Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- RBNZ OCR track provides hawkish surprise, although Governor Orr places heavy caveats around it.

- The PBoC doesn't stand in the way of the latest leg lower in USD/CNY as the cross breaks below CNY6.4000.

- Equities mixed, liquidity thinned in Asia.

BOND SUMMARY: RBNZ Applies Some Pressure To Core FI Markets

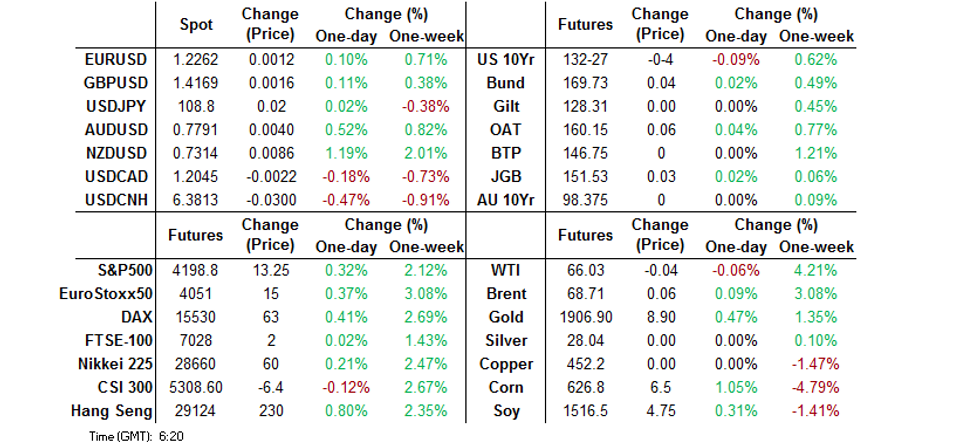

T-Notes traded a touch cheaper during Asia-Pac hours, although there was a lack of notable news flow outside of the hawkish surprise provided by the OCR track that accompanied the RBNZ monetary policy decision. T-Notes last -0-03+ at 132-27+, while cash Tsys saw some modest bear steepening as 20s provided the weak point on the curve, cheapening by ~2.0bp as of typing. T-Note volume hovers around 290K, although ~177K of that has come via the roll, with the latest estimates pointing to ~65% of the TY roll being completed at present. Overnight flow was headlined by a 5.0K block sale of the TYN1 132.50 calls. Fedspeak from Quarles & 5-Year Tsy supply headline the local U.S. docket on Wednesday (2-Year FRN supply is also due).

- JGB futures last +3, sticking to a tight range during Tokyo hours, but backing off from best levels given the pressure seen elsewhere in the core global FI complex. The major cash JGB benchmarks trade little changed to 1.0bp richer on the day at typing, off best levels. Speculation re: the elongation of the states of emergency in play in Tokyo/wider afield continue to do the rounds. Re: the Olympics, Asahi Shimbun, an official partner of the Tokyo games, called for the cancellation of the event, although ruling party lawmaker Yamamoto told RTRS that Japan will hold the games and the event will be "good for the economy." Yamamoto also noted that the government is expected to compile an extra budget in October/November, with the aim of cushioning the economic blow from the COVID-19 pandemic. Bank of Japan board member Suzuki warned of bigger downside risks to the economy and prices amid high uncertainty over the pace of the COVID vaccine rollout/questions over its effectiveness, while continuing to stress that the BoJ must monitor the side effects of its ultra-loose monetary policy settings. Suzuki also noted that some JGB market participants left the space owing to the limited moves that had been observed, while highlighting that the BoJ's permitted 10-Year JGB yield trading may offer "great opportunities" for traders. 40-Year JGB supply headlines the local docket on Thursday.

- Aussie bond futures trickled lower in the wake of the latest RBNZ monetary policy decision across the Tasman, with the previously outlined hawkish inferences from the contents of the resumed publication of the RBNZ's OCR track and tweaks to its forward guidance weighing on NZGBs, creating some trans-Tasman spill over. Still, cash ACGBs comfortably outperform their NZ equivalents on the day. YM -1.5, XM unch. last, with the wider cash curve seeing a similar degree of twist flattening, although operating off of early session flats. Local data (in the form of stronger than expected completed construction work data for Q1 & another uptick in the Westpac leading index) did little for the space. Comfortable absorption of the A$1.0bn ACGB May '32 supply was seen, with the average yield pricing 0.54bp through prevailing mids at the time of supply (per Yielbroker pricing), although the cover was softer than prev. The latter point isn't a great worry, but one to track in future auctions covering this zone of the curve considering the A$200mn decrease in the amount of paper on offer at this auction vs. the prev. auction. Elsewhere, the Melbourne COVID cluster continues to see incremental increases in confirmed cases, although there has been no market reaction to the development in recent days, given Australia's track record in dealing with the virus. Still, regional authorities did not rule out the imposition of tighter restrictions in the Greater Melbourne area. Q1 Private CapEx data headlines the local docket on Thursday.

FOREX: Hawkish RBNZ Sends Kiwi Flying, Risk-On Sentiment Takes Hold

RBNZ monetary policy decision sent the kiwi rallying across the board, as the Reserve Bank left its monetary policy settings unchanged and signalled that the tightening cycle is in sight. The reinstated OCR projection included in the Monetary Policy Statement suggested that the OCR could start rising in mid-2022, slightly earlier than most had expected. Meanwhile, the MPC dropped reference to being "prepared to lower the OCR if required" from its statement, while the summary of the meeting only mentioned that "the OCR is the preferred tool to respond to future economic developments in either direction".

- NZD/USD pierced the $0.7300 figure and attacked key resistance area at $0.7305/07, which represent May 10/Mar 2 highs. The rate managed to take out these levels and trades just above there at typing. NZD/JPY surged to its best levels since Apr 2018, after breaching its YtD peak. Key resistance levels gave way as NZD extended gains during RBNZ Gov Orr's press conference.

- The bid in NZD spilled over into AUD, which was the second best performer in the G10 pack, as well as into the broader commodity FX space. AUD/NZD slid sharply after the RBNZ's announcement and narrowed in on key support from Feb 26 low of NZ$1.0640.

- The PBOC set the central USD/CNY mid-point at CNY6.4099, just 2 pips shy of sell-side estimate. USD/CNH extended losses after the in-line fixing, printing worst levels since Jun 2018.

- Safe haven currencies came under additional pressure as e-minis crept higher. USD and JPY were comfortably the worst performers in G10 FX space.

- Focus turns to French sentiment gauges, Swedish unemployment as well as comments from Fed's Quarles, ECB's Villeroy & BoC's Lane.

FOREX OPTIONS: Expiries for May26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2000(E628mln), $1.2075-90(E1.4bln-EUR puts), $1.2195-10(E1.0bln), $1.2215-30(E746mln-EUR puts)

- USD/JPY: Y108.00($1.0bln), Y108.25-35($534mln), Y108.50-60($558mln), Y108.80($604mln), Y109.25($725mln), Y109.50($879mln), Y110.50($717mln)

- GBP/USD: $1.4220(Gbp422mln-GBP puts)

- EUR/GBP: Gbp0.8600-15(E1.1bln)

- EUR/CHF: Chf1.1000(E741mln-EUR puts)

- USD/SEK: Sek8.2650($642mln-USD puts)

- AUD/USD: $0.7600-10(A$648mln), $0.7740-50(A$1.2bln-AUD puts), $0.7770-85(A$1.1bln-AUD puts)

- NZD/USD: $0.7215-17(N$599mln)

- USD/CNY: Cny6.35($650mln), Cny6.4445($500mln-USD puts)

ASIA FX: Liquidity Thin Due To Holidays

Several markets in Asia are closed for public holidays; Singapore, Indonesia, Thailand, Malaysia and India are all closed today.

- CNH: Offshore yuan strengthened, USD/CNH consolidating below 6.40 as the pair hit the lowest since June 2018. The PBOC fix was broadly in line with sell side estimates, despite the recent strength in the yuan, which markets interpreted as a signal the central bank if comfortable with the move higher in yuan. There was also a commentary in CSJ that predicted yuan strength near term.

