Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The early risk-positive feel surrounding China's latest move to support the property sector, coupled with confirmation that Shanghai will restart it's gradual re-opening process today, was quickly reversed on the back of softer than expected Chinese economic activity data, which magnified any disappointment surrounding PBoC inaction in its latest round of MLF operations (net neutral in liquidity terms and no change in the interest rate applied to use the facility).

- Goldman Sachs downgraded its '22 & '23 U.S. GDP growth forecasts, while the bank also marked its year-end target for the S&P 500 lower.

- The global data docket is very light during the remainder of the day, with central bank speak set to fill the gap. Comments are due from Fed's Williams, ECB's Villeroy, Lane & Panetta, BoE's Bailey, Ramsden, Haskel & Saunders as well as Riksbank's Ingves.

US TSYS: Bid After Two-Way Asia Trade Ultimately Dominated By Soft Chinese Economic Data

Chinese matters were front and centre for broader risk appetite during Asia-Pac dealing, with TYM2 last +0-08+ at 119-14, 0-04 off the peak of its 0-16+ range, on relatively limited volume, given the price swings, of ~115K, with activity a little limited by the observance of the Vesak Day holiday in several Asia-Pac countries (most notably Singapore), Meanwhile, the cash Tsy curve has flattened, with the major benchmarks running 0.5-2.0bp richer on the day, led by 10s.

- The early, positive mood music that surrounded weekend news which revealed the latest move on the part of Chinese authorities re: stimulating the property market (although analysts have questioned the efficacy of a lower mortgage rate floor for first time buyers), coupled with confirmation that Shanghai will start to gradually re-open from today, quickly vanished on the back of softer than expected Chinese economic activity data, which magnified any disappointment surrounding PBoC inaction in its latest round of MLF operations (net neutral in liquidity terms and no change in the interest rate applied to use the facility).

- Note that the aforementioned weekend news flow had allowed wider markets to look through Goldman Sachs downgrading its U.S. economic growth projections and year-end target for the S&P 500 during early Asia dealing.

- Empire manufacturing data and Fedspeak from NY Fed President Williams headline the NY docket on Monday.

JGBS: Contained Tokyo Trade, Following Wider Swings In Risk Appetite

JGBs meandered through Tokyo dealing, trading with a low beta to the wider swings in the wider risk backdrop (as is the norm). As a result, JGB futures initially showed lower vs. late overnight session levels, before recovering (see other bullets for more colour on the China-driven nature of broader risk appetite), last dealing +3. Cash JGB trade has been very limited, with the major cash JGB benchmarks running -/+0.5bp vs. Friday’s closing levels.

- There hasn’t been much in the way of notable domestic headline flow to assess since the Tokyo re-open, leaving wider swings in risk appetite in the driving seat.

- Note that the weekend saw Nikkei sources report that the Japanese government will use deficit-financing bonds to cover Y2.7tn of extra spending under a supplementary budget, as it looks to shield consumers and businesses from the well-documented global inflationary pressures. The article suggested that the government plans to formally decide on the spending decision on Monday, with a view to the stimulus being passed in the current parliamentary session.

- Note that domestic PPI data topped expectations (+10.0% Y/Y vs. BBG median +9.4%) and may have fed into the early, limited downtick in the JGB space.

- 10-Year JGBi supply came and went without much fuss, passing smoothly enough, with no lasting, tangible reaction in breakevens as the cover ratio moderated a touch vs. prev. auction levels.

AUSSIE BONDS: Flatter, All Things China In The Driving Seat

Aussie bond futures were better bid than their U.S. counterparts during early Sydney dealing, even as wider risk assets benefitted from the latest supportive steps drawn up for the Chinese property market (analysts have questioned the impact that the move will have) & confirmation that Shanghai will start (gradually) easing COVID restrictions from today. That was before the wider, China- inspired defensive flows provided some fresh support for the space, with the longer end leading the bid.

- The pace has since eased back from best levels, akin to the move in U.S. Tsys, leaving YM +0.5 & XM +4.0 at typing. Cash ACGB trade sees 30s outperform, richening by ~5bp as of typing.

- The 3-/10-Year EFP box has twist flattened on the day.

- Note that the IR strip has also seen some twist flattening, with contracts running -1 to +3 through the reds. 3-month BBSW set ~3bp higher today, which helped the front end underperform.

- While the ruling coalition’s property policy proposals garnered plenty of headline interest they weren’t seen as a meaningful driver for the ACGB space. A quick reminder that the ruling coalition trailed the opposition Labor Party in the most recent opinion polls, with the Federal election set to take place on 21 May.

- Looking ahead, the minutes of the RBA’s most recent monetary policy decision are set to headline domestic matters on Tuesday. They will be combed for any guidance re: the future path of tightening after the RBA surprised markets with a 25bp hike in May, although the deluge of communique that dropped around and after the May decision may limit the scope for surprise.

FOREX: Bleak Chinese Activity Data, PBOC In/Action Knock Risk On Its Head

PBOC inaction on the MLF front & dismal economic activity data released out of China triggered risk-off flows across G10 FX space, despite the earlier positive reception of headlines surrounding Shanghai COVID-19 situation. Industrial output unexpectedly shrank in April, reflecting the cost of China's strict virus containment measures.

- The PBOC trimmed the mortgage rate for first home buyers to 4.4% over the weekend, but refrained from cutting the interest rate applied to its 1-Year MLF operations, disappointing some market participants.

- Weak bias in the yuan fixing was very marginal but ended a run of nine consecutive stronger than expected fixings.

- Spot USD/CNH reversed initial losses on disappointment with PBOC inaction/yuan fix and posted another upleg upon the release of soft Chinese activity data.

- It was a rags-to-riches session for the yen, which tops the G10 scoreboard as we type. Regional risk barometer AUD/JPY pulled back sharply after a brief look above the Y90.00 figure, as the Aussie dollar led losses in G10 FX space.

- The global data docket is very light during the remainder of the day, with central bank speak set to fill this gap. Comments are due from Fed's Williams, ECB's Villeroy, Lane & Panetta, BoE's Bailey, Ramsden, Haskel & Saunders as well as Riksbank's Ingves.

FOREX OPTIONS: Expiries for May16 NY cut 1000ET (Source DTCC)

- AUD/USD: $0.6880(A$696mln)

- USD/CAD: C$1.3000-15($637mln)

- USD/CNY: Cny6.8485($1.5bln)

ASIA FX: Sentiment Sours On Lead From China

China headline flow set the tone for the region, resulting in the unwinding of initial risk-on moves. The Asia EM FX space started the session on a firmer footing, as Shanghai authorities eased some COVID-19 restrictions and the PBOC trimmed the mortgage rate for first home buyers to 4.40%. Sentiment soured as the PBOC disappointed some participants by failing to take action on the MLF front (both in terms of the interest rate and net injection) and ending a streak of nine firmer than expected yuan fixings. This was followed by a set of below-forecast Chinese economic activity indicators, which failed to meet even the already low expectations.

- CNH: Offshore yuan reversed initial gains and retreated, driven by aforementioned dynamics. The surprise annual contraction in China's industrial output may have spooked regional currency bulls, owing to its correlation with the ADXY Index over the recent months.

- KRW: Spot USD/KRW worked its way through opening losses and is back to virtually neutral levels. The China impulse diverted attention from domestic affairs, with South Korea's top economic officials pledging coordinated response to any instability in the FX market. Meanwhile, BoK Gov Rhee refused to rule out an outsized 50bp rate hike at this stage.

- PHP: China headlines prompted the peso to swing to a loss, even as BSP data showed that the Philippines' overseas cash remittances grew faster than expected in March.

- Markets in Singapore, India, Indonesia, Malaysia and Thailand were closed.

