Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- U.S. Tsy Sec. Yellen pushes for fiscal spending, even if it results in higher rate settings from the Fed.

- U.S. Tsys give back a portion of their post-NFP rally in Asia.

- Headline flow light in overnight trade.

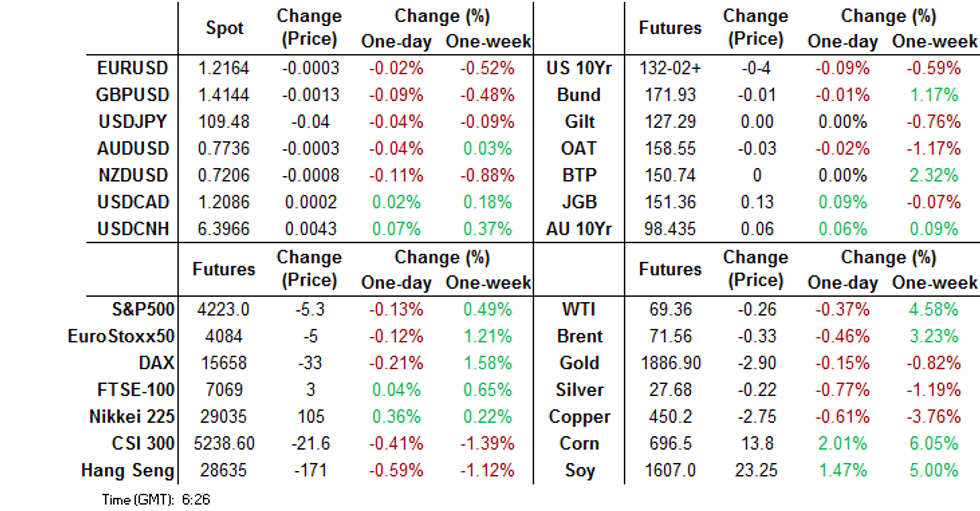

BOND SUMMARY: U.S. Tsys Off Post-NFP Highs

T-Notes print -0-03+ at 132-03, hovering just above session lows as Tsys trade a touch softer across the board after a peculiar pop through Friday's highs for longer dated Tsy futures around the re-open, which was quickly reversed. Cash Tsys run 0.5 to 2.0bp cheaper across the curve, with light bear flattening in play. Weekend focus fell on the G7's agreement re: the broader implementation of a minimum corporate tax rate structure, as they look to fight tax evasion, notably within the big tech space, while a BBG interview with U.S. Tsy Secretary Yellen is also garnering attention. Yellen noted that U.S. President Biden should push on with his $4tn spending schemes, even if they may result in inflation spill over into '22 and higher interest rate settings from the Fed. Elsewhere on the U.S. fiscal front, the weekend saw U.S. Energy Secretary Granholm tell CNN that the U.S. House will start the mark-up of an infrastructure bill on Wednesday, with or without Republican support. U.S. fiscal developments will likely continue to garner most of the attention during Monday's U.S. session, with the Fed now in its pre-meeting blackout period & a lack of meaningful domestic data apparent.

- JGB futures have held to a narrow range, +12 ticks vs. settlement at typing, after a very brief and limited look through overnight session highs. Bonds in the belly of the JGB curve run 1.0-2.0bp firmer, while the wings lag, with the super long end likely limited by the proximity to tomorrow's 30-Year JGB supply. There has been little to note on the domestic front, outside of a RTRS report which flagged the following: "Japan will highlight the need for fiscal reform even as it keeps up stimulus to combat the blow from the coronavirus pandemic, a draft of its economic and fiscal blueprint reviewed by Reuters showed. The government will also unveil plans to promote green and digital investment by drawing in private demand, as part of efforts to revitalise the world's third largest economy, according to the draft of this year's blueprint." Tuesday will see local wage data and the BoP print compliment the aforementioned round of 30-Year JGB supply.

- Aussie bond futures have failed to work their way out of the ranges established early on in Sydney trade, with YM +1.0 and XM +6.0. The latter has struggled to extend meaningfully through the recent highs, but bulls seemingly remain in control there. The presence of the latest round of scheduled RBA ACGB purchases may have provided some support when compared to U.S. Tsys. Headline flow remains light, with a decent pipeline of A$ issuance building (particular focus has fallen on sustainability/social bonds, with onshore and offshore names active there). ANZ Job ads data was strong (once again), with the survey collator noting that "ANZ Job Ads hit 12 straight months of gains in May, and is now consistent with an unemployment rate of around 5%... The Victorian lockdown is unlikely to derail the state's labour market recovery. Even if we see some employment losses in June, as long as restrictions start easing from 11 June as currently planned, workers should be reinstated or find new jobs quite quickly, given the underlying strength in the labour market." The monthly NAB business survey headlines the local docket on Tuesday.

