Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Participants were happy to sell U.S. Tsys & pay U.S. swaps in Asia, weighing on core global FI overnight.

- Will the BoJ step in to defend its 10-Year JGB yield trading band? 10-Year yields closed at the same level that triggered such action in February.

- Russian equity markets re-open for the first time in weeks, albeit in a shortened session, with limits on trading.

- Today's data highlights include U.S. jobless claims & durable goods orders, as well as a slew of PMI readings from across the world. The central bank speaker slate features several Fed, ECB & BoE members. Several European & EM central bank decisions will also cross.

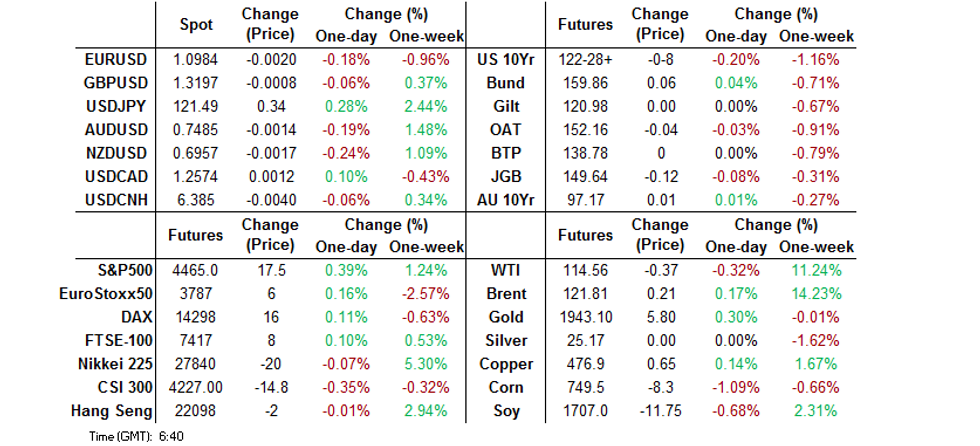

BOND SUMMARY: Payside Flows In U.S. Swaps & A Downtick In Oil Weigh On Core FI In Asia

Payside flows in U.S. swaps and a pullback from fresh ~2-week highs in crude oil futures (a marginal downtick in stagflationary worry) applied pressure to broader core fixed income markets overnight. There was a lack of major headline flow apparent ahead of the heavily awaited NATO summit, with fresh U.S. sanctions directed towards Russia and measures to mitigate European reliance on Russian energy supply front and centre at the upcoming gathering.

- TYM2 pushed to fresh session lows ahead of London trade, with TYM2 last -0-08 at 122-28+, 0-03 off the base of the 0-16+ overnight range, on volume of ~140K. Cash Tsys run 3-6bp cheaper on the day, with 5s leading the way lower (note that 5s provided the focal point of the aforementioned payside swap flows,), allowing the 5- 30-Year yield spread to tag another fresh cycle low. Futures flow was headlined by a block seller of FVM2 (-5,375) & block buyer of TUM2 (+3,399). Fedspeak from Bullard (’22 voter, hawk) offered nothing of any real interest during Asia-Pac hours. Looking ahead, outside of the NATO summit, NY hours will see the release of weekly jobless claims data, durable goods, 10-Year TIPS supply and Fedspeak from Waller, Kashkari (’23 voter), Evans (’23 voter) & Bostic (’24 voter).

- JGB futures finished 12 ticks lower on the day, softening in the Tokyo afternoon, although the contract failed to breach its overnight session lows. 10-Year JGB yields closed at 0.23%, the level that triggered BoJ intervention back in February. Will the Bank announce fixed rate operations after hours today? It did so in February, in a pre-emptive step to protect the upper end of its permitted -/+25bp 10-Year JGB yield trading band. The cash curve twist steepened around the 5-Year point, with 7s (futures-driven) and 40s providing the weak points, cheapening by ~1.5bp on the session. Dovish BoJ dissenter Kataoka provided his usual round of reflationist rhetoric in his latest speech.

- ACGBs were dominated by the wider core FI impetus (allowing the space to move back from its early Sydney peak). Contained swings were once again observed into the futures close (as has been the case on several occasions this week). That left YM -1.0 & XM +1.0 at the close, with the cash curve twist flattening as longer dated cash ACGBs richened by ~3bp.

FOREX: USD Edges Higher, Antipodeans Lag Behind

Modest defensive flows took hold in Asia-Pac trade as regional headline flow failed to provide anything to bolster market sentiment. Regional risk barometer AUD/JPY backed off a multi-year high, as the Antipodeans landed at the bottom of the G10 pile, while the yen got some reprieve in the wake of its recent sharp sell-off.

