Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

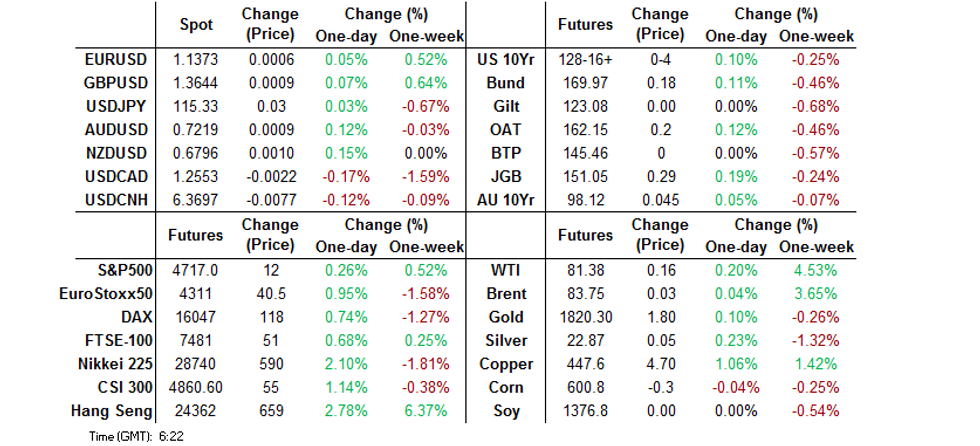

- Asia-Pac equities benefitted from the positive Wall St. lead and softer than expected Chinese inflation data.

- JGB futures unwound yesterday's weakness, with no major news flow observed.

- While U.S. inflation data will certainly take centre stage today, it is worth noting that there are speeches coming up from Fed's Kashkari & BoE's Cunliffe.

BOND SUMMARY: JGB Futures Pop, Core FI Limited Elsewhere Ahead Of U.S. CPI

Core FI markets struggled to find much in the way of clear impetus during Asia-Pac hours, with focus on the impending U.S. CPI release. Chinese inflation data provided a downside miss. As we noted ahead of that dataset, a decrease in inflationary pressures leaves more room for policy easing (with Beijing already tipping their hat towards more pro-growth policy moves in recent months), but that didn’t do much for the space.

- TYH2 struggled to make headway above Tuesday’s high, last dealing +0-04 at 128-16+, while cash Tsys run within -/+0.5bp of Tuesday’s closing levels. The aforementioned CPI release headlines the NY docket on Wednesday, with average hourly earnings also due. Supply comes in the form of 10-Year Tsys, while Fedspeak from Minneapolis Fed President Kashkari (’23 voter, dove) also on the slate.

- JGB futures popped higher, with nothing in the way of overt catalysts observed (a reminder that speculation surrounding the potential for CTA a/c selling weighed on futures on Tuesday). The contract reclaimed the 151.00 level, finishing +29. Futures were in the driving seat when it came to cash JGB trade, with 7s outperforming, as benchmark JGBs printed little changed to ~3.0bp richer across the curve. 5-Year JGB supply wasn’t the firmest in recent history. The cover ratio slipped to print at the lowest level witnessed at a 5-Year JGB auction since May ’21, comfortably below the 6-auction average, although the price tail only experienced an incremental widening, holding tight. The low price met broader dealer expectations. BoJ Governor Kuroda stuck to the well-worn script in his latest address, while the BoJ upgraded its economic assessment of all nine of the Japanese geographical regions that it covers.

- Aussie bond futures seemed to benefit from the bid in JGBs and a solid round of ACGB supply. In terms of specifics, the latest ACGB Nov ’32 auction passed smoothly enough, with the weighted average yield printing 0.42bp through prevailing mids (per Yieldbroker), while the cover ratio was comfortably above 3.50x. YM +2.5 & XM +4.5 come the close, with a limited round of Sydney trade noted.

JGBS AUCTION: Japanese MOF sells Y2.0257tn 5-Year JGBs:

The Japanese Ministry of Finance (MOF) sells Y2.0257tn 5-Year JGBs:

- Average Yield -0.041% (prev. -0.086%)

- Average Price 100.23 (prev. 100.44)

- High Yield: -0.037% (prev. -0.084%)

- Low Price 100.21 (prev. 100.43)

- % Allotted At High Yield: 73.6701% (prev. 85.6453%)

- Bid/Cover: 3.336x (prev. 3.626x)

AUSSIE BONDS: The AOFM sells A$1.0bn of the 1.75% 21 Nov ‘32 Bond, issue #TB165:

The Australian Office of Financial Management (AOFM) sells A$1.0bn of the 1.75% 21 November 2032 Bond, issue #TB165:

- Average Yield: 1.8898% (prev. 1.9690%)

- High Yield: 1.8925% (prev. 1.9700%)

- Bid/Cover: 3.6550x (prev. 3.3900x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 4.9% (prev. 89.0%)

- Bidders 48 (prev. 45), successful 26 (prev. 17), allocated in full 15 (prev. 7)

FOREX: Sentiment Stays Buoyant With Inflation Musings Front And Centre

The yen extended losses in muted Asia-Pac trade amid a broadly positive showing from regional equity markets, with participants digesting Tuesday's congressional testimony from Fed Chair Powell. Oil-tied CAD and NOK were in demand, building on yesterday's strength, even as crude prices stabilised.

