (BBG)

RUSSIA: New satellite images obtained by CNN indicate Russia is preparing to resume test flights of its nuclear-powered cruise missile at a previously-dismantled launch site near the Arctic Circle, according to experts who have analyzed the photos. (CNN)

SOUTH AFRICA: As South Africa revises its legal framework to make it easier to take property without paying for it, the nation's land minister has given assurances that the contentious process won't degenerate into a free-for-all. The ruling African National Congress decided in December 2017 to change the constitution to explicitly allow for expropriation without compensation. Lawmakers have been deliberating since then how the changes should be effected. The government this month published a revised version of its Expropriation Bill that's been in the works since 2008 and specifies which property can be taken -- including land held for speculative purposes or owned by absent landlords. (BBG)

ARGENTINA: Argentina's program with the International Monetary Fund will include measures that address the country's fundamental problems, Economy Minister Martin Guzman said in a written response to questions emailed by Bloomberg News. "We also aim at including structural measures that address the fundamental problems of the country that result in patterns of instability and exclusion". (BBG)

CHINA

PBOC: The PBOC is likely to use open market operations while shunning RRR cuts to maintain liquidity and interest rates at a stable level, the Shanghai Securities News said citing Wen Bin, a researcher from China Minsheng Bank. The PBOC left LPRs unchanged for the sixth month as the strengthening economy forestalled looser policies, the newspaper reported citing comments by Wang Qin, the macro-analyst from Golden Credit Rating. Future fiscal expenditures will improve the liquidity and reduced structured deposits will help banks cut debt costs and push for a decrease in real loan interest rates, Wen said. (MNI)

YUAN: The PBOC's countercyclical move to remove forex dealers' risk reserves has failed to tame the appreciation of the yuan as global capital picked up the pace of acquiring Chinese assets, the 21st Century Business Herald reported citing analysts. The bullishness has been driven by expectations of easing Sino-U.S. tensions and the rapid recovery of the Chinese economy, the newspaper said citing Zhao Yaoting, global market strategist at Invesco Asia Pacific. Many investors also noted the PBOC made no new measures to counter the yuan's rise, the newspaper said citing an unidentified hedge fund manager. Onshore yuan hovered around 6.6800 against the dollar yesterday after touching the highest this year of 6.6784, the Herald said. (MNI)

ECONOMY: The Chinese economy will probably continue expanding at a roughly 5% annual clip over the next 15 years, an adviser to President Xi Jinping told Nikkei, citing a rapidly developing technology sector. (Nikkei)

ECONOMY: China is "fully capable" of keeping its economy growing at 5% to 6% each year during 2021-2025 under the government's 14th Five Year Plan as the resilient economy and strong industrial structure overcomes the pandemic, the 21st Business Herald reported on Wednesday citing Peng Sen, the chairman of the China Society of Economic Reform and a former NDRC vice chairman. China will focus on reform of market elements such as land, labor and capital to ensure high quality of growth rather than focusing purely on the rate, Peng said. (MNI)

OVERNIGHT DATA

AUSTRALIA SEP WESTPAC LEADING INDEX +0.22% M/M; AUG +0.50%

Momentum continues to show a significant improvement consistent with the Australian economy moving out of recession. Westpac expects that growth in both the September and December quarters will be clearly in positive territory, as the Australian economy opens up. We have also revised up our growth forecasts for 2021 and 2022 following the announcement of the Federal Budget. Consistent with the steady progression in the leading Index we expect growth of 2.8% in 2021 and 3.5% in 2022. Key factors behind this stronger profile are a boost to consumer demand, as households spend around 50% of the personal tax cuts, and a lift in business investment in response to the accelerated depreciation allowances. We are disturbed by the government's forecasts that population growth will fall to 0.2% in 2020/21 and 0.4% in 2021/22, reflecting negative net migration in both years. In time, perhaps a more progressive approach to dealing with foreign borders will allow a faster return to normal net migration flows. (Westpac)

NEW ZEALAND SEP CREDIT CARD SPENDING -9.9% Y/Y; AUG -11.8%

NEW ZEALAND SEP CREDIT CARD SPENDING +1.0% M/M; AUG -5.6%

SOUTH KOREA OCT 1-20 EXPORTS -5.8% Y/Y; SEP +3.6%

SOUTH KOREA OCT 1-20 IMPORTS -2.8% Y/Y; SEP -6.8%

SOUTH KOREA SEP PPI -0.4% Y/Y; AUG -0.5%

CHINA MARKETS

PBOC NET INJECTS CY80BN VIA OMOS

The People's Bank of China (PBOC) injected CNY80 billion via 7-day reverse repos with the rate unchanged on Wednesday. This resulted in a net injection of CNY80 billion as no reverse repos matured, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) fell to 2.2000% at 09:20 am local time from the close of 2.3046% on Tuesday: Wind Information.

- The CFETS-NEX money-market sentiment index closed at 35 on Tuesday vs 49 on Monday. A lower index indicates decreased market expectations for tighter liquidity.