- The greenback crept higher along U.S. Tsy yields as Fed's Bullard reiterated his view that policymakers should act more aggressively. Demand for U.S. dollar pushed USD/JPY higher, but yesterday's cycle high remained intact.

- Offshore yuan regained poise after the PBOC set the mid-point of permitted USD/CNY trading band 23 pips below the expected level. This allowed USD/CNH to ease off after a brief look above yesterday's high.

- The Norwegian krone garnered some strength ahead of today's monetary policy decision from Norges Bank, even as Brent crude oil futures pulled back into the red.

- Today's data highlights include U.S. jobless claims & durable goods order as well as a slew of PMI readings from across the world. Central bank speaker slate features several Fed, ECB & BoE members.

FOREX OPTIONS: Expiries for Mar24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0950-70(E1.1bln), $1.1000-20(E615mln), $1.1065-70(E544mln), $1.1100(E1.2bln)

- GBP/USD: $1.3150-60(Gbp1.3bln)

- USD/CAD: C$1.2650($1.1bln), C$1.2800($2.1bln)

ASIA FX: Most Asia EM Currencies Face Mild Pressure, Yuan Ticks Higher

Renewed increase in U.S. Tsy yields underpinned most USD/Asia crosses but the redback managed to eke out some gains. Regional headline flow was rather sparse.

- CNH: Spot USD/CNH briefly showed above yesterday's high before pulling back into negative territory on the back of a stronger than expected PBOC fix. China's central bank set the mid-point of permitted USD/CNY trading band 23 pips below sell-side estimate.

- KRW: The won led losses in the region amid higher U.S. Tsy yields. BoK Gov-nominee Rhee's first public comments offered little in the way of notable insight.

- IDR: Spot USD/IDR lodged a new two-week high before trimming gains, with broader impetus in the driving seat.

- MYR: Spot USD/MYR rallied to a three-month high in early trade but gave away the bulk of those gains thereafter. The ringgit paid little attention to swings in palm oil futures, which snapped a three-day winning streak.

- PHP: Spot USD/PHP rejected Mar 14 high of PHP52.487 and backed off, with participants awaiting monetary policy decision from the Bangko Sentral ng Pilipinas.

- THB: Spot USD/THB pulled back from a new multi-week high, returning to neutral levels. Monthly trade data from Thailand's Customs Dept were eyed.

EQUITIES: Lower As Commodities Hover Near Two-Week Highs

Major Asia-Pac equity indices are mostly lower at typing, following a negative lead from Wall St. Commodity-related sectors across the region largely outperformed peers despite a slight downtick in commodity and crude prices during Asia-Pac dealing, with major commodity benchmarks continuing to trade a touch below two-week highs, above their respective ranges observed in Wednesday’s Asian session, pointing to some “catch up.”

- The ASX200 led regional index peers, finishing 0.1% better off, reversing earlier losses due to gains in materials, energy, and utilities stocks. On the other hand, the technology, healthcare, and financials sub-indices were unable to fully recover from initial losses, providing some counter to the commodity-led rally.

- The CSI300 underperformed, dealing 0.8% softer at typing. Chinese liquor stocks bore the brunt of the day’s selling, led by losses in large-caps such as Kweichow Moutai and Luzhou Laojiao.

- The Hang Seng sits 0.3% softer at typing.after pulling back from worst levels of the day. Underperforming China-based tech names were largely able to pare their early losses, although Tencent Holdings (-3.5%) underperformed after showing no signs of plans for fresh stock buybacks (as well as reporting an earnings miss on Wednesday), after Alibaba and Xiaomi announced their own stock buybacks earlier in the week. Around two-thirds of the Hang Seng’s constituents have reported earnings, with releases underperforming analyst expectations by ~0.8% thus far.

- U.S. e-mini equity index futures sit 0.2% to 0.5% firmer at writing, benefitting from the downtick in crude oil prices.

GOLD: Lower In Asia

Gold deals $5 weaker at writing to print ~$1,938/oz, backing away from one-week highs made earlier in the session, with an uptick in the Dollar (DXY) and U.S. Tsy yields applying some modest pressure.

- To recap Wednesday’s price action, the precious metal closed ~$20/oz firmer, with the move higher facilitated by a broad downtick in U.S. real yields.

- Gold’s geopolitical risk premium remains elevated ahead of the U.S.-NATO summit later on Thursday. Even as there has been little discernible progress in ongoing Russia-Ukraine ceasefire negotiations, tensions between Russia and the west have continued to rise. The spectre of fresh U.S. & European sanctions on Russia lingers.

- Looking to technical levels, bullion isn’t far away from initial resistance at $1,954.7/oz (Mar 15 high). A successful break of that level will expose further resistance at $2,009.2 (Mar 10 high), while support is located some distance away at $1,895.3 (Mar 15 low and 50-Day EMA).

