Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Chinese tech woes and the latest North Korean missile launch provided a slightly defensive tilt when it came to Asia-Pac trade.

- USD/JPY printed as low as Y115.90 before reclaiming the Y116 handle. USD/KRW nears KRW1,200, resulting in speculation re: the potential for official intervention to stem KRW losses.

- Final services & composite PMI data from the Eurozone headlines the pre-NY docket, while U.S. ADP employment data and the minutes from the most recent FOMC decision will garner most of the attention later on Wednesday.

BONDS: Tight Asia Ranges For Core FI

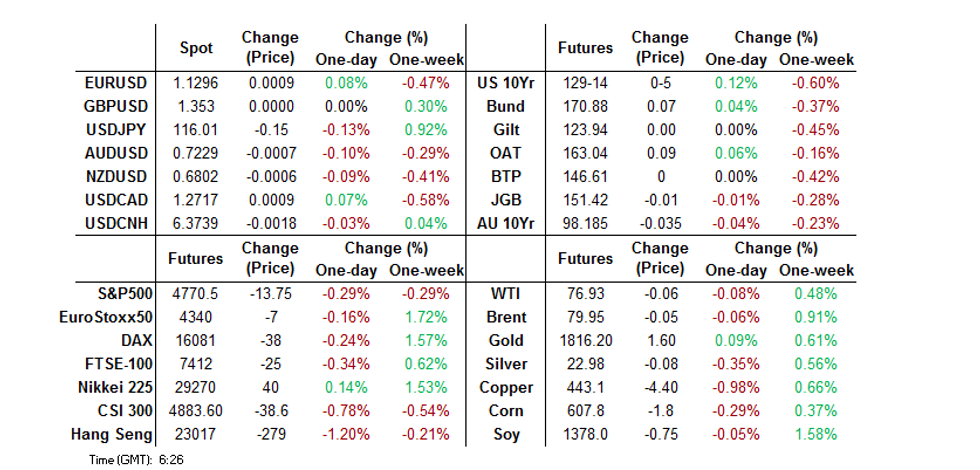

T-Notes operated in a narrow (0-04+) range in Asia, drawing very modest support from the downtick in e-minis. The latter sit 0.3-0.6% lower, on the back of the latest North Korean missile launch and another round of weakness in Chinese equities (driven by further regulatory oversight on the tech sphere). TYH2 last +0-05 at 129-14. Cash Tsys run little changed to ~2bp richer, with 30s outperforming. Broader headline and market flow remains fairly limited. NY hours will see the release of ADP employment data and the minutes from the FOMC’s December meeting. Re: the latter, markets will be looking for any discussion on how soon the central bank may hike rates after the tapering process is concluded and further details surrounding balance sheet normalisation.

- The JGB space coiled during Tokyo trade, with cash yields -/+0.5bp vs. Tuesday’s closing levels come the bell (mostly richer). Futures unwound their overnight losses as U.S. Tsys nudged higher on the aforementioned drivers. The latest round of 10-Year JGB supply passed smoothly, with the low price topping broader dealer expectations as the tail narrowed incrementally vs. the Dec auction, while the cover ratio nudged higher, moving above its 6-auction average. JGB futures ticked higher in the wake of the auction, with demand no doubt supported by the carry and roll aspect that we flagged in our auction preview. Still momentum faltered a little into the close, with the contract finishing -1 on the day.

- Aussie bonds held onto the overnight steepening impetus, with a lack of notable local headline flow leaving the space at the mercy of broader macro drivers. YM unch. & XM -3.5 at the bell. The longer end of cash ACGB curve has cheapened by the best part of 5bp. Soft ANZ job ads data (accompanied by positive revisions) did little for the space, with the data provider noting that “the record employment gain of 366,100 in November was likely a significant factor behind the fall, but we can’t rule out some dampening effect from Omicron. Still, Job Ads are 4.2% above the pre-Delta-lockdown peak in June 2021 and 36.8% above the pre-COVID level.”

JGBS AUCTION: 10-Year JGB Auction Results

The Japanese Ministry of Finance (MOF) sells Y2.0978tn 10-Year JGBs:

- Average Yield 0.096% (prev. 0.060%)

- Average Price 100.03 (prev. 100.38)

- High Yield: 0.097% (prev. 0.063%)

- Low Price: 100.02 (prev. 100.36)

- % Allotted At High Yield: 38.3637% (prev. 63.0466%)

- Bid/Cover: 3.458x (prev. 3.164x)

JGBS AUCTION: 3-Month Bill Auction Results

The Japanese Ministry of Finance (MOF) sells Y4.0667tn 3-Month Bills:

- Average Yield -0.1181% (prev. -0.1128%)

- Average Price 100.0285 (prev. 100.0303)

- High Yield: -0.1078% (prev. -0.1098%)

- Low Price 100.0260 (prev. 100.0295)

- % Allotted At High Yield: 26.3636% (prev. 77.3480%)

- Bid/Cover: 3.112x (prev. 4.470x)

FOREX: KRW On The Defensive, Early JPY Strength Fades

Early Asia trade saw the JPY benefit from defensive flows surrounding the Chinese tech space and the latest North Korea projectile launch. That bid has faded a little, with USD/JPY printing back above Y116.00 after showing as low as Y115.90 in Tokyo dealing.