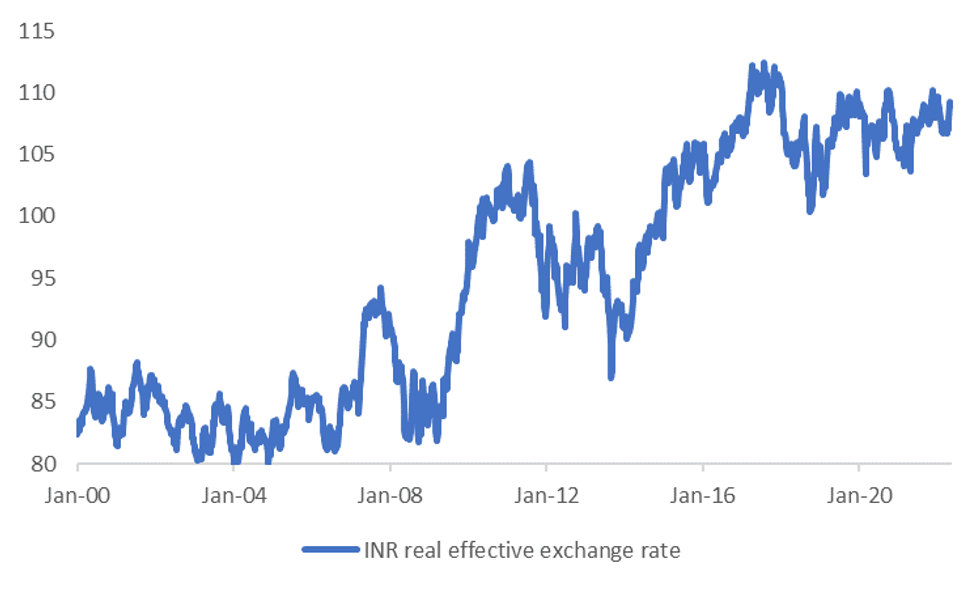

INR: Rupee Reprieve Could Prove Temporary

Spot USD/INR stabilized last week around record highs close to 77.50, following reports that the Indian authorities were intervening in the FX market. However, fundamentals still point to meaningful headwinds for the rupee.

- It's difficult to make the case the INR is cheap from a long term perspective. The first chart below is the INR real effective exchange rate (REER). Current levels sit just below recent cyclical highs and we are only around 3% off record highs.

- A large driver of the elevated REER for INR is the persistently stronger inflation rate in India compared to the rest of the world. Indeed, it has only been in the last 12 months or so that the rest of the world has seen inflation rates on par with those in India. Over the long term the positive CPI differential India has had with the rest of the world has more than offset INR nominal FX depreciation.

Fig 1: INR FX Still Expensive In Real Effective Terms

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

- An expensive currency won't help India's wide trade deficit position, which sits close to historical lows. Exports could also be hurt by lower wheat exports following the weekend announcement. To recap, India's government announced it will ban wheat exports for food security reasons, although exports will still be allowed to countries that require it for their own food security and at the request of governments.

- Net equity outflows persist from offshore investors as well, due to valuation concerns and the RBI's more hawkish turn. Last week saw net outflows of $1.8bn, the largest in EM Asia (outside of China). Outflows from bonds are also evident.

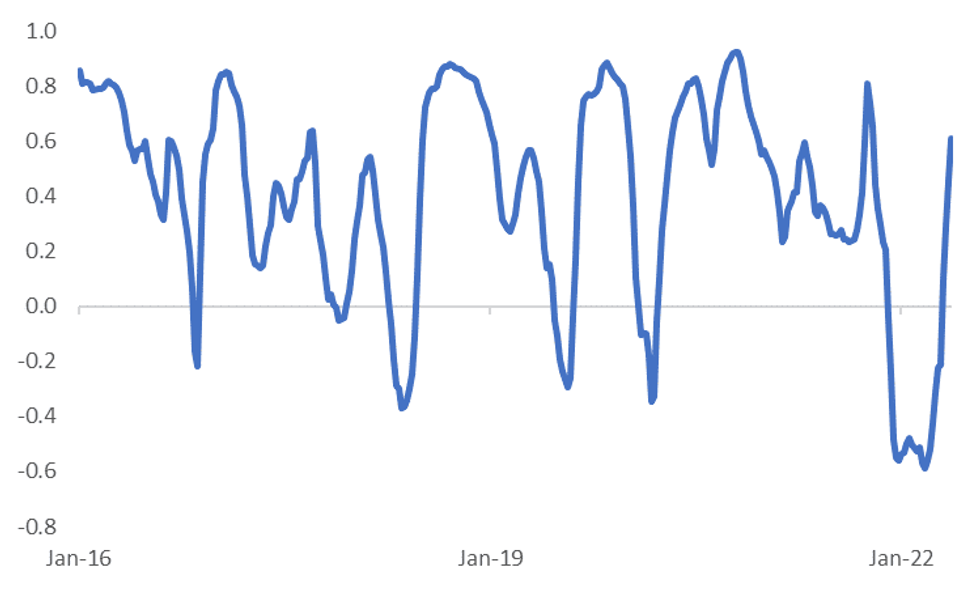

- USD/INR's correlation with USD/CNY is also trending back up, see the chart below. So higher USD/CNY levels should bias USD/INR higher, all else equal.

