Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

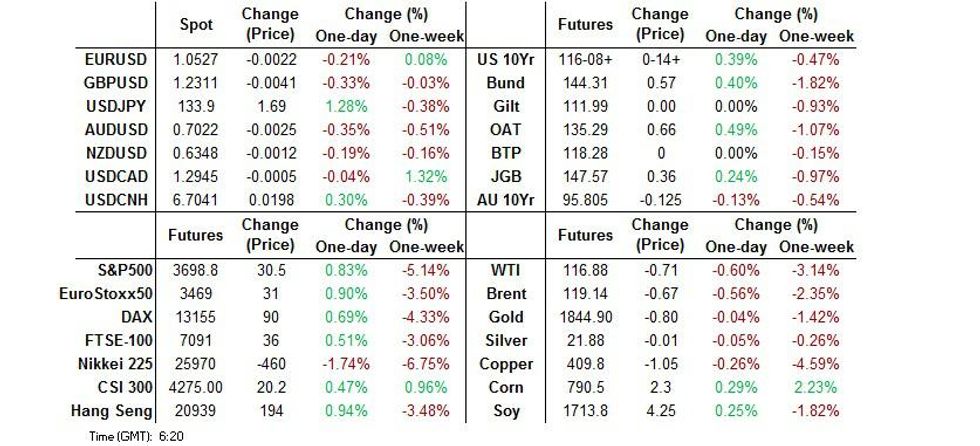

- The BoJ defies the global tightening trend and stands pat on its ultra-loose monetary policy settings, albeit it includes a rare reference to FX markets in the statement. BoJ Governor Kuroda is yet to hold his press conference. Yen slides after the BoJ decision, while 10-Year JGB yield returns into its permitted trading band, as Japan's central bank signals readiness to keep enforcing its YCC framework.

- T-Notes and Aussie bonds come under pressure as U.S. e-minis creep higher. A strong auction for A$1.0bn of ACGB May '32 provides only brief reprieve to Australian FI space

- Greenback catches bid on the back of strong demand for USD/JPY. Aussie dollar slips as regional equity markets take their cue from Thursday's Wall Street rout.

US TSYS: T-Notes Stay On Softer Footing Even As BoJ Comes To Rescue

Selling pressure hit T-Notes as trading got underway in Asia, with the contract extending its pullback from Thursday's peak (116-21). Recovery in U.S. e-mini futures was deemed risk-supportive, sapping strength the Treasuries.

- The slide in T-Notes was stopped by the BoJ, who announced their monetary policy decision. Despite the market testing the resolve of Japan's central bank over the past week, officials stood the course and stuck with their super-loose policy settings, familiar forward guidance and assessment of the economy, although they tipped hat to the need to watch financial and FX markets. Resultant bounce in JGB futures supported T-Notes, which moved away from their session low of 115-28+.

- TYU2 last trades +0-13 at 116-07, while Eurodollar futures run 1.5-5.0 ticks higher through the reds. Cash curve bear flattened in Tokyo trade, with yields last 4.4-6.2bp higher. The spread between 5-/30-Year Tsy yields moved towards zero, but lacked the impetus to turn positive.

- Looking ahead, Fed Chair Powell will speak at the Dollar Conference today, while local data highlights are limited to industrial output.

JGBS: JGBs Extend Rally After BoJ Reaffirms YCC Parameters, 10-Year Yield Returns To Target

JGB futures re-opened sharply higher after the Tokyo lunch break, during which the BoJ demonstrated its steadfast commitment to persistent powerful monetary easing. The contract returned from the trading pause at a new session high of 147.78 before trimming gains.

- The past week saw a tug-of-war between the BoJ and market participants questioning the sustainability of its firm grip on the yield curve, even as local analysts expected the Bank to stand pat today.

- JGB futures crept higher in the lead-up to the policy announcement, with the upswing possibly facilitated by comments from FinMin Suzuki, who said he hopes the BoJ will persist in efforts towards achieving its inflation target.

