Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Familiar areas of risk, and in some case a lack in movement surrounding them, made for a cautious round of Asia-Pac trade. Equity markets were mixed.

- Bond bulls test technical levels in U.S. 10-Year Yields & T-Notes.

- Today's ECB meeting is widely expected to be a low-risk event. The mid-quarter setting (with an absence of fresh macroeconomic projections), the stabilisation in sovereign bond markets following the earlier sell-off, and lack of clarity on the near-term economic direction, suggest that the GC will be content with standing on the side lines for now. Nonetheless, competing views on the economic trajectory and the lifespan of PEPP are starting to emerge, which could come into sharper focus by the time of the June meeting.

BOND SUMMARY: Core FI Firms On Several Risk Negative Matters

Core FI firmed overnight with the U.S. fiscal impasse, suggestions that the U.S.-Iranian talks may not be quite as advanced as some have suggested (per BBG sources), news that a Syrian missile fell near an Israeli nuclear site (triggering a retaliatory attack) & the COVID situation in India all noted in Asia-Pac hours.

- Bulls were not able to overcome technical resistance in T-Notes, in the form of the 50-day EMA, with that contract now 0-01+ off highs, printing +0-06 at 132-23. Meanwhile, cash trade saw the recent low in 10-Year yields hold firm, although that benchmark continues to trade below its 50-DMA (after breaching that metric for the first time since November). The curve has bull flattened, with 10+-Year paper sitting 2.5bp richer on the day. Regional participants have seemingly used the uptick to initiate downside plays/hedges, with 20.0K TYM1 131.50/130.50 put spreads lifted on block (after 20.0K TYM1 131.00/130.00 put spreads were lifted on block during Asia-Pac trade earlier this week), and 5.0K FVM1 122.25 puts lifted on screen, although the former may have represented a position rejig. 5-Year TIPS supply, the end-of-month Tsy auction announcement and weekly jobless claims data headline locally on Thursday.

- JGB futures have latched onto the broader bid in the core FI space, with a continued sprinkling of worry re: the local COVID situation still proving to be a supportive factor. Futures +5 last, back from highs, but more than reversing the modest overnight losses, with the 7-Year zone of the cash curve outperforming, richening by 1.5bp on the day as of typing. 20+-Year swap spreads are tighter once again. The formal decision re: the declaration of COVID-related states of emergency in Tokyo, Kyoto, Hyogo and Osaka is set to come on Friday (the government is expected to give the OK to the requests of the respective regional governments). National CPI & flash PMI data will also hit on Friday.

- The bid in U.S. Tsys dragged the Aussie bond space flatter (which may have been aided by the A$4.4bn+ round of coupon payments in the ACGB space, paid yesterday), leaving YM -0.5 and XM +3.0 at typing. Little to note on the local front, with the RBA delivering the scheduled round of ACGB purchases. A$800mn of ACGB 3.25% 21 April 2025 supply and the release of the AOFM's weekly issuance schedule headline locally on Friday, with flash PMI data also due.

