Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

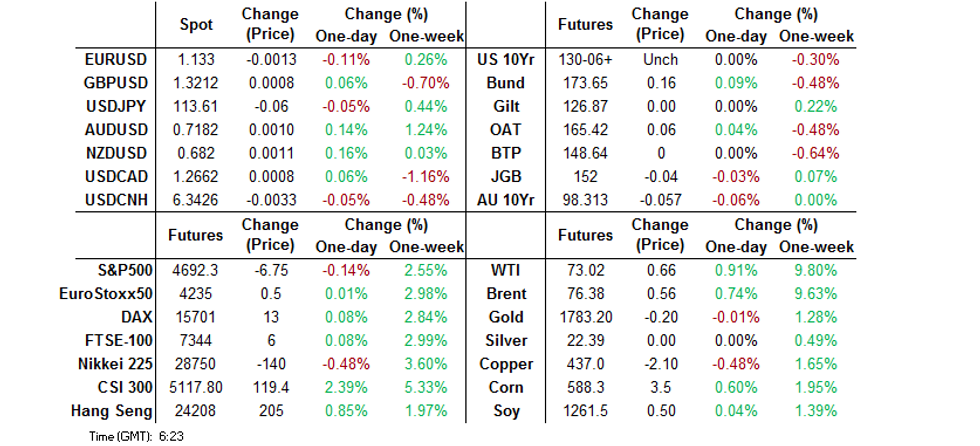

- The CSI 300 hit fresh multi-month highs, while the PBoC fixed USD/CNY a little above exp. i.e. provided a softer than expected fixing for the CNY.

- Worry re: the omicron strain and a troubled Chinese property developer going into receivership applied light pressure to e-minis.

- The global economic docket for the remainder of Thursday is very thin, U.S. weekly jobless claims take focus from here.

BOND SUMMARY: Mixed Performance For Core FI In Asia

U.S. Tsys richened a little overnight, likely drawing support from a study re: the transmissibility/evasive capabilities of the omicron COVID variant. There isn’t much to surprise in the article itself, but the evasive capability of the COVID strain when it comes to infecting the vaccinated/previously infected is once again noted. Reports that Chinese property developer Fantasia entered receivership would have also provided some support. TYH2 last dealing unch. at 130-06+, while cash Tsys run flat to 2.0bp richer on the day, with 20s leading the bid. A 6K block seller of FVH2 was observed overnight. Note that we have seen a block seller of FVH2 futures ahead of London hours Monday-Thursday. Monday, Tuesday and Thursday saw block sales of 6.0K in size, while Wednesday saw a 5.0K block sale. NY hours will see weekly jobless claims data and 30-Year Tsy supply.

- JGB futures edged lower on Wednesday’s U.S. Tsy lead & the weakness observed in broader core global fixed income during early Tokyo trade, before ticking away from worst levels. That left futures -4 at the bell, while cash JGBs run somewhere between -/+0.5bp on the day. We saw a run-of-the-mill round of 5-Year JGB supply. The lack of relative value appeal on the curve, with the aforementioned flatness & richness vs. shorter dated & belly peer JGBs, weighed on the cover ratio. That metric moved away from November’s multi-month high for a 5-Year auction and printed below the 6-auction average (3.98x). We also note that 5s do not provide anything like a comparable carry and roll proposition when looking to longer dated paper, which would disincentivise those looking to enter the long leg of a steepener play at this auction. The tail remained very tight, with the low price just about topping wider expectations (the BBG dealer poll looked for a low price of 100.42).

- Wednesday’s U.S. Tsy price action made for a twist steepening of the ACGB curve, that didn’t really ever go away, even as U.S. Tsys firmed during Thursday’s Asia session. That left YM +1.3 & XM -5.7 come the bell. EFPs narrowed, with the weakness in bonds and reduction in RBA SLF demand covering ’23 & ’24 ACGBs helping ease some of the widening pressure there (at least for now). RBA board member Harper largely echoed Governor Lowe in a BBG interview. Roll flow dominated.