MARKETS

SNAPSHOT: Still Marching To The Beat Of The Fiscal Drum

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 up 102.06 points at 23669.78

- ASX 200 up 12.621 points at 6197.2

- Shanghai Comp. down 11.748 points at 3316.355

- JGB 10-Yr future down 16 ticks at 151.97, yield up 0.8bp at 0.030%

- Aussie 10-Yr future down 5.0 ticks at 99.190, yield up 4.5bp at 0.803%

- U.S. 10-Yr future -0-06 at 138-16+, yield up 3.35bp at 0.819%

- WTI crude down $0.24 at $41.46, Gold up $10.9 at $1917.89

- USD/JPY down 18 pips at Y105.32

- WHITE HOUSE UPS STIMULUS OFFER, PELOSI HOPEFUL ON DEAL THIS WEEK (BBG)

- MCCONNELL WARNS WHITE HOUSE AGAINST STIMULUS DEAL PRE-ELECTION (W POST)

- FED'S EVANS: NO URGENCY TO RAMP UP QE NOW (MNI)

- HUAWEI, CHINA FIRMS ARE SAID TO SEEK CURBS ON NVIDIA'S ARM DEAL

- ASTRAZENECA U.S. VACCINE TRIAL EXP. TO RESUME AS EARLY AS THIS WEEK (RTRS SOURCES)

BOND SUMMARY: Steeper, U.S. Yield Range Breaks Eyed

Participants seemingly chose to focus on the prospect of a U.S. fiscal deal, as opposed to when it may occur, even after apparent pushback from Senate majority leader McConnell re: a pre-election pact on Tuesday. This, coupled with some concession ahead of today's 20-Year Tsy supply, allowed some curve steepening in Asia-Pac hours, with 10- & 30-Year yields pushing through their respective recent highs. A clean, sustained break here would allow participants to focus on the June highs in both metrics. T-Notes are running on above average volume, last -0-06 at 138-16+.

- JGB futures were also lower, in line with the broader tone, last -15 ticks, with the acceleration in the move in Tsys and upticks in the offer to cover ratios in 1-5 Year BoJ Rinban ops eyed. Cash JGBS generally cheapened, with the long end lagging. There were signs of receiving in the longer end of the swap curve during Tokyo morning trade, although that faded in the afternoon.

- Long positioning on the back of the prospect of imminent RBA easing likely added to the pressure seen in the Aussie Bond space, as some of the weaker XM longs folded on the downtick that was driven by the U.S. Tsy market, with YM -0.5 and XM -5.0 as we type. There was little else to really note for the space today, outside of the all-time low in the 3-month BBSW fixing that we flagged earlier and yet another strong ACGB auction.

BOJ: Rinban Sizes Unchanged

The BoJ offers to buy a total of Y1.22tn of JGB's from the market, sizes unchanged from previous operations:

- Y420bn worth of JGBs with 1-3 Years until maturity

- Y350bn worth of JGBs with 3-5 Years until maturity

- Y420bn worth of JGBs with 5-10 Years until maturity

- Y30bn worth of JGBis

AUSSIE BONDS: The AOFM sells A$2.0bn of the 1.0% 21 Dec '30 Bond, issue #TB160:

The Australian Office of Financial Management (AOFM) sells A$2.0bn of the 1.0% 21 December 2030 Bond, issue #TB160:- Average Yield: 0.7672% (prev. 0.8500%)

- High Yield: 0.7675% (prev. 0.8500%)

- Bid/Cover: 6.3665x (prev. 4.1525x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 60.6% (prev. 100.0%)

- bidders 49 (prev. 52), successful 12 (prev. 1), allocated in full 2 (prev. 1)

EQUITIES: Focus On DC

The fiscal impetus from DC and spill over from Wall St. trade supported broader risk appetite in Asia-Pac hours, even in the wake of the late Tuesday fade for equities after Senate majority leader McConnell limited the prospects for a pre-election fiscal pact. Still, e-minis traded shy of their respective Tuesday highs during Asia-Pac hours.

- Chinese mainland equities were the exception to the broader rule, although there was little in the way of notable macro headline flow to drive the move, outside of guidance of 5-6% Chinese GDP growth for the foreseeable futures (per separate comments from an advisor to President Xi and a former state planning body official). This would represent a lower growth clip than we have become accustomed to, although such growth would be more than healthy, with slowing expected as the Chinese economy evolves.

- Nikkei 225 +0.5%, Hang Seng +0.7%, CSI 300 -0.5%, ASX 200 +0.1%.

- S&P 500 futures +20, DJIA futures +143, NASDAQ 100 futures +71.

OIL: Off API-Induced Lows

WTI & Brent sit ~$0.15 below their respective settlement levels at typing, unwinding some of their API-induced post settlement weakness, aided by a weaker US$ and uptick in e-minis during overnight dealing. Reports suggested that this week's API reading revealed a surprise build in headline crude stocks, a larger than exp. drawdown in distillates, a roughly in line with exp. drawdown in gasoline stocks and a build at the Cushing hub.

- This comes after the benchmarks added ~$0.55-0.65 come Tuesday's settlement, supported by the U.S. fiscal dynamic (with focus on a deal being struck, as opposed to when). There was also some speculation (via source reports) that Russia could support an extension of a pact to uphold the current OPEC+ production levels beyond the end of '20, with Russian Energy Minister Novak subsequently stressing that "it is too early to talk about the future of the OPEC+ deal beyond December."

