Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

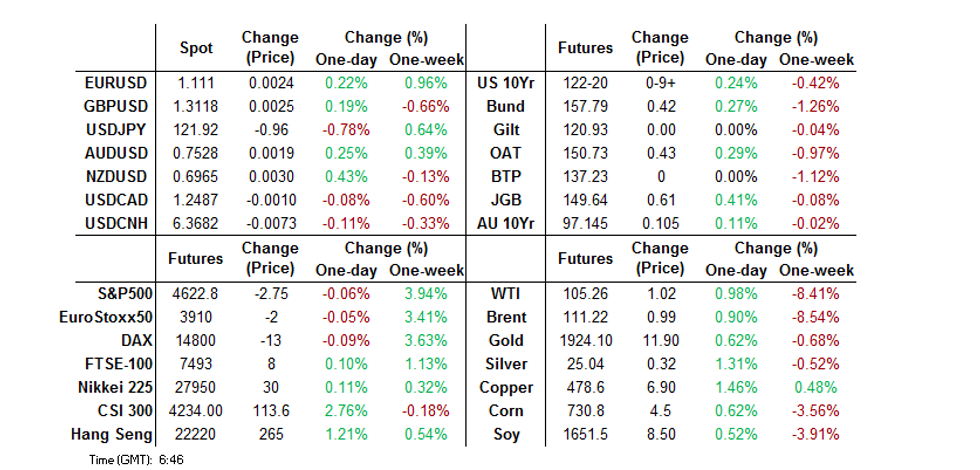

- JPY crosses snapped lower, even as the BoJ reaffirmed its dovish credentials by defending the upper end of its permitted 10-Year trading band in an unconventional manner, with yield spread gyrations & overbought conditions allowing a pullback in JPY crosses.

- Fed's Bostic ('24) didn't provide anything of note, while the latest lockdown of a Chinese city didn't result in any widespread price action.

- Looking ahead, U.S. ADP employment data, and German state & national CPI readings provide the highlights when it comes to Wednesday’s economic prints. Elsewhere, we will get a raft of central bank speakers from the Fed, ECB & BoE.

BOND SUMMARY: BoJ Action Promotes Bid In Core FI

BoJ matters were at the fore overnight, with the central bank-driven bid supporting wider core fixed income.

- That allowed TYM2 to break above Tuesday’s peak, last dealing +0-10 at 122-20+, with volume topping 190K on the session. Cash Tsys run 3-5bp richer on the days, with 5s leading the bid. There wasn’t much else in the way of meaningful headline flow, with Atlanta Fed President Bostic (’24 voter) reaffirming his views re: rate hikes (flexibility required), while pointing to uncertainty promoting some relative demand for the longer end of the Tsy curve resulting in the current flattening dynamic. Markets looked through the latest city lockdown in China (implemented in the tavel hub of Xuzhou, population ~9mn). Flow was headlined by 2 block sales of FVK2 114.00 puts (10K in total) and a block buy of FVM2 futures (+1,945), which may have been related to the options flow. Wednesday’s NY session will bring the release of ADP employment data (ahead of Friday’s payrolls print) & Fedspeak from Richmond Fed President Barkin (’24 voter) & Kansas City Fed President George (’22 voter)

- The U.S./Japan 10-Year yield differential has edged further away from the recent wides, with U.S. 10-Year Tsys managing to outperform their JGB counterparts, even as the BoJ adjusted its Rinban operations to counter recent curve-wide moves higher in yields, with upsized and unscheduled Rinban operations evident this morning, before an unconventional, unscheduled second round of Rinban operations was tendered during the Tokyo afternoon (the wider than expected focus of today’s BoJ’s purchases means that the super-long end of the JGB curve has benefitted more than 10s). JGB futures surged as a result, but have pulled back from best levels, last +60 (25 ticks off their peak). Cash JGB trade has seen bull flattening, with 30s richening by 9bp, while 7s have outperformed nearby paper given the bid in futures. JGB-OIS spreads widened as the BoJ reaffirmed its dovish credentials.