JAPAN: Sizeable Flow Observed In Weekly International Security Flow Data

Japanese investors registered another Y1tn+ week of net selling of foreign bonds last week, with participants seemingly happy to book some profit in the wake of the omicron-inspired richening. Granted, the net level of selling wasn’t quite as large as the multi-month high registered in the previous week, but the 4-week rolling sum of the metric represents the largest level of net selling witnessed since mid-March.

- They were also seemingly happy to buy the omicron dip when it came to offshore equity markets, lodging the largest round of weekly net purchases of foreign equities on record (going back to ’01).

- Elsewhere, foreign investors piled into Japanese bonds, with net purchases topping Y2.0tn, printing at the highest level observed since July’s all-time high, in what could have been a case of cross-currency basis swap pickup being deployed.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -1181.8 | -1337.8 | -2076.5 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 1215.0 | 105.1 | 281.4 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 2005.4 | -451.4 | 3925.8 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | -74.8 | -309.1 | -266.0 |

Source: MNI - Market News/Bloomberg/Japanese Ministry Of Finance

FOREX: Yuan Defies Softer PBOC Fix, Ignores Inflation Data

Offshore yuan appreciated despite the largest miss in the PBOC's daily yuan fixing since mid-October, with central USD/CNY mid-point set 31 pips above sell-side estimate. The redback showed no immediate reaction to China's inflation data, which provided the main highlight of overnight economic calendar. CPI growth accelerated to +2.3% Y/Y, the fastest pace since Aug 2020, but missed median estimate of +2.5%. Factory-gate inflation slowed to +12.9% Y/Y, printing above consensus forecast of +12.1%.

- G10 FX crosses were marginally mixed, the space struggled for a clear uniform direction. Early trade saw the DXY extend its move away from yesterday's low, but the index lost steam and trimmed gains. CAD continued to trade on a softer footing in the wake of Wednesday's monetary policy announcement from the local central bank.

- The global economic docket for the remainder of Thursday is very thin, U.S. weekly jobless claims take focus from here.

FOREX OPTIONS: Expiries for Dec09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1380-00(E978mln), $1.1425(E534mln), $1.1560-70(E1.1bln)

- USD/JPY: Y113.00-25($1.6bln), Y114.00-20($2.4bln)

- EUR/GBP: Gbp0.8550-60(E694mln)

- AUD/USD: $0.7250-60(A$567mln)

- USD/CNY: Cny6.34($2.3bln), Cny6.43($1.1bln); Cny6.3500($1.8bln)

ASIA FX: China Inflation Data Shrugged Off, Asia FX Bid As Omicron Musings Take Focus

The Asia-Pacific caught up with Wednesday's comments from Pfizer/BioNTech, who said a lab study showed that their Covid-19 booster jab generates sufficient immunity against the Omicron variant. The news generated an initial risk-on impulse. An early Japanese study pointing to the high transmissibility of the new variant was a fly in the ointment, but USD/Asia crosses generally continued to trade below neutral levels.

- CNH: USD/CNH went offered despite a considerably softer than expected yuan fixing, which missed sell-side estimate by 31 pips, the most since mid-Oct. China's inflation data were mixed and provoked no tangible market reaction, as consumer price growth accelerated less than expected, while factory-gate inflation slowed less than forecast.

- KRW: Spot USD/KRW operated in negative territory, as positive musings surrounding the global Covid-19 situation yet again overshadowed a worsening local outbreak. South Korea's daily cases stayed above 7,000, while critical cases hit another record high.

- IDR: Spot USD/IDR reopened lower, seemingly thanks to yesterday's Pfizer/BioNTech comments, but trimmed losses later on. Domestic headline flow failed to provide much of real note.

- MYR: The ringgit extended losses to its worst levels since Dec 1, local jobs market data may have provided some incremental support, despite its backward-looking nature. The unemployment rate edged lower in October, while participation expanded a tad.

- PHP: Spot USD/PHP registered its worst levels in more than three weeks, before ticking away from there. The Philippine infectious diseases panel said they are not planning to implement a face shield mandate anytime soon, despite the emergence of a new coronavirus variant.

- THB: Spot USD/THB went offered and approached its 50-DMA, but stopped short of testing that moving average. Thailand's consumer confidence improved to 44.9 in November from 43.9 recorded in the previous month. Comments from BoT Gov Sethaput were eyed.

