Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

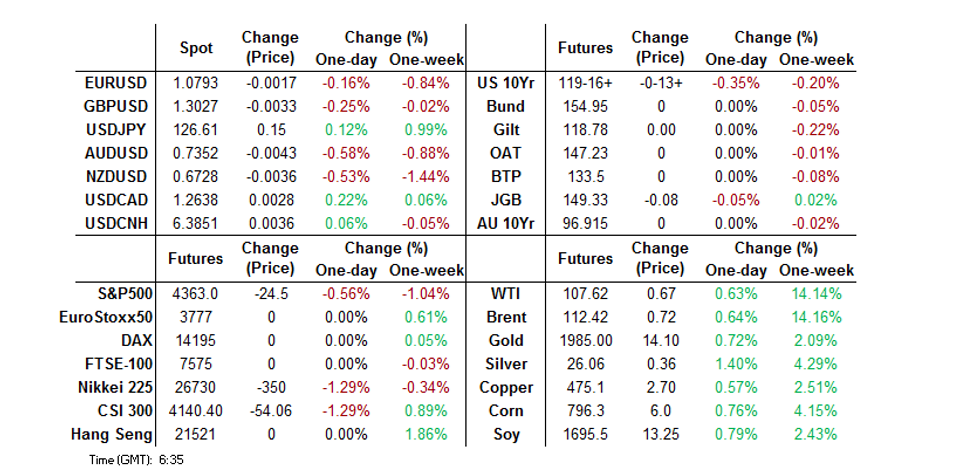

- Chinese headlines dominated as some participants returned from the elongated weekend, with mixed economic data, a smaller than expected RRR cut from the PBoC, wider spread COVID-related mobility restrictions observed and Shanghai sketching out its exit plan from its own restrictions.

- Tsy yields moved higher, clinging to the uptick in oil and some of the positives, with the growth negatives weighing on equities but doing little to support core FI markets. The uptick in Tsy yields supported the DXY.

- NAHB Housing data out of the U.S. & Fedspeak from St. Louis Fed President Bullard (’22 voter) headline the docket on Monday. A reminder that holidays in London, Europe, Australia & Hong Kong will thin out wider liquidity.

US TSYS: Cheaper In Asia

TYM2 has nudged higher in recent trade, to last deal 0-12+ at 119-17+, 0-06 off the base of its 0-15 Asia range, on respectable volume of ~115K (given holidays in the likes of Hong Kong, Australia, London & Europe). Cash Tsys are 2.0-3.5bp cheaper across the curve, with 3s leading the way lower and the long end lagging the wider move at the margin.

- Tsys softened in early Asia-Pac dealing. with participants seemingly clinging to the uptick in crude oil (which has moderated from extremes), with that move, at least in part, facilitated by the Chinese city of Shanghai sketching out its re-opening plan.

- Meanwhile, growth negative factors e.g. a smaller than expected RRR cut from the PBoC, the ongoing Russia-Ukraine conflict and wider spread localised lockdowns in China had little impact.

- Chinese economic data was mixed, with firmer than expected Q1 GDP & Mar industrial production at least partially offset by a larger expected fall in retail sales and unexpected uptick in the unemployment rate.

- TYM2 drifted to fresh session lows in the wake of the data release, although the move was by no means immediate, before the aforementioned uptick in recent dealing.

- The latest NAHB housing data print and Fedspeak from Bullard (’22 voter) headline during NY hours.

JGBS: Curve Steepens, Futures In Narrow Range

The cheapening impetus from U.S. Tsys was felt in the JGB space, with benchmark JGBs running little changed to ~2bp cheaper as we move towards the Tokyo close.

- 5s lagged the wider sell off, while the super-long end of the curve led the way lower. JGB futures are 8 ticks softer on the day, off worst levels of the session, hugging a narrow range.

- Most of the local focus has fallen on the latest raft of policy maker communique re: FX matters. On that front, Japanese Finance Minister Suzuki reiterated the need for vigilance when it comes to monitoring FX rates, presenting some indecision when it came to the net impact of the recent JPY weakness.

- Elsewhere, there was a more guarded tone from BoJ Governor Kuroda re: JPY weakness, with a particular focus on the speed of moves and impact that such moves can have on different sectors of the economy (although he did ultimately reaffirm the overall net positive impact of a weaker JPY on the Japanese economy, noting that it is still “basically positive overall”)

FOREX: USD Benefits From Higher Tsy Yields

An uptick in U.S. Tsy yields has allowed the broader DXY to firm in G10 FX trade.

- The greenback is outperforming all of its G10 FX counterparts, with the Aussie & kiwi finding themselves at the bottom of the G10 FX table as questions re: the health of the Chinese economy continue to circle, weighing on the China-sensitive Antipodean currencies.

- On that front, Q1 Chinese GDP data topped exp., although monthly economic activity data for March was a little more mixed, with retail sales falling by a larger than expected clip (more worry is evident on that front owing to widening localised COVID lockdowns), unemployment unexpectedly ticking higher and industrial production beating expectations. NZD/USD moved to the lowest levels observed since late Feb, while AUD/USD softened to levels not seen since 17 March.

- USD/CNH stuck to a very narrow ~100 pip range, failing to really react to the data, news that Shanghai has started to sketch out the path away from mobility restrictions and after the PBoC delivered a smaller than expected RRR cut on Friday.

