Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

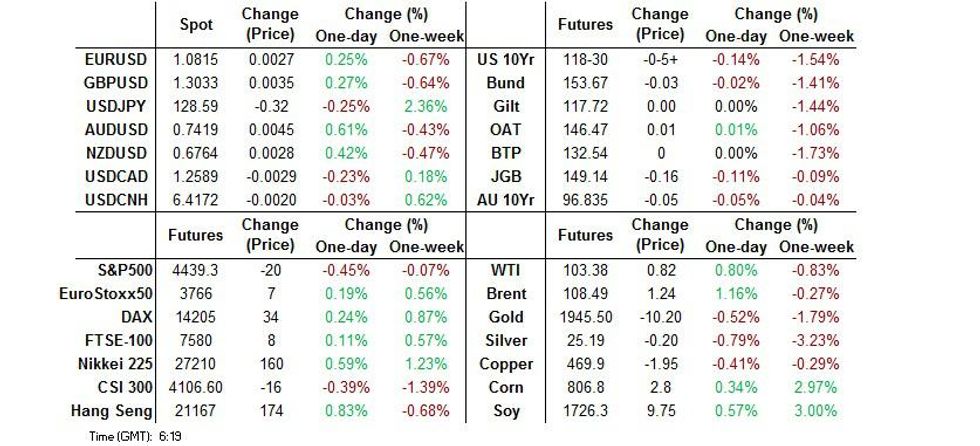

- The initial spill over from Tuesday’s NY cheapening led the Tsy complex lower in early Asia-Pac dealing, with the major cash Tsy benchmarks (from 2s to 30s) tagging fresh cycle highs in yield terms and 10-Year real yields briefly turning positive for the first time since early ’20. The early cheapening impulse reversed as the latest round of PBoC LPR fixings came in at unchanged levels (vs. BBG median expectations for a 5bp cut to both the 1- & 5-Year fixings), with last week’s restrained PBoC easing failing to do enough when it comes to reducing bank costs to a level whereby lower fixings would have been deemed feasible.

- The yen staged a comeback even as the initial round of sales in early Tokyo trade briefly pushed USD/JPY above the Y129.00 figure. The rate's advance towards the psychologically important Y130.00 figure put the resolve of JPY bears to a test, with participants trying to estimate the probability of an intervention around that level.

- Focus moves to Canadian CPI data and U.S. existing home sales as well as comments from several Fed & ECB speakers. The European evening will see eyes turn to the televised debate between French Presidential candidates Macron & Le Pen.

US TSYS: Little Changed After Curve-wide Fresh Cycle Highs In Yield Terms

The initial spill over from Tuesday’s NY cheapening led the Tsy complex lower in early Asia-Pac dealing, with the major cash Tsy benchmarks (from 2s to 30s) tagging fresh cycle highs in yield terms and 10-Year real yields briefly turning positive for the first time since early ’20.

- The early cheapening impulse reversed as the latest round of PBoC LPR fixings came in at unchanged levels (vs. BBG median expectations for a 5bp cut to both the 1- & 5-Year fixings), with last week’s restrained PBoC easing failing to do enough when it comes to reducing bank costs to a level whereby lower fixings would have been deemed feasible.

- The resultant leg lower in Chinese equities and e-minis supported Tsys, with pockets of screen buying in TYM2 futures providing the most notable flow of Asia trade, pulling the contract/space further away from session cheaps. Note that e-minis were already lower in the wake of Netflix earnings (led by the NASDAQ 100 contract), with both the Chinese equity space and e-minis now off of worst levels as we head into London dealing (likely aided by calls from an ex-PBoC official re: easing the restrictions on property developer debt).

- TYM2 is -0-05 at 118-30+ on volume of ~190K, trading closer to the top of its 0-15 overnight range than the bottom. Meanwhile, cash Tsys are little changed on the session.

- In overnight Fedspeak, Minneapolis Fed President Kashkari (’23 voter) noted that the Fed may have to do more to tame inflation if Chinese lockdowns cause further headwinds for global trade logistics.

- Looking ahead to NY hours, existing home sales data will cross, with the release of the Fed’s beige book set to be supplemented by Fedspeak from Bostic (’24 voter), Daly (’24 voter) & Evans (’23 voter).

JGBS: Futures Off Worst Levels, Little Reaction To BoJ Ops

Trade in JGB futures has been two-way since the re-open, albeit contained.

