Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

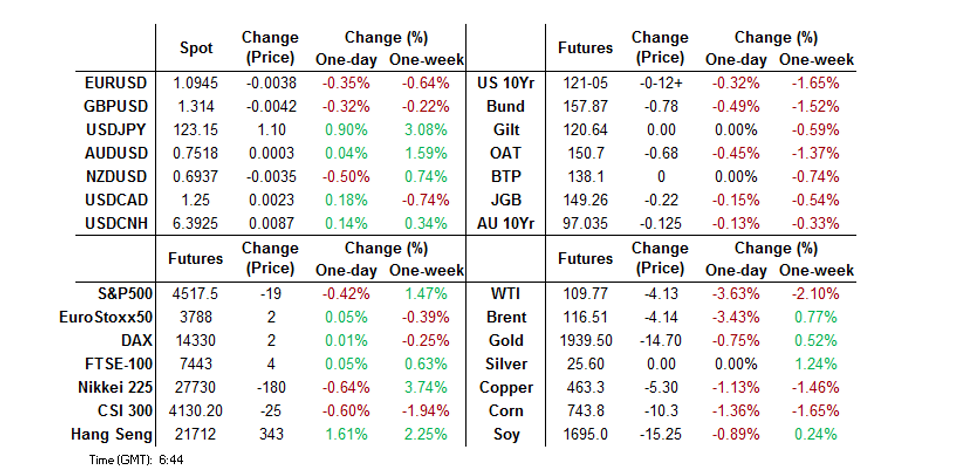

- BoJ policy divergence remained evident as the BoJ stepped in to defend the upper end of its permitted 10-Year JGB yield trading band (twice), with USD/JPY surging above Y123.00 as a result.

- A two-phase lockdown in China's Shanghai weighed on oil.

- Looking ahead, Monday’s focus will fall on central bank speak from ECB’s Rehn & BoE Governor Bailey, with lower tier economic data due from across the globe. Elsewhere, the latest Russia-Ukraine summit in Turkey will garner interest, although there is little in the way of expectations re: a meaningful breakthrough between the two nations.

BOND SUMMARY: U.S. 5-/30-Year Yield Spread Inverts, BoJ Defends 10-Year Band, Twice

Asia-Pac dealing saw core fixed income markets move lower, although there was some brief, limited respite for bulls during early Asia trade (perhaps on some worry surrounding U.S. President Biden’s apparent weekend faux pas, as some of his comments alluded to a desire for regime change in Russia. Note this idea was quickly rowed back by the White House).

- Ultimately, U.S. Tsys continued to cheapen, with TYM2 through Friday’s low, last dealing -0-10+ at 121-07 (next support is seen at the Jan 18 ’19 low, 121-02), with the contract 0-03 off the base of its 0-24+ range, operating on nearly 190K lots. Cash Tsys are 5-10bp cheaper on the session, with 2s leading the way lower. Note that the 5-/30-Year yield spread has inverted for the first time since ’06. Factors helping the cheapening included a move lower in crude oil prices (owing to a two-stage lockdown in China’s Shanghai), some “decent sized” payside flows in U.S. swaps (per market contacts), spill over from JGBs, a truncated U.S. Tsy supply schedule and regional reaction to Friday’s cheapening. Looking ahead, NY hours will bring advance goods trade data, inventory readings and the latest Dallas Fed m’fing activity print. Meanwhile, 2- & 5-Year Tsy auctions headline on the supply front. Elsewhere, the latest Russia-Ukraine summit in Turkey will garner interest, although there is little in the way of expectations re: a meaningful breakthrough between the two nations.

- The move higher in core global fixed income markets has resulted in the BoJ having to defend the upper end of its permitted 10-Year JGB yield trading band. Note that 10-Year JGB yields have had an incremental look above the upper limit of the BoJ’s permitted trading band, resulting in a second round of BoJ buying interest via fixed rate operations after the initial fixed rate operations drew no offers to sell from market participants (we await results of the second round of operations). JGB futures are -24 on the day, after registering another fresh cycle low. Meanwhile, the curve has bear steepened, with 40s running nearly 5bp cheaper on the day (some concession ahead of tomorrow’s 40-Year JGB auction is apparent).

- It was another session of tracking the wider impetus for the Aussie bond space. That leaves YM -18.0 and XM -13.5, with the former shunting lower into the close. Bills run 5-24 ticks lower through the reds. Note that the ruling Australian coalition will cut the fuel excise duty and support first time buyers re: the housing market when it hands down the latest Federal Budget on Tuesday.

FOREX: USD Gains, JPY Tumbles On BoJ Policy Divergence

The greenback has benefitted from an uptick in U.S. Tsy yields and JPY weakness during Asia-Pac dealing, trading higher against most of its G10 FX counterparts as a result.

- JPY has tumbled to the bottom of the same rankings on the back of the latest enforcement attempts re: the top end of the BoJ’s permitted 10-Year JGB yield trading band, as USD/JPY surged to fresh multi-year highs on continued BoJ policy divergence vs. DM central bank peers, printing as high as Y123.16, before easing back to trade around Y123.00. Note that 10-Year JGB yields have had an incremental look above the upper limit of the BoJ’s permitted trading band, resulting in a second round of BoJ buying interest via fixed rate operations after the initial fixed rate operations drew no offers to sell from market participants.

- Elsewhere, there is a bit of defensive tone, with a downtick in oil markets & pressure on Chinese mainland equities amid a two-stage lockdown in the Chinese city of Shanghai garnering most of the attention on the headline front.

