Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

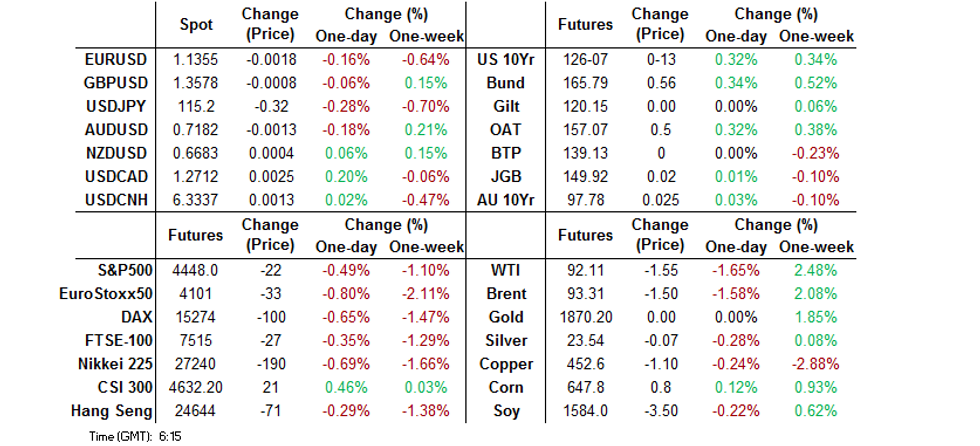

- Asia-Pac trade saw core FI markets draw a bid from unverified Russian reports which pointed to Ukraine conducting mortar and grenade attacks on the separatist region of Luhansk, as false flag fears intensified. Note that the issue has only been covered by Russian state media, with scepticism surrounding the source of the reports resulting in the paring of a chunk of the initial risk-off moves in the wider cross-asset space. Note that early Asia-Pac dealing saw U.S. officials point to a further 7K Russian troops gathering near the Ukrainian border in recent days (contrary to Russian rhetoric on the matter).

- Note that Ukraine has dnied the above attack in the last 10 minutes.

- U.S. housing starts & weekly jobless claims headline the global data docket today. Central bank speaker slate includes Fed's Bullard & Mester, ECB's Lane & de Cos, Norges Bank's Olsen & Riksbank's Breman.

BOND SUMMARY: Russian Reports Of Ukraine Mortar Attack On Luhansk Supports Core FI

Asia-Pac trade saw core FI markets draw a bid from unverified Russian reports which pointed to Ukraine conducting mortar and grenade attacks on the separatist region of Luhansk, as false flag fears intensified. Note that the issue has only been covered by Russian state media, with scepticism surrounding the source of the reports resulting in the paring of a chunk of the initial risk-off moves in the wider cross-asset space. Note that early Asia-Pac dealing saw U.S. officials point to a further 7K Russian troops gathering near the Ukrainian border in recent days (contrary to Russian rhetoric on the matter).

- TYH2 +0-14 at 126-08, 0-07+ off the overnight peak, with the contract operating in a 0-22+ range on a more than healthy and comfortably above average ~290K lots. Cash Tsys run 4-6bp richer on the day, with the belly leading on the curve. Looking ahead, weekly jobless claims, housing starts, building permits and Philly Fed activity data headline In NY hours. We will also get Fedspeak from Bullard & Mester, as well as 30-Year TIPS supply

- Prior to the broader risk-off move, JGB futures rebounded on the back of solid takedown of 20-Year JGB supply, after this morning’s concession-driven cheapening & steepening provided enough enticement for buyers to dip their toe into the water. Futures finished +3 after registering fresh cycle lows during the Tokyo morning. The smooth auction came against a backdrop of multi-year steeps on the curve, as well as appeal on the 10-/20-/30-Year JGB fly, in the wake of the recent buyers’ hiatus when it comes to super-long paper. Still, the cash JGB curve is steeper on the day (benchmarks sit little changed to 5bp cheaper), with the super-long end drifting back towards morning cheaps after the impulse of the auction and wider risk-off flows faded. Optically, the 1.00% yield level in 30s held firm, for now. Crucially 10-Year JGB yields didn’t top 23bp (the level which triggered the recent round of BoJ intervention).

- Aussie bond futures ticked higher on the back of the broader risk aversion, with YM finishing +4.0, while XM was 2.5 better off come the bell. Note that local labour market data provided little impetus for markets, with the unemployment rate meeting exp., headline employment beating expectations (the uptick was driven solely by part-time hiring), while hours worked tumbled on COVID cases and annual leave usage.