- Commodity-tied FX nudged lower on the back of those defensive flows, although broader FX trade was limited, with the major USD crosses trading within 10 pips of Tuesday’s closing levels ahead of European dealing.

- The KRW has traded on the backfoot, with the latest North Korean missile launch weighing on both the currency and KOSPI, with the downtick in the KOSPI (linked to the broader tech space woes) likely weighing on the KRW. USD/KRW is printing just shy of the KRW1,200 level as a result (a level not tested since October). Note that there is some market speculation that Korean authorities could step in to limit KRW weakness around this psychological level.

- Final services & composite PMI data from the Eurozone headlines the pre-NY docket, while U.S. ADP employment data and the minutes from the most recent FOMC decision will garner most of the attention later on Wednesday.

FX OPTIONS: Expiries for Jan05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1190-00(E673mln), $1.1285-90(E539mln)

- USD/JPY: Y113.45-55($960mln)

EQUITIES: Tech Continues To Struggle

Tuesday’s tech share weakness (mostly driven by Chinese regulatory & U.S. Tsy-related pressure) continued in Asia-Pac trade, weighing on the Hang Seng & the KOSPI in particular. Note that the latest batch of regulatory fines dealt out to 3 Chinese tech giants and asset disposal from Tencent applied further pressure to the space.

- North Korea’s latest projectile launch applied further pressure, although the broader risk-off moves in the wake of that particular event weren’t particularly sharp.

- E-minis have nudged lower, shedding 0.2-0.4%, with the NASDAQ 100 leading the way lower there.

GOLD: Flatlining In Asia

Tuesday saw a divergence in U.S. nominal yields & breakevens, which resulted in an uptick in real yields. Still, the move was more notable in the longer end of the real yield space, which meant that the impact on gold prices was not particularly profound. This meant that bullion only managed a shallow showing below $1,800/oz, before correcting from worst levels. Spot then clung to a narrow range in Asia, last dealing unchanged at $1,815/oz, with familiar technical parameters in play.

OIL: Oil Little Changed In Asia, Brent Holds Below $80

WTI & Brent crude futures have shed ~$0.15 vs. Tuesday’s settlement levels. Early defensive posturing across broader markets applied some modest pressure to the crude benchmarks, which have since recovered from worst levels. Asia ranges were tight (~$0.60).

- This comes after OPEC+ lifted its cumulative February oil output target by 400K bpd, matching broader expectations. The group now sees a tighter oil market in Q122 when compared to its Dec projections, signalling a lack of worry when it comes to the impact of the Omicron COVID variant. Brent briefly showed above $80.00 on Tuesday but couldn’t hold the move.

- The latest round of weekly U.S. API inventory estimates reportedly revealed a sharper than expected headline drop in crude stocks, alongside wider than expected builds in gasoline and distillate stocks, in an addition to an uptick in stocks at the Cushing hub. The release had no tangible impact on crude futures.

- Weekly U.S. DoE inventory data will be eyed on Wednesday.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/01/2022 | 0745/0845 | ** |  | FR | Consumer Sentiment |

| 05/01/2022 | 0815/0915 | ** |  | ES | IHS Markit Services PMI (f) |

| 05/01/2022 | 0845/0945 | ** |  | IT | IHS Markit Services PMI (f) |

| 05/01/2022 | 0850/0950 | ** | | FR | IHS Markit Services PMI (f) |

| 05/01/2022 | 0855/0955 | ** |  | DE | IHS Markit Services PMI (f) |

| 05/01/2022 | 0900/1000 | ** |  | EU | IHS Markit Services PMI (f) |

| 05/01/2022 | 1000/1100 | *** | | IT | HICP (p) |

| 05/01/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 05/01/2022 | 1315/0815 | *** | | US | ADP Employment Report |

| 05/01/2022 | 1330/0830 | * |  | CA | Building Permits |

| 05/01/2022 | 1445/0945 | *** | | US | IHS Markit Services Index (final) |

| 05/01/2022 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 05/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 05/01/2022 | 1900/1400 | * | | US | FOMC Minutes |

| 06/01/2022 | 2200/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.