- The likes of the NOK & CAD are struggling with lower oil prices, although the AUD is the top performer within the G10 sphere, benefitting from commodity FX cross- & AUD/JPY related flows, with AUD/NZD moving to the highest level observed since April ’21. Note that the ruling Australian coalition will cut the fuel excise duty and support first time buyers re: the housing market when it hands down the latest Federal Budget on Tuesday.

- Looking ahead, Monday’s focus will fall on central bank speak from ECB’s Rehn & BoE Governor Bailey, with lower tier economic data due from across the globe. Elsewhere, the latest Russia-Ukraine summit in Turkey will garner interest, although there is little in the way of expectations re: a meaningful breakthrough between the two nations.

FOREX OPTIONS: Expiries for Mar28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0950-60(E1.0bln), $1.1000(E532mln)

- USD/JPY: Y120.50-70($649mln)

- USD/CAD: C$1.2535-50($1.0bln)

EQUITIES: Mixed As China Ramps Up COVID Fight

Asia-Pac equity indices are mixed, mirroring Wall St.’s performance on Friday.

- The Hang Seng outperformed, reversing earlier losses to sit 1.1% higher at typing. Losses observed in the utilities and real estate developer sub-indices were countered by gains in China-based technology large-caps, with the Hang Seng Technology Index sitting 3.0% better off at typing. To elaborate, sentiment in Chinese technology giants received a lift from Meituan’s Q4 earnings delivered last Friday, with the latter rallying 14.4% come the lunch bell.

- The CSI300 is 0.8% worse off at typing, underperforming major regional equity index peers despite recovering from declines of up to ~2% earlier in the session. The benchmark has come under pressure as authorities in the Chinese city of Shanghai announced a two-phase lockdown despite earlier assurances to the contrary, raising worry re: slower economic growth for ’22, with downside economic risks set to grow if more Chinese cities adopt similar measures to contain the spread of COVID-19. Steep losses were observed in the consumer staples sub-index, while energy and utilities outperformed.

- The Nikkei sits 0.5% lower at typing after opening lower, on track to end a nine-session streak of gains. The move lower comes despite a weakening in the JPY, with the impulse from a weaker currency failing to counter heavy losses observed in materials and industrial names.

- U.S. e-mini equity index futures sit 0.3% weaker across the board at typing.

GOLD: Lower In Asia As Dollar Rallies

Gold is $12/oz softer printing ~$1,946/oz at writing, operating a touch above Friday’s trough. The precious metal has come under pressure on the back of a firmer USD, with higher U.S. Tsy yields and Fed/BoJ policy divergence allowing the DXY to hit the highest level observed in ~2 weeks.

- To recap, bullion recovered from worst levels on Friday to close virtually unchanged, finishing the week ~$30/oz better off. The rebound was facilitated by rising tensions between Russia and the west amidst a flurry of announcements from Russia-focused meetings between leaders of the G7, NATO, and the European Council, neutralising an uptick in U.S. real yields.

- May FOMC dated OIS now prices in ~45bp of tightening, pointing to an 80% chance of a 50bp rate hike at that particular meeting. The expectation for the May FOMC is a little lower than levels witnessed early last week (after Fed Chair Powell’s hawkish comments on Monday), while OIS markets now show a cumulative ~200bp of Fed tightening priced in for the rest of calendar ’22.

- Looking to technical levels, the short-term outlook for gold is still bearish, providing space for the recent overbought conditions to unwind. Resistance is situated at $1,966.1/oz (Mar 24 high), while support is located at $1,903.7/oz (50-day EMA).

OIL: Lower As Shanghai Enters Lockdown

WTI and Brent are ~-$3.30 at typing, operating a touch above Friday’s worst levels. The benchmarks have come under pressure in Asian hours owing to the declaration of a two-phase lockdown in the Chinese city of Shanghai (even after local authorities pushed back on the idea of a lockdown in the runup to the move), raising worry re: lower fuel demand in China.

- Elsewhere, major crude benchmarks have unwound some of last Friday’s gains as the Houthi rebel group declared a unilateral temporary ceasefire over the weekend (technically due to end later Monday) on a range of offensive actions towards Saudi Arabia. To recap, WTI and Brent reversed earlier losses to close higher on Friday after the Houthi rebels claimed responsibility over an attack on oil storage facilities in Jeddah.

- Turning to the U.S., RTRS source reports have pointed to the Biden administration considering a possible 30mn bbl release of crude from the country’s Strategic Petroleum Reserves, adding to 60mn bbls released earlier this month by IEA member countries.

- Looking at the week ahead, OPEC+ meets on Thursday. International pressure on the group to raise production has so far yielded little by way of concrete commitment, with heavyweights Saudi Arabia and the UAE continuing to emphasise “balance” and “stability” instead.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/03/2022 | 1100/1200 |  | UK | BOE Bailey in Conversation w. Guntram Wolff | |

| 28/03/2022 | 1230/0830 | ** |  | US | Advance Trade, Advance Business Inventories |

| 28/03/2022 | 1430/1030 | ** | | US | Dallas Fed manufacturing survey |

| 28/03/2022 | 1430/1530 | | UK | DMO Consultation Gilt Issuance 2022/23 | |

| 28/03/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 2 Year Note |

| 28/03/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 28/03/2022 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 28/03/2022 | 1700/1300 | * | | US | US Treasury Auction Result for 13 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.