Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORWAY

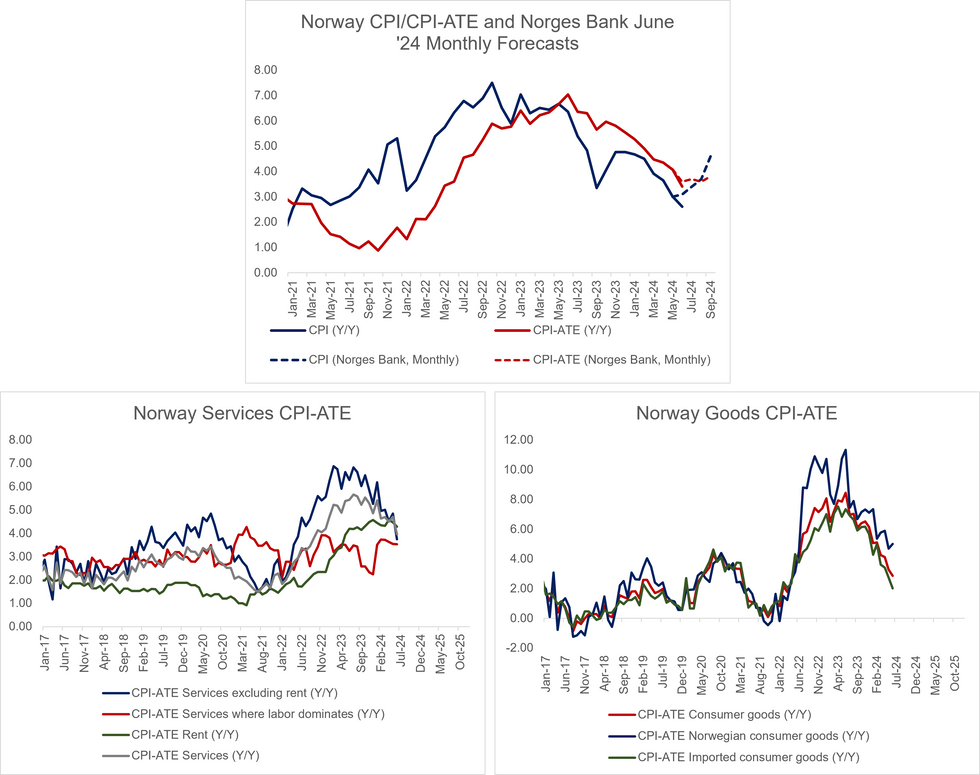

Norwegian June CPI surprised to the downside, with CPI-ATE at 3.4% Y/Y (vs 3.6% expected by consensus and the Norges Bank, 4.1% prior).

- NOK has weakened following the release, with EURNOK (currently 0.45% higher) just above the 100/200-day EMA’s at ~11.51, but still well short of the first resistance at 11.5679.

- Despite the downward surprise, we maintain our view that meaningful alterations to Norges Bank rate cut expectations will need to wait for after the July inflation data, due August 9.

- A sharp pullback in services inflation appears to have driven the surprise, with services CPI-ATE inflation at 4.0% Y/Y (vs 4.7% prior) and 0.2% M/M (vs 0.8% prior). Rents moderated, as did the "services excluding rent" measure.

- The recreation and culture component notably fell to 4.0% Y/Y (vs 7.6% prior).

- Domestically-produced consumer goods actually accelerated on an annual basis to 5.0% Y/Y (vs 4.7% prior), though another deceleration in imported goods inflation offset.

- The downward surprise in CPI-ATE comes in spite of food prices rising 1.9% M/M - faster than analysts with above-consensus forecasts had expected.

- Headline CPI was 2.6% (vs 3.0% cons, 3.1% Norges Bank and 3.0% prior), driven by a ~20% Y/Y fall in electricity prices for the second consecutive month.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok