Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

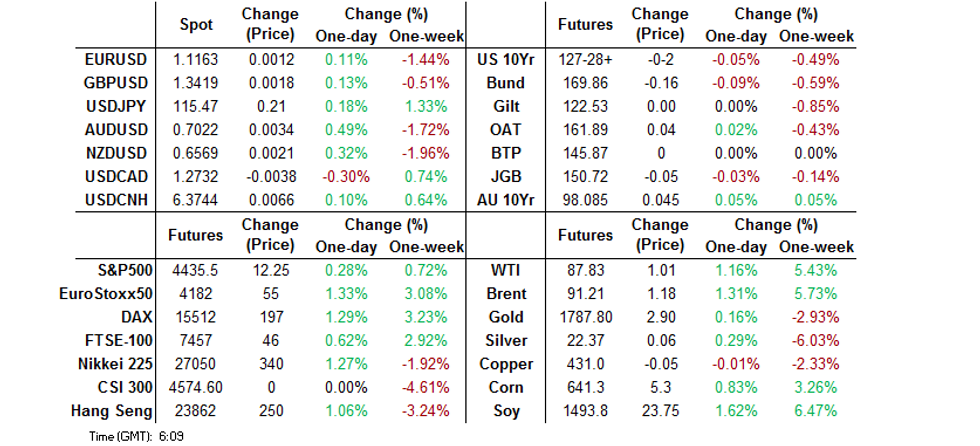

- Atlanta Fed President Bostic alluded to the risks of a swifter pace of rate hikes over the weekend (but stuck to his baseline call of 3 hikes in ’22), this, combined with a more hawkish Fed call from Goldman Sachs (looking for 5x 25bp hikes in ’22 vs. 4x prev.) applied some bear flattening pressure to cash Tsys overnight.

- U.S. e-mini futures unwound their early losses (which were linked to geopolitical worry surrounding Russia & questions re: the hiking trajectory of the U.S. federal Reserve) as we moved through Asia-Pac dealing. A bounce in Chinese tech names listed in Hong Kong aided broader sentiment.

- Advance EZ GDP, flash German CPI, U.S. MNI Chicago PMI & comments from Fed's Daly & George take focus from here.

BOND SUMMARY: U.S. Tsys Bear Flatten, Aussie Bonds Spike Higher At Futures Close

Atlanta Fed President Bostic alluded to the risks of a swifter pace of rate hikes over the weekend (but stuck to his baseline call of 3 hikes in ’22), this, combined with a more hawkish Fed call from Goldman Sachs (looking for 5x 25bp hikes in ’22 vs. 4x prev.) applied some bear flattening pressure to cash Tsys overnight. Participants seemed to look through the continued geopolitical tension surrounding Russia. Still, the Lunar New Year holiday period curtailed broader activity, with TYH2 sticking to the 0-05 range established early on, last -0-03+ at 127-27. Cash Tsys run 1.5-3.5bp cheaper across the curve. TUH2 block activity headlined on the flow front in Asia (with price action pointing to a 6K block buy being followed up with a 6K block sale). Looking ahead, NY hours will see the release of the latest MNI Chicago PMI reading, in addition to the Dallas Fed manufacturing activity print. Meanwhile, Fedspeak will come from Kansas City Fed President George (’22 voter) & San Francisco Fed President Daly (’24 voter)

- 10-Year JGB yields ticked higher in early afternoon trade, topping 0.180%, hitting the highest level since early ’16 in the process. There wasn’t an outright trigger for the move, outside of technical breaks in both 10-Year JGB yields and JGB futures, although the space pared the move as we worked towards the Tokyo close. That left futures -5 at the bell, while cash JGBs were little changed to ~2.5bp cheaper, as the super-long end led the weakness.

- In the ACGB space, it looked like pre-RBA short covering came to the fore at the bond futures close, with YM spiking higher, making fresh session highs. That left the contract +10.0 at settlement, while XM was +4.5. ACGBs outperformed during Asia trade, with incumbent PM Morrison struggling in the polls (although he just about retained his preferred PM status in the most recent Newspoll offering) and some pre-RBA caution supporting the space for much of Sydney trade. The spike higher in YM also supported the IR strip into the bell.

FOREX: High-Betas Gain In Risk-On Trade

Improvement in broader risk sentiment (U.S. e-mini futures turned green) and an uptick in crude oil prices supported high-beta FX space at the start to the week. Liquidity was drained by holiday market closures in China, South Korea and New Zealand's Auckland, with a couple of regional financial centres observing shortened trading hours.

- The AUD firmed ahead of the RBA's monetary policy decision due tomorrow. The Reserve Bank are expected to scrap their QE programme and update their forward guidance re: interest rates.

