Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

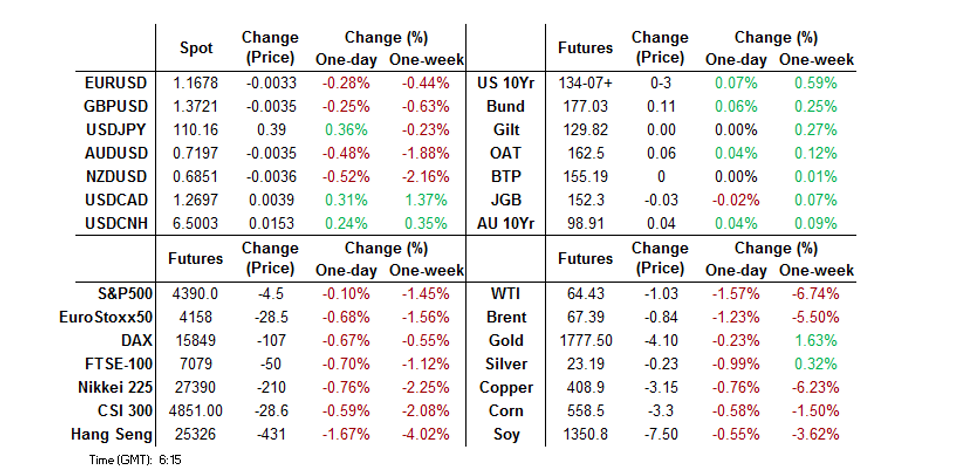

- The DXY has now more than reversed the initial knee-jerk lower seen in the wake of the release of the minutes covering the latest FOMC meeting, hitting the highest level witnessed since Nov '20 in the process.

- The major Asia-Pac equity indices struggled in the wake of the negative lead from Wall St.

- The broader economic docket is relatively sparse on Thursday. Second tier U.S. data and the latest Norges Bank monetary policy meeting headline.

BOND SUMMARY: Tight Ranges For Core FI In Asia

T-Notes clung to a tight 0-03+ range in Asia-Pac hours, with a lack of notable macro news headlines and market flow evident. The contract prints +0-02+ at 134-07 on volume of ~66K ahead of European hours. The major cash Tsy benchmarks sit unchanged to 1.0bp cheaper across the curve. Looking to Thursday's U.S. docket, weekly jobless claims data, the latest Philly Fed survey and 30-Year TIPS supply will be eyed.

- Aussie bond futures initially drew support from an uptick in the new COVID case count in Victoria, as well as another record high in NSW's daily case count. The latest Australian monthly labour market report was skewed by the sample period (mid-July) which provided a much more optimistic round of releases than the current reality reflects (notably, a fresh lockdown in Victoria has gone into play since then). The fact that the sample period caught Victoria emerging from a lockdown resulted in a surprise uptick in headline employment (+2.2K), which when combined with the fall in participation resulted in a downtick in the unemployment rate. Hours worked were -0.2% in the month, but once again skewed by the sample dynamics, with much of the headwinds in NSW offset by the sampling issues outlined above.

- JGB futures held a narrow range and last trade -4, with the major cash JGB benchmarks little changed across the curve. There wasn't much change in the underlying dynamics witnessed in the most recent off-the-run 15.5- to 39-Year JGB liquidity enhancement auction vs. the prior offering.

JAPAN: Little To See In Weekly International Security Flow Data

The latest round of Japanese weekly international security flow data revealed no meaningful movement of the 4-week rolling sums covering the major metrics.

- Japanese investors reverted to buying foreign bonds last week, although as has been the case in recent weeks, the recent net purchases are dwarfed by the recent net sales, leaving the 4-week rolling sum comfortably in negative territory.

- Japanese investors also reverted to modest net sales of foreign equities after lodging the largest round of weekly net purchases seen since May '20 in the previous week.

