Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Most of the major regional equity indices ticked higher in Asia, although the Nikkei 225 struggled on domestic COVID worry.

- JGB futures spiked lower at the close, with some pointing to NFP-related hedging ahead of the long Tokyo weekend as a driving factor.

- While the U.S. NFP report provides the focal point today, flash EZ CPI, German industrial output and Canadian jobs data are also due. The central bank speaker slate features Fed's Daly & Bostic as well as BoE's Mann.

BOND SUMMARY: JGBs Sell Off At Bell, Markets Await NFPs

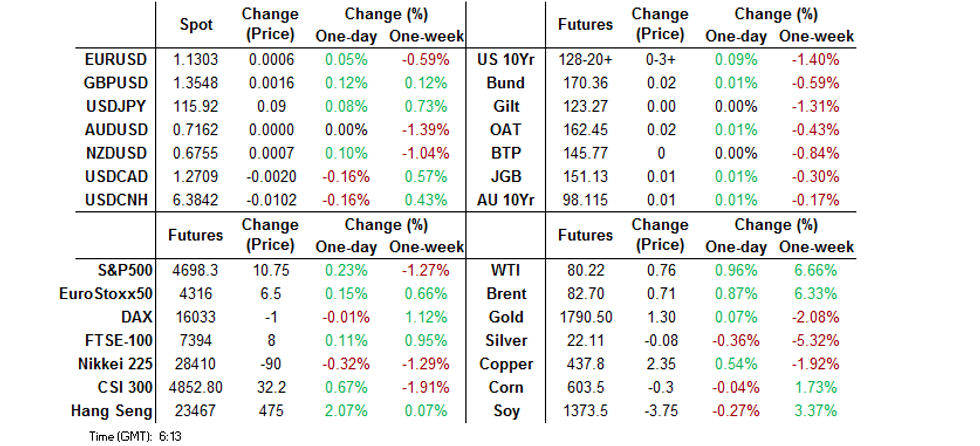

Tsys have moved away from best levels but remain in limited range. TYH2 +0-02+ at 128-19+ at typing, operating within a 0-05+ trading band, while cash Tsys sit little changed to 1.0bp cheaper across the curve. There has been a lack of meaningful news flow during asia hours, with participants focused on Friday’s NFP release. A block trade consisting of the sale of FVG2 120.00 puts (-15.0K) and FVH2 buying (+8K) headlined on the flow side. As mentioned, focus is squarely on Friday’s NFP report, with the recent hawkish repricing in the front end of the Tsy curve & STIRs providing the potential for increased volatility if the dataset disappoints. Elsewhere, Fedspeak will come from ’24 voters Bostic & Daly.

- JGB futures initially unwound their overnight weakness on local COVID worry (potential for a delay re: the Go To travel campaign & for a quasi state of emergency declaration in a handful of prefectures). That was before a sharp bout of selling hit the contract into the bell, leaving it -15 at the close. This was perhaps a result of some pre-U.S. NFP worry in thin markets ahead of elongated Tokyo weekend. Elsewhere, 30-Year JGB supply went well, with the tail narrowing and cover ratio moving higher when compared to last month’s auction. More granularly, the cover ratio hit the highest level seen at a 30-Year auction since July, residing comfortably above the 6-month average. Elsewhere, the low price also topped broader dealer expectations. Outright interest on the back of multi-month high yields and the previously outlined long end interest on the part of Japanese life insurers likely drove demand at the auction. Cash yields were marginally higher (<+1.0bp) across most of the curve.

- Aussie bonds benefitted from the reinstatement of some COVID-related limits in NSW, although the moves weren’t particularly pronounced. YM +2.0 and XM +1.0 at the bell as a result. There wasn’t anything in the way of a notable market reaction to the AOFM declaring that “a new November 2033 Treasury Bond will be issued by syndication in the final quarter of 2021-22 (subject to market conditions),” with a lack of Q122 syndication and a run of the mill extension of the 10-Year futures basket providing no headwinds for the space.

JGBS AUCTION: Japanese MOF sells Y732.1bn 30-Year JGBs:

The Japanese Ministry of Finance (MOF) sells Y732.1bn 30-Year JGBs:

- Average Yield 0.719% (prev. 0.673%)

- Average Price 99.51 (prev. 100.65)

- High Yield: 0.720% (prev. 0.677%)

- Low Price 99.50 (prev. 100.55)

- % Allotted At High Yield: 88.4482% (prev. 14.8255%)

- Bid/Cover: 3.629x (prev. 3.214x)

JGBS AUCTION: Japanese MOF sells Y4.0667tn 3-Month Bills:

The Japanese Ministry of Finance (MOF) sells Y4.0667tn 3-Month Bills:

- Average Yield -0.1054% (prev. -0.1181%)

- Average Price 100.0260 (prev. 100.0285)

- High Yield: -0.0993% (prev. -0.1078%)

- Low Price 100.0245 (prev. 100.0260)

- % Allotted At High Yield: 56.7007% (prev. 26.3636%)

- Bid/Cover: 2.937x (prev. 3.112x)

AUSSIE BONDS: AOFM Releases Weekly Issuance Slate & Details Of ’22 Syndications

The AOFM has released its weekly issuance slate:

- On Wednesday 12 January it plans to sell A$1.0bn of the 1.75% 21 November 2032 Bond.

