Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

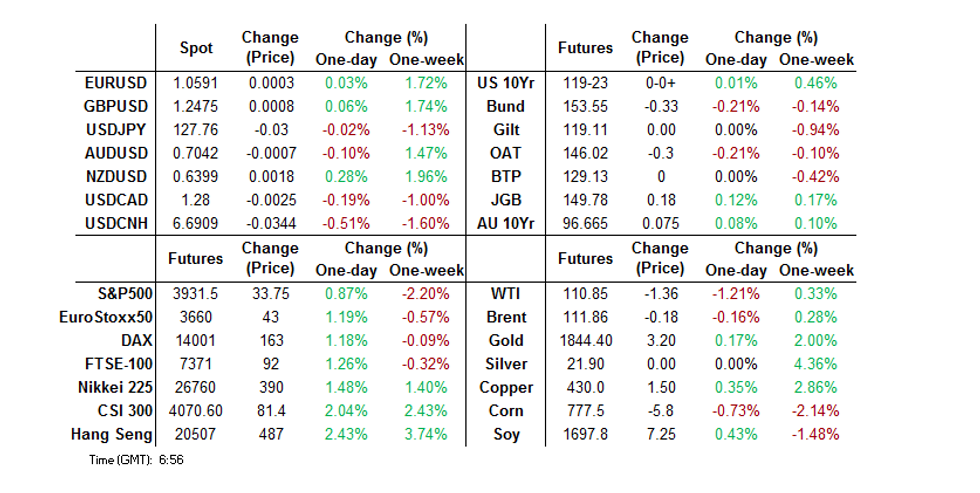

- Tsys unwound the cheapening impulse that came on the back of the latest Chinese 5-Year LPR fixing moving 15bp lower (consensus looked for a 5bp cut), with the move aimed at supporting the Chinese property sector. There wasn’t an overt reason for the uptick from session cheaps, with wider risk assets underpinned and a lack of major risk-negative headline flow evident.Note that earlier in the session we had some mixed headlines re: the COVID situation in the Chinese city of Shanghai (reopening plans for the financial district of Pudong were outlined vs. 3 COVID cases being detected outside of the city’s quarantine facilities).

- USD/CNH pulls lower in Beijing afternoon.

- UK retail sales & Eurozone consumer confidence will take focus today. Comments are due from ECB's Muller, Kazaks, Simkus, Centeno, de Cos as well as BoE's Pill. We will also see St. Louis Fed President Bullard ('22 voter) via an interview with Fox business.

US TSYS: Off Lows Even As China LPR Move Supports Equities

TYM2 last deals +0-02 at 119-24+, 0-03 shy of the peak of the 0-10+ Asia-Pac range, on volume of ~100K. Benchmark cash Tsys run 1bp cheaper to 1bp richer as the curve twist flattens, pivoting around 10s.

- Tsys unwound the cheapening impulse that came on the back of the latest Chinese 5-Year LPR fixing moving 15bp lower (consensus looked for a 5bp cut), with the move aimed at supporting the Chinese property sector. There wasn’t an overt reason for the uptick from session cheaps, with wider risk assets underpinned and a lack of major risk-negative headline flow evident.

- Note that earlier in the session we had some mixed headlines re: the COVID situation in the Chinese city of Shanghai (reopening plans for the financial district of Pudong were outlined vs. 3 COVID cases being detected outside of the city’s quarantine facilities).

- A Fox Business interview with St. Louis Fed President Bullard headlines domestically on Friday.

JGBS: A Firm End To The Week

JGB futures initially eased from late overnight levels on the back of slightly firmer than expected national core CPI data, although the move back from lows didn’t take long, probably given the focus on previous BoJ rhetoric, which foretold such a move (in rough absolute terms), while the Bank has played down the need to tweak its policy settings given the cost-push nature of the currently inflationary impulse (in addition to technicalities surrounding mobile phone charges). The BoJ remains focused on facilitating a rebound in economic growth and fostering an environment that will generate sustained underlying inflationary pressure.

- Futures then nudged higher through the remainder of the morning, before the previously outlined uptick from session cheaps for U.S Tsys provided support in the afternoon.

- A reminder that the BoJ’s continued presence in the market as it enforces its YCC conditions is seemingly limiting any sell offs in paper out to 10s at present.

- The latest round of 20-Year JGB supply came in on the firmer side and likely aided the bid further, with the cover ratio moving higher (topping the 6-auction average of 3.34x), price tail narrowing to a much more normal level vs. what was seen at the previous 20-Year auction and low price topping wider expectations. Stabilisation of the wider core global FI space, short covering and lifer demand likely resulted in the smooth passage of supply (factors we flagged in our auction preview).

- JGB futures last print +22, just off best levels, with cash JGBs running little changed to ~2.5bp firmer. 7s and the super-long end lead the bid, with 7s benefitting from the move in futures and the super-long end rallying in the wake of supply.

- In terms of flows, note that BBG headlines covering the monthly JSDA data pointed to foreign funds selling the largest monthly amount of 10-Year JGBs on record in April, while major domestic banks bought the largest amount of 10-Year JGBs since ’14 during the month, once again, per BBG headlines.

- Looking ahead to next week, Tokyo CPI headlines the domestic docket (Friday), with 40-Year JGB supply (Thursday) and the usual BoJ Rinban & fixed rate operations also due.

AUSSIE BONDS: Tight, Pre-Election Trade

Aussie bond futures have been happy to hug tight ranges, generally tracking gyrations in risk sentiment, with participants on the sidelines ahead of the weekend, filtering through news re: domestic political matters. That leaves YM +6.0 and XM +8.5 at typing, with the contracts never straying too far from late overnight levels during the first half of Sydney trade. 10s provide the firmest point on the wider cash ACGB curve. EFPs are a touch tighter today, with the 3-/10-Year EFP box flattening. Bills run 2-9bp firmer through the reds.

- A quick reminder that the Federal election that will take place over the weekend. It isn’t expected to be too much of a market moving event given the lack of meaningful policy differentiation observed between the ruling coalition and opposition Labor Party. The ruling coalition has narrowed the gap to the opposition during the run in, although most projections still point towards a slim majority for Labor when the dust settles (read more on the matter in our full preview of the event)

- Some still pointed to election risk as a headwind for the ASX & AUD on Friday. On this front, we would suggest that a hung parliament outcome (which may require some form of Labor-Green power sharing agreement) would provide much more uncertainty than a win for the opposition Labor Party (which the opinions polls currently lean towards) or the ruling coalition.

- On the supply side, market stabilisation, a digestible DV01, as well as the recent demand for access the line as seen in the RBA’s SLF mechanism in recent days and the relative rarity when it comes to taps of the line seemed to combine to result in a well-received round of ACGB Apr-27 supply. The weighted average yield printed 1.22bp through prevailing mids (per Yieldbroker), with the cover ratio comfortably above 3.00x (very solid in post-QE times). Next week’s AOFM issuance slate sees the AOFM revert to a combination of 10- & 30-Year basket issuance.

Drawing Parallels With The '10 Election

The AUD continues to lag the risk on tone in markets, which is particularly evident in equities. AUD/USD is up from the lows, but is still down 0.30% from the NY close. Some of the underperformance is being attributed to uncertainty around this weekend's election result.

- Arguably the greatest uncertainty for markets rest with a hung parliament result, where neither party can form a majority and have to rely on minor parties to from government.

- The tightening of opinion polls over the past week has seen this risk rise. One possibility is the Labor Party relying on Greens support to form government. This probably creates the most policy uncertainty in terms of what concessions the Labor party needs to make to ensure it can pass legislation.

- There are some parallels with the 2010 election, where neither party had an outright majority and Labor needed to rely on the support of independents to form government.

- This election was held on August 21 2010, which was a Saturday. AUD/USD closed the Friday before at 0.8939. We closed Monday the 23rd of August at 0.8913, although did have an intra-day low of 0.8833. The DXY was higher on the day as well, which could have impacted A$ performance.

- AUD/USD was weaker through Tues/Wed of that week, but again the USD was firmer through this period. Australian equities also fell, but recovered strongly into early September. Likewise for the AUD, which was at fresh highs by the start of September that year. By early September it was also clear that the Labor party would form government with the support of the independents.

- Hence the 2010 election didn't have a lasting impact on market sentiment.

FOREX: Aussie Dollar Lags, Greenback Shakes Off Weakness

The Aussie dollar went offered, lagging better risk sentiment, amid positioning ahead of this weekend's federal election. This week's opinion polls have shown the race tightening, with the prospect of a hung parliament likely putting some participants on the defensive. On the eve of the election day, the opposition Labour party remains ahead of the ruling Liberal/National Coalition, but PM Morrison could still replicate his upset victory from last election, while a minority Labour administration propped up by the Greens could lead to policy instability.