- Higher crude prices and Tsy yields saw USD/JPY print a fresh cycle high of Y126.79 before the combination of Tokyo fix-related flows, Japanese Finance Minister Suzuki reiterating the need for vigilance when it comes to monitoring the FX rate/presenting some indecision when it came to the net impact of the recent JPY weakness and a more guarded tone from BoJ Governor Kuroda re: JPY weakness, with a particular focus on the speed of moves and impact that such moves can have on different sectors of the economy (although he did ultimately reaffirm the overall net positive impact of a weaker JPY on the Japanese economy, noting that it is still “basically positive overall”), combining to push USD/JPY to session lows of Y126.25, before the cross rebounded to last deal around Y126.65.

- NAHB Housing data out of the U.S. & Fedspeak from St. Louis Fed President Bullard (’22 voter) headline the docket on Monday. A reminder that holidays in London, Europe, Australia & Hong Kong will thin out wider liquidity.

EQUITIES: Mixed In Asia; Chinese GDP Provides Little Relief

Major Asia-Pac equity indices are mixed at writing, with Japanese and Chinese equities broadly underperforming.

- The Nikkei 225 brings up the rear amongst its major regional peers, rising from session lows to sit 1.4% weaker at typing. ~200 of the index’s 225 constituents are in the red, with large-cap names such as Nintendo Co and Fast Retailing Co leading losses. The financials sub-index bucked the broader trend of losses amongst peers, trading 0.8% higher largely on outperformance in Credit Saisson Co.

- The CSI300 deals 0.9% softer at typing, rising from session lows on the mixed Chinese Q1 GDP release (that saw faster GDP growth, but weaker retail sales and the highest jobless rate since May ‘20). Consumer staples and financials equities struggled, while stocks in semiconductor, automobile, and medical equipment production were notably bid, benefiting from the Chinese authorities announcing on Friday that 666 companies in those sectors would be allowed to resume production in Shanghai. The tech-heavy STAR50 has correspondingly caught a bid, trading 2.7% higher at writing.

- The Hang Seng outperformed, adding 0.7% at writing amidst gains in virtually all major sub-indices. Real estate names and China-based tech outperformed, with the Hang Seng Properties Index and Hang Seng Tech Index dealing 2.1% and 1.2% higher at typing.

- U.S. e-mini equity index futures sit 0.2% to 0.9% worse off at typing, with relatively high-beta NASDAQ contracts leading losses.

GOLD: Higher On Stagflation Worry

Gold is ~$5/oz better off at $1,983/oz, back from fresh five-week highs made earlier in the session. The overall move higher comes as major crude benchmarks have extended a three-day streak of gains in Asia-Pac dealing, fuelling worry from some quarters re: stagflation despite a broad uptick in nominal U.S. Tsy yields and the USD (DXY).

- To recap, the precious metal closed ~$5/oz firmer in the previous week on the highest headline U.S. CPI print since 1981, although the lower-than-expected M/M increase in Mar core CPI likely helped cap gains as some have regarded it as a possible sign of inflationary pressures peaking.

- Elsewhere, hope surrounding a diplomatic resolution to the Russia-Ukraine conflict has likely evaporated, with Ukrainian leaders stating over the weekend that peace talks would end if Russian forces eliminate the remaining defenders of the city of Mariupol.

- Debate over a “de facto” EU ban on Russian gas has also done the rounds in Asia (re: the EU’s inability to pay in rubles due to sanctions), raising worry over the potential for elevated energy prices.

- Looking ahead, focus will turn to the Fed’s Bullard as he speaks on the U.S. economy and monetary policy later in the U.S. session (2000 GMT).

- From a technical perspective, the short-term outlook is bullish, following the recent move above $1,966.1/oz (Mar 24 high). Resistance is situated at $2,001.6/oz (61.8% retracement of Mar8-29 downleg), while immediate support is seen at around ~$1,942.6/oz, near the 20-Day EMA.

OIL: Light Bid On Libyan Disruption; EU Oil Sanctions In The Works

WTI is +$0.90 and Brent is +$1.10 at writing, back from best levels and on track to extend a three-session streak of gains. Both benchmarks have caught a light bid as focus turns to the European Commission’s preparations to include oil in the EU’s incoming sixth round of sanctions on Russia, with European Commission head von der Leyen touting “clever mechanisms” to include Russian oil in the package, adding to well-documented worry over shortfalls in global crude supplies.

- A note that both the IEA and OPEC revised their crude demand forecasts for ‘22 downwards last week, pointing to overall lower-than-expected consumption from OECD countries, and an ongoing COVID outbreak in China.

- To elaborate, the Chinese authorities continue to expand pandemic control measures, with more areas/cities being placed under some form of movement restrictions, most notably a partial lockdown on the city of Xian (pop. 13mn) on Friday.

- Elsewhere, some Libyan oil production and export operations were suspended after protestors forced their way into the Al-Fil oil field and two ports on Sunday, resulting in disruptions at all three locations. Production at the Al-Fil oil field is estimated at around 70K bpd, while a RTRS source report pointed to a tanker being blocked from loading ~1mn bbls at the port of Zueitina.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/04/2022 | 1400/1000 | ** |  | US | NAHB Home Builder Index |

| 18/04/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 18/04/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 18/04/2022 | 2000/1600 | | US | St. Louis Fed's James Bullard | |

| 18/04/2022 | 2230/1830 | | US | New York Fed's Lorie Logan | |

| 19/04/2022 | 0430/1330 | ** |  | JP | Industrial production |

| 19/04/2022 | - |  | EU | ECB Lagarde & Panetta in IMF/World Bank Meetings | |

| 19/04/2022 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 19/04/2022 | 1230/0830 | *** | | US | Housing Starts |

| 19/04/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 19/04/2022 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 19/04/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 19/04/2022 | 1605/1205 | | US | Chicago Fed's Charles Evans |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.