Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- A lack of escalation re: Sino-U.S. tensions in the wake of the Biden-Xi call meant that the worst case scenario was averted.

- The RBA's November meeting minutes flagged a greater upside risk re: inflation, with a wider range of outcomes surrounding the matter now possible. RBA Governor Lowe reaffirmed his dovish tone in a subsequent address.

- UK labour market data and a raft of central bank speak headlines the broader docket on Tuesday.

BOND SUMMARY: Worst-Case Averted

The light bid in U.S. Tsys that was apparent ahead of the Xi-Biden phone call faded from extremes, with the opening salvos ahead of the call seemingly a little bit more open vs. some expectations. While the meeting itself seemingly failed to herald any meaningful progress re: Sino-U.S. relations (as was exp.), the lack of overt conflict re: matters such as Taiwan meant that the call avoided the worst-case scenario for risk assets. TYZ1 +0-05 at 130-14+, back from session highs of 130-17, as cash Tsys run flat to 2bp richer across the curve, with 10s outperfroming. Flow was headlined by a 5K screen buyer of the TYZ1 130.00 puts. Tuesday's domestic docket is retail sales-centric, with industrial production, business inventories & NAHB housing data also due. Tuesday will also bring a deluge of Fedspeak, with Bullard, Barkin, Bostic, George & Daly all set to make addresses.

- The JGB curve was subjected to some twist steepening, with the belly representing the weak point (cheapening by ~1bp) in the wake of the weakness in futures overnight. The move in futures extended during the Tokyo morning as local participants reacted to overnight developments and set up for this afternoon's 5-Year JGB supply. The auction was solid, with the low price meeting broader expectations (taken from the BBG dealer survey), while the tail width held steady when compared to the previous auction as the cover ratio moved higher, topping the 6-auction average as it hit the highest level witnessed at a 5-Year JGB auction since April. Value vs. futures and the ability to set relative value steepener plays ahead of the impending outline of the well-discussed fiscal support package (which may weigh on the super long end on an increased issuance burden) were the most likely supporting factors for takedown (outlined ahead in our preview of supply). Futures are still lower on the day, -11 ahead of the close.

- While there was little in the way of fresh meaningful substance in the RBA's November meeting minutes, some light pressure crept into the front end of the ACGB curve post-release. That likely came on the back of the sentence which noted that "while a range of outcomes for global inflation in 2022 were possible, risks to inflation forecasts were tilted to the upside." A reminder that the market has been pricing an early RBA liftoff (when compared with Bank forward guidance) for some time, which limited the move. The Bank's overview on inflation remained relatively well balanced, with the minutes reiterating the idea that "members agreed that the distribution of possible outcomes for inflation had widened." The minutes then fleshed out upside and downside scenarios for the path of inflation. YM made new session lows on the release, with the same holding true for XM, although the contracts edged away from worst levels, with a subsequent address from RBA Governor Lowe reaffirming the well-known dovish stance at the centre of the central bank. YM -5.0 & XM -6.5 at the close.

FOREX: Virtual Summit Aids Redback, Dents Safe Havens

The first face-to-face virtual summit between U.S. Pres Biden and China's Pres Xi inspired some cautious optimism, sapping strength from safe havens USD and JPY in Asia-Pac hours.

- Note that $1.6bn worth of USD/JPY options with strikes at Y114.30 will roll off at today's NY cut, with a further $1.3bn of options due to expire at Y113.40-50. Spot USD/JPY last trades at Y114.17.

- AUD garnered some strength as the minutes from the RBA's most recent monetary policy meeting showed that the Reserve Bank sees risks to inflation shifting upwards. Its Antipodean cousin NZD traded on a softer footing, with AUD/NZD showing above the 38.2% recovery of its Oct 13 - Nov 9 sell-off.

- Offshore yuan went bid and printed its best levels since Jun 1, while spot USD/CNH plunged through support from ascending trendline/Oct 19 low in the process, as headlines surrounding Biden/Xi talks stole the limelight.

- U.S. retail sales & industrial output, UK labour market data and flash EZ GDP take focus on the data front, while central bank speaker slate features Fed's Bullard, Barkin, Bostic, George & Daly, ECB's Lagarde, BoC's Schembri & Riksbank's Breman.

