Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Familiar themes i.e. the U.S. fiscal impasse and continued musings from Chinese policymakers re: regulatory crackdown in the domestic metals markets dominated headline flow in Asia.

- Cryptocurrency swings garnered most of the attention over the weekend, again.

- The Pentecost holiday will thin liquidity in European hours on Monday.

BOND SUMMARY: Core FI Generally A Touch Firmer In Asia

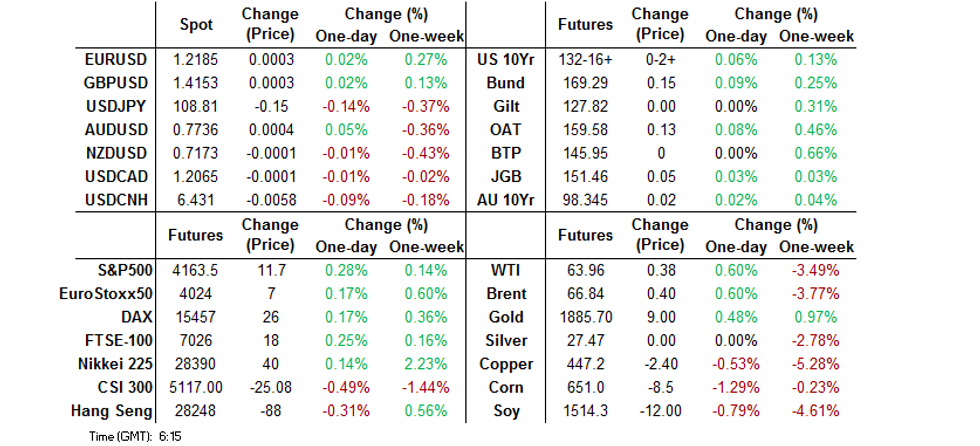

A non-committal start to the week for U.S. Tsys, with T-Notes last +0-02 at 132-16, sticking to a 0-02+ range thus far on volume of ~55K. Futures activity was supported by the quarterly rolling process, although volume was still sub-par overnight. Participants have looked through the latest round of headlines pointing to greater regulatory oversight for commodities markets in China, with authorities flagging excessive speculation as a key driver in the recent run up in domestic commodity prices, vowing a zero tolerance policy re: monopolies operating in the space (the benchmark Chinese metal futures trade ~4-7% lower on the day at typing as a result). Yields are little changed across the cash Tsy curve. The latest Chicago Fed national activity index reading & Fedspeak from Brainard, Bostic, Mester & George are set to headline during NY hours on Monday.

- JGB futures stuck to a narrow range, briefly extending on the gains lodged in the final overnight session of last week, with little to go off outside of the previously flagged potential for an extension of the state of emergency in play across various regions of Japan (which would likely bring the expiry of the restrictions in play across most regions in line with the expiry of the restrictions in the Hokkaido region). Futures last print 5 ticks above Tokyo settlement levels, with the major cash benchmarks little changed to 1.0bp richer across the JGB curve. Elsewhere, the BoJ conducted its scheduled round of 1- to 5-Year JGB purchases, leaving the purchase sizes unchanged, with no movement in the offer to cover ratios observed vs. prev. ops covering the buckets in play. Tuesday's local docket will be headlined by machine tool orders data and a liquidity enhancement auction for off-the-run JGBs with 5- to 15.5-Years until maturity.

- Aussie bond futures have ticked higher in early trading this week, with YM taking out the recent highs, last +2.0, a touch shy of best levels (after bulls forced the highest levels since liquidity moved into the M1 contract, testing the March highs on a continuation chart in the process), with short positioning (flagged back on Friday) potentially aiding the move. XM also trades +2.0, as both contracts build on their respective gains lodged back on Friday. 3-Year EFP has pushed above 10bp, printing at levels last seen back in March. We should highlight that the ACGB Apr '24/Nov '24 yield spread has narrowed to the tightest levels seen since the backend of April (last ~18.0bp), reflecting a higher probability that the RBA's 3-Year yield targeting mechanism will be rolled over to ACGB Nov '24 in July. Still, the spread only operates around the mid-point of the range witnessed since mid-March. On the supply front, we have seen SAFA launch a tap of its May '32 line, for up to A$500mn, while NBN is taking IOIs on 7-Year issuance. Tuesday's local docket is headline by ABS payrolls data and preliminary trade balance data.