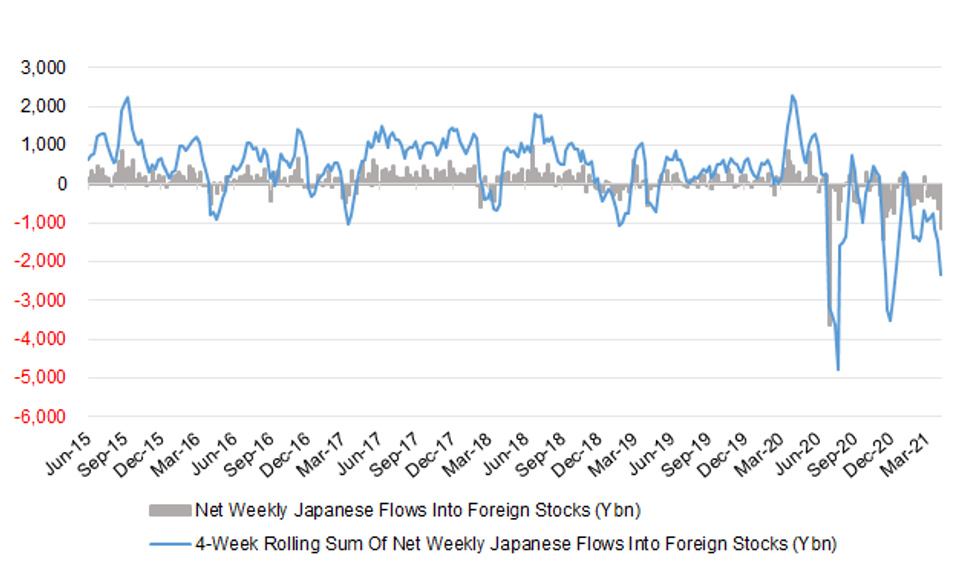

JAPAN: Familiar International Flows Apparent

A quick look at the latest round of weekly Japanese international security flow data revealed that Japanese participants stuck to familiar net flow patterns, i.e. net selling of foreign equities & net buying of foreign bonds, for a fifth consecutive week. While some of this no doubt represents portfolio rebalancing, the net amount of foreign bond purchases exceeds the net amount of foreign equity sales over that time period (to the tune of ~Y1.144tn), which would suggest that some Japanese participants have started to take advantage of the pick ups offered by some of the major offshore global FI markets (we have flagged areas of appeal, in both FX-hedged and -unhedged terms in recent weeks).

- We should also note that the sample week represented the largest weekly round of Japanese net selling of foreign equities witnessed since November.

- On the other side of the ledger, foreign investors remained net buyers of Japanese bonds and equities in the most recent week, although the net buying moderated across both categories.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | 906.5 | 1715.5 | 3198.4 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | -1145.1 | -622.5 | -2334.5 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 353.2 | 1226.5 | -240.2 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 286.3 | 641.1 | 1052.6 |

Source: MNI - Market News/Bloomberg/Japanese Ministry Of Finance

FOREX: Kiwi Goes Offered In Quiet Asia-Pac Trade

NZD helped bring up the rear in G10 basket. Lacklustre news flow made it hard to pin the kiwi's weakness on any fundamental catalyst, but a BBG trader source flagged NZD sales against its Antipodean cousin, with AUD/NZD seemingly forming a base around its 200-DMA.

- The DXY extended yesterday's losses, even as the three e-mini contracts edged lower in Asia. The greenback's weakness may have been related to a slide in USD/CNH, which extended its current losing streak to nine straight days.

- The redback continued to appreciate even as the PBOC set its central USD/CNY mid-point at CNY6.4902, 8 pips above sell-side estimates.

- CAD continued to grind away from yesterday's post-BoC highs in narrow Asia-Pac trade.

- The ECB's latest monetary policy decision and U.S. initial jobless claims provide the main points of note today.

FOREX OPTIONS: Expiries for Apr22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800(E969mln), $1.1900-10(E1.3bln), $1.1975-87(E923mln-EUR puts), $1.2045-50(E558mln-EUR puts)

- USD/JPY: Y108.00-05($1.8bln), Y108.30-40($2.6bln-USD puts), Y108.50-55($505mln), Y108.65-75($801mln-USD puts), Y109.00($693mln), Y109.90-110.00($1.1bln)

- EUR/GBP: Gbp0.8550(E580mln)

- USD/CHF: Chf0.9175($495mln)

- EUR/CHF: Chf1.1050-55(E490mln-EUR puts)

- AUD/USD: $0.7500(A$713mln), $0.7750(A$595mln-AUD puts)

- AUD/JPY: Y83.05-15(A$514mln)

- EUR/AUD: A$1.5525(E443mln-EUR puts)

- NZD/USD: $0.7060(N$917mln-NZD puts), $0.7090(N$942mln-NZD puts)

ASIA FX: Gains As US Yields Decline

US yields declined which kept USD on the back foot, while positive risk sentiment also helped support Asia EM FX.

- CNH: Offshore yuan gained, USD/CNH dropping after the PBOC set USD/CNY mid-point at 6.4902, 144 pips below yesterday's fix, but 8 pips above sell side estimates. This is the first fix below 6.50 since March 18.

- SGD: Singapore dollar stronger, there were reports that Singapore and Hong Kong have delayed the travel bubble announcement. USD/SGD was unconcerned with the announcement

- TWD: Taiwan dollar strengthened after weakening into the close yesterday. USD/TWD is off session lows, with chatter that with the central bank hamstrung after warnings from the US Tsy the CBC enlisted state-owned lenders to purchase the greenback in order to defend the 28.00 handle

- KRW: Won is stronger, moves somewhat muted as the number of coronavirus cases picks up again.