- The RBI maintains a very large pool of FX reserves of just under $600bn. However, we doubt the central bank will defend 'a line in the sand' with USD/INR, but rather manage the pace of depreciation.

Fig 2: USD/INR And USD/CNY Rolling Correlation (6mth Window)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

EQUITIES: Easy Come, Easy Go

The early positive mood music that surrounded weekend news which revealed the latest move on the part of Chinese authorities re: stimulating the property market, coupled with confirmation that Shanghai will start to gradually re-open from today, quickly vanished on the back of softer than expected Chinese economic activity data, which magnified any disappointment surrounding PBoC inaction in its latest round of MLF operations (net neutral in liquidity terms and no change in the interest rate applied to use the facility).

- Note that the aforementioned weekend news flow had allowed wider equity markets to look through Goldman Sachs downgrading its U.S. economic growth projections and year-end target for the S&P 500 during early Asia dealing.

- A positive lead from Wall St., after the S&P 500 rose by over 2.0% on Friday, also factored into early price action.

- The above moves leave the major regional equity indices in mixed territory, with the Nikkei 225 (+0.5%) and ASX 200 (+0.3%) higher on the day, while the Hang Seng (-0.4%) & CSI 300 (-0.8%) are lower, with the China-centric nature of market drivers resulting in losses.

- E-minis are 0.4-0.6% lower, with the NASDAQ 100 contract leading losses. The S&P 500 contract is back below 4,000.

GOLD: Meandering Through Asia Dealing

Gold has meandered through Asia-Pac dealing, with the relatively widespread observance of the Vesak Day holiday limiting liquidity during regional trading hours, leaving spot little changed, just above $1,810/oz. This comes after general risk-positive price action pressured gold on Friday.

- Bullion has shown little reaction to the respective bouts of risk-positive and risk-negative price action witnessed thus far.

- Note that our weighted U.S real yield monitor operates a little shy of its recent cycle highs.

- Our technical analyst has noted that gold remains vulnerable - Wednesday's move lower confirmed a resumption of the current downtrend. Bears now target a sustained break of psychological support (1,800/oz), after a brief and limited show below on Friday. This would allow them to focus on the Jan 28 low ($1,780.4/oz).

OIL: Ultimately Lower In Two-Way Asia Session

Oil swung with wider risk sentiment during Asia-Pac hours, with WTI & Brent last printing ~$1.50 softer than their respective settlement levels.

- The initial positive mood surrounding the weekend declaration of the gradual re-opening of the Chinese city of Shanghai has reversed after any disappointment surrounding PBoC inaction re: its latest round of MLF operations was magnified by much softer than expected Chinese economic activity data for the month of April, pressuring crude.

- Oil-specific weekend news flow was headlined by Iran talking up its ability to double exports, assuming there is sufficient demand, while the Iraqi government suggested that forces from the regional Kurdish government took control of some oil wells in the Kirkuk region (although the Kurdish authorities denied such a move had taken place).

- A quick reminder that Friday saw WTI & Brent crude add over $4.00 apiece, with buoyant equity markets, hope surrounding the aforementioned re-opening of Shanghai and geopolitical worry surrounding Sweden & Finland’s impending NATO membership applications supporting crude. We also note that Friday saw EC VP Sefcovic stress that the European Union is “very much determined to maintain a united front against Moscow by securing unanimous support for the proposed ban on Russian oil and winning Hungary over,” per the FT.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/05/2022 | 0600/0800 | * |  | DE | Wholesale Prices |

| 16/05/2022 | 0820/1020 |  | EU | ECB Panetta Speech at Digital Euro Event | |

| 16/05/2022 | 0840/1040 | | EU | ECB Panetta & Lane in Discussion on Digital Euro | |

| 16/05/2022 | 0900/1100 | * | | EU | Trade Balance |

| 16/05/2022 | 0900/1100 | | EU | EC Spring Economic Forecasts | |

| 16/05/2022 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 16/05/2022 | 1230/0830 | ** |  | US | Empire State Manufacturing Survey |

| 16/05/2022 | 1255/0855 | | US | New York Fed's John Williams | |

| 16/05/2022 | 1300/0900 | * | | CA | Home Sales – CREA (Canadian real estate association) |

| 16/05/2022 | 1400/1500 |  | UK | BOE TSC to discuss May MPR | |

| 16/05/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 16/05/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 16/05/2022 | 2000/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.