OIL: Slightly Lower In Asia

WTI is -$0.70 and Brent is -$0.30, printing $114.30 and $121.30 respectively at writing.

- Both benchmarks have backed away from two-week highs made earlier in the session but operate near the top of Wednesday’s range, finding support as debate over possible EU sanctions on Russian energy exports has done the rounds in Asia, while disruptions to the Caspian Pipeline Consortium (CPC) pipeline has exacerbated worry re: tightness in global crude supplies.

- To elaborate on the latter, CPC officials announced that crude exports from the port of Novorossiysk were completely halted on Wednesday, flagging “abnormal storms” as the cause of “critical” damage to facilities. The closure is expected to remove up to 1.2mn bpd of crude from global markets for the duration of repair works (estimated to be ~2 months).

- Looking at possible EU measures re: Russian energy exports, U.S. national security adviser Jake Sullivan has pointed to a “practical roadmap” to increase LNG supplies to Europe, which will be unveiled on Friday, with the obvious aims of addressing concerns re: cuts in Russian gas supplies & reducing European reliance on Russian energy. Ultimately, the timeline surrounding fresh measures to curb Russian energy exports to the EU remains uncertain, with French officials casting doubt over new energy-related sanctions on Russia this week.

- Weekly EIA data released on Wednesday saw a surprise drawdown in crude stockpiles with larger-than-expected declines in gasoline and distillate inventories (against WSJ estimates), while there was a build in stocks at the Cushing hub. The release largely matched the figures observed in reports covering Tuesday’s weekly API inventory estimates.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/03/2022 | 0030/0930 | ** |  | JP | IHS Markit Flash Japan PMI |

| 23/03/2022 | 0105/2105 |  | US | St. Louis Fed's James Bullard | |

| 24/03/2022 | 0745/0845 | ** |  | FR | Manufacturing Sentiment |

| 24/03/2022 | 0815/0915 | ** | | FR | IHS Markit Services PMI (p) |

| 24/03/2022 | 0815/0915 | ** | | FR | IHS Markit Manufacturing PMI (p) |

| 24/03/2022 | 0830/0930 |  | CH | SNB interest rate decision | |

| 24/03/2022 | 0830/0930 | *** | | CH | SNB policy decision |

| 24/03/2022 | 0830/0930 | ** |  | DE | IHS Markit Services PMI (p) |

| 24/03/2022 | 0830/0930 | ** | | DE | IHS Markit Manufacturing PMI (p) |

| 24/03/2022 | 0900/1000 | *** |  | NO | Norges Bank Rate Decision |

| 24/03/2022 | 0900/1000 | ** |  | EU | IHS Markit Services PMI (p) |

| 24/03/2022 | 0900/1000 | ** | | EU | IHS Markit Manufacturing PMI (p) |

| 24/03/2022 | 0900/1000 | ** | | EU | IHS Markit Composite PMI (p) |

| 24/03/2022 | 0930/0930 | *** |  | UK | IHS Markit Manufacturing PMI (flash) |

| 24/03/2022 | 0930/0930 | *** | | UK | IHS Markit Services PMI (flash) |

| 24/03/2022 | 0930/0930 | *** | | UK | IHS Markit Composite PMI (flash) |

| 24/03/2022 | 0930/1030 | | EU | ECB Elderson at IIEA Webinar | |

| 24/03/2022 | 1030/1030 | | UK | Bank of England Financial Policy Report | |

| 24/03/2022 | 1100/1100 | ** | | UK | CBI Distributive Trades |

| 24/03/2022 | - | | EU | ECB Lagarde at European Council Meeting | |

| 24/03/2022 | 1230/0830 | ** | | US | Jobless Claims |

| 24/03/2022 | 1230/0830 | ** | | US | durable goods new orders |

| 24/03/2022 | 1230/0830 | * | | US | Current Account Balance |

| 24/03/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 24/03/2022 | 1230/0830 | | US | Minneapolis Fed's Neel Kashkari | |

| 24/03/2022 | 1300/1300 | | UK | BOE Mann Panels Institute of International Finance event | |

| 24/03/2022 | 1300/1400 | | EU | ECB Elderson in Panel at LSE | |

| 24/03/2022 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 24/03/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (flash) |

| 24/03/2022 | 1350/0950 | | US | Chicago Fed's Charles Evans | |

| 24/03/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 24/03/2022 | 1500/1100 | | US | Atlanta Fed's Raphael Bostic | |

| 24/03/2022 | 1530/1130 | ** | | US | NY Fed Weekly Economic Index |

| 24/03/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 24/03/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 24/03/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 24/03/2022 | 1900/1500 | *** |  | MX | Mexico Interest Rate |

| 25/03/2022 | 2330/0830 | ** | | JP | Tokyo CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.