- The yen went offered amid reduced demand for safe havens. The fact that Sunday was a Gotobi day may have exacerbated the yen's woes. Risk barometer AUD/JPY briefly showed above the Y81.00 mark.

- The U.S. dollar index (DXY) lost steam after the Fed's hawkish pivot rattled markets last week. That being said, the extremes of last Friday's range remained intact.

- Advance EZ GDP, flash German CPI, U.S. MNI Chicago PMI & comments from Fed's Daly take focus from here.

FOREX OPTIONS: Expiries for Jan31 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1100(E1.3bln), $1.1370-90(E715mln)

- USD/JPY: Y114.00($850mln), Y114.95-05($1.1bln), Y117.00($1.2bln)

- AUD/USD: $0.7300-15(A$587mln)

- USD/CAD: C$1.2550-60($931mln)

ASIA FX: Holiday Market Closures Limit Activity Across Asia

Market closures in several Asian economies (China, South Korea, Taiwan) and shortened trading hours in others (Malaysia, Hong Kong) limited activity on Monday.

- CNH: Spot USD/CNH crept higher after initially holding a very tight range. The rate tested Jan 27 two-week high of CNH6.3758 but struggled to make much headway beyond there. China's Caixin Manufacturing PMI released over the weekend unexpectedly slipped into contractionary territory.

- IDR: Spot USD/IDR re-opened on a firmer footing, but trimmed gains thereafter. Domestic headline flow was light.

- MYR: The ringgit inched higher, despite a rise in Malaysia's daily Covid-19 cases (but not hospitalisations or ICU admissions).

- PHP: Spot USD/PHP extended its pullback from hey resistance at PHP51.500, printing its worst levels in two weeks. The peso gained after the Philippine Covid-19 task force eased curbs in Metro Manila and several other areas.

- THB: The baht faltered, even as Thailand's factory output grew faster than forecast. BoP current account balance & trade balance are due later in the day.

EQUITIES: E-minis Unwind Losses, Chinese Tech Nudges Higher

U.S. e-mini futures unwound their early losses (which were linked to geopolitical worry surrounding Russia & questions re: the hiking trajectory of the U.S. federal Reserve) as we moved through Asia-Pac dealing. A bounce in Chinese tech names listed in Hong Kong aided broader sentiment, as that space benefitted from another round of hope that the worst is behind us when it comes to the regulatory clampdown on the sector, in addition to a technical bounce and some speculation re: month-end rebalancing flows. Japanese equities also ticked higher on the day, while Australia’s ASX 200 lodged modest losses. A reminder that Chinese markets were closed for the Lunar Year Holiday, with Hong Kong markets ceasing trade at lunch time, owing to the observance of the same holiday.

GOLD: Marginally Lower To Start The Week

Gold remains comfortably within the confines of the recently established range, with spot dealing a handful of dollars lower in Asia-Pac hours, printing just above $1,785/oz at typing. Last week saw bullion print at the highest level witnessed since November, briefly topping $1,850/oz, before the hawkish reaction to Fed Chair Powell’s post-FOMC press conference saw gold finish the week ~$60/oz shy of Tuesday’s high. Technicals remain well-defined, in line with those portrayed at the backend of last week.

OIL: Geopolitics & Surging Natural Gas Prices Support Crude

WTI & Brent crude futures have added ~$1.20 vs. Friday’s settlement levels, with geopolitical tensions surrounding Russia remaining elevated (U.S. security officials pointed to a further increase in the number of Russian troops amassed on the Ukrainian border over the weekend, while U.S. & European sanctions targeting Russia remain in the offing) and a weather-driven surge in U.S. natural gas prices eyed. Wednesday’s OPEC+ meeting provides some event risk for participants this week.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 31/01/2022 | 0800/0900 | *** |  | ES | HICP (p) |

| 31/01/2022 | 0900/1000 | *** |  | IT | GDP (p) |

| 31/01/2022 | 1000/1100 | *** |  | EU | GDP (p) |

| 31/01/2022 | 1300/1400 | *** |  | DE | HICP (p) |

| 31/01/2022 | 1330/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 31/01/2022 | 1445/0945 | ** |  | US | MNI Chicago PMI |

| 31/01/2022 | 1530/1030 | ** | | US | Dallas Fed Manufacturing Survey |

| 31/01/2022 | 1630/1130 | | US | San Francisco Fed's Mary Daly | |

| 31/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 31/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 31/01/2022 | 1740/1240 | | US | Kansas City Fed's Esther George | |

| 31/01/2022 | 2200/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.