Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

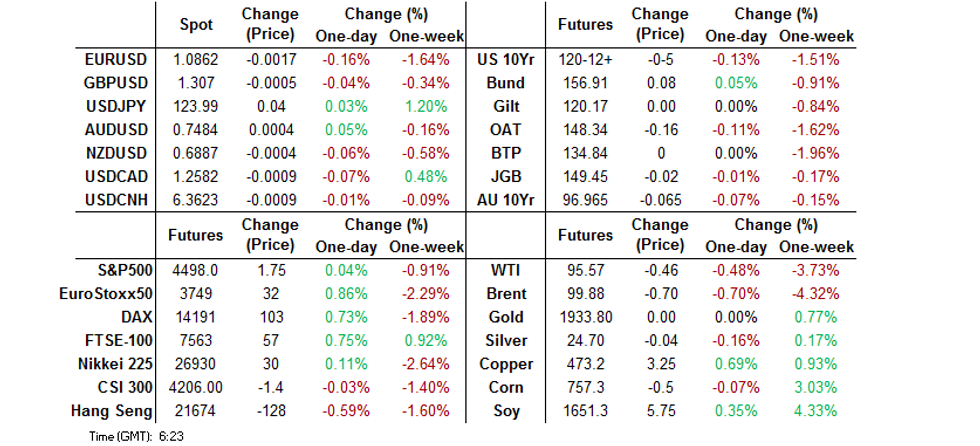

- The spectre of aggressive Fed tightening action looms large, helping the DXY logde a fresh cycle high.

- Initial bid into core FI futures fades ahead of the London open, with flattening impetus evident in U.S. Tsy yield curve.

- Focus turns to U.S. wholesale inventories, Canadian jobless rate, Japan's Eco Watchers Survey & plenty of ECB speak.

BOND SUMMARY: JGBs Keep Pushing Higher, U.S. Tsys & ACGBs Lose Initial Allure

JGBs maintained bullish momentum, diverging from U.S. Tsys and Aussie bonds which lost their initial strength. The prospect of hawkish FOMC action loomed large at the end of a week that witnessed fresh rounds of bullish Fedspeak.

- The initial uptick in T-Notes proved short-lived, with the contract plunging in afternoon trade and probing the water below Thursday's worst levels. TYM2 last changes hands -0-03+ at 120-14, hovering just above the session low of 120-11. Eurodollar futures run 1.5-6.0 ticks lower through the reds. Twist flattening evident in cash Tsy space, with yields last seen +4.1bp to -2.3bp across the curve. Wholesale inventories headline the U.S. docket on Friday.

- 10-Year Aussie bond futures moved in tandem with T-Notes, XM trades -6.0 when this is being typed. Bills run 1-4 ticks lower through the reds. Cash ACGB curve has bear steepened, with yields last seen 1.5bp-5.7bp higher, as Aussie bonds played catch up with impetus from the NY session. The RBA released the semi-annual Financial Stability Review, in which it warned against "elevated" medium-term systemic risks.

- JGB futures re-opened on a firmer footing and extended gains thereafter, posting a sharp upswing just after the Tokyo lunch break. JBM2 trades at 149.51 at typing, 4 ticks above last settlement. Cash trade saw JGBs register gains, with yields depressed across the curve, with the super-long end leading gains. Participants kept an eye on the scheduled round of 1-10 Year Rinban operations but purchase sizes were unchanged, albeit it is worth flagging downticks in bid/cover ratios, which may have supported underlying bullish momentum in afternoon trade:

- 1- to 3-Year: 2.62x (prev. 3.02x)

- 3- to 5-Year: 1.90x (prev. 2.64x)

- 5- to 10-Year: 1.86x (prev. 1.92x)

FOREX: DXY Edges Higher, Yen Consolidates Around Y124

The latest headline flow failed to add much new to the familiar narrative. The key gauge of broader USD strength (DXY) lodged a fresh cycle high, approaching the psychologically important 100 level. The greenback gained as U.S. Tsy yields pushed higher, driven by a sell-off in short end of the curve, as a week marked by continued hawkish Fed drumbeat draws to an end.

- The kiwi dollar underperformed ahead of next week's monetary policy decision, with NZD/USD lodging its worst levels in more than two weeks. It is unclear whether New Zealand's central bank will opt for an outsized 50bp rate hike, albeit the OIS strip prices a ~67% chance of of such outcome. NZD/USD implied 1-week volatility holds near yesterday's multi-week high.

- USD/JPY consolidated around the round figure of Y124.00 which provided a firm layer of resistance on Thursday. A breach of that level entailed further buying in early trade, with the rate running as high as to Y124.23. Demand petered out and the rate sank into negative territory ahead of the Tokyo fix, before a bouncing towards neutral levels.

- Offshore yuan slipped as China Securities Journal ran a front-page report noting that China is likely to cut banks' RRR in Q2, while Shanghai declared more than 20k new Covid-19 infections.

- Today's data highlights include U.S. wholesale inventories, Canadian jobless rate & Japan's Eco Watchers Survey. Speeches are due from ECB's de Cos, Centeno, Panetta, Stournaras, Makhlouf & Herodotou.

FOREX OPTIONS: Expiries for Apr08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0825-50(E1.3bln), $1.0990-05(E3.3bln), $1.1045-50(E555mln)

- USD/JPY: Y119.75-95($1.3bln), Y124.00($730mln)

- USD/CAD: C$1.2500($859mln), C$1.2665-70($531mln), C$1.2750($616mln)

ASIA FX: Fed Hawkishness Undermines Asia EM FX

The spectre of aggressive Fed tightening loomed large, sapping strength from Asia EM currencies on Friday.