- On Thursday 13 January it plans to sell A$1.0bn of the 13 May 2022 Note.

- On Friday 14 January it plans to sell A$1.0bn of the 0.25% 21 November 2025 Bond.

- The AOFM also notes that “this notice provides updated details of planned issuance of Australian Government Securities by the Australian Office of Financial Management (AOFM) for the remainder of 2021-22. At MYEFO the AOFM indicated planned Treasury Bond issuance of around A$105 billion (of which A$44.3 billion has been completed). Two tenders will be conducted most weeks. A new November 2033 Treasury Bond will be issued by syndication in the final quarter of 2021-22 (subject to market conditions). Planned issuance of Treasury Indexed Bonds is A$5-5.5 billion (of which A$4.1 billion has been completed). Two tenders will be held most months. Regular issuance of Treasury Notes will continue. Weekly issuance volumes will depend on the timing and size of government receipts and outlays and the AOFM’s assessment of its cash portfolio requirements.

JAPAN: Little To Shout About In Weekly International Security Flow Data

Weekly international security flow data out of Japan provided the following observations:

- Japanese investors registered a third straight weekly round of net selling of foreign bonds, with the 4-week rolling sum of the measure remaining comfortably in negative territory, even as a Y1tn+ round of weekly net selling dropped out of the sample period.

- Foreign investors reverted to net purchases of Japanese bonds (albeit in a limited fashion, with liquidity thinned owing to the time of year) after shedding over Y1tn of Japanese paper in the previous week. This was the fourth week out of the last five which saw net purchases of Japanese bonds on the part of foreign investors.

- Japanese investors net purchased foreign equities for a sixth consecutive week, although the 4-week rolling sum fell as a large round of weekly net purchases fell out of the sample.

- Foreign investors registered another round of limited net purchases when it came to Japanese equities, with the 4-week rolling sum of that measure still residing comfortably in negative territory.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -416.5 | -310.0 | -1854.9 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 213.6 | 131.7 | 793.0 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 447.2 | -1221.6 | 1637.6 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 17.1 | 124.5 | -1306.1 |

FOREX: Dollar Slips With NFP Front & Centre

Thursday's risk aversion petered out as participants were preparing for the release of U.S. labour market data. The report will receive close scrutiny amid attempts to forecast the trajectory of policy tightening by the Federal Reserve, following this week's hawkish repricing on that front.

- The DXY slipped in Asia-Pac trade, indicating the dissipation of broader demand for the greenback. This helped drag USD/CNH lower, even as the ongoing outbreak of Covid-19 in several location across China continued to stoke concerns.

- NOK and CAD held firm, even as their commodity-tied peers AUD and NZD lost their initial appeal. The yen remained the worst G10 performer, albeit USD/JPY gave up almost all of its early gains.

- While U.S. NFP report provides the sole focal point today, flash EZ CPI, German industrial output and Canadian jobs data are also due. The central bank speaker slate features Fed's Daly & Bostic as well as BoE's Mann.

FOREX OPTIONS: Expiries for Jan07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250(E982mln), $1.1290-00(E1.5bln), $1.1350-53(E905mln)

- USD/JPY: Y116.00($2.5bln)

- AUD/USD: $0.7160(A$2.1bln), $0.7200(A$1.3bln), $0.7250-55(A$728mln)

- USD/CAD: C$1.2650($665mln), C$1.2675-90($1.3bln), C$1.2700($581mln), C$1.2800($639mln)

ASIA FX: Asia EMFX Trade Mixed Before NFP Release

Currencies from the Asia EM basket traded mixed, with participants bracing themselves for the release of the latest jobs market data out of the U.S. later today. Covid-19 dynamics in different regional localities drew attention, as some Asian nations moved to tighten restrictions.

- CNH: Offshore yuan went bid in spite of the ongoing spread of Covid-19 infections, concentrated in Shaanxi and Henan. Pre-NFP greenback weakness likely helped drag USD/CNH lower.

- KRW: Spot USD/KRW operated in positive territory, as onshore won was wounded by Fed tightening talk. Samsung's earnings missed estimates in Q4, but this was due to the payment of a one-off bonus to employees.

- IDR: The rupiah led gains in Asia, even as Indonesia's daily Covid-19 caseload topped 500 on Thursday. The authorities said in December that they might tighten restrictions if that threshold is met.

