Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

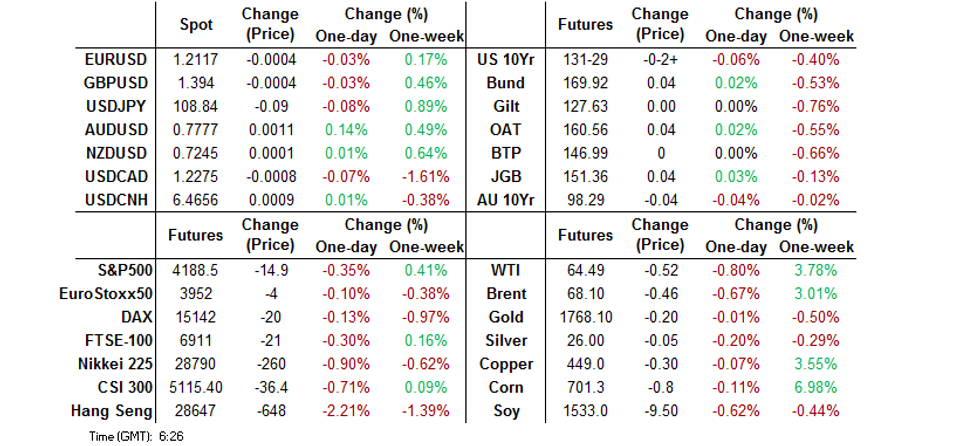

- China's continued clampdown on the fintech sector weighed on equities overnight, with the Hang Seng leading the way lower.

- Chinese PMIs were mixed, the official surveys were softer than expected, while the SME-focused Caixin manufacturing reading topped expectations (all 3 reamined in expansionary territory).