- The Policy Board indeed maintained its YCC settings, forward guidance and overall assessment of the economy despite recent yen weakness and growing pressure on the 0.25% cap on 10-Year yield.

- The yield on 10-Year JGBs rose to the highest level since 2016 this morning, with the Bank conducting another round of unlimited fixed-rate debt purchases in the afternoon.

- But the decision to stick with ultra-loose monetary policy stance dragged benchmark 10-Year yield back into the target range and it last sits at 0.22%.

- The 7-10-Year sector covered by the Bank's daily bond-purchase operations outperforms on the cash curve, with yields mostly lower as we type, save for the super-long end. JGB futures have stabilised trade at 147.45, 24 ticks above previous settlement.

- All eyes are on the press conference with BoJ Gov Kuroda this afternoon.

AUSSIE BONDS: Cheapening Pressure Prevails Despite Strong ACGB Auction, BoJ's Dovish Resolve

Selling pressure spilled over from U.S. Tsys into ACGBs, although a solid ACGB May '32 auction & fallout from the BoJ's policy meeting helped reduce losses for Aussie bonds.

- U.S. Tsys were dumped from the off, correcting Thursday's rally, as upticks in U.S. e-mini futures indicated that the local equity space may get some reprieve. Aussie bonds clung to the coattails of Tsys, trading with a heavier bias through the session.

- A strong auction for A$1.0bn of ACGB May '32 prompted ACGBs to briefly pop higher, as one successful bidder took the whole amount on offer, reducing the price tail to zero. Based on our quick calculations, the last time when a single buyer snapped all of ACGBs on offer was in Sep 2020. Excluding two 2020 sales, when single buyers managed to purchase A$2.0bn of auctioned bonds each time, today's was the largest amount bought by a lone bidder on record.

- ACGBs resumed losses but took another brief breather as the BoJ announced its monetary policy decision, keeping all ultra-loose settings and broader rhetoric unchanged. Resultant bid in JGBs spilled over into the broader core FI space.

- When this is being typed, YM trade -10.5 & XM -13.5, with bills sitting 4-10 ticks lower through the reds. Cash curve runs steeper, with yields last 9.5-16.5bp higher.

FOREX: Yen Tumbles As BoJ Chooses To Remain World's Dovish Dissenter

The BoJ dispelled the doubts and reaffirmed its ironclad commitment to ultra-loose monetary policy, keeping all YCC parameters, overall assessment of the economy and forward guidance unchanged. In an unusual move, the Bank underlined the need to "pay due attention to developments in financial and foreign exchange markets and their impact on Japan's economic activity and prices." Yet this laconic commentary on FX matters fell well short of some of the more aggressive remarks issued by Japanese financial officials in the recent weeks.

- The yen began tumbling ahead of the BoJ's announcement amid continued assessment of the sustainability of the Bank's dovish stance. FinMin Suzuki's remark that he hopes policymaker would continue to work towards their inflation target appeared to have cooled the enthusiasm of some yen bulls.

- Spot USD/JPY whip-sawed after the announcement, running as high as to Y134.63, before retracing to its current levels. The pair last deals +186 pips at Y134.07 (and climbing), with the yen still comfortably underperforming all of its major peers.

- Looking into the options space, as might have been expected, USD/JPY implied volatilities pulled back sharply across the curve, while 1-month risk reversal soared off its lowest levels since March 2020.

- Demand for USD/JPY boosted the greenback, allowing it to take a breather after Thursday's sell-off and land atop the G10 scoreboard. Firmer U.S. Tsy yields amplified buying pressure.

- The Antipodeans struggled for any topside impetus as most regional equity benchmarks slipped on a negative lead from Wall Street, while crude oil traded on a softer footing.

- The focus now shifts to Gov Kuroda's press conference, where he is likely to be quizzed on any potential policy tweaks at the July policy meeting and FX intervention risks.