FOREX OPTIONS: Expiries for Nov16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E695mln), $1.1539-50(E892mln), $1.1600-25(E1.4bln)

- USD/JPY: Y113.40-50($1.3bln), Y114.30($1.6bln)

- GBP/USD: $1.3495-00(Gbp500mln)

- EUR/GBP: Gbp0.8525(E791mln)

- AUD/USD: $0.7300-15(A$757mln)

- USD/CAD: C$1.2370-90($830mln)

- USD/CNY: Cny6.4000($2.3bln); Cny6.4390-00($1.3bln)

ASIA FX: Yuan Appreciates Amid Assessment Of Xi/Biden Talks

The leaders of China & U.S. held their first summit, which was interpreted as a positive sign re: bilateral relations and lent some support to the redback.

- CNH: Offshore yuan outperformed in Asia. Spot USD/CNH descended past ascending trendline drawn off 2018 low/Oct 19 low and bottomed out at its worst level since Jun 1, with the PBOC yuan fixing falling in close proximity to sell-side estimate.

- KRW: Spot USD/KRW wiped out its opening gains and returned to neutral levels. South Korea reported public finance data, which showed a pick-up in tax revenue.

- IDR: USD/IDR crept higher, with the rupiah struggling for momentum. FinMin Indrawati noted that the gov't sees 2021 budget deficit at 5.25% of GDP.

- MYR: USD/MYR oscillated around neutral levels, as early voting in Melaka state election kicked off.

- THB: The baht meandered after FinMin Arkhom said that a weaker exchange rate supported exports in 2021.

- PHP: The peso lagged behind its regional peers, despite a beat in overseas remittances reported yesterday. The list of candidates for the 2022 elections has been finalised following some last-minute reshuffles ahead of Monday's deadline for replacing candidates.

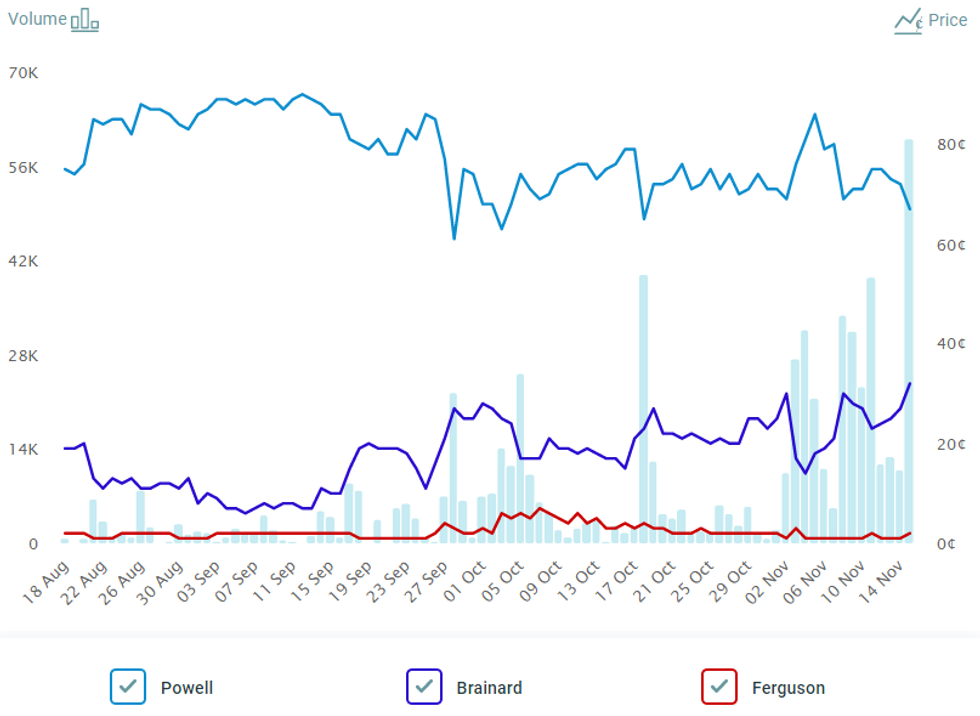

FED: A Look At What The Betting Markets Have To Say On The Race For Fed Chair

A reminder that late Monday saw BBG flag comments from Senate Banking Committee Chair Brown, who revealed that he was told by White House officials to expect an "imminent" announcement re: President Biden's pick to Chair the Federal Reserve. Brown said "I'm not going to speculate who I think it might be now. I assume the decision's been made and they haven't announced it, but I don't even know that."