US TSY FUTURES: CFTC CoT: Positioning Moves Mixed, Specs Net Short Eurodollars

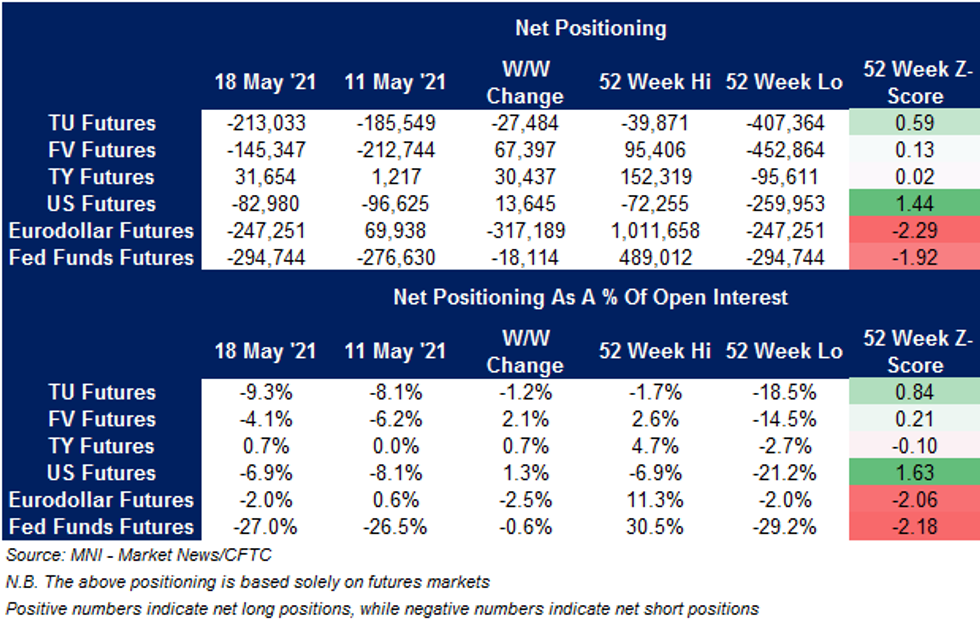

The latest CFTC CoT report revealed that changes in non-commercial net positioning across the major U.S. Tsy futures contracts were once again mixed, but fairly insignificant in terms of the broader picture.

- It was the net positioning in Eurodollar futures contracts that stole the show, flipping into net short territory for the first time since July '20, reflecting the deepest outright net short position witnessed since May '20 in the process.

FOREX: AUD Wounded By Collateral Damage From China's Commodity Talk

The Antipodeans cemented their underperformance after China's NDRC warned it will take a "zero tolerance" approach toward violations in spot and futures commodity markets, sending industrial metals tumbling. The statement by Chinese authorities represented another step in Beijing's attempts to reign in the recent rally in commodity prices. Resultant iron ore weakness undermined AUD, while NZD faltered in tandem with its Antipodean cousin, despite a beat in domestic quarterly retail sales print.

- JPY led gains in G10 pack amid sparse news flow and little in the way of notable catalysts from over the weekend. Local press reported that the gov't is planning to extend Covid-19 state of emergency in nine prefectures beyond May 31, possibly through Jun 20, which marks the expiry of emergency declaration in Okinawa.

- The PBOC set the central USD/CNY mid-point at CNY6.4408, just 3 pips above sell-side estimates. USD/CNH lost some altitude, but remained within the confines of Friday's range. Over the weekend, PBOC Vice Gov Liu said that China's central bank will maintain yuan stability, while continuing to enhance the managed floating exchange rate system.

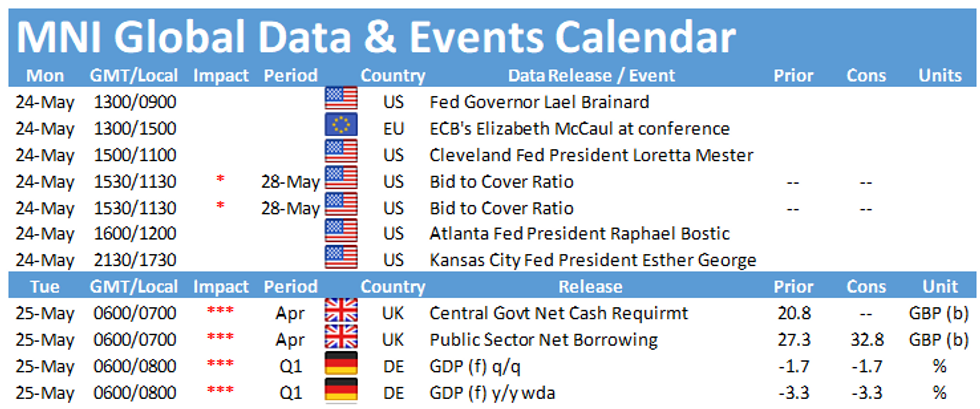

- Global data docket is light today, with comments from Brainard, Mester, George & Bostic as well as BoE's Bailey, Cunliffe, Haldane & Saunders eyed going forward.

FOREX OPTIONS: Expiries for May24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2145-60(E1.0bln-EUR puts), $1.2200(E1.1bln, E1.03bln EUR puts)

- USD/JPY: Y108.45-50($440mln-USD puts), Y108.80-109.00($665mln-USD puts)

- GBP/USD: $1.4150(Gbp298mln-GBP puts)

- AUD/USD: $0.7615-35(A$655mln), $0.7710-25(A$1.4bln-AUD puts), $0.7750(A$556mln-AUD puts)

- USD/CAD: C$1.2150($875mln-USD puts)

- USD/CNY: Cny6.5125($780mln)

ASIA FX: Muted Moves

Uncertain risk sentiment and muted performance saw most Asia EM FX fluctuate within ranges.