- TWD: Taiwan dollar has continued its move higher on Wednesday, USD/TWD last down 0.061 at 27.80 the lowest since May 10. 1-month 25 delta risk reversals are hovering around 0.00 after being positive since March.

- KRW: Won is stronger, USD/KRW hovers just above its 100-DMA at 1116.71. Data earlier in the session showed manufacturers business confidence fell to 97 in June from 98 in May. Non-manufacturers confidence fell to 81 from 82 in May. Domestic demand would seem to have picked up, the proportion of companies complaining about weak demand fell to 11.7% from 11.8% previously. Markets await the BoK rate announcement tomorrow where the bank is expected to upgrade growth forecasts.

- PHP: Peso is stronger, OCTA Research Group said Tuesday advised that the gov't could gradually relax restrictions in Metro Manila, as the Covid-19 situation continued to improve.

EQUITIES: Mixed

Mixed performance in Asia with markets oscillating between minor positive and minor negative territory. Mainland China is higher after a robust rally yesterday, Tuesday saw Chinese mainland equities benefit from record daily net inflows via the northbound legs of the Hong Kong-China Stock Connect schemes, totalling a net CNY21.7233bn. In Japan the Nikkei is around 0.4% higher, while the TOPIX is slightly lower, the NHK has suggested that the Tokyo Metropolitan Government is considering asking the central government to extend a coronavirus state of emergency in the capital that's due to expire May 31. In South Korea markets are mixed with the KOSPI marginally lower as coronavirus cases rise above 700. Several markets in Asia are closed for public holiday's; Singapore, Indonesia, Thailand, Malaysia and India are all closed today. US futures are higher after dropping yesterday with the Nasdaq outperforming.

GOLD: $1,900/oz Breached, RSI Eyed

Tuesday's move lower in U.S. real yields and the latest leg of weakness for the USD (as measured by the broad DXY index) coupled to propel spot gold above $1,900/oz for the first time since early January (although the move was not sustained on a closing basis), with further gains lodged during Asia-Pac hours. Spot currently sits just above $1,905/oz, with bulls now eying resistance in the form of the Jan 8 high, which is located at $1,917.6/oz, although the RSI is starting to show worrying signals, topping 75 for the first time August (a swing in the measure back below 70 will trigger a technical sell signal for some).

OIL: Crude Little Changed

Oil is little changed in Asia on Wednesday, still inside yesterday's range after a flat finish on Tuesday; WTI is a handful of cents lower, while Brent sits a handful of cents better off. Data late yesterday from API showed headline US crude stocks fell by 439k bbls, while gasoline stocks fell 2m bbls, and crude stocks at Cushing fell 1.2m bbls. Talks between Iran and world powers continue in Vienna, E.A. Gibson Shipbrokers estimate Iran could have up to 69m bbls of crude in tankers at sea. Elsewhere Nigeria signed a deal for investment in an offshore oil field with Shell, Exxon, Total and Eni for a production sharing contract which could take capacity at the field to around 350k bpd from 200k bpd currently.

UP TODAY (Times GMT/Local)

ASIA RATES: Rising Tide

Moves exacerbated in thin liquidity. Several markets in Asia are closed for public holiday's; Singapore, Indonesia, Thailand, Malaysia and India are all closed today.

- SOUTH KOREA: Bonds higher in South Korea as markets await the BoK rate announcement, the bank is expected to remain on hold but upgrade economic forecasts on the back of robust exports and a solid economic recovery. There is still some doubt over the pandemic with new cases rising back above 700 on Wednesday.

- CHINA: Repo rates dropped after a jump yesterday, the overnight repo rate down 16bps to 1.9993%. The PBOC matched maturities with injections again. Futures rose with the 10-year moving back towards resistance at 98.65. The MOF sold 10-year upsized bonds to strong demand; the auction drew a yield of 3.02% and cover of 5.8, previous auction on April 21 drew a yield of 3.1265% and was covered 4.73x.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.