- NZD/USD is on track to register its first weekly gain after seven consecutive weeks of losses. All key data ahead of next Wednesday's RBNZ monetary policy meeting have been released, leaving market participants to digest available signals.

- There was good demand for CHF, which sits atop the G10 pile. Regional reaction to remarks from SNB Pres Jordan may have facilitated the move, after the official flagged a sense of concern with price pressures.

- The greenback traded on a firmer footing, aided by an uptick in U.S. Tsy yields.

- The yen firmed even as it is a Gotobi Day today.

- UK retail sales & EZ consumer confidence will take focus later in the day. Comments are due from ECB's Muller, Kazaks, Simkus, Centeno, de Cos as well as BoE's Pill.

EURUSD: Breaches The 20-Day EMA

- RES 4: 1.0866 Bear channel resistance drawn from the Feb 10 high

- RES 3: 1.0758 Low Apr 14 and a recent breakout level

- RES 2: 1.0642 High May 5 and key short-term resistance

- RES 1: 1.0607 High May 19

- PRICE: 1.0573 @ 06:05 BST May 20

- SUP 1: 1.0461/350 Low May 18 and19 / Low May 13 and bear trigger

- SUP 2: 1.0341 Low Jan 3 2017 and a key support

- SUP 3: 1.0333 1.236 proj of the Feb 10 - Mar 7 - 31 price swing

- SUP 4: 1.0288 2.0% 10-dma envelope

EURUSD traded higher Thursday and breached resistance at the 20-day EMA. The average intersected at 1.0569 and the move above this level suggests scope for a stronger short-term recovery. This has opened the next key resistance at 1.0642, the May 5 high. Note that the recent bounce from 1.0350, May 13 low, also marks a recovery from the base of a bear channel, drawn from the Feb 10 high. Initial support is at 1.0461, May 18/19 low.

EQUITIES: Better Bid In Asia As Chinese 5-Year LPR Lowered

A larger than expected cut in the latest Chinese LPR fixing, aimed at boosting support for the property sector, facilitated a bid in the major Asia-Pac regional indices ahead of the weekend, even with mixed headlines coming out of Shanghai re: COVID (reopening plans for the financial district of Pudong were outlined vs. 3 COVID cases being detected outside of the city’s quarantine facilities). Elsewhere, risk assets may have benefitted from White House suggestions that Presidents Biden & Xi could speak again, within weeks.

- This leaves the major regional equities up 1-2% at typing, with the ASX 200 slightly lagging vs. its regional counterparts. Some pointed to election risk as a headwind for the ASX, with Australia set to head to the voting booths on saturday. On this front, we would suggest that a hung parliament outcome (which may require some form of Labor-Green power sharing agreement) would provide much more uncertainty than a win for the opposition Labor Party (which the opinions polls currently lean towards).

- E-minis are 0.7-1.1% better off, with the NASDAQ 100 leading.

GOLD: On Course To Break Run Of Weekly Losses

A limited round of Asia-Pac dealing leaves spot gold little changed around $1,840/oz, with bullion on track to break a 4-week run of weekly losses after a lower USD and general worries re: the wider growth outlook/stagflation provided support on Thursday. Familiar technical lines in the sand remain in play.

OIL: Overnight Downtick

WTI & Brent have shed a little over $1.00 apiece vs. their respective settlement levels. The final Asia-Pac session of the week provided mixed headlines when it came to the Chinese COVID situation, with Shanghai unveiling the initial return to work limitations for the financial district of Pudong, while the city also discovered 3 COVID cases outside of quarantine facilities (with little in the way of official communique surrounding the matter evident).

- Crude markets experienced a degree of two-way price action given the lack of meaningful fundamental news flow evident during overnight trade.

- As a reminder, Thursday saw confirmation that the G7 were discussing a potential price cap for Russian oil via secondary sanctions, although no further details were forthcoming.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/05/2022 | 0600/0800 | ** |  | DE | PPI |

| 20/05/2022 | 0600/0700 | *** |  | UK | Retail Sales |

| 20/05/2022 | 0730/0830 | | UK | BOE Chief Economist Huw Pill speech | |

| 20/05/2022 | - |  | EU | ECB Lagarde & Panetta in G7 Meeting | |

| 20/05/2022 | 1200/1400 | | EU | ECB Lane in Discussion at Stockholm Uni | |

| 20/05/2022 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 20/05/2022 | 1400/1000 | * |  | US | Services Revenues |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.