- CNH: Offshore yuan Is higher, managing to reverse a move lower in the wake of a weaker fix from the PBOC. Over the weekend the PBOC said it will maintain the exchange rate at "basically stable" levels, the comments come after rhetoric by its officials who suggested the yuan be allowed to appreciate and authorities should eventually relinquish control over the currency.

- SGD: Singapore dollar gained. On the coronavirus front Singapore will close two malls after new cases were linked to the properties. The vaccine programme is gathering pace, over 2m residents in Singapore have had their first dose of the vaccine, over 1/3 of the population.

- TWD: Taiwan dollar strengthened, Health Minister said that the coronavirus situation in Taiwan is "stable" and the rate of positive cases as a percentage of tests is decelerating. There is no current need to impose a harder lockdown if Taiwanese people cooperate to fight the pandemic he noted.

- KRW: Won weakened slightly, but is holding most of Friday's gain. South Korean President Moon has returned from his summit with US President Biden, on the back of the visit South Korea and the US have announced an agreement to deepen cooperation in a range of industries including pharmaceutical companies making Covid-19 vaccines, electric-vehicle batteries and semiconductor producers.

- MYR: Ringgit is flat. With further record-breaking daily Covid-19 case counts, Malaysia's gov't decided to tighten MCO (Movement Control Order) 3.0, albeit PM Muhyiddin clarified to Bernama/RTM that it will not be a total lockdown resembling MCO 1.0 imposed in March 2020 due to unbearable economic cost.

- IDR: Rupiah is flat, Bank Indonesia begin their policy meeting, with decision announcement coming up tomorrow. The MPC are widely expected to leave their benchmark interest rate unchanged for the fourth straight time.

- PHP: Peso is lower. The Philippines and China held bilateral talks on the situation in the South China Sea, seeking to diffuse tensions over disputed waters. Philippine Foreign Affairs Dept called the talks "friendly and exchanges," underlining the need for continued dialogue. Meanwhile, Vice Pres Robredo said that the dispute should be resolved in a multilateral format.

ASIA RATES: South Korea Second Budget Shock Reversed

Uncertain risk sentiment saw muted moves in the fixed income space, with the exception of South Korea where futures cratered on reports of an additional budget and then rallied on the denial.

- INDIA: Yields mostly lower in early trade. Participants await an INR 110bn state debt sale. Auctions on Friday were smooth, the RBI took the opportunity to sell more than the advertised amount amid decent demand. The central bank sold INR 378bn against an announced target of INR 320bn. The move saw bonds give up early gains though, yields finished around 1bps higher. The RBI also approved an INR 991.2bn dividend to the government on Friday, higher than expected, which helped assuage some worries over coronavirus financing for the finance ministry.

- SOUTH KOREA: Futures in South Korea are lower, but off worst levels. The initial move lower came after reports in Asia Business Daily that the government was internally considering a second extra budget plan. The finance ministry then issued a denial which saw futures come off worst levels, but fail to recover all of their losses. Elsewhere, a 5-year auction was taken down smoothly with the government selling around KRW 120bn more than planned.

- CHINA: Futures in China are in negative territory, grinding lower through the session. A PBOC policy advisor told MNI the PBOC is likely to keep liquidity stable unless the consumer price index rises over 3% year-on-year while continuing to restrict further credit expansion in the hot property market.

- INDONESIA: Yields mixed, curve twist steepens. Bank Indonesia said Friday that its third week survey suggested that CPI may come in at +1.69% Y/Y this month. The Bank begin their policy meeting, with decision announcement coming up tomorrow. The MPC are widely expected to leave their benchmark interest rate unchanged for the fourth straight time.

EQUITIES: Broadly Positive

A broadly positive day for equities in the Asia-Pac region, most indices are in the green though gains are modest. Bourses in Japan are higher by around 0.4% despite plans to extend Covid-19 state of emergency beyond the end of the month. Mainland China is just in positive territory, struggling to make headway after China once again warned against rising commodity prices and promised to crack down. Markets in South Korea struggled and are in negative territory at the time of writing. In the US futures are higher following a mixed finish for US stocks on Friday.

GOLD: Well-Defined Resistance Remains In Play

Bullion has nudged higher during Asia-Pac hours, last +$4/oz at $1,885/oz, within the confines of last week's range. Bulls remain focused on $1,892.7/oz, the 76.4% retracement of the Jan 6 - Mar 8 fall. The USD/inflation/U.S. real yield mix remains at the fore on the fundamental side.

OIL: Benchmarks Gain

Oil is higher in Asia-Pac trade on Monday, building on Friday's gains. WTI & Brent sit ~$0.40 above their respective settlement levels. There are positive signs that the US is making progress in its battle with coronavirus, data showed in the latest week there were no days where new cases were over 30,000 for the first time in 11 months. The optimism surrounding the recovery is outweighing demand concerns as much of Asia deals with elevated case numbers, and the prospect of additional supply from Japan.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.