Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

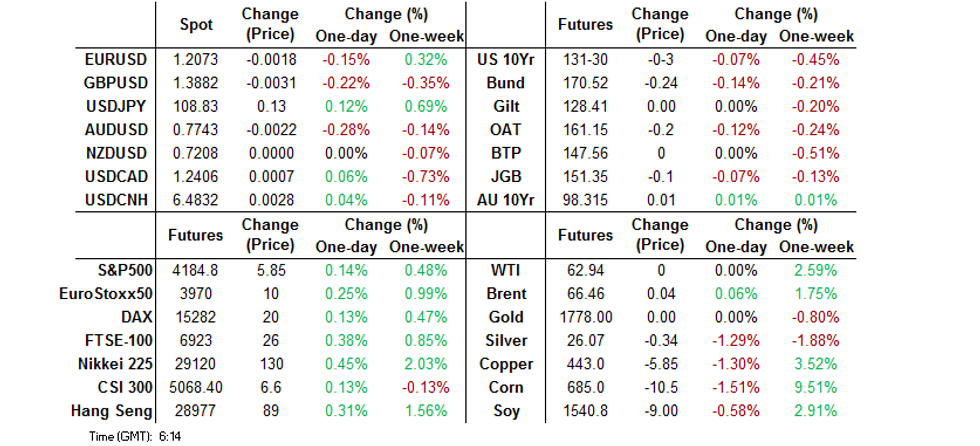

- AUD leaks lower and ACGBs outperform on the back of weaker than expected Aussie CPI data.

- Speculation continues to do the rounds re: U.S. President Biden's tax plans.

