Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

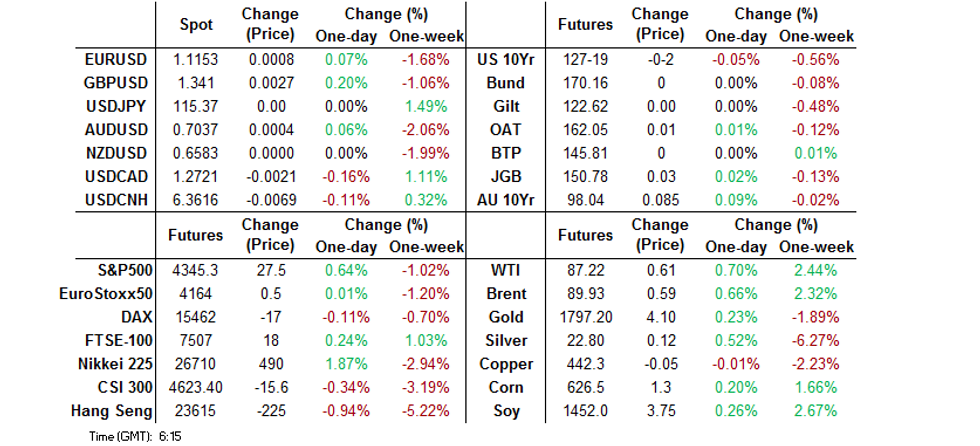

- U.S. e-mini futures edge higher after a strong earnings report from Apple, which helps soothe the nerves at the end of a week which saw the Fed rattle markets with their hawkish turn.

- Marginal weakness in U.S. Tsys, while short-end ACGBs catch mild bid. Australian headline flow is thin, but a WSJ opinion piece pours some cold water on hawkish RBA expectations

- Major currency pairs hold tight ranges, yen struggles amid reduced demand for safe havens. Yuan gains ahead of the week-long Lunar New Year holiday.

BOND SUMMARY: U.S. Tsys Slip As Dust Settles After Fed

The final Asia-Pac session of this lunar year allowed core FI markets to catch a breath after a volatile week dominated by the Fed's hawkish rhetoric and simmering Russia tension. A strong earnings report from Apple has helped soothe the nerves, lending support to U.S. equity index futures.

- T-Notes held a tight range, with a mild bearish bias. TYH2 last trades -0-03 at 127-18, near session lows. Eurodollar futures run 1.0-1.5 tick lower through the reds. Cash Tsys slipped across the curve, with yields seen 0.8-1.8bp higher at typing, with 10-Year Tsys leading losses. Core PCE Price Index & U. of Mich Sentiment headline the U.S. data docket on Friday.

- JGB futures faltered after the re-open to stabilise later on. JBH2 last operates at 150.78, 3 ticks above previous settlement. JGBs are broadly softer, with a degree of steepening evident in cash trade, as the super-long end underperforms. A deceleration in Tokyo CPI inflation underscored the need for the BoJ to stand by their ultra-loose policy stance.

- ACGB curve flattened in cash Sydney trade, with yields last seen 4.3-7.0bp lower. YM remains elevated and last sits +4.0, with XM +6.5 after trading sideways. Bills trade 3-4 ticks higher through the reds. The front end caught a light bid in the afternoon, even as domestic headline flow remained light. It is worth noting that around that time, the WSJ published an opinion piece noting that the RBA could "categorically rule out the idea" that raising interest rates in lockstep with the Fed "is an option." The auction for A$1.0bn worth of ACGB May '32 came and went.

FOREX: Market Sentiment Stabilises

The dust settled after post-FOMC market swings, allowing risk sentiment to stabilise. A strong earnings report from Apple drove a tech-led uptick in U.S. e-mini futures, helping reduce demand for safe haven assets. Major currency pairs were happy to hold tight ranges in the final Asia-Pac session before Lunar New Year holidays.

- The yen traded on a softer footing, with USD/JPY consolidating above breached resistance from Jan 18 high of Y115.06.