JGBS AUCTION: Japanese MOF sells Y971.0bn 20-Year JGBs:

The Japanese Ministry of Finance (MOF) sells Y971.0bn 20-Year JGBs:

- Average Yield 0.736% (prev. 0.532%)

- Average Price 95.91 (prev. 99.41)

- High Yield: 0.739% (prev. 0.536%)

- Low Price 95.85 (prev. 99.35)

- % Allotted At High Yield: 67.1546% (prev. 94.8003%)

- Bid/Cover: 3.392x (prev. 3.179x)

JGBS AUCTION: Japanese MOF sells Y2.9377tn 1-Year Bills:

The Japanese Ministry of Finance (MOF) sells Y2.9377tn 1-Year Bills:

- Average Yield -0.0551% (prev. -0.0909%)

- Average Price 100.055 (prev. 100.091)

- High Yield: -0.0491% (prev. -0.0879%)

- Low Price 100.049 (prev. 100.088)

- % Allotted At High Yield: 46.1531% (prev. 5.5750%)

- Bid/Cover: 2.732x (prev. 3.164x)

FOREX: Growing Drumbeat Of Ukraine Conflict Escalation Inspires Risk Aversion

Headlines from Russian state media pointing to alleged shelling of targets in Luhansk and Donetsk People's Republics by Ukrainian security forces in breach of the Minsk agreements inspired a round of risk-off flows in G10 FX space. While the initial story was circulated by Sputnik, a portal often described as the Kremlin's propaganda outlet, it was quickly picked up by other Russian outlets.

- Reports of rising tensions in the Donbas came on the heels of comments from a senior U.S. official, who said that Russia's claims that it was reducing military presence near Ukraine were "false" and Moscow has instead added 7,000 troops along the border. There was a modest risk-off reaction to those remarks but it was promptly unwound, albeit markets were left on the alert for further developments.

- The prospect of military escalation in east Ukraine inspired a flight to safety, putting a bid into JPY and CHF. Major safe haven currencies gained at the expense of their riskier peers (save for NZD), with Scandie FX coming under particular pressure. The SEK landed at the bottom of the G10 pile owing to its sensitivity to the Ukraine crisis. The Russian rouble retreated as Moscow trading re-opened, but weekly lows remain some way off.

- The Aussie dollar was unfazed by domestic labour market data, as political risk headlines took precedence. Part-time jobs drove a surprise overall gain in employment in January, which absorbed marginally wider participation to generate an unchanged headline unemployment rate.

- U.S. housing starts & weekly jobless claims headline the global data docket today. Central bank speaker slate includes Fed's Bullard & Mester, ECB's Lane & de Cos, Norges Bank's Olsen & Riksbank's Breman.

FOREX OPTIONS: Expiries for Feb17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1390-00(E522mln), $1.1435-50(E1.7bln), $1.1500-20(E1.1bln)

- USD/JPY: Y115.00($1.3bln), Y115.75($860mln), Y116.00($1.5bln)

- GBP/USD: $1.3400(Gbp1.0bln), $1.3500(Gbp1.0bln)

- EUR/GBP: Gbp0.8390(E583mln)

ASIA FX: Russia/Ukraine Tension Spills Over Into Asia, BSP Policy Decision Eyed

Selling pressure hit Asian EM currencies as geopolitical worry returned on the back of headlines from Russian media noting that Ukraine has attacked Luhansk People's Republic in breach of ceasefire agreements. While exchanges of fire between Ukrainian troops and Donbas separatists are not unusual, the circulation of these reports by Russian state media came amid Western suspicions that the Kremlin might be looking for a pretext to launch an intervention.

- CNH: Offshore yuan remained stable, with an uptick in USD/CNH in reaction to Russia headlines promptly faded.

- KRW: Spot USD/KRW erased its initial losses, with gyrations in broader risk sentiment in the driving seat. Meanwhile, South Korea said that it is preparing for potential trade disruptions in case the Russia-Ukraine standoff escalates.

- IDR: The rupiah underperformed, extending losses as broader risk-off flows kicked in. Domestic headline flow was rather limited.

- MYR: The ringgit joint its regional peers and sold off in reaction to renewed geopolitical angst.

- PHP: Gains in spot USD/PHP took the rate closer to key resistance from PHP51.500 associated with BSP interventions. The Philippine central bank will announce its monetary policy decision today but is not expected to touch policy levers.

- THB: The baht returned from a holiday on a firmer footing and remained in positive territory, despite trimming some gains on the back of Russia headlines. The PDMO played down the risk posed by rising global interest rate to Thailand's financial position.

BONDS: Plenty Of Net Bond Selling In Japanese Weekly International Flow Data

Bond flows dominated the latest batch of weekly international security flow data out of Japan, with Japanese investors net selling foreign bonds at a rate not experienced since ’18 as core global bond markets continued to cheapen on the back of the well-documented hawkish central bank repricing.