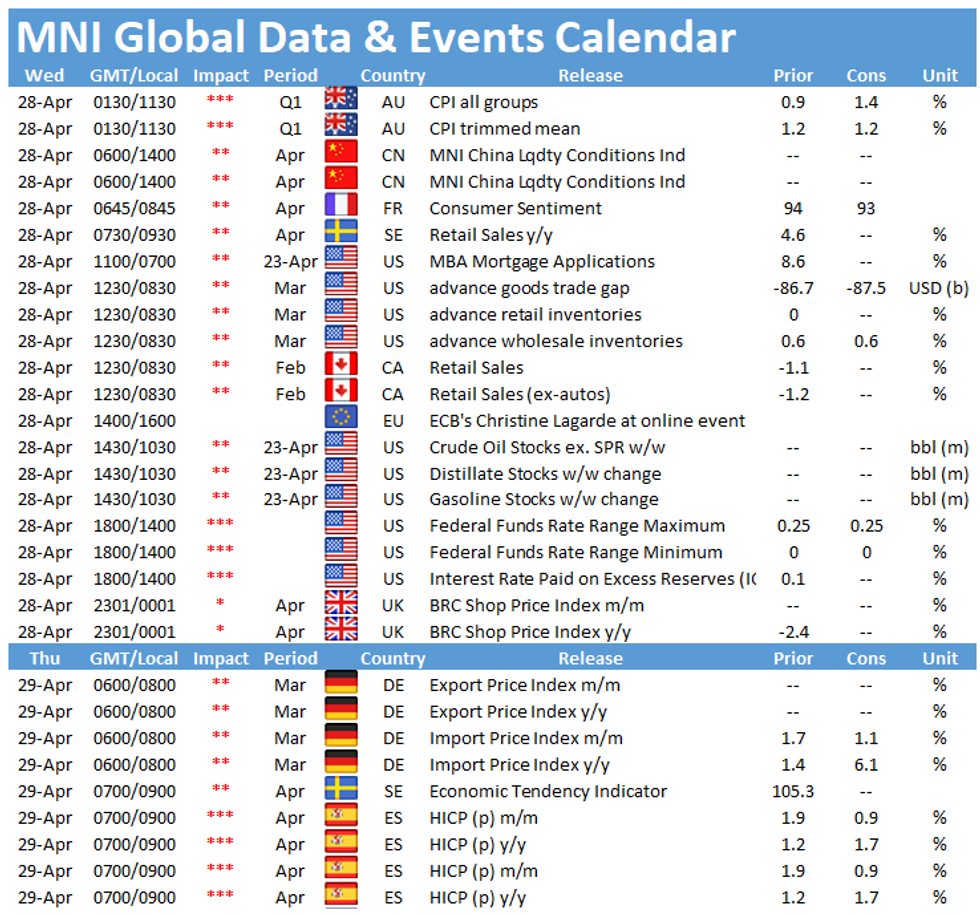

- Focus at the April FOMC will be on any changes to the statement to reflect strong incoming economic activity data, and the degree to which (if any) Powell indicates that the upcoming meetings are 'live' with regards to discussions on tapering asset purchases. Opinion is split on whether the Fed will deliver a technical change to its administered rates at this meeting, but it's doubtful that short-end rates have fallen low enough to force the central bank's hand.

BOND SUMMARY: ACGBs Firm On Soft CPI, JGB Traders Look To BoJ Rinban Schedule

T-Notes corrected from overnight lows as Aussie bonds moved higher, printing fresh session highs on the move, before moving back from best levels. The contract last trades -0-02 at 131-31, within a 0-05 range. Cash Tsy trade has seen some light twist steepening of the curve. Macro headline flow was light, with continued speculation surrounding the tax side of U.S. President Biden's fiscal plan. On the flow side we saw 10.0K of the TYM1 133.50 calls lifted at 0-09 via a block trade (we saw a 10.0K block buy of the same option at 0-24 ahead of European hours on 21 April). There was also a 2,350 block seller of UXYM1 futures. The latest FOMC decision headlines the local docket on Wednesday (please see our full preview for more on that matter).

- JGB futures added to overnight losses in Tokyo trade, last -10. Cash trade saw yields little changed to a touch higher across the curve, given the move in futures since yesterday's close. A well-received round of 2-Year JGB supply saw the tail narrow when compared to the previous auction, with the cover ratio moving higher and low price topping broader expectations. Reports from TV Asahi suggested that the Japanese government is considering raising the cap of subsidies it pays to large commercial facilities cooperating by shutting their doors during the COVID state of emergencies evident across regions of Japan. Suggestions point to this equating to Y500bn, which will be drawn from the reserve fund. A reminder that the BoJ's Rinban schedule for May will hit after hours today, with participants seemingly eying the Golden Week holiday exit. The holiday period gets underway on Thursday, although markets will be open on Friday, with the usual month end domestic data dump due. Markets will then be closed Monday through Wednesday.

- Aussie bonds firmed, paring all of their overnight/early Sydney losses in the wake of the softer than expected local Q1 CPI data. YM +2.0, XM +1.0 at typing. The ACGB Apr '24/Nov '24 yield spread has flattened by 3.5bp today and sits 6bp shy of its intraday steeps. The softer than expected Q1 CPI reading has also been the driving factor here. A reminder that this spread is often used to gauge market pricing of the chances of the RBA extending its 3-Year yield targeting measure to ACGB Nov '24 from ACGB Apr '24. Elsewhere, ~30K of IRM1 traded in the wake of the CPI print, at one price, with ~20K lifted and ~10K given. The IR strip runs unchanged to +2 through the reds. The latest round of ABS payrolls data revealed that jobs fell by 1.8% in the fortnight to 10 April. The ABS noted that "the latest fortnight included the Easter holiday period which regularly sees a seasonal fall in a range of labour market indicators, especially hours worked. These seasonal factors make it difficult to gauge any effect of the end of the JobKeeper wage subsidy on 28 March. The next fortnight of data (available on 11 May) should provide a better sense of the state of the labour market after JobKeeper. Comparisons with the same fortnight a year ago are also difficult, as nationwide pandemic restrictions were in place." Terms of trade data headlines the local docket on Thursday.

FOREX: Australian CPI Miss Pulls The Rug From Under AUD

Australia's underwhelming Q1 CPI report triggered AUD sales, as consumer prices rose just 1.1% Y/Y, missing expectations of a 1.4% increase, while the key metric of core inflation printed at the weakest level on record. The Aussie remained comfortably the worst performer in G10 FX space, even as AUD crosses edged away from respective lows, with a market contact flagging demand from exporters.