- The NZD failed to jump on the risk-on bandwagon and underperformed all of its G10 peers, although domestic headline flow was fairly thin.

- U.S. Core PCE Price Index & final U. of Mich. Sentiment, EZ sentiment gauges as well as flash German & French GDPs take focus from here, in the absence of any notable central bank speak.

FOREX OPTIONS: Expiries for Jan28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1100(E734mln), $1.1130-50(E1.3bln), $1.1200-15(E1.4bln), $1.1300-20(E1.5bln)

- USD/JPY: Y114.00($672mln), Y114.50($645mln), Y115.00($1.3bln), Y115.50($1.5bln), Y115.90-00($1.7bln)

- EUR/JPY: Y126.25(E1.2bln), Y130.00(E1.2bln)

- USD/CAD: C$1.2695-00($709mln)

ASIA FX: Yuan Firms, Asia EM FX Mixed

The yuan edged higher ahead of the week-long Lunar New Year holiday, with Asia EM currencies trading mixed towards the end of a volatile week.

- CNH: Yuan bulls were undeterred by yesterday's sharp rally in spot USD/CNH. The rate slipped in Asia-Pac trade, moving away from a two-week high printed on Thursday. The PBOC set their yuan reference rate at CNY6.3746, just 8 pips above sell-side estimate.

- KRW: Spot USD/KRW punched through key resistance from Jan 7 cycle high of KRW1,203.90 and continued to creep higher, ignoring upbeat factory production data released out of South Korea. The BoK said they will hold a meeting on Feb 3 to review market situation.

- IDR: The rupiah garnered some strength amid stabilisation after the Fed's hawkish announcement.

- MYR: Spot USD/MYR extended losses after December data showed a solid beat in Malaysia's trade surplus, as shipments topped expectations.

- PHP: Spot USD/PHP pulled back after a rejection of resistance from PHP51.500. The peso may have been supported by strong Philippine GDP data released Thursday, as Fed jitters receded. Elsewhere, the Philippines said it will scrap quarantine requirement for fully vaccinated visitors from Feb.

- THB: Spot USD/THB pushed higher before trimming some gains. The Finance Ministry revised 2021 GDP growth forecast to +1.2% Y/Y from +1.0% and kept the 2022 forecast at +4.0%, noting that the Covid-19 outbreak is expected to peak in March.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/01/2022 | 0630/0730 | ** |  | FR | Consumer Spending |

| 28/01/2022 | 0630/0730 | *** | | FR | GDP (p) |

| 28/01/2022 | 0700/0800 | ** |  | SE | Unemployment |

| 28/01/2022 | 0700/0800 | ** | | SE | Retail Sales |

| 28/01/2022 | 0700/0800 | *** | | SE | GDP |

| 28/01/2022 | 0700/0800 | * |  | NO | Norway Unemployment Rate |

| 28/01/2022 | 0700/0800 | ** |  | DE | Import/Export Prices |

| 28/01/2022 | 0745/0845 | ** | | FR | PPI |

| 28/01/2022 | 0800/0900 | *** |  | ES | GDP (p) |

| 28/01/2022 | 0900/1000 | ** |  | IT | ISTAT Consumer Confidence |

| 28/01/2022 | 0900/1000 | ** | | IT | ISTAT Business Confidence |

| 28/01/2022 | 0900/1000 | *** | | DE | GDP (p) |

| 28/01/2022 | 1000/1100 | ** |  | EU | Economic Sentiment Indicator |

| 28/01/2022 | 1000/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 28/01/2022 | 1000/1100 | * | | EU | Business Climate Indicator |

| 28/01/2022 | 1330/0830 | ** |  | US | Personal Income and Consumption |

| 28/01/2022 | 1330/0830 | ** | | US | Employment Cost Index |

| 28/01/2022 | 1500/1000 | *** | | US | Final Michigan Sentiment Index |

| 28/01/2022 | 1600/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.