- The incumbent, Jerome Powell, remains the favourite in betting markets, although the odds on that particular outcome have taken a hit in recent days after several press outlets noted that Lael Brainard's interview for the role went better than expected. BBG went as far as deeming her to be a "serious rival" for Powell, per a source report released last week.

- FOX's Charlie Gasparino suggested that Wall St. now sees odds re: a reappointment of Powell at just 50/50 after the decision was seen as a layup in favour of Powell not long ago. Betting market odds aren't quite as finely balanced, but the differential between Powell & Brainard has narrowed in recent days, leaving Powell priced at 67c, with Brainard on 32c.

- One development to note is the recent withdrawal of former Fed Vice Chair, Roger Ferguson, from a role at Apollo Global Management (before he even started work). Ferguson apparently has unspecified commitments he must fulfil with his prior employer (pension firm TIAA), which prevented him from taking up the role at Apollo. Ferguson may enter the running for any of the open positions at the Fed, although his chances of attaining the seat atop the central bank are seemingly slim at best.

Fig. 1: Odds re: Whom Will The Senate Next Confirm As Chair Of The Federal Reserve?

Source: MNI - Market News/PredictIt

Source: MNI - Market News/PredictIt

GOLD: DXY Caps Gold, ETFs Not Participating In Latest Rally

Spot gold trades a handful of dollars higher at $1,868/oz at typing. A fresh YtD high for the DXY capped gold on Monday. Our weighted U.S. real yield monitor was ultimately little changed come the close, although underlying worry re: inflation continues to support bullion. Resistance remains intact at the June 14 high ($1,877.7/oz). A break there would expose the June 8 high ($1,903.8/oz). Initial support is seen at the Nov 10 low ($1,822.4/oz).

- It is interesting to note that ETF holdings of gold are essentially unchanged in net terms over the last 6 sessions, after hitting the lowest level witnessed since mid-May '20 in the middle of last week. Still, the rebound from the trough in that metric hasn't been steep. On net, the dynamic in known ETF holdings of gold points to a lack of participation in the latest leg of the gold rally on the part of ETFs, with a steady weekly net liquidation of ETF holdings of gold seen up until last week.

OIL: A Little Firmer In Asia

WTI & Brent crude futures sit ~$0.50 & ~$0.60 above their respective settlement levels in Asia, after the benchmarks were essentially flat on Monday.

- A lack of imminent action from the U.S. re: the release of inventories from its SPR to combat the recent, well-documented rise in gasoline prices has supported crude. White House Press Secretary Psaki once again pointed to the consideration of all of the options available to the Biden administration re: the matter, with markets seemingly tiring of that line of dialect.

- On the broader supply front, a weather-related closure of Canada's Trans-Mountain pipeline has been noted.

- A quick reminder that Monday saw marginal upward revisions to the EIA's U.S. shale production estimates for the month of December.

- The latest round of weekly API crude inventory estimates is due to be released on Tuesday, as is the IEA monthly oil market report.

EQUITIES: Stocks Generally Higher In Asia

A lack of outright hostility in the opening salvos ahead of the Biden-Xi phone call facilitated a warmer risk tone in Asia-Pac hours, with most of the major regional indices moving higher. The concluding comments also pointed to a lack of confrontation re: Taiwan, which would have aided risk appetite further. Casino names listed on the Hang Seng benefited from optimism surrounding regulatory review in Macau, while several Chinese tech names moved higher on the back of a press report which pointed to the Chinese powers that be potentially resuming online game approvals in the near future. Elsewhere, reports surrounding a continued lack of payment of bond coupons on the part of Chinese property developer Kaisa reminded us of the fragile state of affairs that particular sector is facing at present. The ASX 200 was the broader exception to the rule, registering modest losses as material names led the way lower. U.S. e-mini futures are little changed, with Tesla CEO Musk once again headlining in that particular sphere. Musk confirmed the sale of yet more of his equity holdings in the company (~$930mn worth) after he exercised options (the move is essentially tax-related).

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.