Real-time Actionable Insight

Get the latest on Central Bank Policy and FX & FI Markets to help inform both your strategic and tactical decision-making.

Free Access- RBA Governor Lowe pushed back on market pricing of '22/'23 rate hikes, reaffriming the Bank's well-trodden forward guidance, while he fleshed out the thought process behind the RBA's recently adjusted tapering setup.

- PBoC liquidity dynamics and continued stress for China Evergrande provided familiar sources of headline interest.

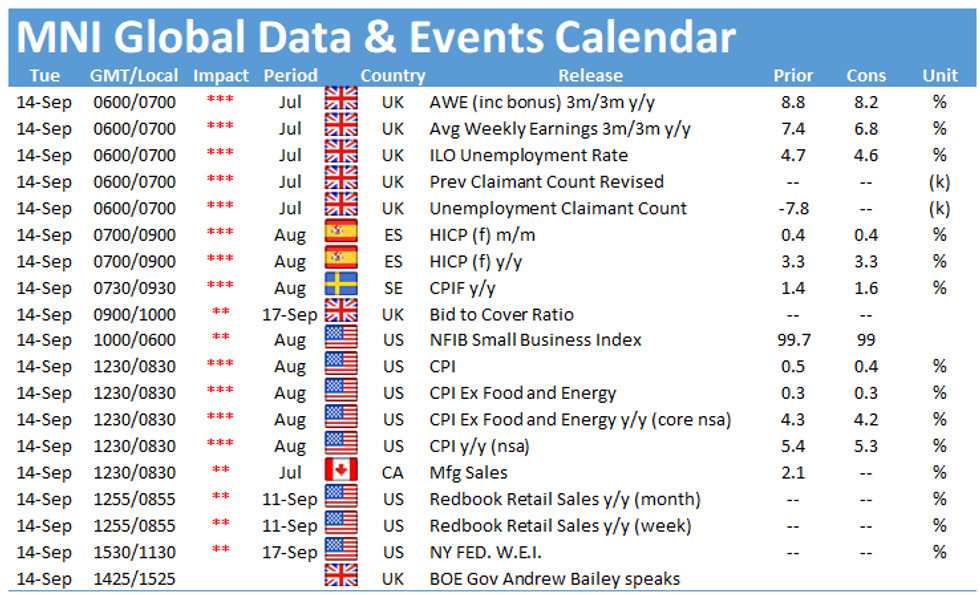

- U.S. CPI is set to dominate matters on Tuesday.

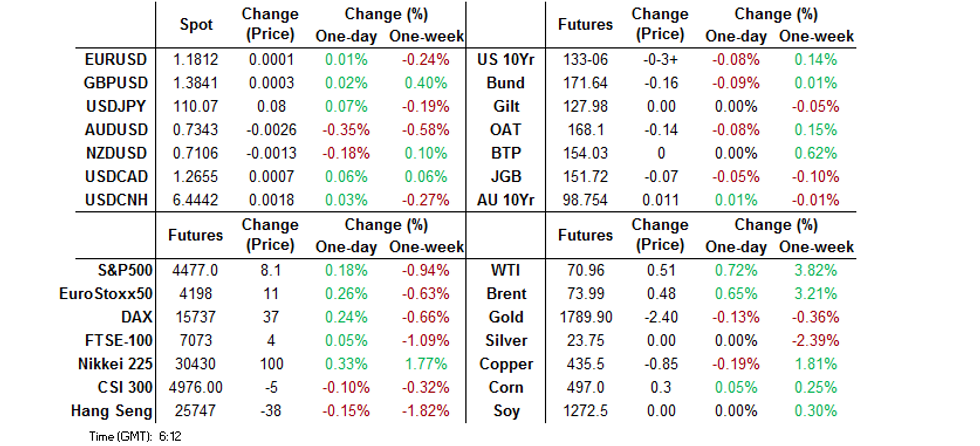

BOND SUMMARY: Cross Currents In Asia, Lowe Plays Down Market Pricing Re: Rate Hikes

A fresh multi-decade high for the Nikkei 225 helped apply modest pressure to U.S. Tsys during early Asia-Pac dealing, with some feedthrough from the Aussie bond space also evident. A couple of pockets of TY screen selling added to the downward pressure, although the contract stuck to a 0-05 range, recovering from worst levels as ACGBs turned bid to last trade -0-03 at 133-06+. Meanwhile, cash Tsys trade little changed to ~1.0bp cheaper on the day, with 5s underperforming. The latest round of U.S. CPI data dominates the NY docket on Tuesday.

- The uptick in the Nikkei 225 applied some light pressure to JGB futures, with the contract last 6 ticks below yesterday's settlement levels. Cash JGB trade sees the major benchmarks trading either side of unchanged out to 20s, within -/+0.5bp boundaries of yesterday's closing levels after initially benefitting from the overnight richening in U.S. Tsys. 30s & 40s print ~0.5bp cheaper on the day. The space seemed to look through a well-received 5- to 15.5-Year liquidity enhancement auction covering off-the run JGBs.