- When it comes to Japanese bonds, foreign investors were net sellers, after 2 consecutive weeks of net purchases. A reminder that the pressure observed in the JGB space over the period covered by the latest dataset triggered a pre-emptive move from the BoJ. The Bank defended the top of its permitted 10-Year JGB yield trading band (+0.25%) as the benchmark yield metric came within 2bp of its line in the sand.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -1910.7 | -107.1 | -2557.2 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 111.2 | 264.5 | 979.7 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | -894.1 | 287.9 | -1764.4 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | -29.7 | -232.1 | -373.1 |

EQUITIES: Mixed As Japanese Equities Lag

Unverified Russian reports of a Ukrainian mortar & grenade attack on the separatist region of Luhansk saw the major regional equity benchmarks move back from best levels, with the news story having varying degrees of impact on the space, as worries of a Russian false flag did the rounds.

- Chinese and Korean equity indices outperformed their major regional peers, while Australian, Japanese, and Hong Kong equities are flat to lower.

- The CSI300 is 0.4% firmer, aided by gains in new energy and metals sub-indices. On the other hand, the sub-index tracking real estate developers leads losses, as COVID–19 outbreaks in Hong Kong and some Chinese cities (e.g. Suzhou) weigh on sentiment.

- The Nikkei 225 leads regional losses, sitting 1.0% weaker, with heavily favoured names such as Recruit Holdings and NTT Data feeling the brunt of the wider risk-off pressure. Re-opening plays e.g. railways and airlines, were more fortunate, with expectations surrounding an impending announcement from Japanese PM Kishida re: the loosening of border restrictions providing tailwinds.

- E-minis sit 0.4-0.6% lower, having pared some of the Ukraine-related losses as questions re: the validity of the source of the reports allowed some of the initial risk-off move to fade.

GOLD: Modest Bid Overnight

Gold added a handful of dollars overnight, trading at $1,875/oz ahead of European hours, with (unverified) Russian reports of a Ukrainian mortar & grenade attack on the separatist region of Luhansk weighing on broader risk-appetite (with false flag worry elevated).

- The precious metal sits just below the recently recorded multi-month highs.

- To recap, continued western questions/apprehension re: the Russian claims of at least a partial troop pullback from the Ukrainian border remained evident on Wednesday. This fed into yesterday’s price action, as bullion added ~$15/oz in spot trade, given the continued line of questioning from western powers. A lack of fresh, hawkish developments in the Fed minutes covering the central bank’s most recent monetary policy meeting also supported gold on Wednesday.

- On the technical front, bulls now look to resistance at $1,881.6/oz (1.00 projection of Dec 15-Jan 25-28 price swing), while initial support is defined at $1,844.7/oz (Feb 15 low).

OIL: Lower Than Settlement, But Paring Losses Overnight

WTI is ~-$0.60 and Brent is ~-$0.70 from settlement at typing, recovering from session lows to print $94.20 and $92.95, respectively.

- A sharp rally came on the back of unconfirmed reports (from Russian media outfits Ria and Sputnik) of a mortar and grenade attack by Ukrainian armed forces on Luhansk (recently recognised by Russia as a sovereign state). A reminder that western powers have warned of Russia possibly creating “false narratives” to justify military intervention in Ukraine.

- To recap, WTI traded as low as $90.0 on Wednesday, while Brent troughed at $91.1, tumbling in post-settlement trade as the Iranian nuclear talks in Vienna were seemingly moving in a positive direction. French Foreign Minister Le Drian suggested that “it is a question of days” when it comes to concrete developments on the matter. Optimism for a nuclear deal received a further boost when Iran’s top nuclear negotiator tweeted: “After weeks of intensive talks, we are closer than ever to an agreement.” However, he did caution that “nothing is agreed until everything is agreed, though. Our negotiating partners need to be realistic, avoid intransigence and heed lessons of past 4yrs. Time for their serious decisions.”

- That was before the aforementioned worry re: Russia boosted geopolitical risk premium overnight.

- Looking to technical levels, support for WTI and Brent remain intact at $88.41 (Feb 9 low) and $89.93 (Feb 8 low) respectively, while resistance is seen at Feb 14 highs ($95.82 for WTI and $96.78 for Brent).

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/02/2022 | 0700/0800 |  | EU | ECB Schnabel discussion with SPD | |

| 17/02/2022 | 1100/0600 | * |  | TR | Turkey Benchmark Rate |

| 17/02/2022 | - | | EU | ECB Lagarde at G20 CB Governors Meeting | |

| 17/02/2022 | 1330/0830 | ** |  | US | Jobless Claims |

| 17/02/2022 | 1330/0830 | *** | | US | Housing Starts |

| 17/02/2022 | 1330/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 17/02/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 17/02/2022 | 1400/1500 | | EU | ECB Lane on MNI Webcast on ECB Policy | |

| 17/02/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 17/02/2022 | 1600/1100 | | US | St. Louis Fed's James Bullard | |

| 17/02/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 17/02/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 17/02/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for TIPS 30 Year Bond |

| 17/02/2022 | 2200/1700 | | US | Cleveland Fed's Loretta Mester | |

| 18/02/2022 | 2330/0830 | *** |  | JP | CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.