- Aussie bonds traded as a wider function of core FI markets, with no immediate reaction to firm pricing in an auction of the illiquid ACGB Apr-24 (with the same illiquidity likely resulting in extremely strong pricing, even as the cover ratio printed below 2.50x), while the AOFM’s initial FY22/23 issuance outline wasn’t as high as expected (once again, this failed to inspire price action, as the lower issuance task likely points to completed pre-funding of an upcoming ACGB maturity). YM +13.0 & XM +9.0 into the bell.

FOREX: JPY Firms In Asia, Despite BoJ Upping Defence of 10-Year Yield Target

It was another case of JPY watching during Asia-Pac hours. The U.S./Japan 10-Year yield differential has edged further away from the recent wides, with U.S. 10-Year Tsys managing to outperform their JGB counterparts, even as the BoJ adjusted its Rinban operations to counter recent curve-wide moves higher in yields, with upsizing and unscheduled Rinban operations evident this morning, before an unconventional, unscheduled second round of Rinban operations was tendered during the Tokyo afternoon (the wider focus of today’s BoJ’s purchases means that the super-long end of the JGB curve has benefitted more than 10s). We would suggest that the 2bp narrowing in the yield spread shouldn’t equate to the ~100 pip fall observed in USD/JPY (at least in isolation), but as our technical analyst previously noted, a pullback in the cross was overdue, given the overbought conditions, which is likely factoring into the move. JPY sits atop the G10 FX pile as a result, although it wasn’t all one-way trade, with the initial reaction to the BoJ’s first Rinban announcement being one of limited JPY weakness, before yield differential took control. USD/JPY last deals at Y121.85 (after printing as low as Y121.32), with initial technical support at Y121.97 breached, bears now look to the Mar 24 low (Y120.95) as the next meaningful target. JPY

- The aforementioned downtick in U.S. Tsy yields and pull lower in USD/JPY applied some pressure to the USD in a broader context, with the greenback finding itself at the bottom of the G10 FX pile as a result.

- There wasn’t much in the way of meaningful headline flow elsewhere, with the latest localised city-wide lockdown in China having little impact on broader price action.

- Looking ahead, U.S. ADP employment data, and German state & national CPI readings provide the highlights when it comes to Wednesday’s economic prints. Elsewhere, we will get a raft of central bank speakers from the Fed, ECB & BoE.

FOREX OPTIONS: Expiries for Mar30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1000(E2.7bln), $1.1050-60(E1.7bln), $1.1100(E1.5bln), $1.1150-55(E1.1bln), $1.1195-00($1.6bln)

- GBP/USD: $1.3195-00(Gbp774mln)

- EUR/JPY: Y121.00-05(E636mln), Y122.00-05(E660mln), Y122.90-00(E870mln)

- USD/CAD: C$1.2500($503mln), C$1.2525($640mln)

EQUITIES: Mostly Higher As Russia-Ukraine Worry Moderates

Asia-Pac equity indices are mostly higher on a positive lead from U.S. and European markets, with Japanese stocks bucking the wider trend of gains. High-beta equities across the region broadly outperformed as hope re: a de-escalation in the Russia-Ukraine conflict has spilled over into Asian hours, adding to an easing in stagflation-linked worry as commodity benchmarks have backed away from recent highs as well.

- The CSI300 leads gains amongst regional peers, being 2.0% better off at writing and operating at session highs. Richly valued consumer staples and healthcare stocks lead gains, with the largest contributions observed in Chinese liquor stocks. Chinese tech stocks caught a strong bid as well, with the tech-heavy ChiNext and STAR50 sitting 2.9% and 2.3% higher at typing respectively.

- The Hang Seng trades 1.2% higher at typing, led by gains in the real estate and financials sub-indices. The index has backed away from session highs as China-based tech stocks pared earlier gains, with the Hang Seng Tech Index printing 0.3% better off at typing after recording gains of up to 2.3% earlier in the session. The pullback comes as WSJ source reports have pointed to Chinese authorities planning to place curbs on the country’s $30bn live-streaming industry, raising worry re: regulatory action on some large-cap technology names.

- The Japanese Nikkei 225 underperformed, sitting 1.4% lower at typing. The move lower comes as the JPY has retreated below Y122.00 in Asia, unwinding some of the recent dynamic re: yen weakness boosting hopes re: corporate earnings for Japanese companies.

- U.S. e-mini equity index futures deal 0.1% to 0.2% weaker at typing.