- RBA Governor Lowe's explicit push back against market pricing of rate hikes in '22 & '23 has promoted some outperformance in the front end of the ACGB curve, with YM +3.6 and XM +0.9 at typing (quoting the Dec '21 contracts). The comments also allowed the IR strip to flatten. Elsewhere, Lowe pointed to the potential for a cessation of bond purchases in '22. He also outlined the reasoning behind moving ahead with tapering at the Bank's September decision, in addition to adjusting the meeting where the RBA will reconsider its bond purchase rate to Feb '22. The thoughts were largely in line with the broader groupthink expressed in the wake of the decision i.e. gives the time bank to assess the economic impact of re-opening, addresses any COVID-related delay of reaching RBA goals and provides some insurance against downside risks. The uptick in the Nikkei 225 and syndication of a new 30-Year NZGB across the Tasman had applied some pressure to the space earlier in the day.

FOREX: Aussie Goes Offered On Lowe's Comments

AUD sold off as RBA Gov Lowe delivered a speech on "Delta, the Economy and Monetary Policy," in which he downplayed market pricing pointing to a rate hike in '22 & '23, reaffirming the Bank's well-trodden guidance. A BBG trader source suggested that short-term accounts initiated AUD/USD shorts in the lead-up to Lowe's address.

- NZD faltered on the back of apparent trans-Tasman spillover. The latest house sales data from REINZ showed that activity in New Zealand's property market took a hit from lockdowns in August, but median prices continued to rise reaching record highs.

- JPY softened into the Tokyo fix and remained on the back foot, as Japanese equity benchmarks traded in the green. Japanese headline flow was dominated by political headlines related to the ongoing LDP leadership race.

- U.S. CPI headlines today's global data docket, with UK labour market report also due. A round of comments from BoE Gov Bailey is eyed.

FOREX OPTIONS: Expiries for Sep14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1745-55(E1.1bln), $1.1835(E1.1bln), $1.1900-25(E1.2bln)

- AUD/USD: $0.7340-45(A$1.0bln)

- USD/CAD: C$1.2600-10($747mln), C$1.2650($661mln)

- USD/CNY: Cny6.4390($600mln), Cny6.5000($532mln)

ASIA FX: KRW Leads Gains Ahead Of Chuseok Holiday, With Covid Cases Below 1,500

KRW and PHP outperformed in Asia as participants assessed the state of play on the Covid-19 front, amid talk of South Korean exporters selling the greenback ahead of a local holiday.

- CNH: USD/CNH printed a session high of CNH6.4472 before trimming most gains. USD/CNY 1-year swap points continued to surge, reaching strongest levels in six years.

- KRW: The won garnered some strength amid talk of USD sales by local exporters ahead of the Chuseok holiday. The currency may have drawn some additional support from the fact that South Korea's Covid-19 case count remained under 1,500, even as the upcoming holiday continues to inspire concerns about potential uptick in virus transmission related to heightened travel activity.

- PHP: The peso traded on a firmer footing after the government unveiled a fresh Covid-19 strategy for Metro Manila, which relies on more targeted lockdowns covering smaller areas. Interior Sec Ano told CNN Philippines that the capital region will be initially set at Alert Level 4 when the new five-level scheme is implemented on Thursday.

- IDR: The rupiah stuck to a fairly tight range amid limited local headline flow.

- MYR: The ringgit treaded water, shrugging off Malaysia's decision to raise the debt ceiling to 65% of GDP.

- THB: The baht lagged its peers from Asia EM basket, even as Thailand's Covid-19 cases continued to ease, while the government said they may implement measures to boost domestic travel in one month's time.

EQUITIES: Mixed Overnight

The Nikkei 225 tagged fresh multi-decade highs on Tuesday, benefitting from positive reports surrounding the domestic COVID vaccine drive in Japan and expectations surrounding post-election stimulus. Elsewhere, it was China Evergrande that continued to steal the headlines, with the giant property developer flagging further risks and headwinds to company operations, while it confirmed that it has hired restructuring advisors to explore avenues out of its multitude of problems. The CSI 300 and Hang Seng both trade a little below unchanged levels. U.S. e-minis added incrementally to Monday's rally. Participants are zeroed in on Tuesday's U.S. CPI print.

GOLD: U.S. CPI Eyed As Gold Coils

Gold has meandered through the early rounds of trade this week, with spot continuing to print around $1,790/oz. That leaves the technical overlay as it was, with firm support at the Aug 19 low ($1,774.5/oz), while firm resistance is located at the July 15 high ($1,834.1/oz). Tuesday's U.S. CPI print provides the next notable input for participants.

OIL: A Little Firmer

WTI & Brent futures have added ~$0.40 to settlement levels, building on 2 sessions of gains. Monday's rally was aided by the continued issues re: getting U.S. Gulf supply back online in the wake of hurricane Ida, with a bullish sell-side note from Goldman Sachs no doubt helping the bid. The U.S. Gulf dynamic is feeding into the tight supply mantra, and the impact on prices was compounded by the latest OPEC report, released Monday, which revealed an uptick in the cartel's global demand forecasts. The latest round of weekly API crude inventory estimates will headline on Tuesday.

UP TODAY (Times GMT/Local)

Why Subscribe to

MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.