- MYR: Spot USD/MYR retreated after Health Min Khairy pledged that the gov't will avoid re-imposing lockdown as much as possible.

- PHP: The Philippine peso struggled for any momentum after the gov't tightened restrictions in a number of areas, while Pres Duterte warned that unvaccinated people who ignore stay-at-home orders may face arrest.

- THB: The baht came under pressure as Thailand's Covid-19 task force debated fresh containment measures, clouding the outlook for the critically important domestic tourism industry.

EQUITIES: Japan Struggles On COVID Woes

The major Asia-Pac equity indices were mixed during the final session of the week, with participants keenly awaiting the impending U.S. NFP report.

- Local omicron worries weighed on Japanese equities, with reports pointing to the potential for a delay when it comes to the restart of the Go To travel campaign and rising chances re: the declaration of a quasi state of emergency in a handful of Japanese prefectures dominating Japanese headline flow. This allowed the Nikkei 225 to unwind its early gains, with the index trading in negative territory ahead of the close.

- The remainder of the major regional equity indices ticked higher. Chinese equities benefitted from another bout of reassuring rhetoric from the top Chinese regulatory body (delivered late Thursday). Elsewhere, Chinese state-owned developers supported the property sector, after reports suggested that M&A loans will not be included in China’s three red lines surrounding debt. It wasn’t all rosy in the developer space, after one of Shimao’s units missed payment on a domestic loan, triggering discussion re: the scope of contagion that could grip the sector.

GOLD: Technicals Continue To Contain Broader Price Action

Gold remains in familiar territory, with spot dealing a touch above $1,790/oz at typing, holding a tight range during Asia-Pac dealing.

- Bullion continues to operate within the confines of well-defined technical parameters. As a reminder, support comes in at the channel base drawn from the Aug 9 low, while key near-term resistance is seen at the Jan 3 high ($1,831.9/oz).

- Friday’s NFP print provides the key risk event during the remainder of the week. Note that a softer than expected round of NFP data would provide the potential for increased volatility (at least intraday), owing to the hawkish repricing (re: the Fed) witnessed since the release of the minutes covering the FOMC’s December meeting.

OIL: Modest Gains In Asia

WTI & Brent futures added ~$0.50 overnight. Geopolitical risk surrounding Kazakhstan continues to garner attention, generating support for oil, even though there hasn’t been anything in the way of reports pointing to any meaningful disruption when it comes to the country’s crude supply. Elsewhere, Libyan crude production remains sub-par, with plenty of questions already apparent re: OPEC+’s ability to continually execute when it comes to higher output (without adjusting the country splits when it comes to quota allocations).

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/01/2022 | 0645/0745 | ** |  | CH | unemployment |

| 07/01/2022 | 0700/0800 | ** |  | DE | industrial production |

| 07/01/2022 | 0700/0800 | ** | | DE | trade balance |

| 07/01/2022 | 0700/0700 | * |  | UK | Halifax House Price Index |

| 07/01/2022 | 0730/0830 | ** | | CH | retail sales |

| 07/01/2022 | 0745/0845 | ** |  | FR | Consumer Spending |

| 07/01/2022 | 0745/0845 | * | | FR | industrial production |

| 07/01/2022 | 0745/0845 | * | | FR | foreign trade |

| 07/01/2022 | 0745/0845 | * | | FR | current account |

| 07/01/2022 | 0930/0930 | ** | | UK | IHS Markit/CIPS Construction PMI |

| 07/01/2022 | 1000/1100 | ** |  | EU | Economic Sentiment Indicator |

| 07/01/2022 | 1000/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 07/01/2022 | 1000/1100 | * | | EU | Business Climate Indicator |

| 07/01/2022 | 1000/1100 | *** | | EU | HICP (p) |

| 07/01/2022 | 1000/1100 | ** | | EU | retail sales |

| 07/01/2022 | 1330/0830 | *** |  | CA | Labour Force Survey |

| 07/01/2022 | 1330/0830 | *** |  | US | Employment Report |

| 07/01/2022 | 1500/1000 | * | | CA | Ivey PMI |

| 07/01/2022 | 1500/1000 | | US | San Francisco Fed's Mary Daly | |

| 07/01/2022 | 1600/1600 | | UK | BOE Mann at CFR meeting | |

| 07/01/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 07/01/2022 | 1715/1715 | | UK | BOE Mann on panel at AEA | |

| 07/01/2022 | 1715/1215 | | US | Atlanta Fed's Raphael Bostic | |

| 07/01/2022 | 2000/1500 | * | | US | Consumer Credit |

| 08/01/2022 | 1400/1500 | | EU | ECB Schnabel at AEA meeting | |

| 08/01/2022 | 1500/1500 | | UK | BOE Mann on panel at AEA | |

| 08/01/2022 | 1715/1715 | | UK | BOE Mann on panel at AEA | |

| 08/01/2022 | 1715/1215 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.