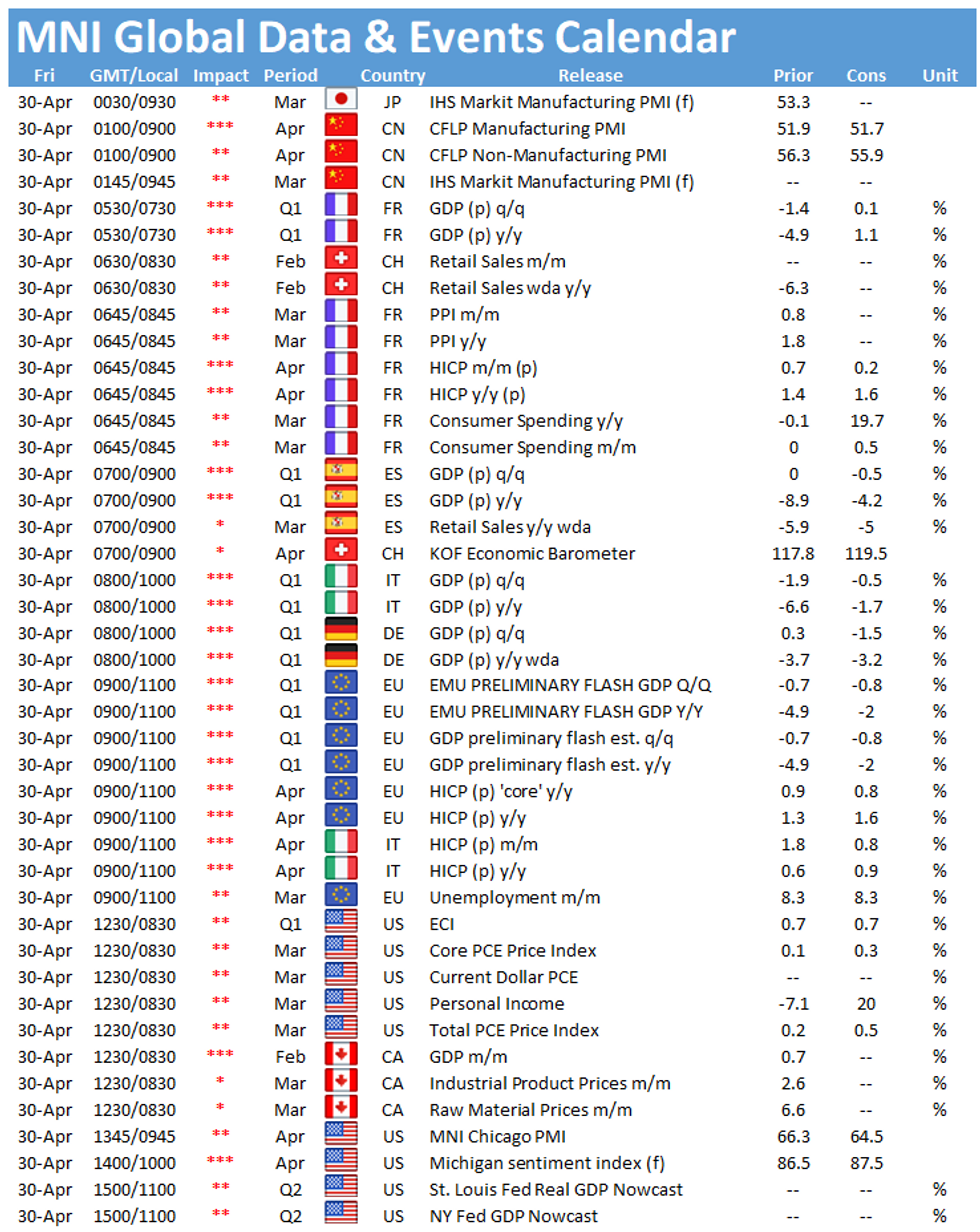

- A busy docket rounds off the week.

BOND SUMMARY: Off Worst Levels In Lackluster Trade

T-Notes have edged away from lows. Regional participants were happy to sell Tsys at the cash re-open even as e-minis ticked lower (ESM1 back below 4,200), before softer than expected official Chinese PMI data helped the space form a base. The cash Tsy market was closed during yesterday's Asia-Pac session, owing to a Japanese holiday, with the same story in play Monday through Wednesday of next week (with a Chinese market holiday also set to sap liquidity over that period). T-Notes last -0-02 at 131-29+, operating in a 0-05+ range, with recent trade seeing a 3,750 lot block seller at the current market price. The cash space trades little changed to 1.0bp cheaper across the curve.

- JGB yields traded either side of unchanged in Tokyo, with little in the way of definitive direction observed across the curve, in a session that plugs a gap between 2 holiday periods. Futures last +2 vs. the previous settlement level. Local data was mixed, with Tokyo CPI missing, while the labour market report and industrial production reading proved to be firmer than expected.

- YM -1.0, XM -3.0, a little off their respective Sydney lows, in what has been fairly limited trade. Softer than expected official Chinese PMI data helped the space find a bit of a base after what seemed to be a case of offshore-related pressure (stemming from U.S. Tsys and heavy offers in the latest RBNZ LSAP operation). Next week's AOFM issuance slate proved to be relatively vanilla. Elsewhere, The latest round of ACGB Jun '31 supply saw the weighted average yield stop 0.73bp through prevailing mids at the time of supply (per Yieldbroker pricing), meanwhile, local private sector credit growth topped exp. Month-end extension flows are eyed, given the upcoming maturity of ACGB 5.75% 15 May 2021.

JAPAN: Muted International Security Flows Seen

The latest round of weekly international security flows data revealed a moderation in 3 of the 4 categories, in what was a muted week (ending 23 April) for the dataset.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | 132.8 | 1006.3 | 3229.7 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | -318.6 | -1145.2 | -2285.2 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 123.2 | 352.7 | 2271.0 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 492.2 | 288.3 | 2399.2 |

Source: MNI - Market News/Bloomberg/Japanese Ministry Of Finance

FOREX: Chinese PMIs Provide Highlights Of Quiet Asia-Pac Session

The yuan faced some temporary headwinds as China's official PMI readings missed forecasts, but it regained poise ahead of the release of Caixin M'fing PMI, which topped expectations. USD/CNH tested yesterday's low in afternoon trade after a fresh round of sales. The PBOC set its central USD/CNY mid-point at CNY6.4672, 7 pips above sell-side estimates, with little in the way of market reaction seen after the fix.

- G10 crosses were happy to hug familiar ranges, with AUD outperforming at the margin. SEK lagged all of its peers from the basket, after bringing up the rear on Thursday.