- The DXY resumed its upward drift as participants prepared for today's monetary policy decision from the FOMC & U.S. Pres Biden's first speech to the Congress.

- GBP went offered as simmering tensions between London and Brussels have overshadowed the expected ratification of the Brexit deal by MEPs, to be confirmed today.

- The PBoC set its central USD/CNY mid-point at CNY6.4853, 7 pips below sell-side estimates. USD/CNH briefly showed above yesterday's peak, but then pared the bulk of its earlier gains.

- FOMC MonPol decision & subsequent presser with Fed Chair Powell provide the main points of note today. ECB speak from Lagarde, Schnabel, Centeno & Rehn as well as flash U.S. wholesale inventories & Canadian retail sales are also due.

FOREX OPTIONS: Expiries for Apr28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1900(E2.0bln), $1.1980-85(E1.8bln-EUR puts), $1.2000(E2.6bln, E2.35bln of EUR puts), $1.2030-50(E1.5bln), $1.2080(E1.1bln), $1.2100-05(E1.4bln), $1.2125-45(E1.7bln-EUR puts), $1.2150(E823mln)

- USD/JPY: Y108.10-15($1.0bln-USD puts)

- GBP/USD: $1.4000(Gbp362mln)

- EUR/GBP: Gbp0.8550-55(E500mln)

- EUR/NOK: Nok10.00(E400mln), Nok10.08(E568mln), Nok10.29(E561mln)

- AUD/USD: $0.7700(A$516mln), $0.7720-35(A$753mln-AUD puts), $0.7800-05(A$520mln-AUD puts)

- USD/CAD: C$1.2600($1.1bln-USD puts), C$1.2800($800mln)

- USD/CNY: Cny6.60($683mln)

ASIA FX: EM Asia Pressured Ahead Of FOMC

Most Asia EM FX declines as markets await the FOMC decision later today.

- CNH: Offshore yuan weaker, but off worst levels. Asian Development Bank (ADB) released a report today that forecasted China's GDP to surge this year despite persistent uncertainties over the pandemic. A story in the FT said that China is set to report its first population decline since the People's Republic was founded in 1949. This could have significant implications for China's economy

- SGD: Singapore dollar weakened slightly, market looks ahead to the Q1 unemployment rate which is scheduled to hit today, but has no fixed time. The rate is expected to have dropped to 3.0% from 3.3% previously.

- TWD: Taiwan dollar bucks the trend, strengthening further after two consecutive closes below 28.00. A strong electronics export sector and prospect of less intervention from the central bank has given TWD bulls confidence.

- KRW: Won is weaker, reversing yesterday's post-GDP strength. In a worrying sign South Korea reported 775 daily new coronavirus cases in the past 24 hours, the highest in four days and nearing 800, and the proportion of untraceable infections hit the highest point ever amid concerns of another wave of the pandemic. Weakness was tempered by strong consumer confidence figures.

- MYR: Ringgit is weaker, Malaysia left existing curbs on interstate travel in place, extended the CMCO in Kuala Lumpur, Selangor, Sarawak, Johor and Penang through May 17 and decided to raise the level of restrictions in Sabah to CMCO from the lowest RMCO from Apr 29. Sabah's Local Gov't and Housing Min said that inter-district travel will still be allowed, based on a system of zones.

- IDR: Rupiah has fallen, little to pen on notable domestic developments, headline flow has been sparse. Kompas cited State Sec Pratikno as noting that the new Investment Ministry will not replace the Indonesia Investment Coordinating Board and Bahlil Lahadia will remain at the helm of the agency.

- PHP: Peso is on heavier footing. The Presidential Palace said that determining the next quarantine status of the NCR+ bubble will be a "difficult decision" for Pres Duterte. He is scheduled to deliver an address on the matter today, following yesterday's deliberations of the Philippine Covid-19 task force.