- The contract is a touch above late overnight levels ahead of the Tokyo bell, -16 vs. Tuesday’s settlement.

- Cash JGBs are 0.5-2.0bp cheaper on the day, with the super-long end leading the way lower. Note that 10-Year JGBs are sitting at 0.25%, with the latest round of BoJ fixed rate operations failing to push 10-Year JGB yields away from the upper boundary of the Bank’s permitted trading range. Note that the BoJ has not came in with a second round of fixed rate ops/Rinban.

- On the fiscal front there have been some apparent leaks re: the support package that will be announced in the coming weeks, with one pillar centring on cash handouts to low income Japanese families with children.

- A liquidity enhancement auction for off-the-run 15.5- to 39-Year JGBs headlines the domestic docket on Thursday.

AUSSIE BONDS: Bear Flattening

The weakness in YM remains a little stickier than in XM, with the former trickling back towards session lows after the U.S. Tsy-led, PBoC-driven uptick flagged elsewhere. YM -8.0 & XM -5.0 at typing. Super long ACGBs are ~4bp cheaper on the session.

- EFPs are wider on the day, with the 3-/10-Year box flattening.

- Bills are 4-10 ticks cheaper through the reds, with little reaction to the latest 3-month BBSW fixing, which set ~2.8bp higher. Note that the cheapening in the bond space had already shifted Bills lower pre-fixing.

- An uptick in the weekly ANZ-Roy Morgan consumer confidence print (although the index was still comfortably below 100.0) and firm Westpac leading index reading had little impact on the space.

- One other matter to be aware of in coming sessions will be the potential re-deployment of ACGB coupon payments, with ~A$4.9bn of ACGB coupons being paid yesterday. Elsewhere, the cash flows surrounding the maturity of the A$7.0bn 22 April ’22 note may impact the shorter end of the curve intraday in the coming sessions.

- Thursday’s local docket looks particularly light.

FOREX: Yen Pauses Dramatic Sell-Off, Greenback Retreats

The yen staged a comeback even as the initial round of sales in early Tokyo trade briefly pushed USD/JPY above the Y129.00 figure. The rate's advance towards the psychologically important Y130.00 figure put the resolve of JPY bears to a test, with participants trying to estimate the probability of an intervention around that level.

- Japan's Deputy Chief Cabinet Secretary Isozaki said that the government will coordinate with other currency authorities as it continues to watch FX moves with vigilance. Local officials have been issuing warning on rapid yen weakening pretty much every day lately.

- The BoJ stepped in with unlimited fixed-rate JGB purchases to enforce the official cap on 10-Year JGB yield. The action was expected, but there was speculation that some participants expected something extra.

- For the record, Japan's March trade deficit proved deeper than expected. While the yen showed little reaction to domestic data (as it usually does), the report should give JPY bears another argument in support of their case.

- USD/JPY implied volatilities kept rising across the curve (1-year tenor reached a new two-year high). The pair's 3-month 25 delta risk reversal erased its initial uptick but remains above par.

- The pullback in USD/JPY coincided with a bout of broader greenback sales, making the U.S. dollar the worst performer among the world's major currencies.

- The greenback's retreat allowed USD/CNH to give away its initial gains. The rate had earlier shot higher in reaction to the PBOC fix, with China's central bank setting the yuan reference rate ~100 pips above sell-side estimate.

- Antipodean FX paced gains in the G10 basket. Although AUD/JPY moved away from fresh multi-year highs, it managed to hold above the Y95.00 mark cleared on Tuesday, when the rate charted a bull pennant pattern.

- Focus moves to Canadian CPI data and U.S. existing home sales as well as comments from several Fed & ECB speakers.

FOREX OPTIONS: Expiries for Apr20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0790-11(E1.5bln), $1.0875(E588mln)

- AUD/USD: $0.7400-20(A$909mln)

- USD/CAD: C$1.2600-15($680mln)

ASIA FX: Yuan Takes Hit From Weak Bias In PBOC Fix, But Quickly Licks Its Wounds

The dollar index (DXY) lost some altitude along U.S. Tsy yields, which applied pressure to USD/Asia crosses late doors. The PBOC drew attention by failing to trim benchmark policy rates despite expectation that it would take a more supportive attitude as China is battling its renewed outbreak of Covid-19.