- JPY ignored the local data deluge, despite a solid beat in flash industrial output. USD/JPY slipped over the Tokyo fix, as Gotobi Day flows failed to dictate price action, but the pair recouped most losses thereafter.

- Focus turns to GDP reports from Canada, Germany, Italy, France & EZ as well as U.S., PCE data & MNI Chicago PMI. Fed's Kaplan is due to speak.

FOREX OPTIONS: Expiries for Apr30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1950-60(E687mln), $1.2030(E734mln), $1.2050-65(E749mln), $1.2075(E676mln), $1.2100(E1.9bln-EUR puts), $1.2125(E546mln), $1.2150(E937mln)

- USD/JPY: Y108.50($837mln), Y109.25-30($715mln)

- GBP/USD: $1.3900(Gbp671mln)

- EUR/GBP: Gbp0.8600(E776mln)

- USD/CAD: C$1.2400($990mln-USD puts)

- USD/MXN: Mxn19.50($1.46bln)

ASIA FX: Peso Outperforms On Marginally Looser Restrictions, Narrower BoP Deficit

The Philippine peso led gains in tight Asia-Pac trade on the back of local drivers, with Chinese PMI figures providing the main points of note in broader Asia EM space.

- CNH: USD/CNH popped higher as Chinese official PMI readings missed expectations, generating selling pressure on the redback. The rate retraced the move even before Caixin M'fing PMI proved firmer than forecast. The PBOC set its central USD/CNY mid-point at CNY6.4672, 7 pips above sell-side estimates.

- KRW: The won turned its tail, with USD/KRW moving away from two-month lows printed yesterday. Local industrial output data provided little in the way of immediate market reaction, as a beat in the annual reading was coupled with a miss in the monthly print. Vice FinMin Lee said April CPI, due next week, will likely top the 2% target.

- PHP: The peso easily outperformed all of its regional peers as the Presidential Palace announced that some businesses will be allowed to resume operations with limited capacity, while Thursday's data showed that the Philippine BoP deficit narrowed markedly.

- THB: USD/THB failed to break under Apr 19 low of THB31.173, which would complete the formation of a double top pattern. Local Covid matters took focus, after Thailand backpedalled on its earlier decision to cut the length of mandatory quarantine and imposed fresh restrictions.

- IDR: The rupiah was rangebound, with local news flow revolving around Indonesia's plans to attract more FDI.

- MYR: USD/MYR continued to creep away from a recent cycle low, with pent up market impetus from Thursday (a market holiday in Malaysia) easily digested at the re-open.

- Markets in Taiwan & Vietnam were closed owing to local public holidays.

EQUITIES: China Fintech Pressure Weighs On Broader Equities

Equities traded on the defensive in Asia-Pac hours, although losses were generally modest. The Hang Seng was the exception to the "modest" rule, leading the way lower, shedding 1.5% as of typing, after the WSJ noted that "China is reining in the ability of the country's internet giants to use big data for lending, money-management and similar businesses, ending an era of rapid growth that authorities said posed dangers for the financial system. On Thursday, China's central bank and other regulators ordered 13 firms, including many of the biggest names in the technology sector, to adhere to much tighter regulation of their data and lending practices." U.S. e-minis also ticked lower. Participants eyed the potential for equity negative month-end rebalancing flows from funds, given the general outperformance for equities vs. bonds in the month of April (although most calculations point to fairly modest rebalancing flows, at least from a historical perspective). Softer than expected official Chinese PMI data (although still expansionary) also provided some headwinds, although the SME-focused Caixin m'fing PMI survey, also out of China, topped expectations.

GOLD: A Touch Softer

Thursday's swings in U.S. yields drove gold prices, which ultimately softened, but finished off of worst levels. Spot has nudged lower again during Asia-Pac hours, but remains comfortably away from yesterday's low, to last trade -$5/oz, just above $1,765/oz, with bears needing to force a break through key support in the form of the April 5 low ($1,721.4/oz) to turn the technical tide.

OIL: Iran Talks & Equity Downtick Apply Weight

The previously flagged downtick in the major equity indices and suggestions of progress in the U.S.-Iran talks applied light pressure to crude oil in overnight trade. WTI & Brent both print ~$0.60 lower on the day, with no let up on the demand side given the ongoing COVID issues for India.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.