- Foreign net purchases of Japanese bonds were registered for a 3rd straight week and a 6th week in 7, although the size of the net purchases was tame.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | 661.8 | -1103.6 | -1299.2 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | -85.4 | 615.7 | 474.1 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 161.5 | 681.8 | 1163.3 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 198.8 | 105.0 | 248.5 |

Source: MNI - Market News/Bloomberg/Japanese Ministry Of Finance

ASIA FX: Bad Day At The Office

The greenback rose post-FOMC minutes hitting 2021 highs, pervasive risk off sentiment pressured Asia EM currencies.

- CNH: Offshore yuan is weaker, USD/CNH is up 133 pips, the PBOC fixed USD/CNY at 6.4953, in line with sell side estimates. As a reminder markets look to the PBOC's LPR announcement tomorrow.

- SGD: Singapore dollar is weaker, USD/SGD consolidating further above the 1.36 handle. Singapore today eased work from home rules which means hat around half of those currently WFH will be allowed to return to the office.

- TWD: Taiwan dollar is weaker, USD/TWD approaching the 28.00 handle. Markets look ahead to BOP current account data today, export orders are expected to have risen 21.2% in July, down from a 31.1% rise in June, this would be the sixteenth month of expansion.

- KRW: Won is lower, on the coronavirus front there were 2,152 new cases in the past 24 hours, up from 1,805 yesterday with the long weekend being blamed for increased transmission. Short term external debt rose to $178bn in Q2 from $165.7bn previously.

- MYR: Ringgit declined, the Malaysian King invited lawmakers who support Ismail Sabri Yaakob as the new prime minister to an audience today. Sabri was deputy PM in Muhyiddin's coalition.

- IDR: Rupiah declined, hitting the lowest levels in two weeks. Markets await the Bank Indonesia rate announcement today, the Central Bank is expected to keep rates on hold.

- PHP: Peso is lower, yesterday the government cut its 2021 economic growth forecast to 4-5% from 6-7% previously. Markets await a decision on a two week lockdown extension.

- THB: Baht is weaker, approaching its 2021 low. Thailand reported a record single day coronavirus case tally of 20,515 on Wednesday. Elsewhere the BoT decided fiscal measures would be more effective than a further reduction in the policy rate according to the minutes released yesterday.

FOREX: Dollar Index Hits Highest Since Nov 2020

Despite a lack of significant newsflow during the session the greenback managed to rise to the highest levels since 2020 which helped catalyse moves in major pairs. It was hard to identify a fresh cue for the move, though proximity to the FOMC minutes could suggest Asia-Pac participants are looking the Fed's July meeting minutes from a different perspective.

- AUD/USD heads into Europe hovering around the 0.7200 handle, near the lowest since November 2020 with losses of around 30 pips. Data showed that the labour market unexpectedly gained jobs which took the pair off its lows, but the breakdown of the data was weak and the move lower resumed. There was also a pickup in Victoria coronavirus cases which added to negative sentiment.

- NZD/USD is down 39 pips. There were 11 new cases of coronavirus, taking the community total to 21. RBNZ Governor Orr spoke earlier and stressed that the Bank's strong view is to continue to reduce stimulus given the strong position of the NZ economy, Orr also noted that the Bank would have likely lifted the OCR yesterday in the absence of lockdown/COVID cases.

- USD/JPY is up 40 pips. Driven mainly by the move in USD. The Reuters Tankan manufacturing survey rose to 33 from 25 previously.

- Offshore yuan is weaker, USD/CNH is up 133 pips, the PBOC fixed USD/CNY at 6.4953, in line with sell side estimates. As a reminder markets look to the PBOC's LPR announcement tomorrow.

- Oil continued its decline which saw USD/CAD rise 35 pips, while EUR/USD and GBP/USD both fell around 40 pips.

- Upcoming data includes weekly US employment data, the labour market is seen as key for the Fed taper after the FOMC minutes yesterday.