- MYR: Ringgit is higher. Palm oil futures extended their rally, showing at levels not seen sine 2008.

- IDR: Rupiah is stronger, moves muted compared to peers. With little of note on the local data docket, focus turns to a press briefing with FinMin Indrawati, who will provide an update on 2021 state budget at 0700BST/1400HKT.

- PHP: Peso has gained, concern remains over the pandemic though. The Dept of Health warned that hospitals in five regions are running out of ICU beds. The ICU utilisation rate in Manila is not at 84%. The U.S. asked its citizens to refrain from travelling to the Philippines, owing to "a very high level of COVID-19 in the country."

- THB: Baht is higher, Moody's warned that curbs imposed to constrain the third wave of coronavirus may negatively affect Thailand's economic recovery and fiscal position. Meanwhile PM Prayuth said Wednesday that the gov't wants to increase its vaccine stock by 50% to 100mn doses this year.

ASIA RATES: Bonds Mostly Higher Alongside UST's

Coronavirus concerns in the region exert effects on bond markets, while a move higher in UST's is supportive.

- INDIA: Bonds supported as INR and stocks decline, the number of coronavirus cases continues to surge, India now holds the dubious honour of reporting the highest tally of daily cases. Meanwhile New Delhi and Mumbai impose lockdowns, even as PM Modi issues plea to states to only use enact lockdowns as a last resort. Markets will await the release of the minutes from the April meeting, the main point of the meeting was the announcement of the GSAP programme, participants will parse the minutes for signs that there is still dry powder after the first round of the programme was largely ineffective.

- SOUTH KOREA: Futures higher, South Korea reported 735 new virus cases for the second straight day on Thursday amid lingering woes over another wave of the pandemic as the country's vaccination campaign gathers pace, with vaccinations set to top 2 million. Elsewhere, while foreign inflows into South Korean bonds continue the pace has slowed as the week has progressed. Yesterday saw inflows of $106.72m, down around $189m form the day before and some $350bn lower than Monday.

- CHINA: Bond futures are lower, 10-year future reversing all of yesterday's gains and extending past Tuesday's low. There are reports that China is considering a plan that would see the PBOC take on CNY 100bn of assets from China Huarong Asset Management in order to help the state-owned company clean up its balance sheet and refocus on managing distressed debt. If this did transpire it would be a clear signal of government support for firms under distress. While there is speculation China could respond to Australia after scrapping of an agreement for the state of Victoria to cooperate under the Belt and Road Initiative.

- INDONESIA: Bonds higher, the 10-year yield drops to the lowest level since mid-February. The government sold IDR 2.64tn of bonds via a greenshoe option yesterday, receiving IDR 3.41tn of bids. With little of note on the local data docket, focus turns to a press briefing with FinMin Indrawati, who will provide an update on 2021 state budget at 0700BST/1400HKT.

EQUITIES: Rebound Following Two-Days Of Declines

Risk sentiment rebounded in Asia-Pac trade on Thursday, taking a positive lead from the US. Markets in Japan lead the way higher, retracing all of yesterday's sharp decline. Markets in mainland China struggled to make significant headway, while Taiwan, South Korea and Antipodean bourses saw modest increases in a quiet session. US futures dipped slightly, markets await the ECB rate announcement while there are reports that Republicans are planning to present their counterproposal to US President Biden's infrastructure plan later today.

GOLD: $1,800/oz In View

Lower U.S. real yields and a softer DXY (on net) have combined to support bullion over the last 24 hours or so, with bulls now looking to force a break above the $1,800/oz mark to open up the way towards the Feb 25 high at $1,805.7/oz. Spot last deals little changed, just shy of the $1,795/oz mark.

OIL: Crude Futures Slip For Third Day

Oil is lower again on Thursday; WTI & Brent sit ~$0.25 below their respective settlement levels. Crude futures are on track for a third straight loss.

- Oil was pressured yesterday after the a tweet from the WSJ that the US is open to easing sanctions against Iran, while the move was exacerbated by US DOE inventory figures showed the first build in stocks in a month. Headline crude stocks rose 594k against expectations of a 3.265m bbl draw. There are also demand concerns as the coronavirus situation in India worsens, Mumbai and New Delhi have both imposed lockdowns, despite a plea from Indian PM Modi to only use lockdowns as a last resort.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.