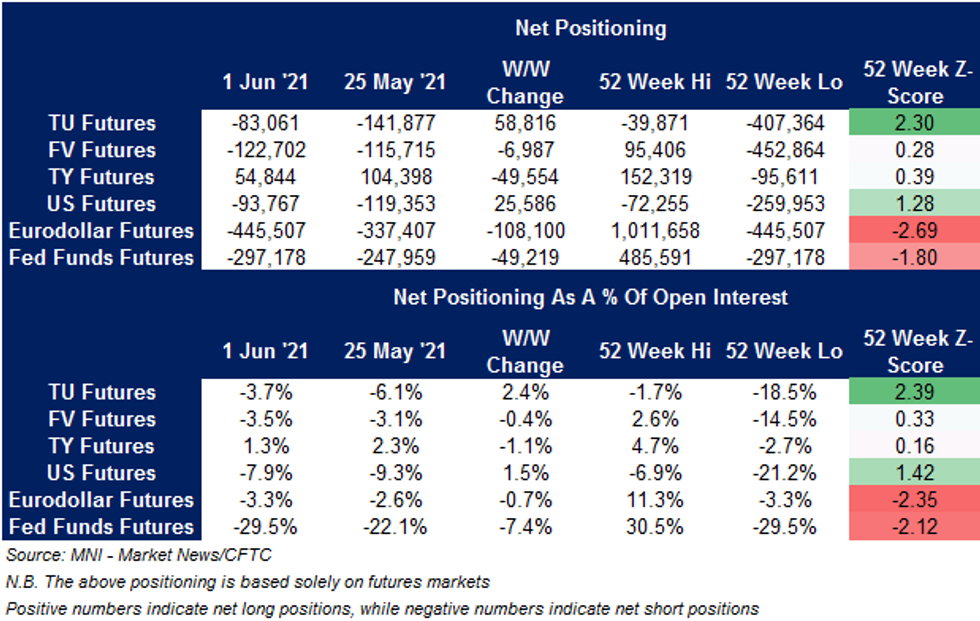

US TSY FUTURES: Eurodollar Net Shorts Continue To Headline CFTC CoT

The latest CFTC CoT report (covering the week ending 1 June), revealed the following non-commercial net positioning moves ahead of Friday's NFP print.

- Net short positioning in Eurodollar futures continues to draw the most attention, with net positioning in the space moving to the deepest net short witnessed since early May '20.

FOREX: Yuan Falters After Softer Then Expected PBOC Fix

The yuan weakened as the PBoC set its central USD/CNY mid-point at CNY6.3963, 32 pips above sell-side estimate. The fixing represented yet another sign that China's central bank is opposed to further yuan appreciation. USD/CNH reclaimed the bulk of its Friday loss, even as it showed little immediate reaction when China's trade surplus proved narrower than forecast.

- Yuan weakness in combination with softer e-minis may have applied a modicum of pressure to the Antipodeans, with regional liquidity sapped by a market holiday in New Zealand. AUD failed to draw any meaningful support from a solid local ANZ job ads print & S&P's decision to upgrade Australia's credit rating outlook.

- Sterling showed some weakness in Asia-Pac hours amid worries over the spread of a highly transmissible variant of coronavirus in the UK as well as continued tensions with the EU over Northern Ireland.

- German factory orders, Norwegian industrial output & comments from BoE's Broadbent take focus from here.

FOREX OPTIONS: Expiries for Jun07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2050(E677mln-EUR puts), $1.2175-80(E661mln-EUR puts), $1.2210-15(E759mln-EUR puts),$1.2250(E651mln-EUR puts), $1.2290-1.2305(E956mln-EUR puts)

- USD/JPY: Y108.25-35($776mln-USD puts), Y109.00-20($625mln-USD puts), Y109.50-65($1.55bln-USDputs), Y110.00($1.0bln-USD puts), Y110.50($825mln)

- EUR/JPY: Y133.40(E440mln-EUR puts)

- USD/CHF: Chf0.9125($600mln-USD puts)

- AUD/USD: $0.7700(A$543mln-AUD puts)

- USD/CAD: C$1.2000($970mln-USD puts)

- USD/MXN: Mxn19.65($507mln)

ASIA FX: Playing Catch Up

The fall in the greenback saw most USD/Asia EM FX pairs decline at the open but retrace losses as the session wore on amid negative risk sentiment.

- CNH: Offshore yuan is weaker, declining as the PBOC intimated a preference for a weaker yuan at the fix, while a miss in trade data saw yuan hold its losses.

- SGD: Singapore dollar is flat having hugged a tight range, on the coronavirus front there were only six cases discovered locally in the past 24 hours, the lowest tally since May 10.

- TWD: Taiwan dollar is slightly stronger but off best levels. The Taiex saw heavy selling and at one point was down 2%,, it was announced that the soft lockdown would be extended to June 28.

- KRW: The won is stronger, there were reports in the Yonhap that South Korea may collect around KRW 32tn in excess tax revenue this year, potentially securing ammunition to finance another round of an extra budget under review

- IDR: Rupiah is stronger, limited local headline flow. Bank Indonesia will release the monthly update on foreign reserves tomorrow, with official consumer confidence data coming up Wednesday. Danareksa's consumer sentiment gauge is expected at some point this week.

- PHP: Peso gained, Philippine Dept of Health said that the local Covid-19 outbreak remains "manageable" and asked Filipinos to observe the current health protocols, the government begins the inoculation of essential workers against Covid-19 today.

- THB: Baht is stronger, Thailand's nationwide Covid-19 vaccine rollout kicks off today. Meanwhile, Thai businesses have voiced concern over restrictions, which are part of the plan to reopen Phuket to foreign visitors next month. Under current regulations, tourists will have to remain on the island for 14 days after arrival.

ASIA RATES: Market Continues To Digest Last Week's RBI

- INDIA: Yields mixed in early trade, curve twist flattens. Bonds ended the day lower on Friday despite a dovish RBI and the announcement of a bigger GSAP 2.0 programme. The size was slightly smaller than expected at INR 1.2tn, and the assumption of inclusion of state debt also spooked some investors. Also adding to negative sentiment was the announcement that the final round of GSAP purchases of INR 400bn this quarter will have INR 100bn allocated to state bonds. Also on Friday the RBI's consumer confidence survey showed a drop in confidence, the current situation index fell to a record 48.5 in May from 53.1 previously with respondents also pessimistic about the year ahead as coronavirus clouds the outlook.

- SOUTH KOREA: Futures in South Korea are higher, there were reports in the Yonhap that South Korea may collect around KRW 32tn in excess tax revenue this year, potentially securing ammunition to finance another round of an extra budget under review. This would appear to all but confirm comments from FinMin Hong on Friday that extra issuance would not be necessary.

- CHINA: Futures lower in China, in the cash space 10-year yield touched the highest since May 7 at 3.15%. Trade data showed exports and imports missed estimates though both still rose at a decent clip. The trade surplus widened more than expected in yuan terms but missed estimates in USD terms. In USD terms exports missing broader expectations by a wider margin that imports. The CNY side of the data saw a slightly wider than expected trade surplus, with exports missing broader expectations by a slimmer margin than imports. Repo rates are higher, the overnight repo rate up around 13bps, 7-day repo rate up 4bps to 2.2905% above the PBOC's 2.20% rate.

- INDONESIA: Yields mixed in Indonesia amid a lack of significant local news flow. Some light twist flattening seen. Bank Indonesia will release the monthly update on foreign reserves tomorrow, with official consumer confidence data coming up Wednesday. Danareksa's consumer sentiment gauge is expected at some point this week.

EQUITIES: Nursing Losses

A broadly negative day for equity markets in the Asia-Pac region, most major markets nursing losses but off worst levels. The Taiex was earlier down around 2% but has recovered most of the downside, it was announced that the soft lockdown would be extended to June 28. Some underperformance for HK/mainland Chinese equities, there were weekend reports surrounding continued IPO headwinds in Hong Kong in the wake of the "Chinese tech crackdown," while Sino-U.S. tensions and deeper COVID restrictions for China's Guangzhou also garnered some attention. In the US futures are lower as markets assess the most recent comments from US Tsy Sec Yellen and Friday's NFP report, while looking ahead to inflation data later this week.

GOLD: Range Is Now Defined

Very modest upticks in U.S. yields and the broader USD have provided light pressure for gold during Asia-Pac hours, with spot last dealing a handful of dollars lower around $1,886/oz. To recap, our weighted measure of U.S. real yields moved back to Thursday's lows on the back of Friday's softer than expected headline NFP print, with nominal yields lower on the day, while breakevens were little changed. A defensive round of post-data dealing for the broader USD also helped support gold. Still, bulls failed to reclaim the $1,900/oz, with no substantial movement on the technical front seen.

OIL: WTI Slips After Briefly Hitting $70/bbl

Oil is lower in Asia-Pac trade on Monday on the back of a stronger USD and some profit taking; WTI retreating slightly after earlier rising above $70/bbl for the first time since October 2018. WTI & Brent sit ~$0.30 below settlement levels at typing. Crude futures rose around 4% last week, and have risen in five out of the last six weeks.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.