- Market sentiment was further buoyed by Chinese data, which showed that inflation (both CPI and PPI) slowed more than expected into the year-end, opening up space for local policymakers to take more stimulatory steps. Spot USD/CNH fell to a one-week low in reaction to the release.

- The DXY showed at its lowest point since Nov 30, as selling pressure hit the greenback ahead of the release of U.S. CPI. The data will inform the ongoing discussion about the most likely Fed policy tightening path.

- While U.S. inflation data will certainly take centre stage today, it is worth noting that there are speeches coming up from Fed's Kashkari & BoE's Cunliffe.

FOREX OPTIONS: Expiries for Jan12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1275-85(E618mln), $1.1300-05(E2.4bln), $1.1400(E542mln)

- USD/JPY: Y112.90-10($784mln), Y113.50-70($1.2bln), Y115.50($638mln), Y116.00-05($750mln)

- GBP/USD: $1.3595-00(Gbp797mln)

- EUR/GBP: Gbp0.8494-00(E1.2bln)

- USD/CAD: C$1.2690($1.0bln), C$1.2750-60($1.2bln), C$1.2790($1.8bln)

- USD/CNY: Cny6.4500($1.3bln)

EQUITIES: Powell & Chinese Inflation Support Stocks

The positive lead from Wall St. provided upside impetus for the major regional Asia-Pac equity indices, while weaker than expected inflation data out of China provided another leg of support, as the dataset lifted the prospect of deeper monetary easing from the PBoC.

- Chinese tech benefitted from Tuesday’s outperformance in the NASDAQ, which was a product of the stabilisation/downtick in U.S. Tsy yields. This allowed the Hang Seng to outperform its major regional counterparts, adding a little over 2.0% as of typing.

- U.S. e-mini futures were little changed, consolidating Tuesday’s rally which came on the back of Fed Chair Powell’s failure to introduce any fresh, meaningful hawkish information in his latest testimony on the hill.

GOLD: Rangebound Ahead Of U.S. CPI

Tuesday’s downtick in U.S. real yields & the DXY supported bullion, with spot subsequently dealing little changed around the $1,820/oz mark during Asia-Pac hours.

- A reminder that the technical bull channel and recent range remain well and truly in play, with key resistance located at the Jan 3 high ($1,831.9/oz).

- Note that ETF holdings of gold are off the recent trough, but only incrementally so.

- The latest U.S. CPI release, due later today, provides the most notable immediate risk event for participants to digest.

OIL: Crude Little Changed In Asia

WTI and Brent crude futures are essentially unchanged vs. Tuesday’s settlement levels as of typing, after a brief look above Tuesday’s high during Asia hours. A reminder that a lack of fresh, meaningful hawkish inferences from Fed Chair Powell supported broader risk assets during the second half of NY trade on Tuesday, as the major oil benchmarks added the best part of $3.00 apiece.

- Reports pointed to a smaller than expected drawdown in headline crude stocks in the latest round of API inventory estimates, which was coupled with a drawdown in stocks at the Cushing hub. Meanwhile, gasoline stocks saw a far sharper than expected build, per the same reports. Distillate stocks rounded off the report, experiencing a slightly wider than expected build. The net impact of the report was marginally bearish when it came to the immediate reaction in crude prices, with the builds on the product side dominating the drawdowns outlined above.

- Weekly DoE inventory data out of the U.S provides the focal point for participants on Wednesday.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/01/2022 | 1000/1100 | ** |  | EU | Industrial Production |

| 12/01/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 12/01/2022 | 1330/0830 | *** | | US | CPI |

| 12/01/2022 | 1415/1415 |  | UK | BOE Cunliffe at Crypto Fin Conference | |

| 12/01/2022 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 12/01/2022 | 1630/1130 | * | | US | US Treasury Cash Management Bill Auction Result |

| 12/01/2022 | 1700/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/01/2022 | 1700/1200 | ** | | US | USDA GrainStock - NASS |

| 12/01/2022 | 1700/1200 | *** | | US | USDA Winter Wheat |

| 12/01/2022 | 1800/1300 | ** | | US | US 10 Year Treasury Auction Result |

| 12/01/2022 | 1800/1300 | | US | Minneapolis Fed's Neel Kashkari | |

| 12/01/2022 | 1900/1400 | ** | | US | Treasury Budget |

| 12/01/2022 | 1900/1400 | | US | Fed Beige Book |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.