FOREX OPTIONS: Expiries for Aug19 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-10(E610mln), $1.1650(E656mln), $1.1670-90(E2.9bln), $1.1700(E2.3bln), $1.1750(E2.0bln), $1.1780-00(E4.0bln), $1.1850(E1.3bln)

- USD/JPY: Y108.15($500mln), Y108.50-70($612mln), Y109.00-20($1.3bln), Y109.35-50($752mln), Y109.65-80($1.4bln), Y110.00($512mln), Y110.50-60($1.6bln), Y111.50($606mln)

- GBP/USD: $1.3800(Gbp720mln)

- EUR/GBP: Gbp0.8500-20(E691mln)

- AUD/USD: $0.7250(A$2.0bln), $0.7320-35(A$1.3bln), $0.7350-60(A$1.4bln)

- NZD/USD: $0.6800(N$1.4bln)

- USD/CAD: C$1.2575-85($1.6bln)

- USD/CNY: Cny6.4720($750mln)

ASIA RATES: Bonds Benefit From Broad Risk Off

- INDIA: Indian markets are closed today and will return tomorrow.

- SOUTH KOREA: Futures in South Korea higher, the 3-Year contract up 7 ticks at 110.52, 10-Year contract up 4 ticks at 128.89. Yields mostly lower in the cash space, 10-Year bucking the trend and rising 0.5bps. Participants will look ahead to the KRW 100bn 10-Year linker auction tomorrow. PPI figures will also be released tomorrow. On the coronavirus front there were 2,152 new cases in the past 24 hours, up from 1,805 yesterday with the long weekend being blamed for increased transmission.

- CHINA: Futures rose in China as equity markets came under heavy selling pressure amid fears of further regulatory curbs and crackdowns. Futures jumped higher at the open and actually trended lower throughout the session but managed to remain above Wednesday's closing levels. Elsewhere there were reports that China Huarong Asset Management will be racapitalised by state backed investors, finally answering the question if the firm was deemed too big to fail by the government. The PBOC matched maturities with injections, repo rates stayed within recent ranges.

- INDONESIA: Yields mixed ahead of the BI rate announcement later today, the Central Bank are expected to remain on holiday by all economists surveyed by Bloomberg. Elsewhere Indonesia sold IDR 30t of bonds in an auction Wednesday, missing the IDR 33t target, there were IDR 77tn of bids. The Finance Ministry said it will sell IDR 10t in a sukuk auction on Aug. 24.

EQUITIES: Asia-Pac Markets Drop, US Futures Pick Up From Closing Lows

Stocks in Asia came under heavy selling pressure, taking a negative lead from the US. The MSCI Asia-Pac index hit the lowest since December. The Hang Seng was down 1.80%, weighed by Alibaba which hit record lows during the session, the tech selloff in China's technology giants has continued as the government continues its crackdown. In Mainland China indices were down by around 1%, Tencent's earnings disappointed as the firm warned of regulatory curbs, Markets in Japan were down by around 0.8%, while emerging market indices endured hefty losses with the Kospi and Taiex both down over 1.8%. Risk off sentiment saw the greenback hit the highest levels since November 2020. U.S. e-mini futures shed 0.1% after plunging into the close on Wednesday.

GOLD: Asia Reaction To FOMC Minutes Pressures Bullion

The bullish price action in the USD witnessed during Asia-Pac hours (which resulted in the DXY printing at the firmest levels witnessed since Nov '20) weighed on bullion, with regional participants focusing on the passage in the FOMC's July meeting minutes which pointed to most of the U.S. Fed being of the opinion that a tapering move will come later in '21. Still, spot gold continues to stick to familiar territory, after last week's sell off and subsequent recovery rejigged the downside technical parameters. Spot last deals $8/oz or so softer around $1,780/oz, a little off worst levels of the session.

OIL: Crude Futures On Track To Decline For Sixth Straight Session

Crude futures continued to decline in the Asia-Pac session on Thursday, WTI is down ~$1.10 from settlement while Brent is down ~$0.90; both benchmarks showed at the lowest levels seen since May overnight. Markets continue to assess the weekly DoE crude oil inventories which showed a surprisingly large build in gasoline inventories - with stockpiles rising by 696,000 bbls, against an expected draw of over 2.3mln bbls. This countered both the crude oil and distillates headlines, which both showed larger draws on inventories than forecast. Oil was also pressured by a stronger greenback, the dollar index hit the highest since November 2020.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.