GOLD: Higher In Asia

Gold deals ~$4/oz firmer to print ~$1,923/oz at writing, with the move higher facilitated by a downtick in the USD and U.S. Tsy yields.

- To recap, bullion briefly fell to one-month lows ($1,890.2/oz) on Tuesday as perceived progress in Russia-Ukraine talks facilitated risk-positive outflows. Still, the yellow metal pared losses when Russian negotiators cautioned that talks had “a long way to go”, while western-led scepticism over Russian concessions further shaved earlier optimism re: a de-escalation in the conflict, with prices ultimately closing ~$3/oz lower for the day.

- To elaborate, Russia’s announcement to scale back military activity around Ukraine’s north did not address recent Russian plans to concentrate forces in the east of the country, with the U.S. calling the former a “repositioning” rather than a withdrawal. Well-documented Russian demands for Ukraine to cede territories also saw incremental progress, with Ukraine offering to discuss the matter separately from ongoing ceasefire negotiations.

- On the technical front, gold’s move lower on Tuesday breached support at ~$1,902.7/oz (50-Day EMA) and $1,895.3/oz (Mar 16 low) exposing further support at $1,878.4/oz (Feb 24 low and key short-term support).

OIL: Slightly Higher Amidst Russia-Ukraine Worry As Chinese Demand Outlook Provides Balance

WTI and Brent are ~$0.70 firmer apiece, printing $104.9 and $110.9 respectively at typing. Both benchmarks operate comfortably above Tuesday’s trough as some hope re: progress in Russia-Ukraine ceasefire talks has turned to caution, with well-documented western scepticism towards Russia’s announcements of military de-escalations in the north of Ukraine doing the rounds in Asia.

- To recap, WTI and Brent fell to session lows at $98.44 and $104.84 respectively on Tuesday amidst perceived progress in ongoing Russia-Ukraine negotiations, before erasing losses as the top Russian negotiator stated that talks had “a long way to go”.

- Looking to China, demand worry remains elevated as authorities announced a rise in both symptomatic and asymptomatic cases (total of 8,825 cases for Mar 29 vs. 7,051 for Mar 28), with a 3-day lockdown announced in the Chinese city of Xuzhou as well (population ~9mn).

- Turning to the Middle East, there has been no discernible progress in indirect U.S.-Iran nuclear talks.

- Elsewhere, weekly U.S. API inventories crossed on Tuesday, with reports pointing to drawdowns in crude, gasoline, distillate, and Cushing hub stocks. Looking ahead, EIA data is due later on Wednesday (1430 GMT), with WSJ median estimates calling for declines in crude, gasoline, and distillate stockpiles as well.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/03/2022 | 0600/1400 | ** |  | CN | MNI China Liquidity Survey |

| 30/03/2022 | 0600/0800 | ** |  | SE | Retail Sales |

| 30/03/2022 | 0700/0900 | *** |  | ES | HICP (p) |

| 30/03/2022 | 0700/0900 | * |  | CH | KOF Economic Barometer |

| 30/03/2022 | 0800/1000 | * |  | IT | Industrial Orders |

| 30/03/2022 | 0800/1000 | *** |  | DE | Bavaria CPI |

| 30/03/2022 | 0800/1000 |  | EU | ECB Lagarde Speech at Central Bank of Cyprus | |

| 30/03/2022 | 0810/0910 |  | UK | BOE Broadbent Speaks at NIESR | |

| 30/03/2022 | 0900/1100 | ** | | EU | Economic Sentiment Indicator |

| 30/03/2022 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 30/03/2022 | 0900/1100 | * | | EU | Business Climate Indicator |

| 30/03/2022 | 0900/1100 | *** | | DE | Saxony CPI |

| 30/03/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 30/03/2022 | 1200/1400 | *** | | DE | HICP (p) |

| 30/03/2022 | 1215/0815 | *** | | US | ADP Employment Report |

| 30/03/2022 | 1230/0830 | *** | | US | GDP (3rd) |

| 30/03/2022 | 1315/0915 | | US | Richmond Fed's Tom Barkin | |

| 30/03/2022 | 1415/1615 | | EU | ECB Panetta Hearing on Digital Euro at ECON | |

| 30/03/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 30/03/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 30/03/2022 | 1700/1300 | | US | Kansas City Fed's Esther George |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.