- Outside of Japan, final EZ CPI, U.S. industrial output & comments from Fed's Powell, ECB's Simkus as well as BoE's Pill & Tenreyro are eyed today.

FOREX OPTIONS: Expiries for Jun17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0425(E561mln), $1.0490-00(E1.7bln), $1.0650(E764mln), $1.0700(E650mln)

- USD/JPY: Y133.00($681mln), Y133.85-00($564mln)

- GBP/USD: $1.2110(Gbp1.3bln)

- EUR/GBP: Gbp0.8630-50(E1.9bln)

- AUD/USD: $0.7000-05(A$638mln)

- USD/CAD: C$1.2885($585mln)

- USD/CNY: Cny6.7000($1.5bln), Cny6.75($2.7bln)

ASIA FX: Most USD/Asia Pairs Higher On USD/JPY Spike

Most USD/Asia pairs have trended higher today, in line with a stronger USD against the majors, particularly the spike in USD/JPY. The Korean won has been a notable outperformer.

- CNH: USD/CNH has broadly followed USD/JPY shifts today, albeit with a beta well below 1. USD/CNH is back above 6.7000, following a late NY session dip sub 6.6800. The fixing bias shifted back to a firmer CNY. China/HK equities have also outperformed the regional sell-off.

- KRW: The won has outperformed, with USD/KRW 1 month falling back below the 1283 level. Korean equities are lower, down by -0.50% at this stage, but this is not as bad as the tech drops recorded overnight. The won's performance is all the more impressive today given the JPY drop and modest CNH weakness.

- INR: USD/INR is holding relatively steady, remaining above the 78.00 level. The 1 month NDF is still being supported on dips below 78.20, we were last at 78.30. Lower than expected monsoon rainfall may delay the planting of crops, although conditions are expected to improve.

- IDR: USD/IDR continues to push higher, with spot through 14800, highs last seen in October 2020. Bond inflow momentum has rolled over once again. Focus is also on next week's BI meeting. With real yields drifting negative the pressure will increase for the central bank to act.

- PHP: Spot USD/PHP is hitting another round-figure ceiling and this time it is PHP53.500. The rate last deals at PHP53.471, little changed on the day. Reminder that the BSP holds its monetary policy meeting next Thursday and its leaders flagged potential for a hike. The question seems to be not whether they raise rates but by how much.

- THB: USD/THB has continued to push higher today, rising a further 0.5% to 35.27. Some carry over from yesterday's large $165mn in net equity outflows has likely weighed. Higher USD/JPY levels will have impacted as well. Late doors on Thursday, one of the seven MPC members denied speculation that the rate-setting panel could hold an emergency meeting soon. BoT's Kanit Sangsubhan noted that the next meeting will be held in August, in line with the schedule.

EQUITIES: Asia Follows Wall St. Lower; Hong Kong, Chinese Equities Outperform

Most Asia-Pac equity indices are worse off at typing, largely tracking a negative lead from Wall St. Hong Kong and Chinese equities bucked the broader trend of losses, continuing their recent outperformance against peers globally.

- The Hang Seng Index outperformed, sitting 0.8% better off after paring opening gains of as much as 1.2%. China-based tech names lead gains (HSTECH: +1.5%), with analysts pointing to an easing in regulatory crackdowns by the Chinese authorities, rising bets for policy support for the COVID-hit Chinese economy (keeping in mind that China May new home price data released yesterday pointed to a decline for a second consecutive month), and rate divergence between the U.S. and China to support optimism in the space.

- The CSI300 trades 0.3% higher, having flipped between gains and losses throughout Asia-Pac dealing. Broad gains in consumer staples and industrials countered relatively shallower losses in healthcare and financials, with large-caps such as Kweichow Moutai (+2.9%) and CATL (+4.2%) leading gains.

