Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The latest RBNZ decision came down on the hawkish side of the spectrum, with the Bank delivering the widely expected 25bp OCR hike. In addition to that it flagged its QT plans and shifted its OCR projections higher. Australian WPI came in between RBA assumptions and the median BBG estimate.

- Equities nudged higher overnight, with participants breathing a sign of relief as Western sanctions on Russia avoided the worst-case scenario.

- While geopolitical risk will continue to draw attention today, data highlights include final EZ CPI & German consumer confidence. Speeches are due from Fed's Daly, ECB's de Guindos, de Cos & Villeroy and BoE's Bailey, Broadbent, Haskel & Tenreyro. Early Morning comments from ECB hawk Holzmann pointed to the need for 2 rate hikes during '22. He also suggested the neutral rate could be somewhere in the region of 1.50%, a level that he believes could be reached by '24.

BOND SUMMARY: Antipodean Headline Flow Dominates

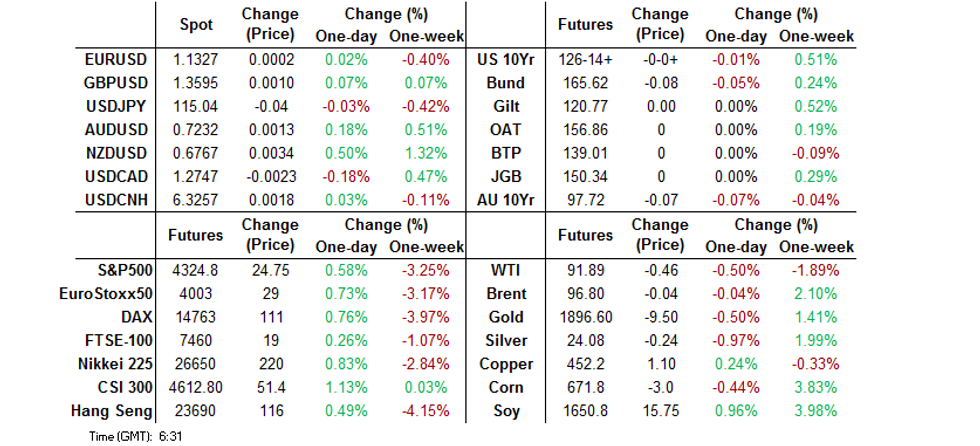

TYH2 stuck to a narrow 0-05+ overnight, hampered by the closure of cash Tsy trade, owing to the observance of a Japanese holiday. The contract last deals -0-00+ at 126-14+, just off the base of the overnight range. Gyrations in the ACGB space provided some lead for Tsys, but a lack of meaningful macro headline flow made for a contained session. The space looked through the cancellation of Thursday’s Blinken-Lavrov meeting, while the White House took a Biden-Putin meeting off the table (until there is a de-escalation re: Ukraine). Fedspeak from Daly & 5-Year Tsy supply are due on Wednesday.

- Aussie bonds ran lower in early Sydney trade, with Western sanctions on Russia avoiding the worst-case scenario. The presence of 10-Year ACGB supply, RBA-related jitters ahead of WPI data and perhaps some pre-RBNZ trans-Tasman spill over provided further sources of downward impetus early on, with YM testing cycle lows. WPI data provided the most marginal of misses in Y/Y terms but was still in broadly line with RBA assumptions. This saw the space off of worst levels as some of the more aggressive market pricing re: RBA hiking moderated at the margin (although CBA are sticking with their June hike call). Still, hawkish trans-Tasman spill over capped the space, with the RBNZ delivering the widely expected 25bp hike, as it outlined its QT plans and signalled a higher path for interest rates over the forecast horizon (in which it envisages a move comfortably above its estimate of neutral levels). YM was -8.5, while XM was -7.0. EFPs narrowed by 1.0-1.5bp on the session.

AUSSIE BONDS: The AOFM sells A$1.0bn of the 1.25% 21 May ‘32 Bond, issue #TB158:

The Australian Office of Financial Management (AOFM) sells A$1.0bn of the 1.25% 21 May 2032 Bond, issue #TB158:

- Average Yield: 2.2870% (prev. 1.9536%)

- High Yield: 2.2900% (prev. 1.9575%)

- Bid/Cover: 3.3650x (prev. 2.1450x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 38.8% (prev. 4.1%)

- Bidders 47 (prev. 37), successful 18 (prev. 23), allocated in full 11 (prev. 18)

FOREX: Hawkish RBNZ Rate Outlook Underpins NZD, Market Sentiment Stabilises

The kiwi leapt higher, taking the lead in G10 FX space, as the RBNZ raised the OCR by 25bp and forecast more aggressive interest-rate action for the period ahead. The MPC now expect their policy rate to rise faster and peak at a higher point, with the balance sheet runoff officially set to commence through a combination of bond maturities and managed sales. The statement highlighted that the decision to hike the OCR by 25bp rather than 50bp was "finely balanced," while the Committee was "willing to move the OCR in larger increments if required." Explicit readiness to deliver bold tightening steps and a relatively hawkish OCR track underscored the Reserve Bank's resolve in combating soaring inflation.

- AUD/NZD took a nosedive after the RBNZ published their Monetary Policy Statement. New Zealand policy decision was announced after Australia reported unimpressive wage price (WPI) data, which prompted participants to pare RBA rate hike bets. The conjunction of Antipodean developments weighed on 2-Year Australia/New Zealand swap spread, which filtered through into AUD/NZD price action. The rate bottomed out within touching distance from its 50-DMA, which has remained intact since early December, before trimming some losses.

- Nonetheless, the AUD is heading for the London session as the second best G10 performer after its Antipodean cousin. The Aussie dollar unwound its marginal post-WPI dip registered against major peers, as the spillover from hawkish RBNZ decision and improving risk environment extended a helping hand. The recovery in market sentiment (U.S. e-mini futures operated in the green) lent support to the broader high-beta FX space.

- Demand for safe haven assets waned, with the greenback struggling for any topside impetus. JPY and EUR also came under pressure. Note that liquidity in Asia hours was sapped by a market holiday in Japan. Overnight news flow provided little to alter the familiar narrative on the Russia-Ukraine conflict, with participants assessing the first barrage of sanctions imposed by the West.

- The yuan ignored a marginally stronger PBOC fix. Spot USD/CNH crept higher after China's central bank set the reference rate 17 pips below sell-side estimate, only to gradually return to virtually neutral levels thereafter.

- While geopolitical risk will continue to draw attention today, data highlights include final EZ CPI & German consumer confidence. Speeches are due from Fed's Daly, ECB's de Guindos, de Cos & Villeroy and BoE's Bailey, Broadbent, Haskel & Tenreyro.

FOREX OPTIONS: Expiries for Feb23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200(E1.0bln), $1.1250(E601mln), $1.1275(E1.1bln), $1.1300-15(E1.6bln), $1.1350-60(E1.4bln), $1.1380-85(E575mln)

- USD/JPY: Y114.00($860mln)

- AUD/USD: $0.7190-00(A$1.3bln), $0.7225($637mln)

ASIA FX: Asia EM Space Sees Stabilisation, Peso Leads Gains

Wednesday brought a spell of stabilisation for Asia EM currencies as participants awaited further in Russia-Ukraine situation.

- CNH: Spot USD/CNH posted a brief uptick but is back to neutral levels. A marginally stronger than expected PBOC fix failed to affect offshore yuan.

- KRW: The won gave away its initial gains, returning to virtually neutral levels. South Korea's daily Covid-19 cases hit another record, exceeding 170k new infections.

- IDR: Spot USD/IDR held a tight range, with domestic headline flow providing little of real note.

- MYR: Spot USD/MYR recouped its opening downtick. Malaysia said it aims to pass constitutional amendments against party hopping by late March.

- PHP: The Philippine peso caught a bid, outperforming all of its regional peers. It may have drawn support from the fact that Metro Manila mayors unanimously backed easing Covid Alert Level in the capital region.

- THB: The baht slipped as Thailand's daily Covid-19 cases rose to a six-month high, with the main virus response task force set to debate loosening countermeasures. The minutes from the BoT's most recent monetary policy meeting showed that the central bank attributed THB volatility to normalisation prospects.

EQUITIES: Higher As China Tech Leads Rally

The major Asia-Pac equity indices trade 0.5-0.9% higher at writing despite a negative lead from Wall St., as the former benefitted from the perception that western sanctions on Russia were more lenient than some participants had earlier feared. A quick reminder that Japanese markets were closed on Wednesday, as the country observed a national holiday.