- CNH: Offshore yuan had a round trip to multi-month highs. It took a hit as the PBOC set the mid-point of permitted USD/CNY trading range ~100 pips above average estimate, while keeping the Loan Prime Rates unchanged (BBG consensus looked for 5bp cuts). But these losses proved short lived and USD/CNH pulled back into negative territory amid a bout of broad-based USD sales.

- KRW: Spot USD/KRW had a look above the KRW1,235.00 mark before erasing its initial gains. The IMF slashed its 2022 growth outlook for South Korea, while revising the inflation forecast sharply higher.

- IDR: The rupiah held a fairly tight range, retaining its recent stability. It was unfazed by yesterday's monetary policy decision from Bank Indonesia, which kept the 7-Day Reverse Repo Rate unchanged, while hinting at less urgency to tighten.

- MYR: The ringgit paced losses in the Asia EM basket. Spot USD/MYR opened sharply higher as onshore players returned from a public holiday. The rate trimmed the bulk of gains as the greenback lost ground, but managed to print a fresh multi-month high beforehand.

- PHP: The peso operated in close proximity to the PHP52.500 mark, which has provided a ceiling to recent price action.

- THB: Spot USD/THB rose to its highest point since early December, before giving away the bulk of those gains.

EQUITIES: Mostly Higher In Asia; Search For Bottom In Chinese Equities Continues

Major Asia-Pac equity indices are mostly higher at writing, largely following a positive lead from Wall St.

- The CSI300 sits 0.5% softer at typing, on track to record a fourth straight day of losses despite rising from session lows. The earlier move lower came as the PBOC chose to hold LPR rates steady, largely surprising market expectations. The real estate sub-index (-4.4%) underperformed as the sector looks set to continue struggling with a liquidity crunch, compounding dismal new home sales data earlier on Monday (-25.6% YTD Y/Y) pointing to a third straight quarter of declines. On the other hand, consumer staples outperformed, with the sub-index hitting one-month highs earlier in the session on broad gains in Chinese liquor companies.

- Taking a step back, hopes for economic stimulus/easier monetary policy in China amidst an ongoing barrage of weak economic data have largely evaporated for now, following no change to the MLF rate last week, as well as a 25bp RRR cut (against hopes for a less “conservative” 50bp cut). Many are now looking to consideration for supportive measures to be taken in Q2 instead in line with a more cautious pace of easing, in line with intensifying official rhetoric re: supportive policy.

- The Nikkei 225 sits 0.9% better off at typing, back from best levels after the JPY staged a comeback, with USD/JPY on track to snap a 13-day streak of gains. Export-related names particularly in electronics and automobile manufacturers nonetheless held on to earlier gains, with large-cap Fast Retailing contributing the most.

- U.S. e-mini equity index futures are 0.1% to 0.7% worse off at writing, rising from worst levels inspired by Netflix’s -25.7% after-hours plunge (following well-covered reports of a large miss in new subscriber figures)

COMMODITIES: Can The Trend In Commodity Prices Persist Despite Weakening Global Demand?

Executive summary

- Investors have been questioning if the trend in commodity prices could persist in the medium term as global demand keeps weakening and a growing range of ‘fundamental’ indicators keep pricing in ‘cheaper’ commodities.

- Commodity prices have been mainly supported by the global supply chain disruptions and the investment narrative with market participants seeking for ‘inflation-hedges’.

In the past few months, we have seen that commodity prices have been constantly reaching new highs while global demand has been significantly weakening. Part of the weakening in global demand has been attributed to the sharp deceleration in Chinese economic activity amid ‘zero-Covid’ policy (which keeps weighing on growth expectations). The chart below shows the strong divergence between China imports (YoY), which have fallen to -0.1% in March (down from over 30% YoY in November last year) and the annual change in commodity prices (BCOM index). As China represents over 50% of the total demand for some commodities (i.e. copper), the two times series have historically strongly co-moved together in the past 20 years.

Two main factors could explain that divergence:

- Global supply chain disruption (Covid, severe droughts in Latam and more recently the Ukraine war shock).

- The investment narrative with participants looking for ‘inflation hedges’ as inflation keeps surprising positively (commodities have historically been good ‘inflation hedges).

Can the divergence persist in the medium term?

Sentiment on commodities is ‘strongly bullish’, global demand is weakening and some investors are speculating that inflation peaked in March.