- THB: Baht is weaker, Thailand's main Covid-19 task force chaired by PM Prayuth meets today to consider stricter measures to arrest the spread of new Covid-19 infections. Tuesday saw the Cabinet give a nod to a temporary transfer of certain prerogatives to the PM to allow him to make swift decisions on new restrictions, as the nation scrambles to contain the deadly virus.

ASIA RATES: BoK To Purchase KRW 1tn Of Govt Securities Today

South Korean bonds drop despite BoK purchase, India continues to grapple with the pandemic, while China faces prospect of lower growth on structural issues.

- INDIA: Yields higher in early trade after dipping yesterday. The coronavirus situation continues to concern as the number of deaths approaches 200k. Market participants will scrutinize today's INR 360bn bill sale for indications of market demand for government securities, and to see if the RBI attempts to influence the sale, which could be a portent for the bond sales on Friday. The RBI announced a smaller auction calendar for Friday's sale, a total INR 260bn compared to a planned INR 320bn last week that only saw INR 220bn go ahead.

- SOUTH KOREA: Futures lower in South Korea, dropping sharply at the open after grinding out small gains yesterday. The BoK reported yesterday that it would purchase up to KRW 1tn of government securities from the market today, the BoK has previously announced it will buy KRW 5tn – KRW 7tn of bonds in the first half of the fiscal year. In a worrying sign South Korea reported 775 daily new coronavirus cases in the past 24 hours, the highest in four days and nearing 800, and the proportion of untraceable infections hit the highest point ever amid concerns of another wave of the pandemic.

- CHINA: The PBOC matched maturities with injections for the thirty seventh straight session, the last time the bank injected funds into the financial system was Feb 25. The overnight repo rate is higher on the day at 1.7717% but still below yesterday's high around 1.83%. The 7-day repo rate slightly lower at 2.1289%, back below but hovering around the PBOC's 2.20% rate. Futures are higher, 10-year future seeing the most upside while moves in 5- and 2-year futures are more muted. China Huarong Asset Management repaid an offshore bond yesterday with funds provided by Industrial & Commercial Bank of China , the nation's largest state-owned bank, according to Bloomberg reports. The moves follows a request by the financial regulator for banks to extend loans to Huarong by at least six months to help the company refinance debt.

- INDONESIA: Yields higher, moves mixed across the curve. Indonesia's bond auction yesterday drew higher demand than the previous offering in April, this was the last auction until May 25. Indonesia received bids of IDR 52.7t at the auction, up from IDR 40.2t at the previous sale.

EQUITIES: Minor Positive Moves For Most

Most Asia-Pac stocks found minor positive territory on Wednesday, after US stocks recovered from early losses to finish flat. Markets in Japan are higher, while mainland China have struggled to make decisive gains. Markets in South Korea are lower in a heavy day for earnings. Bourses in Australia are higher, earlier in the session Australia reported a CPI data that missed expectations. In the US futures are higher, the Nasdaq leading the way higher after falling behind its peers yesterday, the index lagged as Tesla and Alphabet came under pressure following earnings. Markets are focused on the FOMC rate announcement later today.

GOLD: Sticking Sticking Within The Lines

Gold has nudged lower during Asia-Pac hours, with the U.S. Tsy curve twist steepening and the DXY ticking higher. Spot last deals ~$5/oz or so softer, just above $1,770/oz. The previously flagged technical picture remains intact, with the 50-day EMA acting as initial support.

OIL: Crude Futures Oscillate Around Neutral

Oil is flat in Asia-Pac trade, with WTI & Brent hovering around neutral levels after rising yesterday.

- Participants are still digesting the news that the OPEC+ group will proceed with plans to increase supply by 2m bpd over the next three months. The group estimates that demand will rebound by 6m bpd in 2021, but were cognizant of risks from coronavirus. OPEC+ will now skip its meeting originally scheduled for today. Elsewhere, Saudi Arabia is in talks to sell a 1% stake in Aramco to "one of the leading energy companies", and could offer a secondary share offering within two years. Data yesterday showed headline crude stocks rose 4.3m bbls, while stocks in Cushing, OK rose 700k bbls. The downstream report was more bullish, distillate stocks fell 2.4m bbls, while gasoline stocks fell 1.3m bbls.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.