- The Hang Seng leads gains amongst regional peers, +0.9% at writing. China-based large cap tech names such as Meituan outperformed, despite losses in their U.S. ADRs on Tuesday. The Hang Seng Tech Index added 1.3% as a result. Fears over a wide regulatory crackdown on tech companies have eased from Friday’s extremes, with a lack of escalation evident when it comes to fresh regulatory burden, at least week-to-date. Elsewhere, rumours pointing to a renewed crackdown on the online gaming sector haven’t been realised, yet.. The bid in Chinese equities also fed into mainland dealing.

- E-minis sit 0.4-0.7% better off at writing, with lingering worry re: Russia-Ukraine tensions providing a cap on the space. Participants continue to debate the possibility of a diplomatic resolution to the situation, with a lack of impending top level dialogue evident (Blinken-Lavrov and Biden-Putin talks are “off the table” for now).

CHINA STOCKS: Net Northbound Connect Flows Still Positive YtD, But Lagging ‘21

A quick look at flows observable on the northbound leg of the Hong Kong-China Stock Connect schemes reveals that yesterday saw the largest round of net selling via the Connect schemes since the week before the LNY break. Note that mainland shares have still been subjected to net inflows via the Connect schemes during ’22, but the flows have only been modest, totalling CNY16.2bn YtD (vs. a net ~CNY86bn over the comparable period in ’21).

GOLD: Steady In Asia

Gold is virtually unchanged from settlement at typing, printing $1,899.6/oz in very limited Asia-Pac dealing.

- To recap, gold closed lower on Tuesday as the initial round of sanctions from the U.S., UK, and the EU on Russia were deemed to be less harsh than some had feared. The precious metal remains below Tuesday’s cycle highs ($1,914.25/oz), with some beginning to question Russia’s willingness to move troops beyond the separatist states of Luhansk & Donetsk (and further into Ukraine). Still, the elevated threat of deeper Russian incursions continues to provide background support for gold, while providing a sense of continuous headline risk.

- The cancellation of Thursday’s Blinken-Lavrov meeting, and subsequent White House comments noting that a potential meeting between Biden & Putin “certainly is not in the plans” provided little in the way of market reaction.

- On the technical front, gold remains in an uptrend, with resistance located at $1,916.6 (Jun 1 ’21 high and key bull trigger). A break above this level would expose the top of the bull channel drawn from the Aug 9 ’21 low.

OIL: Slightly Higher In Asia

WTI and Brent are ~$0.40 higher from settlement at typing, printing $92.31 and $97.24 respectively.

- To recap, both benchmarks backed away from fresh cycle highs on Tuesday ($96.00 for WTI and $99.50 for Brent), with participants removing some of the geopolitical risk premium that had developed earlier in the day as it became apparent that western sanctions re: Russia were a little more lenient than some had feared. BBG source reports carrying remarks from a senior U.S. State Dept official noted that the sanctions were designed to avoid upsetting energy markets.

- A reminder that hope surrounding a potential U.S.-Iran nuclear deal remains elevated, providing at least some counter to the impulse from the ongoing Russia-Ukraine situation.

- From a technical perspective, bullish conditions remain intact for oil. Tuesday’s rally saw WTI and Brent clear resistance at $98.94 (2.764 projection of the Dec 2-9-20 price swing) and $95.82 (Feb 14 high and bull trigger), respectively, before pulling back to current levels. Bulls now look to $98.24 (3.00 proj. of the Dec 2-9-20 price swing) in WTI and $100.00 (key psychological barrier) in Brent.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/02/2022 | 0700/0800 | * |  | DE | GFK Consumer Climate |

| 23/02/2022 | 0700/1500 | ** |  | CN | MNI China Liquidity Suvey |

| 23/02/2022 | 0745/0845 | ** |  | FR | Manufacturing Sentiment |

| 23/02/2022 | 0915/1015 |  | EU | ECB Elderson Intro & panel participation at Eurofi Seminar | |

| 23/02/2022 | 0930/0930 |  | UK | BOE Governor Bailey et al at TSC | |

| 23/02/2022 | 1000/1100 | *** | | EU | HICP (f) |

| 23/02/2022 | 1130/1230 | | EU | ECB de Guindos Q&A at El Español & Invertia symposium | |

| 23/02/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 23/02/2022 | 1330/0830 | * |  | CA | Quarterly financial statistics for enterprises |

| 23/02/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 23/02/2022 | 1500/1500 | | UK | BOE Tenreyro speaks at NIESR Institute lecture | |

| 23/02/2022 | 1630/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 23/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 23/02/2022 | 1800/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 23/02/2022 | 2030/1530 | | US | San Francisco Fed's Mary Daly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.