EQUITIES: New Multi-Month Highs For The CSI 300, Mixed Performance Elsewhere

Hopes re: deeper policy easing in China & supportive cross borders flows have allowed China’s CSI 300 to register a fresh multi-month high (see earlier bullet for more colour on that matter).

- Still, it wasn’t all rosy. The Nikkei 225 and the ASX 200 edged lower, with U.S. e-mini futures also recording modest losses (~0.2%). A story re: the evasive nature of the omicron COVID variant, when it comes to bypassing antibodies, provided some modest headwinds for risk assets, although there wasn’t much to note in that particular story, making for modest moves.

GOLD: Coiling Ahead Of U.S. CPI.

Spot has held to a narrow range in Asia, benefitting from some modest risk-off flows as we grind towards European trade, last dealing marginally higher on the day, printing $1,785/oz. U.S. real yields remain at the fore for bullion, with spot holding within the recently established range, leaving familiar technical boundaries intact. Focus remains squarely on Friday’s U.S. CPI report. ETF holdings of gold have unwound around 50% of their very modest late November bounce, holding around the lowest level witnessed since the all-time peak registered in Oct ’20. That leaves that metric 10.5% shy of record levels, but it still remains elevated in a historical sense.

OIL: Higher, But Off Best Levels

WTI & Brent futures are off of best levels, with e-minis edging lower on the back of negative reports re: the capability of omicron when it comes to evading antibodies. Still, the benchmarks trade ~$0.60 higher on the day, with that particular source of worry providing little in the way of fresh, meaningful information when it comes to the newest COVID strain.

- The earlier pop higher didn’t have anything in the way of overt headline drivers. Bulls have forced WTI & Brent above $73 & $76 respectively. The benchmarks recouped ~$11/bbl in the rally from last week’s lows to Asia session highs, with broader omicron fear fading, providing more faith in medium-term oil demand outlooks. From a technical perspective, the 50-day EMAs in both contracts provide the next real target for bulls, after the benchmarks extended through their previous week-to-date peaks on the run higher in Asia-Pac trade (which pointed to a technical/flow-driven move, given the lack of headline flow).

- Matters re: Iran will garner interest in the coming days, with the U.S. Special Envoy for Iran set to travel to Vienna over the coming weekend. He will meet with world powers re: reviving Iran's 2015 nuclear deal.

CHINA STOCKS: Multi-Month Highs For CSI 300 On Hope For Deeper Policy Easing

The recently announced 50bp RRR cut from the PBoC has opened up the gates when it comes to speculation re: further loosening of PBoC monetary policy settings.

- This view has gained further credence in the wake of a WSJ article pointing to senior CCP members pressuring the PBoC into the RRR cut, which went against recent guidance issued by some of the Bank’s own senior leadership team. A sign that President Xi was keen to exert influence.

- Elsewhere, the readout at the end of the recent Politburo meeting struck a dovish tone, with focus centring on tweaks to the language surrounding the property space in the wake of the well-documented headwinds currently pressuring the sector (which accounts for ~25% of broader Chinese economic activity, based on a relatively wide range of estimates), as well as a more pro-growth orientation in general.

- The prospect of deeper policy easing in China, alongside a more-growth friendly approach & reduced worry re: the mortality threat posed by the omicron COVID strain, has supported the CSI 300.

- This has allowed the index to move to the highest levels observed since July during today’s morning session, closing the gap lower from the 23 July close, clearing the 200-DMA in the process. Bulls now look to the 38.2% retracement of the Feb-July drawdown (5,147.90).

- Note that the 21- & 50-DMAs have started to turn upwards, while the 200-DMA is still downward sloping.

- The 14-day RSI has moved above the 70 mark i.e. into overbought territory, but this is not considered a bearish signal until we see a pullback below that particular line in the sand.

- Observable international capital flows have also been supportive for the Chinese equity space, with 7 consecutive sessions of net buying via the northbound leg of the Hong Kong-China stock connect schemes observed as of typing. This morning’s session has positioned net buying via this channel at the highest level witnessed since June, although this could of course change during the afternoon.

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.