Source: Bloomberg/MNI.

GOLD: Lower As U.S. 10-Year Real Yields Reach Positive Territory

Gold is ~$4/oz worse off to print $1,946/oz at writing, a little above fresh one-week lows made earlier in the session.

- The precious metal operates around the bottom of Tuesday’s range, coming under pressure as U.S. real yields have moved higher in Asia-Pac dealing, with U.S. 10-Year real yields briefly turning positive for the first time since early ‘20. Looking to cash Tsys, nominal 10-Year Tsy yields hit session highs at ~2.98%, reaching levels last witnessed in end-2018.

- To recap Tuesday’s price action, gold closed ~$29/oz softer for its sharpest daily loss in three weeks. The move lower was facilitated by a broad surge in U.S. real yields and the USD (DXY), with the latter recording fresh cycle highs after briefly showing above 101.00 for the first time since Mar ‘20.

- Up next, Fedspeak from Daly (‘24 voter), Evans (‘23 voter), and Bostic (‘24) is due during the NY session, although the latter is noted to be speaking on the topic of equity in urban development.

- Slightly further out, Fed Chair Powell is due to speak on Thursday, in his final scheduled public appearance before the pre-meeting blackout period for the May FOMC.

- From a technical perspective, gold has broken initial support at the 20-Day EMA at ~$1,951.6/oz, exposing further support at ~$1,924.2/oz (50-Day EMA).

OIL: A Little Higher In Asia; Growth Worry Takes Focus Over Crude Supply Woes

WTI and Brent are $1.20 firmer apiece at typing, operating a touch above Tuesday’s troughs as debate re: the impact of lower global economic growth on energy demand does the rounds in Asia.

- To recap, both benchmarks shed between $5.50 to $6.00 on Tuesday as worry re: demand destruction arising from lower economic growth in ‘22 helped ease lingering crude supply constraint fears from extremes seen earlier in the year.

- On that topic, the International Monetary Fund (IMF) slashed global economic growth forecasts for ‘22 by 0.8% on Tuesday (4.4% to 3.6%), compounding growth fears (keeping in mind continued worry surrounding the COVID outbreak in China) after the World Bank’s 0.9% downgrade on Monday (4.1% to 3.2%), with both organisations citing Russia’s invasion of Ukraine as a primary driver of the downgrade.

- Elsewhere, RTRS source reports pointed to OPEC+ producing 1.45mn bpd below production targets in March, with Russian crude output reportedly falling 300k bpd short of target, suggesting that well-documented worry re: buyer self-sanctioning and sanctions may be taking effect.

- Turning to the U.S., the latest round of API inventory estimates crossed late on Tuesday, with reports pointing to a surprise drawdown in crude inventories, unwinding some of the build reported last week. An increase in gasoline and Cushing stocks was reported as well, while a drawdown was observed in distillate stockpiles.

- EIA data is due later on Wednesday (1430 GMT), with WSJ estimates calling for a build in U.S. crude inventories, while drawdowns are expected to be seen in gasoline and distillate stockpiles.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/04/2022 | 0600/0800 | ** |  | DE | PPI |

| 20/04/2022 | 0845/0945 |  | UK | BOE Mutton Panelist on Central Bank Digital Currencies | |

| 20/04/2022 | 0900/1100 | ** |  | EU | industrial production |

| 20/04/2022 | 0900/1100 | * | | EU | Trade Balance |

| 20/04/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 20/04/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 20/04/2022 | - | | EU | ECB Lagarde & Panetta in IMF/World Bank Meetings | |

| 20/04/2022 | - | | EU | ECB Lagarde & Panetta at G7 &G20 Finance Ministers' Meetings | |

| 20/04/2022 | 1230/0830 | *** |  | CA | CPI |

| 20/04/2022 | 1400/1000 | *** | | US | NAR existing home sales |

| 20/04/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 20/04/2022 | 1430/1030 | | US | Chicago Fed's Charles Evans | |

| 20/04/2022 | 1430/1030 | | US | San Francisco Fed's Mary Daly | |

| 20/04/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 20/04/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 20/04/2022 | 1700/1300 | | US | Atlanta Fed's Raphael Bostic | |

| 20/04/2022 | 1800/1400 | | US | FOMC Beige Book | |

| 21/04/2022 | 2245/1045 | *** |  | NZ | CPI inflation quarterly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.