- Weekly DoE inventory data is due to be released on Wednesday.

GOLD: DXY Downtick Supports

USD weakness has been the supporting factor over the last 12 or so hours, aided by increased prospects of a fiscal deal in DC, despite some apparent pushback from Senate majority leader McConnell re: the prospects of a pre-election deal. The broader USD downtick has supported bullion, nullifying any impact from U.S. Tsy yields, although spot still hasn't challenged the first technical resistance line at $1,933.3/oz (the Oct 12 high and bull trigger), last dealing +$12/oz at $1,919/oz.

FOREX: Risk-On Flows Dent Greenback, CNH & KRW Print Fresh Cycle Highs

Some optimistic signals on U.S. fiscal front and a spillover from Wall Street supported risk appetite, generating risk-on flows across G10 FX space. There was little in the way of fresh headline/data catalysts, with U.S. stimulus talks still taking centre stage. Commodity-tied FX picked up a bid, while safe havens lagged. The greenback underperformed all of its peers from the basket, with the DXY registering a one-month low.

- Greenback weakness helped some USD/Asia crosses fall to fresh cycle lows. USD/CNH sank through the CNH6.65 mark to its worst levels since Jul 2018 and a softer than expected PBoC fix failed to arrest the move. USD/KRW dipped to levels not seen since Apr 2019, as a continued recovery in South Korea's daily average exports bolstered the won, rendering it the best performer in the region.

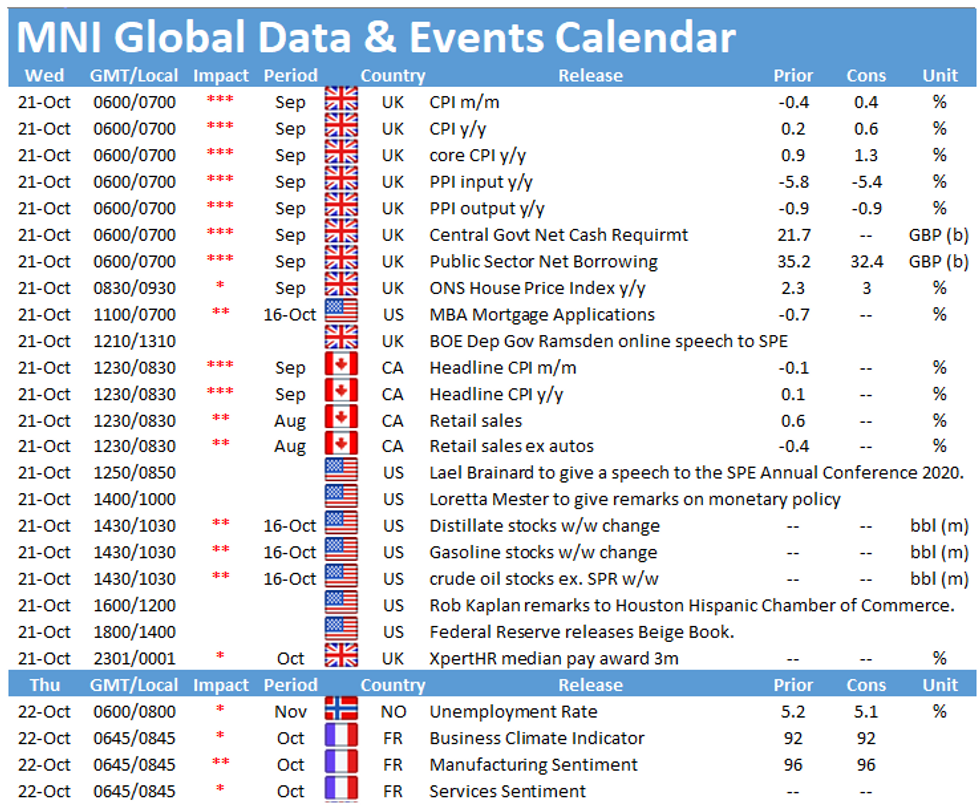

- On the radar today we have UK & Canadian inflation data, Canadian retail sales and comments from Fed's Mester, Kashkari, Kaplan, Barkin, Quarles & Bullard, ECB's Lagarde, de Guindos & Lane and BoE's Ramsden.

FOREX OPTIONS: Expiries for Oct21 NY cut 1000ET (Source DTCC):

- EUR/USD: $1.1750-65(E851mln), $1.1800(E947mln), $1.1850-60(E662mln), $1.2000(E506mln)

- USD/JPY: Y105.00-10($1.9bln), Y105.45-50($1.5bln), Y105.90-106.00($2.4bln), Y106.65($1.0bln)

- EUR/GBP: Gbp0.9165-75(E520mln), Gbp0.9350(E578mln-EUR calls)

- AUD/USD: $0.6900(A$847mln), $0.7220(A$598mln), $0.7600(A$1.1bln)

- USD/CAD: C$1.3000($800mln-USD puts)

- USD/CNY: Cny6.7000($500mln)

UP TODAY (Time GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.