- CNH: Spot USD/CNH crept higher as China Securities Journal outlined the case for an RRR cut that could com to fruition in Q2, while Shanghai continued to battle its Omicron outbreak declaring more than 21,000 new Covid-19 cases.

- KRW: South Korean won retreated as participants assessed this week's barrage of hawkish Fed commentary. The prospect of aggressive Fed tightening resulted in the won being the worst performer in the region. Recall that the BoK will meet next week but its Governor-nominee is unlikely to be confirmed by then.

- IDR: Spot USD/IDR rejected resistance from Mar 24 high of IDR14,380 and pulled back, virtually erasing its initial gains. The official consumer confidence index weakened to 111.0 last month from 113.1 prior, touching a six-month low even as optimists still outnumber pessimists.

- MYR: Spot USD/MYR advanced, printing fresh weekly highs as a result.

- PHP: Spot USD/PHP crept higher even as data showed that the Philippines' trade deficit narrowed in February.

- THB: The baht faltered in tandem with most of its regional peers, even as Thai officials decided to ease Covid-19 rules for foreign visitors.

- INR: The rupee caught a bid as the Reserve Bank of India kept its benchmark policy rate unchanged at 4.0% and restored its Liquidity Adjustment Facility corridor to 50bp, while upgrading its FY23 inflation forecast.

EQUITIES: Mixed As Chinese Regulatory Worry Rises, Hawkish Fed In View

Most major Asia-Pac equity indices are mixed, largely bucking a positive lead from Wall St. High-beta stocks across the region underperformed, with the spotlight on China-based tech as large-cap Tencent Holdings made a decision to shutter their video game streaming service, fanning familiar fears over regulatory risks.

- The Hang Seng sits 0.6% lower at typing, approaching the week’s worst levels after 3 consecutive lower daily closes. China-based tech bore the brunt of the downward pressure, with the Hang Seng Tech Index trading 2.3% weaker at writing, with steep losses observed in large-caps such as Bilibili (-7.8%), JD.com (-3.4%), and Netease Inc (-2.3%).

- The ASX200 was the sole index to record gains amongst major regional peers, dealing 0.4% firmer at typing, led by outperformance in materials and energy names. On the other hand, the S&P/ASX All Technology Index underperformed, sitting 0.4% worse off at typing, with large-cap Block Inc dragging the index lower.

- U.S. e-mini equity index futures sit virtually unchanged at writing, trading on either side of neutral throughout Asian hours.

GOLD: A Little Lower As Fed Hawkishness, Developments In Ukraine Eyed

Gold is ~$3/oz lower to print $1929/oz at typing, backing away from best levels and operating at session lows as the greenback has strengthened, with the DXY notching fresh cycle highs in Asian hours.

- The precious metal has traded within a relatively tight ~$30/oz trading range throughout the week, struggling to make headway above ~$1,940/oz as the DXY and U.S. real yields have steadily climbed over the same period, hitting successive cycle highs in the process.

- Looking to the Russia-Ukraine conflict, there has been virtually no concrete progress in ongoing ceasefire/peace talks, with Russian FM Lavrov on Thursday describing the latest Ukrainian draft deal (submitted on Wednesday) as “unacceptable”. Elsewhere, the west continues to impose additional sanctions on Russia in the wake of alleged war crimes in Ukraine, but the EU’s progress towards closely-watched bans on Russian crude imports remains scant, with Germany and Hungary continuing to lead opposition to the measure.

- From a technical perspective, bullion remains range bound, with the outlook remaining bearish following the pullback from $2,070.4/oz (Mar 8 high). Initial support is situated around ~$1,908.9/oz (50-Day EMA), with further support at $1,890.2/oz (Mar 29 low and bear trigger). Resistance is seen at $1,966.1/oz (Mar 24 high).

OIL: Lower On Fading EU Sanction Worry, Ongoing Outbreak In China

WTI is ~-$0.30 and Brent is ~-$0.50, sitting ~$2 above Thursday’s trough at writing. Both benchmarks appear headed for their second straight lower weekly close (and on track for a fourth consecutive lower daily close), and trade a touch above levels last witnessed before the Russian invasion of Ukraine.

- Earlier worry surrounding the likelihood of an EU ban on Russian crude imports has eased from highs seen earlier in the week, with well-documented German and Hungarian-led opposition to the measure remaining intact for now. A note that BBG source reports have also pointed to Russian Sokol crude finding more buyers in Asia, with cargoes for May currently sold out.

- Looking ahead, the EU is due to soon pass a (phased) ban on Russian coal that RTRS source reports have suggested will take full effect in mid-August, while the EU’s top diplomat Borrell has said that the bloc’s FMs will meet on Apr 11 to discuss the possibility of sanctions on Russian crude.

- Elsewhere, concern re: China’s energy demand have intensified, as nationwide daily COVID case counts continue to rise. Authorities in Shanghai reported over 20K fresh cases (both symptomatic and asymptomatic) for Apr 7 with the city’s lockdown remaining indefinite for now, keeping most business and factories shuttered.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/04/2022 | 0001/0101 | ** |  | UK | IHS Markit/REC Jobs Report |

| 08/04/2022 | 0600/0800 | ** |  | NO | Norway GDP |

| 08/04/2022 | 0700/0900 | ** |  | ES | Industrial Production |

| 08/04/2022 | 0800/1000 | * |  | IT | Retail Sales |

| 08/04/2022 | 1115/1315 |  | EU | ECB Panetta at IESE Business School Conference | |

| 08/04/2022 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 08/04/2022 | 1400/1000 | ** |  | US | Wholesale Trade |

| 08/04/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.