- The Nikkei 225 sits 1.6% worse off at typing, with tech-based names and large-caps underperforming amidst evident spillover from weak sentiment in high-beta equities during Thursday’s NY session. Large losses were observed in favoured names such as Softbank Group (-3.4%), Tokyo Electron (-5.1%), and Fujitsu Ltd (-3.9%).

- The ASX200 deals 2.2% lower at writing after plunging to as low as -2.5% after the open, with losses observed across virtually every sub-index. Commodity and tech-based names lead losses, with focus on worry re: economic stagnation evident.

- U.S. e-mini equity index futures sit 0.5% to 0.7% better off at typing, with NASDAQ contracts leading gains. Zooming out, e-minis operate a little above their respective cycle lows made on Thursday (18-month low for S&P500 contracts).

GOLD: Back Towards The 200 Day MA

Golds recent volatility continues, with the precious metal back towards its 200 day MA ($1844). This around 0.70% weaker from NY closing levels.

- The firmer USD trend, with the DXY rebounding 0.65% today to 104.30, is the main driver of gold weakness.

- Whilst much of this is concentrated in terms of the USD/JPY bounce (+1.5% to +134.15), all major currencies are weaker against the USD so far today.

- US yields are also higher following sharp drops in the previous two sessions. The 2yr is back up to 3.15%, around 5bps firmer on the day.

- Gold got close to $1858 late in the NY session. USD weakness, plus sharp falls in US equities were the main drivers.

- US equity futures are higher today, while regional Asia Pacific equity market sentiment remains downbeat for the most part.

- At this stage, gold is tracking 1.5% down for the week, although we are comfortably above the weekly lows of sub $1810.

OIL: On Track To Break Weekly Streak Of Gains Despite Lingering Supply Worry

WTI and Brent are ~$0.60 worse off apiece, operating a little under Thursday’s best levels at typing.

- Both benchmarks are nonetheless on track to end the week lower, snapping a streak of consecutive higher weekly closes (seven weeks for WTI, four weeks for Brent), as a slew of ultimately hawkish central bank decisions from Europe to the Americas this week has brought debate re: recessionary risks (and thus reduced energy demand) to the fore.

- Looking to the Middle East, U.S. Treasury officials on Thursday announced sanctions on Chinese, UAE, and Iranian companies for breach of crude-related sanctions on Iran. The move cratered earlier, scant hopes for the U.S. to ease sanctions on Iranian crude in the face of tight global supplies, seeing WTI and Brent flip to session highs after hitting two-week lows.

- Elsewhere, RTRS source reports have pointed to OPEC+ producing 2.7mn bpd below quotas in May, mainly on well-documented production issues faced by some members, as well as ongoing sanctions on Russian crude.

- Libyan crude production in particular is expected to continue facing issues in June, with the country declaring on Tuesday that output is around 100K - 150K bpd (output in 2021 was ~1.2mn bpd) in the face of the country’s previously-flagged political woes.

- BBG source reports have also pointed to the likelihood of the U.S. introducing a partial ban on fuel exports (currently estimated at ~755K bpd), possibly exacerbating well-documented supply worries in Europe as the Biden administration continues to explore ways to tamp down surging gasoline prices at home.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/06/2022 | 0830/0930 |  | UK | BOE Tenreyro Opens BOE Household Finance Workshop | |

| 17/06/2022 | 0900/1100 | ** |  | EU | Construction Production |

| 17/06/2022 | 0900/1100 | *** | | EU | HICP (f) |

| 17/06/2022 | - | | EU | ECB de Guindos at ECOFIN Meeting | |

| 17/06/2022 | - |  | JP | Bank of Japan policy meeting | |

| 17/06/2022 | 1230/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 17/06/2022 | 1315/0915 | *** |  | US | Industrial Production |

| 17/06/2022 | 1430/1530 | | UK | BOE Pill Panels BOE Household Finance Workshop |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.